An Analysis of CSR on Firm Financial Performance in Stakeholder Perspectives

1

Technology Management, Economics and Policy Program, Seoul National University, Seoul 08826, Korea

2

Graduate School of Technology Management, Kyung Hee University, Yongin 17104, Korea

*

Author to whom correspondence should be addressed.

Sustainability 2017, 9(6), 1023; https://doi.org/10.3390/su9061023

Submission received: 5 April 2017

/

Revised: 9 June 2017

/

Accepted: 9 June 2017

/

Published: 14 June 2017

Abstract

:Sustainable growth can be a source of success for firms. Corporate social responsibility (CSR) is a key tool for sustainable growth. However, should firms invest in CSR without having confidence in the effects and methods of CSR? This study explored the R&D, technology commercialization, and CSR motivation as core competencies that enhance corporate performance through CSR from a normative perspective—the stakeholder’s perspective. The purpose of this study was to investigate both strategic and traditional CSR’s relationships with financial performance based on the confidence in the effectiveness of CSR. Another important objective of this study was to explore management factors that influence strategic CSR. Firms consider R&D and technology commercialization as strategic management factors. Therefore, this study analyzed the influence of these strategic management factors along with CSR motivations, which may influence strategic and traditional CSR.

1. Introduction

Is corporate social responsibility (CSR) really an essential factor for sustainable growth? Sustainable growth is one of the key issues faced by firms, and the importance of this factor is increasing. Today, given that the environment has been affected as technology improves, firms are making various efforts to reinforce competitiveness through change and innovation. With the backdrop of this business environment, CSR is considered a necessary factor for enabling businesses to meet the demands of the changing times as well as achieve sustainable growth. Recently, CSR has become one of the most important business trends for building a firm’s reputation and image. In addition, firms have been considering means of simultaneously pursuing economic profits and contributing toward society to help achieve sustainable growth for some time. The concept of CSR became prominent recently due to the creation of social value through CSR and the growing popularity of strategic CSR.

However, little research has been done to analyze the effects of the demand for CSR in the field of strategic business management. In this paper, we analyze the effects of the relationship between CSR and strategic business management. To create win-win results for strategic CSR, it would be necessary to ensure that both the firm and society acquire shared common value from CSR. The factors of innovation should be used as inputs for creating common value and achieving positive results. Therefore, we discuss how R&D and technology commercialization—two of many input factors of innovation—influence traditional and strategic CSR.

Through our empirical results, we are able to understand the manner in which financial performance is influenced by technology-focused R&D, technology commercialization, and CSR. In addition, the research will help us develop a better understanding of the relationship between CSR and the aforementioned factors. Research on the correlation between each factor suggests a basis for setting the direction of strategic management for the sustainable growth of firms.

2. Theoretical Background

2.1. Corporate Social Responsibility (CSR)

2.1.1. The Definition of CSR and CSR Motivation

Although there are various opinions regarding CSR, they can be summed up broadly as the activities that are conducted by businesses to satisfy societal values and goals, which go beyond the profit motive of the business. Bowen [1] introduced the concept of CSR in business and defined it as the “obligation of businessmen to pursue desirable policies from the perspective of society’s goals and values, and make decisions or conduct business within the context of them”; providing a broader definition, McGuire [2] explains that CSR’s obligations toward society extend beyond economic and legal obligations; Carroll [3] divided CSR into five stages: economic responsibility (maximization of profit), legal responsibility (observation of regulations), ethical responsibility (observation of ethical standards), altruistic responsibility (conducting charitable deeds regardless of profits earned), and final stage includes strategic responsibility (making profits through charitable deeds).

Kim [4] analyzed the internal factors that motivate firms to conduct CSR activities. These factors include the CEO’s willingness to conduct altruistic activities, active communication within the organization, voluntary participation of the employees, financial capacity, and the satisfaction level of the employees. Kim [5] divided the external factors that motivate CSR activities as follows: social atmosphere, understanding social needs, international CSR standards, government incentives, and collaboration with NGO’s. From the perspective of stakeholders, Kim [5] divided factors that motivate CSR into a firm’s internal capacity, hierarchical system, and environmental factors. The internal capacity comprises of the firm’s debt ratio, cash flow, productivity and profitability, and advertising and training expenses; hierarchical systems include shareholders, the CEO, the board of directors, foreign investors, and institutional investors; environmental factors consist of industrial features, welfare and the improvement in the working environment of employees, and the influence of unseen factors such as competitors, customers, debtors, regulations, tax policies, and local communities.

2.1.2. Stakeholder Perspectives on CSR

The stakeholder-oriented approach is divided into the following categories: normative, instrumental, and visually descriptive [6]. The normative perspective is related to the level of motivation of CSR from the management position and their concerns with whether or not to make a sound and moral business decision; the instrumental perspective is a question of how CSR can play a key role in generating corporate performance. Meanwhile, the explanatory perspective relates to the attempt to understand CSR’s emergence, and how it is perceived alongside the reality of corporate management. This approach has the advantage of utilizing CSR strategically according to the CSR type, the targets, and the priorities after theorizing and systematizing CSR [7].

