Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda

1

School of Economics, Department of Management and Law, University of Rome “Tor Vergata”, Via Columbia 2, 00133 Rome, Italy

2

Department of Management, University of Turin, Corso Unione Sovietica 218 bis, 10134 Turin, Italy

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(9), 4750; https://doi.org/10.3390/su13094750

Submission received: 12 March 2021

/

Revised: 21 April 2021

/

Accepted: 21 April 2021

/

Published: 23 April 2021

(This article belongs to the Special Issue Role of Impact Assessment in Sustainable Development)

Abstract

:The social impact assessment (SIA) process is widely utilised and is receiving increasing interest from both scholars and practitioners. A systematic approach was applied in this study to search for articles about SIA models. In the first step, we analysed six main SIA model mappings between 2004 and 2015. In the second step, 98 models were identified. The main findings include the definition of emerging paths for the future research agenda on this topic. Compared with previous SIA mappings, we identified 22 additional models that are related to the sustainability discourse. The meaning of sustainability is defined both by the emergence of new systems in finance that require specific metrics and in relation to the global agenda towards sustainable development. It is interesting to notice how social impact models, sustainability indicators (under the global framework of sustainable development goals (SDGs)) and new financial scores (such as environmental, social and governance (ESGs)) are converging into a common discourse, even if divergence is still present, and further research is needed to unlock the relationships among them.

1. Introduction

Over the last few years, attention has focused on the study of different models of measurement and evaluation of value that cannot be directly recognised through conventional financial metrics [1]. This growing attention has led to changes in organisations that operate in the third sector and in hybrid companies, which, at various levels, are increasingly trying to find credible solutions to demonstrate the social value generated through processes of measurement and social impact assessment (SIA).

Issues in SIA are receiving more attention from a whole range of social enterprises in what Young et al. [2] defined as the “Social Enterprise Zoo”, each with a different approach and purpose.

At the same time, governments on regional and national scales have launched programmes to strengthen their ability to assess the social value generated by the evolution of the traditional welfare state. They are in the difficult position of having to respond to a growing demand for public goods and services with fewer resources available for public financing yet, at the same time, are being faced with challenges concerning the management of public debt, as dictated by spending constraints and increasing social need from an aging population and increased immigration [3,4].

When this study discusses social impact, it refers to Clark’s definition [5]: “Social impact is the portion of the total outcome that occurred as a direct result of the intervention, net of that portion that would have occurred equally without the intervention”.

The scope of social impact is the construction and transmission of a set of information capable of expanding and deepening the knowledge of the value generated to better guide decision-making processes at different levels is precisely the treated topic of social impact [6,7,8].

A central issue is the debate about “who” is affected by the impact discussion. It is necessary to start from the assumption that the impact generated can be positive or negative, and this can be precisely the most immediate answer, because it is able to influence the well-being of people, the community and the community [9].

For this reason, each stakeholder, with different levels of priority, is interested in the issue. Some scholars argue that the primary stakeholder in impact evaluation is the PA [10]. We find impact as an element of relationship between different organizational configurations that populate a redrawn geography of value, where distinctions and perimeters are no longer marked by mere formal elements, but by different visions, intentions, and values. To address the question of who is interested in SIA, Klemelä [11] examined the role of legitimation means from the perspective of different stakeholders.

The study does not address the issue of impact for specific stakeholders, such as the public, private or non-profit sector. However, through this insight, the impact generated will directly and indirectly benefit the whole community.

When dealing with the topic of social impact, there are three key aspects to keep in mind: intentionality, measurability and additionality; the authors focus on the second mentioned. Assessing social impact is still not easy today, largely because of the difficulties in identifying qualitative and quantitative metrics to demonstrate the extent to which social impact is generated.

In many of the existing contributions, the effort needed to align theory and practice is noticeable. These studies show that in academic discourse, there are many assumptions that practitioners are not able to make for various reasons. For Smith and Stevens [5], this is particularly true for SIA models, where the developed metrics range from highly qualitative, self-developed input measures to more sophisticated quantitative output and impact measures.

However, the SIA process is widely utilised, and it is gaining increasing interest from both scholars and practitioners. In this study, we analysed SIA models in order to understand their main features and the emerging paths that may determine the future research agenda on this topic. We particularly noticed that the last academic work that tried to summarise the scientific production on SIA is a paper from six years ago [6], and since this time, the number of publications on this topic has continually increased, thus suggesting a need for a new systematisation of the literature.