2.1.3. CSR and Performance

Most empirical studies conducted on CSR relate to factors that have stimulated CSR activities and influenced CSR in terms of economic performance. Studies conducted by Waddock and Graves [8], Wright and Ferris [9], Teoh and Wazzan [10], and McWilliam and Siegal [11] revealed a positive, negative, and neutral relationship, respectively, between CSR and economic performance. Studies in which a positive relationship is observed suggest that CSR increases a firm’s productivity by boosting the confidence of employees and organizational solidarity. Further, CSR is said to enhance the corporate reputation of the firm in the eyes of all stakeholders, not just the shareholders. Therefore, financial performance is improved. Studies that noted a negative relationship indicate that CEOs consider CSR an unnecessary expenditure that increases total cost. This outlook influences the managerial results adversely.

2.1.4. Strategic CSR

Strategic CSR is a business activity that is conducted based on the expertise that is acquired from management to provide social products or services. Fry et al. [12] insist that a charitable activity is based on the financial strategy of facilitating activities that contribute toward society. Lantos [13] as well as Porter and Kramer [14] define strategic CSR activity that simultaneously benefits the firm and society. Quester and Thompson [15] explain that strategic CSR is not only beneficial for a firm and a society, but it is also beneficial for accruing financial profits. In addition, Porter and Kramer [14] suggest that strategic CSR practices do not increase expenditure, but facilitate opportunities and innovation. They go on to suggest that strategic CSR increases comparative advantage, competitive power, and social welfare by sharing the increased value with society. While defining CSR, Porter and Kramer [14] emphasized the necessity to re-recognize product and market, redefine productivity in the value chain, and develop industrial cluster comprising of local communities for creating a shared value.

Sharma and Vredenburg [16] maintain that strategic management activities involve the creation of comparative advantage and value when new business resources are added to existing resources. Value creation requires innovation, and CSR provides an opportunity for innovation.

Byun [17] divided CSR into traditional CSR and strategic CSR, and analyzed the relationship between each CSR factor and the firm’s performance. The traditional CSR factors are based on Carroll’s [3] CSR pyramid model; the factors include responsible profit-making activities and legal and ethical activities. The strategic CSR factors are also based on Carroll’s [3] CSR pyramid model; the factors include social contribution activities and socio-innovative responsible activities, which was discussed in the Eiko [18] study.

2.2. R&D

Firms try to develop new technology by investing in R&D, which allows them to have a comparative advantage and achieve success in the market through innovative products. The R&D capacity of a firm is a dynamic capacity that is used to maintain comparative advantage, conduct R&D, and create knowledge to reinforce the firm’s power [19].

The learning mechanism in a firm plays an important role in maintaining the R&D capacity of a firm [20]. Effective organizational learning through knowledge sharing and knowledge creation are good for improving the performance of the firm and maintaining comparative advantage. The use of external resources through a network play an important role in technological innovation, which is the result of R&D [21]. Yam [22] described the R&D capacity as the capacity to combine R&D strategy, project execution and management, and manage R&D expenditures. In addition, Yam [22] refers to the R&D intensity as one of the factors of the R&D capacity.

The studies mentioned in this section describe the relationship between R&D and CSR. Hull and Rothenberg [23] maintained that CSR with a lower innovation intensity and a lower degree of product differentiation has a high influence on financial performance. Innovation intensity is classified as R&D expenditure and the degree of differentiation is classified as advertisement expenditure. Social performance is classified by the KLD (Kinder, Lydenberg, Domini & Company) index and financial performance is classified by ROA (Return on Assets). Padgett [24] found that the R&D intensity influences social responsibility significantly in the manufacturing industry; however, the findings did not show a significant effect in the non-manufacturing industry. As explained in Padgett’s [24] analysis, pressure from the government and stakeholders in the manufacturing industry is high, and the influence of the R&D intensity on CSR is higher for this industry. Padgett [24] discovered that a higher probability of implementing a CSR activity has a positive relationship with corporate governance variables, such as the leadership and independency of the board of directors as well as the sharing of institutional investors. In addition, the likelihood of the CSR implementation has a positive relationship with corporate characteristics variables, such as size of the firm, R&D expenditure, profitability, and diversification; however, it has negative relationship with debt ratio. Mcwilliams and Siegel [11] indicate there are theoretical and empirical limitations of existing studies which analyze the correlation between CSR and financial performance without taking into consideration the R&D intensity. R&D intensity is an important variable, and a lack of emphasis on this variable affects the accuracy of explanations in these studies.

2.3. Technology Commercialization

There are cases in which the results of successful R&D cannot be connected with the performance of a firm, and an analysis of the capacity to commercialize technology while considering strategic, institutional, and environmental factors is necessary to overcome this inability.

The main models for technology commercialization are discussed in this section. Cooper’s [25] technology commercialization process model describes the process as the development of a concept, examining feasibility, field tests, and finally determining the scale of commercialization; Jolly [26] divided it differently into technological observation, cultivation, realization, stimulation, and continuation; Goldsmith [27] proposed a different description of the phases as follows: the inspection stage, the development stage, commercialization, technology, and marketing.