The remainder of the paper is as follows. Section 2 presents the theoretical background of the study. Section 3 describes the method for conducting the literature review. Section 4 focuses on the analysis of the six main SIA model mappings that emerged from the literature. Section 5 presents an update of SIA model mappings, identifying 98 models. Section 6 consists of concluding considerations, limitations and ideas for the future research agenda.

2. Theoretical Background

The definition of “impact” has been widely discussed in the literature as cited in the previous section [6,12,13,14,15,16]. Social Impact Assessment combines social research, public engagement, planning and social change management [17].

Social impact measurement aims to assess the social and environmental value produced by the activities or operations of any organization (for-profit, non-profit or public). Although any company can have a social impact, we will always need to distinguish between companies that are socially oriented, such as non-profit organizations, social enterprises and public bodies, and those that create it indirectly. For these reasons, it is necessary to make order among the entire panorama of models, precisely to create tools that can best represent the impact of an organization, enhancing its social vocation.

The relationship between impact and complexity seems particularly interesting considering the systems change perspective and the possibility of legitimizing forms of value generation not recognized by conventional financial metrics [18]. The complexity approach has unveiled the perspectives of SIA from being a performance construct specific to a minority portion of organizations to becoming a determinant for the generation of new cross-sectoral relationships among public, for-profit, and non-profit organizations

Arvidson and Lyon [19] stated that social impact can be perceived as a social construction. The complexity of SIA lies in this: there is no clear definition of what is meant by “social”, so discretion must be involved when assessing social impact [19,20].

Through the analysis of the existing literature, we identified five streams of studies that discuss, from different points of view, the “social” meaning:

- (1)

- social value creation and corporate social responsibility (henceforth CSR) studies;

- (2)

- social enterprise (henceforth, SE) studies primarily focused on the issues of performance and accountability;

- (3)

- environmental impact studies;

- (4)

- public sector and impact finance studies;

- (5)

- developing economies studies.

(1) The first avenue is rooted in CSR around the notion of “creating social value”, as developed by Porter and Kramer [21], in order to explain a deeper relationship between business and society. Organisations should move beyond the traditional belief that their economic value is separate from, and in conflict with, their social value by assuming the perspective of blended value, as coined by Emerson [12]. Within the wider process of value creation, organisations need to be aware of the importance of quantification in unlocking new value and creating valuable opportunities for innovation and growth that would otherwise be missed [6,22,23].

(2) The most consistent field of study concerning SIA is related to SE performance and accountability. Social impact is described as a combination of resources, inputs, processes or policies that occur as a result of the real, implied or imagined presence or actions of individuals in achieving their desired outcomes [24,25,26]. In order to assess the performance of an SE, Clark and Brennan [27] developed the Balanced Value Matrix (henceforth, BVM), which concludes that separate and balanced indicators exist for outputs (enterprise actions), outcomes (the benefits associated with enterprise actions) and impacts (the results that enterprises desire) [28].

It is worth contrasting this approach with the contribution of Clark et al. [5], who introduced the concept of the impact value chain (henceforth, IVC). Since then, IVCs have been widely used to better understand the relationship between programme inputs and outcomes and to discover which mechanisms of change are involved in moving from inputs to desired results [29]. Bagnoli and Megali [30] suggested that measurement of SE performance should consider economic and financial performance, social effectiveness and institutional legitimacy. According to Dart [31], SIA promotes improved accounting practices, increasing the legitimacy of the organisation with its stakeholders and enhancing the relationship of trust with the organisation’s funders. In a context of scarcity and competition for funds, the use of standard procedures for assessing and reporting social outcomes might encourage investment in an SE that adopts them [22,32,33].

Based on a study of five SEs in the UK, Nicholls [34] argued that evaluations and audits are used as a means by which to “enhance social mission rather than merely to respond to regulation”. He suggested that “emergent reporting practices constitute a spectrum of disclosure logics that social entrepreneurs exploit strategically to support their various mission objectives with key stakeholders”. Impact measurement is thus seen as a part of a negotiation process between stakeholders.