Nevens et al. [28] maintained that technology commercialization is the capacity to acquire comparative advantage through cost reduction, quality improvement, and the acquisition of new technology. To this end, CEOs should prioritize technology commercialization and set clear goals regarding technology commercialization. Further managerial decision-makers should participate in the technology commercialization process. Concerns for the strategic plan are increasing the technology commercialization capacity. Adler and Shenbar [29] suggest that the capacity must satisfy market needs, facilitate the manufacture of products, satisfy future needs, and guard against utilizing unexpected technology. Cooper and Kleinschmidt [30] emphasize the importance of technologic strategy, technologic process, and technologic organization.

We used Yam’s [22] analysis of the relationship between technological innovation and the firm’s performance to substitute for technology commercialization capacity. We then analyzed the relationship regarding technological innovation capacity. Zahra [19] argue that a firm should consider financial performance measurements when considering the successfulness of technology commercialization. Camison and Villar-Lopez [31] analyze the effect of business performance on the capacity for technological innovation and divide technological innovation capacity into process innovation capacity and product innovation capacity.

3. Hypothesis and Operational Definition of Variables

3.1. Hypothesis

The aim of the present study is to set the hypothesis for a firm’s long-term strategy through the use of CSR’s essential factors. This study sets the hypothesis of CSR, R&D, and technology commercialization as strategic factors of management and financial performance based on earlier studies mentioned above. CSR is divided into traditional CSR and strategic CSR based on the study conducted by Porter and Kramer [14], as well as Byun [17]. Traditional CSR is based on Carroll’s [3] CSR pyramid model and divided into economic responsibility, legal responsibility, and ethical responsibility. Strategic CSR is partly based on Carroll’s [3] CSR pyramid model, which includes charitable responsibility and partly includes the socio-innovative responsibility of Porter’s [32] CSV factor. Strategic CSR creates new value for a firm and society, and innovation is considered an important factor for value creation. Here, we investigate the relationship between traditional CSR and strategic CSR by using R&D and technology commercialization capacity as variables. Based on the studies conducted by Yam et al. [22], Cohen and Levinthal [33], Dutta et al. [34], and Hagedoorn [35], the R&D capacity is composed of organizational learning, R&D intensity, and external networks. The technology commercialization capacity is composed of strategic technology planning, technological process capacity, and organizational capacity, which are based on the studies conducted by Nevens et al. [28] and Cooper and Kleinschmidt [30]. In addition, based on Kim [5], the factors motivating CSR are divided into internal CSR motivation factors, such as CEOs and leaders of an organization, and external factors, such as socio-environmental factors and the government. Therefore, Structural Equation Modeling (SEM) is used in this study for considering the merits of setting CSR, R&D, and technology commercialization as variables that influence traditional CSR and strategic CSR.

- H1:

- CSR is positively related to a firm’s performance.

- H1–1:

- Traditional CSR is positively related to a firm’s performance.

- H1–2:

- Strategic CSR is positively related to a firm’s performance.

- H2:

- R&D capacity is positively related to CSR.

- H2–1:

- Organizational learning is positively related to traditional CSR.

- H2–2:

- Organizational learning is positively related to strategic CSR.

- H2–3:

- R&D intensity is positively related to traditional CSR.

- H2–4:

- R&D intensity is positively related to strategic CSR.

- H2–5:

- Network externality is positively related to traditional CSR.

- H2–6:

- Network externality is positively related to strategic CSR.

- H3:

- Technology commercialization capacity is positively related to CSR.

- H3–1:

- Planning strategic technology capacity is positively related to traditional CSR.

- H3–2:

- Planning strategic technology capacity is positively related to strategic CSR.

- H3–3:

- Technology process capacity is positively related to traditional CSR.

- H3–4:

- Technology process capacity is positively related to strategic CSR.

- H3–5:

- Technical organization capacity is positively related to traditional CSR.

- H3–6:

- Technical organization capacity is positively related to strategic CSR.

- H4:

- CSR motivation is positively related to CSR.

- H4–1:

- Traditional CSR is positively related to the CSR’s internal motivation.

- H4–2:

- Traditional CSR is positively related to the CSR’s external motivation

- H4–3:

- Strategic CSR is positively related to the CSR’s internal motivation.

- H4–4:

- Strategic CSR is positively related to the CSR’s external motivation

3.2. Operational Definition of Variables

The following variables are used for operational definition for the structural model. Table 1 shows variables and measurement parameters. CSR motivation is divided into internal and external CSR that are measured by three items from Kim’s [4] research. Traditional CSR is divided into economic responsibility, legal responsibility, and ethical responsibility. Economic responsibility is measured by four parameters. Legal responsibility and ethical responsibility are measured by three parameters that are based on Carroll [36], Maignan [37] and the list goes on and on. Strategic CSR is divided into charitable responsibility and social innovation responsibility. Charitable responsibility and social innovation responsibility are measured by three parameters based on Carroll [3], as well as Porter and Kramer [14]. The R&D capacity is composed of organizational learning, R&D intensity, and network externality. They are measured by three parameters based on the studies by Yam [22] and Hagedoorn [34]. Technology commercialization consists of planning strategic technology capacity, technology process capacity, and technical organization capacity. Three parameters are used to measure technology commercialization with reference to Nevens et al. [28] and Cooper and Kleinschmidt [30]. Financial performance was measured using three parameters with reference to [17,38].

4. Research Methodology

4.1. Sample

A survey method was used to verify the hypothesis of this study. To analyze the influence of individual recognition on the decision-making of an organization, employees of a company who are familiar with CSR were chosen for the questionnaire survey. Based on the pilot analysis of the surveyed questions, the questionnaire was revised and finalized. The survey was conducted from 28 October 2015 to 31 October 2015 via e-mail. This mode of conducting the survey was designed by a specialized company. The responses of 212 participants, out of a total of 1408 respondents who work in a company and are familiar with CSR are used as valid data. The demographics of the population surveyed are shown in Table 2 as follows:

4.2. Verification of the Validity and the Reliability of Variables

Four survey questions related to CSR variables that were not compatible with the internal consistency were deleted after conducting a factor analysis of each variable. A factor analysis was conducted on the remaining questions. The result revealed a factor-loading index that was higher than 0.7 for all questions. This score proved the internal and external validity of the questions.

A validity analysis was conducted through Cronbach’s alpha coefficient. Cronbach’s alpha coefficient is used to measure validity or consistency between variables. An alpha coefficient that is higher than 0.8 implies a strong consistency, and an alpha coefficient that is higher than 0.6 implies acceptable consistency. In this analysis, all the variables scored higher than 0.7. Therefore, the respondents answered the questions consistently. Table 3 summarizes factor analysis and feasibility analysis.

4.3. Verification of Hypothesis

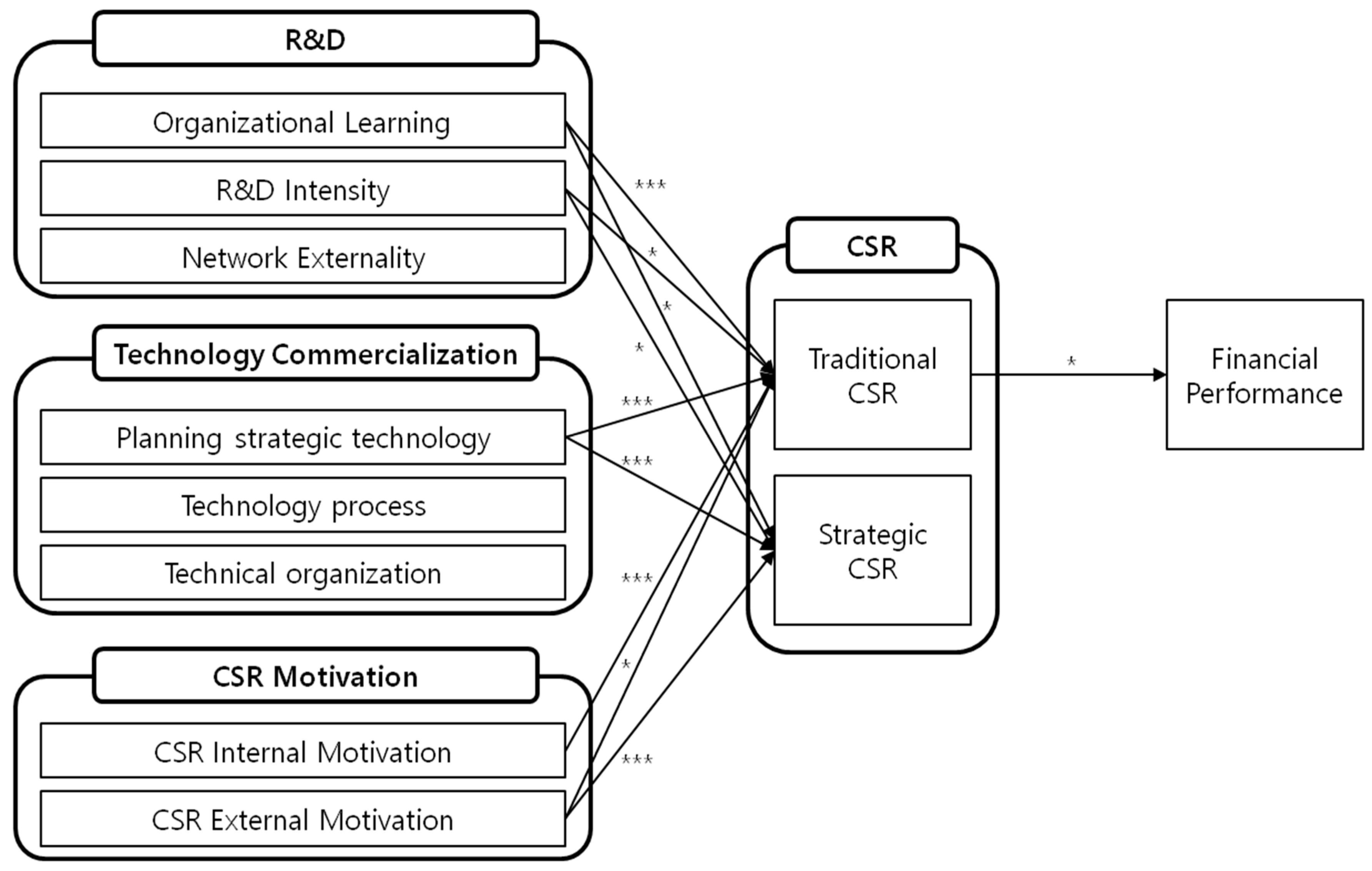

This study analyzed the influence of CSR, R&D, technology commercialization, and CSR motivation on CSR. The results of this analysis are shown in Figure 1 and Table 4. The point of this study was to understand the correlation between multiple independent and dependent variables, and hence the study used SEM to consider the question of correlation. The SEM is composed of a structure model and a measurement model. The structure model indicates a correlation between latent variables, and the measurement model indicates a correlation between latent variables and observation variables.

SEM route analysis was used to verify the hypothesis concerning the correlation between the variables. If the non-standardized regression significance value (p) is smaller than 0.05, then the correlation is significant. The financial performance path coefficient of traditional CSR was –0.4291 (H1–1). Strategic CSR demonstrated a positive impact; however, the hypothesis was rejected due to a lack of significance.

With respect to traditional CSR, the path coefficient of organizational learning for the R&D capacity was 0.3297(H2–1); R&D intensity was –0.1356 (H2–3); strategic technology plan of technology commercialization capacity was 0.3114 (H3–1); external CSR motivation was 0.0241 (H4–3). Therefore, the above hypotheses were considered effective and others were rejected.

Concerning the strategic CSR, the path coefficient of the R&D intensity was 0.1332 (H2–4); organizational learning was 0.0996 (H2–2); strategic technology plan of technology commercialization capacity was 0.2406 (H3–2); external motivation was 0.4603 (H4–4). Therefore, the above hypotheses were considered significant while others were rejected.

5. Conclusions

CSR has been considered to be necessary, rather than optional, in recent times. However, internally, firms are still considering CSR as an optional charitable activity. In other words, CSR is considered an expensive practice. To overcome this mindset, it is important to conduct research that studies the relationship between corporate image, social performance, and the profit motive. This study categorized CSR as traditional CSR and strategic CSR, and empirically analyzed the effect of R&D capacity and technology commercialization capacity on the implementation of CSR by basing CSR on previous studies. We analyzed the influence of core strategic management factors, such as traditional CSR, strategic CSR, R&D capacity, and technology commercialization, and then looked at the manner in which these factors influence traditional and strategic CSR. According to the results of the analysis, traditional CSR can have a negative effect on financial performance factors and organizational learning for R&D capacity, whereas the technologic strategy plan of the technology commercialization capacity could have a positive effect. Internal factors of a firm that motivate CSR, organizational learning for R&D capacity, and technologic strategy plan have a positive effect on traditional CSR. On the other hand, factors that could have a negative effect, including R&D intensity and external factors that motivate CSR activities in a firm. The results of strategic CSR analysis revealed that the factors exercising a positive influence on strategic CSR include R&D intensity of the R&D capacity, technologic strategic plan of technology commercialization capacity, and CSR external motivation. These results are based on empirical analyses.

From a stakeholder’s perspective, CSR can generate sustained value depending on its relationship with various stakeholders. Therefore, it is necessary to understand and persuade stakeholders effectively in order to create long-term corporate value. In order for firms to use CSR efficiently with limited resources, it is necessary to identify their stakeholders’ CSR attitudes and to identify core competencies that affect strategic CSR. The implications of this study are as follows.

First it is important to determine the appropriate CSR for the stakeholders. CSR motivation is divided into internal CSR motivation and external CSR motivation based on the stakeholders.

Traditional CSR is influenced more by internal factors, such as the willingness of CEOs or the motivation of the leaders to promote CSR in an organization. In contrast, strategic CSR is influenced more by external factors, such as socio-environmental, governmental, and non-governmental organization (NGO) factors. In particular, the environmental dimension of CSR is that the firms maintain a clean environment and fulfill its environmental protection responsibilities. This can help firms improve corporate image and productivity. The social dimension of CSR is that firms contribute to better community development. For example, firms support eco-friendly business, culture, and sports activities to grow together with businesses and communities.

Second, from a stakeholder’s perspective, a firm’s CSR should address not just social responsibility issues but actual strategic issues. To do this, the CSR of a firm should be implemented in a way that the strategic CSR meets the needs of various stakeholders. R&D intensity and organizational learning among the R&D capabilities and planning strategic technology among the technology commercialization capabilities should be derived as key factors for effective strategic CSR. Firms that consider technology as an important competence factor should focus on developing R&D intensity and technology strategic plan to create strategic CSR implementation rather than simply focusing on technology development. R&D and technology commercialization capabilities will enhance the effectiveness of strategic CSR and enhance corporate value by meeting the needs of various stakeholders. The ratio between R&D and CSR can be the strategic investment of a firm.

Third, the negative relationship between traditional CSR and financial performance shows that firms still recognize traditional CSR activities as a liability. They need to employ different strategies for developing CSR activities. These strategies could boost social and economic performance (instead of increasing costs) and broaden perceptions of strategic CSR by focusing on the potential to create shared value for social innovation and the firm’s innovation at the same time [16].

Despite the implications of the above results, there are some limitations. It is necessary to conduct research on other emerging countries rather than targeting only a specific area of South Korea. If the targets of the survey and the analysis of CSR, R&D, and technology commercialization comprised of decision makers, it would have been possible to analyze the implications with greater accuracy. In addition, the CSR factors were based on the study of Carroll (1991) [8] and Porter et al. (2011) [33]. However, further studies are needed to develop and use persuasive strategic CSR and CSV factors for analyzing the influence of these factors on social and financial performances. In addition, depending on the characteristics of stakeholders, it is necessary to examine factors that promote CSR. In addition, if research that reflects the characteristics of various industries is advanced, it will be able to convey a more comprehensive understanding.

Author Contributions

S.O. carried out the empirical studies, the literature review, drafted the manuscript and communication with the editor of the journal; A.H. participated in the design of the study and the statistical analysis; J.H. helped to draft and review the manuscript. All authors read and approved the final manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Bowen, H.R. Social Responsibilities of the Businessman; Harper: New York, NY, USA, 1953. [Google Scholar]

- McGuire, J.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Kim, S.J.; Paik, E.B.; Khulan, T. An Empirical Study on Shared Value Created by CSR Activities of Korean Corporations. Logos Manag. Rev. 2012, 10, 1–28. [Google Scholar]

- Kim, S.H.; Lee, K.W. Corporate Social Responsibility (CSR) in Accounting: Review and Future Direction. DAEHAN J. Bus. 2013, 26, 2397–2425. [Google Scholar]

- Donaldson, T.; Preston, L. The stakeholder theory of the corporation: Concept, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: What’s the bottom line. Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The Corporate Social Performance-Financial Performance Link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Wright, P.; Ferris, S.P. Agency conflict and corporate strategy: The effect of divestment on corporate value. Strateg. Manag. J. 1997, 18, 77–83. [Google Scholar] [CrossRef]

- Teoh, S.H.; Welch, I.; Wazzan, C.P. The Effect of socially activist investment policies on the financial markets: Evidence from the South African boycott. J. Bus. 1999, 72, 35–39. [Google Scholar] [CrossRef]

- McWilliam, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Fry, L.W.; Keim, G.D.; Meiers, R.E. Corporate contribution: Altruistic or for profit? Acad. Manag. J. 1982, 25, 92–106. [Google Scholar] [CrossRef]

- Lantos, G.P. The Boundaries of Strategic Corporate Social Responsibility. J. Consum. Mark. 2001, 18, 595–632. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and Society: The Link between Competitive Advantage and Corporate Social Responsibility. Harv. Bus. Rev. 2006, 84, 78–82. [Google Scholar] [PubMed]

- Quester, P.; Thompson, B. Advertising and Promotion Leverage on Arts Sponsorship Effectiveness. J. Advert. Res. 2001, 41, 33–47. [Google Scholar] [CrossRef]

- Sharma, S.; Vredenberg, H. Proactive Corporate Environmental Strategy and the Development of Competitively Valuable Capabilities. Strateg. Manag. J. 1998, 19, 729–753. [Google Scholar] [CrossRef]

- Byun, S.Y.; Kim, J.W. Strategic CSR and Corporate Performance in Korea and Japanese Corporations. Korean Acad. Int. Bus. 2011, 22, 83–110. [Google Scholar]

- Eiko, I. CSR Management Strategy; Toyo Keizai: Tokyo, Japan, 2005. [Google Scholar]

- Zahra, S.; George, G. Absorptive Capacity: A Review, Reconceptualization, and Extension. Acad. Manag. Rev. 2002, 27, 185–203. [Google Scholar]

- Lucas, B.; Bell, S. Strategic Market Position and R&D Capability in Global Manufacturing Industries: Implications for Organizational Learning and Organizational Memory. Indus. Mark. Manag. 2000, 29, 565–574. [Google Scholar]

- Bell, M.; Albu, M. Knowledge Systems and Technological Dynamism in Industrial Clusters in Developing Countries. World Dev. 1999, 27, 1715–1734. [Google Scholar] [CrossRef]

- Yam, R.C.; Guan, J.C.; Pun, K.F.; Tang, E.P. An Audit of technological innovation capabilities in Chinese firms: Some empirical findings in Beijing, China. Res. Policy 2004, 31, 543–567. [Google Scholar] [CrossRef]

- Hull, C.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Padgett, R.; Galan, J. The Effect of R&D Intensity on Corporate Social Responsibility. J. Bus. Ethics 2010, 93, 407–419. [Google Scholar]

- Cooper, R.G. Winning at New Product; Addison-Wesley: Boston, MA, USA, 1986. [Google Scholar]

- Jolly, V.K. Commercializing New Technologies; Harvard Business School Press: Boston, MA, USA, 1997. [Google Scholar]

- Goldsmith, R. Model of Commercialisation. 2003. Available online: http://asbdc.ualr.edu/technology/commercialization/the_model.asp (accessed on 15 September 2012).

- Nevens, T.M.; Summe, G.L.; Utta, B. Commercializing technology: What the best companies do? Harv. Bus. Rev. 1990, 18, 154–163. [Google Scholar] [CrossRef]

- Adler, P.S.; Shenbar, A. Adapting your technological base: The organizational challenge. Sloan Manag. Rev. 1990, 32, 25–37. [Google Scholar]

- Cooper, R.G.; Kleinschmidt, E.J. Winning business in product development: The critical success factors. Res.-Technol. Manag. 2007, 50, 52–66. [Google Scholar]

- Camison, C.; Villar-Lopez, A. Organizational innovation as an enabler of technological innovation capabilities and firm performance. J. Bus. Res. 2014, 67, 2891–2902. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. Harv. Bus. Rev. 2011, 89, 4–17. [Google Scholar]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Dutta, S.O.; Narasimhan, S.R. Success in High-Technology market: Is marketing capability critical? Mark. Sci. 1999, 18, 547–568. [Google Scholar] [CrossRef]

- Hagedoorn, J.; Schakenraad, J. A Comparison of Private and Subsidized R&D Partnerships in the European Information Technology Industry. J. Common Mark. Stud. 1993, 31, 373–390. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 499–505. [Google Scholar]

- Maignan, I. Consumers’ Perceptions of Corporate Social Responsibilities: A Cross-Cultural Comparison. J. Bus. Ethics 2001, 30, 57–72. [Google Scholar] [CrossRef]

- Arora, P.; Dharwadkar, R. Corporate Governance and Corporate Social Responsibility (CSR): The Moderating Roles of Attainment Discrepancy and Organization Slack. Corp. Gov.: Int. Rev. 2011, 19, 136–152. [Google Scholar] [CrossRef]

Figure 1.

Result of structural equation model. * p < 0.1; ** p < 0.05; *** p < 0.01.

{kind=link}

Table 1.

Variables and measurement parameters.

| Variable | Measurement Parameter | Researcher | |

|---|---|---|---|

| CSR Motivation | Internal Motivation | Charity contribution of a firm’s CEO Motivation provided by leaders of organizations Organizational network communication | Kim (2012) [22] |

| External Motivation | Socio-environmental variable Government motive NGO motive | Kim (2012) [22] | |

| Traditional CSR | Economic responsibility | Profit maximization Quality improvement Operating expense reduction Strategy for long-term growth | Carroll (1979) [3], Maignan (2001) [26] |

| Legal responsibility | Law-abiding management Compliance to relevant laws Compliance with legal demands | ||

| Ethical responsibility | General principles of ethics Ethical norms Effort for ethical trust | ||

| Strategic CSR | Charitable responsibility | Donation Resolution of social problems Contribution to local community | Carroll (1991) [8] |

| Socio-innovative responsibility | Re-recognition of product and market Redefine the productivity in the value chain Industrial cluster development for local community | Porter and Kramer (2006) [14] | |

| R&D capacity | Organizational learning | Capacity to monitor technological trend continuously Capacity to absorb knowledge acquired externally Recognition of the importance of tactical knowledge (intangible knowledge) | Yam et al. (2004) [37], Cohen and Levinthal (1990) [11] |

| R&D Intensity | Ratio of R&D investigation in total sales Ratio of R&D human resource in the total employees Expected R&D expenditure in accordance to growing sales | Yam et al. (2004) [37] Dutta et al. (1999) [13] | |

| Network externality | Developing new markets through technological cooperation with external institutions Creation of synergy effect through technological cooperation with external institutions Effectiveness of technology cooperation with external institutions | Hagedoorn (1993) [20] | |

| Technology commercialization capacity | Planning strategic technology capacity | Clear goal for technology commercialization Degree of understanding customer demand for developing new markets Benchmarking competitors | Nevens et al. (1990) [7] Cooper and Kleinschmidt (2007) [10] |

| Technology process capacity | Standardized technology commercialization process Systemized feedback Staged management and risk management | ||

| Technical organization capacity | Operation of specialized department for technology commercialization Degree of human resource participation in commercialization Collaboration for technological commercialization | ||

| Financial Performance | Increased revenue Increased profit Increased growth rate trend | Arora (2011) [1] Byun(2011) [5] | |

Table 2.

Features of the population surveyed.

| Features | Response Rate | ||||

|---|---|---|---|---|---|

| Gender | Male (49.5%) | Female (50.5%) | |||

| Age | 20 years (22.7%) | 30 years (23.1%) | 40 years (22.6%) | 50 years (31.6%) | |

| Education | High school (9.4%) | University (76.4%) | Masters (9.9%) | Doctorate (4.3%) | |

| Position | Deputy (52.8%) | Section chief (18.4%) | Deputy head of the department (9.5%) | Head of department (11.8%) | Board member (7.5%) |

| Working Period | Less than 5 years (46.7%) | 5–10 years (22.2%) | 10–20 years (18.4%) | More than 20 years (12.7%) | |

| Number of Employees | Less than 50 (27.8%) | 51–100 (15.1%) | 101–500 (30.2%) | More than 501 (26.9%) | |

| Established Years of the Firm | Less than 10 (15.6%) | 10–20 (30.7%) | 20–30 (18.4%) | 30–40 (15.6%) | More than 40 (9.4%) |

Table 3.

Summary of factor analysis and feasibility analysis.

| Variable | Initial Question Number | Final Question Number | Factor Loading | Cronbach’s Alpha | |

|---|---|---|---|---|---|

| CSR motivation | Internal variable | 3 | 3 | 0.8082 0.8967 0.8845 | 0.8291 |

| External variable | 3 | 3 | 0.7334 0.8595 0.8083 | 0.7204 | |

| Traditional CSR | Economic responsibility | 4 | 2 | 0.7507 0.7047 | 0.7156 |

| Legal responsibility | 4 | 4 | 0.8261 0.8094 0.7794 0.8117 | ||

| Ethical responsibility | 4 | 3 | 0.8380 0.8328 0.8562 | ||

| Strategic CSR | Charitable responsibility | 4 | 3 | 0.7308 0.7049 0.7096 | 0.8730 |

| Socio-innovative responsibility | 3 | 3 | 0.7178 0.7144 0.7610 | ||

| R&D capacity | Organizational learning | 3 | 3 | 0.8200 0.8658 0.8343 | 0.7915 |

| R&D Intensity | 3 | 3 | 0.9162 0.9152 0.8927 | 0.8936 | |

| Network externality | 3 | 3 | 0.7322 0.8943 0.9104 | 0.8927 | |

| Technology commercialization capacity | Planning strategic technology capacity | 3 | 3 | 0.8708 0.8817 0.7121 | 0.7441 |

| Technology process capacity | 4 | 4 | 0.8208 0.8992 0.8669 0.9005 | 0.8949 | |

| Technical organization capacity | 3 | 3 | 0.8689 0.9283 0.8652 | 0.8653 | |

| Financial Performance | 3 | 3 | 0.9021 0.9164 0.9153 | 0.8979 | |

Table 4.

Path analysis summary.

| Hypothesis | Path Name | Coefficient | p-Value | Ad/Re |

|---|---|---|---|---|

| H1–1 H1–2 | Traditional CSR → Performance Strategic CSR → Performance | –0.4291 0.0316 | 0.018 0.864 | adopt reject |

| H2–1 H2–2 H2–3 H2–4 H2–5 H2–6 | Organizational learning → Traditional CSR Organizational learning → Strategic CSR R&D Intensity → Traditional CSR R&D Intensity → Strategic CSR Network externality → Traditional CSR Network externality → Strategic CSR | 0.3297 0.0996 –0.1356 0.1332 0.0565 0.0609 | 0.000 0.096 0.024 0.010 0.334 0.206 | adopt adopt adopt adopt reject reject |

| H3–1 H3–2 H3–3 H3–4 H3–5 H3–6 | Planning strategic technology→ Traditional CSR Planning strategic technology→ Strategic CSR Technology process → Traditional CSR Technology process → Strategic CSR Technical organization → Traditional CSR Technical organization → Strategic CSR | 0.3114 0.2406 –0.0870 –0.0312 –0.0937 0.0441 | 0.000 0.008 0.179 0.671 0.152 0.401 | adopt adopt reject reject reject reject |

| H4–1 H4–2 H4–3 H4–4 | CSR Internal Motivation→ Traditional CSR CSR Internal Motivation → Strategic CSR CSR External Motivation → Traditional CSR CSR External Motivation → Strategic CSR | 0.4199 0.0945 –0.0241 0.4603 | 0.000 0.134 0.017 0.000 | adopt reject adopt adopt |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Oh, S.; Hong, A.; Hwang, J. An Analysis of CSR on Firm Financial Performance in Stakeholder Perspectives. Sustainability 2017, 9, 1023. https://doi.org/10.3390/su9061023

AMA Style

Oh S, Hong A, Hwang J. An Analysis of CSR on Firm Financial Performance in Stakeholder Perspectives. Sustainability. 2017; 9(6):1023. https://doi.org/10.3390/su9061023

Chicago/Turabian StyleOh, Seungwoo, Ahreum Hong, and Junseok Hwang. 2017. "An Analysis of CSR on Firm Financial Performance in Stakeholder Perspectives" Sustainability 9, no. 6: 1023. https://doi.org/10.3390/su9061023

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.