In another study, Nicholls [35] showed how a “flexible reporting format can be used strategically in various ways by companies according to their particular objectives and resource limitations”. Therefore, SIA is seen as a strategic opportunity for SE development [34,36].

(3) Bakar et al. [17] consider SIA to be a subfield of Environmental Impact Assessment (henceforth, EIA). EIA refers to the assessment of impacts concerning the environment. Although EIA was intended as an all-inclusive framework for analysing environmental and social issues, it failed to adequately address social issues [6], and, therefore, SIA was developed with a gradual extension of the items under consideration [37,38].

(4) Another field of study relates to the transformation of welfare systems and the role of impact finance. The increasing scarcity of public resources has led to innovation in economic relationships between public bodies and private organisations [39,40,41,42,43]. These changes present a challenge in the form of a hybrid market with unexplored potential, involving financial intermediaries and local bodies, small and medium-sized enterprises (henceforth, SMEs), large enterprises, SEs and civil society [44]. The Organization for Economic Cooperation and Development (OECD) report on “new investment approaches to meet the social and economic challenges” [45] stated that impact investing has declined as a result of the changing relationship between finance and philanthropy.

One of the issues addressed by this field of study is that the assessments are often under pressure to demonstrate short-term effects rather than to emphasise long-term impact. Although there are generally accepted accounting principles that support financial reporting, similar standards related to the measurement and communication of social impact have not been produced yet because it is difficult to arrive at a comprehensive definition of the concept of social impact, and the related measurement models often lack the rigour that characterises accounting approaches aimed at assessing financial returns [39].

(5) The last field of study is related to the “people aspect” of development-induced change by empowering communities with a voice in the EIA process [46]. Countries with emerging economies are especially affected by poverty, and SIA conducted within this context necessitates mitigation of both the direct impacts of development as well as the social legacies that can entrench poverty and inequality. Social development is seen as an approach that can be used to reduce poverty and inequality [46].

The proposed overview sheds light on a nebulous and confused approach to the topic of SIA. As highlighted by the OECD [1], the lack of a common language and understanding of the definition of “social impact” and the best way to measure it has hampered both academic debate and the adoption of SIA models amongst practitioners.

Within managerial studies are these five perspectives on the meaning of social impact. This heterogeneity is the reason why, in the literature, many models for assessing social impact have been developed over time. Therefore, some authors have dedicated their work to clustering, categorising and mapping SIA models.

3. Method

A systematic approach was applied in this study to search for articles about SIA models. We used the Web of Science and Scopus databases to find relevant articles. For both databases, the following keywords were used for article searching: “Social impact assessment” OR “Social performance assessment” OR “Nonfinancial performance assessment” OR “Social return assessment” OR “ESG assessment” OR “Impact investing assessment” AND “Model*”. Table 1 shows the criteria used in searching and selecting articles.

For the Web of Science, our search was limited to searching titles, abstracts and keywords, resulting in 101 unique documents. After limiting the search by selecting only the article and review options, we arrived at 84 documents, which was further reduced to 82 by excluding articles not written in English. A list of these 82 articles was then downloaded as a comma-separated values (CSV) file and imported into a spreadsheet.

For the Scopus database with the same three keywords, 245 documents were found on the first search attempt. Limiting the search to the article’s category brought this down to 214 articles and focusing further on articles written in English reduced this to 207 documents. Furthermore, we limited this search to the following five categories: Business, Management and Accounting Economics, Econometrics and Finance, Psychology, and Decision Sciences. We merged the 82 articles from the Web of Science and the 207 articles from Scopus into an Excel file. We were aware that some articles would be listed in both databases, so we removed 58 duplicates through spreadsheet filtering. Thus, we arrived at 231 unique articles. Upon checking the title, keywords and abstract of each article, we found 187 relevant articles for inclusion.

We decided to supplement the academic results by collecting 43 articles from the two most acknowledged practitioners’ repositories: The Foundation Center (TRASI) and the NEF. We then had 230 articles from the searching process to include in this review. We read these papers with two main purposes:

- Identifying previous studies that mapped the evolution of SIA models and then analysing those studies to verify whether they provided clusters or groups of SIA models;

- Investigating the models already reviewed by previous studies and the new SIA models proposed since the last mapping study to highlight emerging patterns and to shape the future research agenda in this field of research.

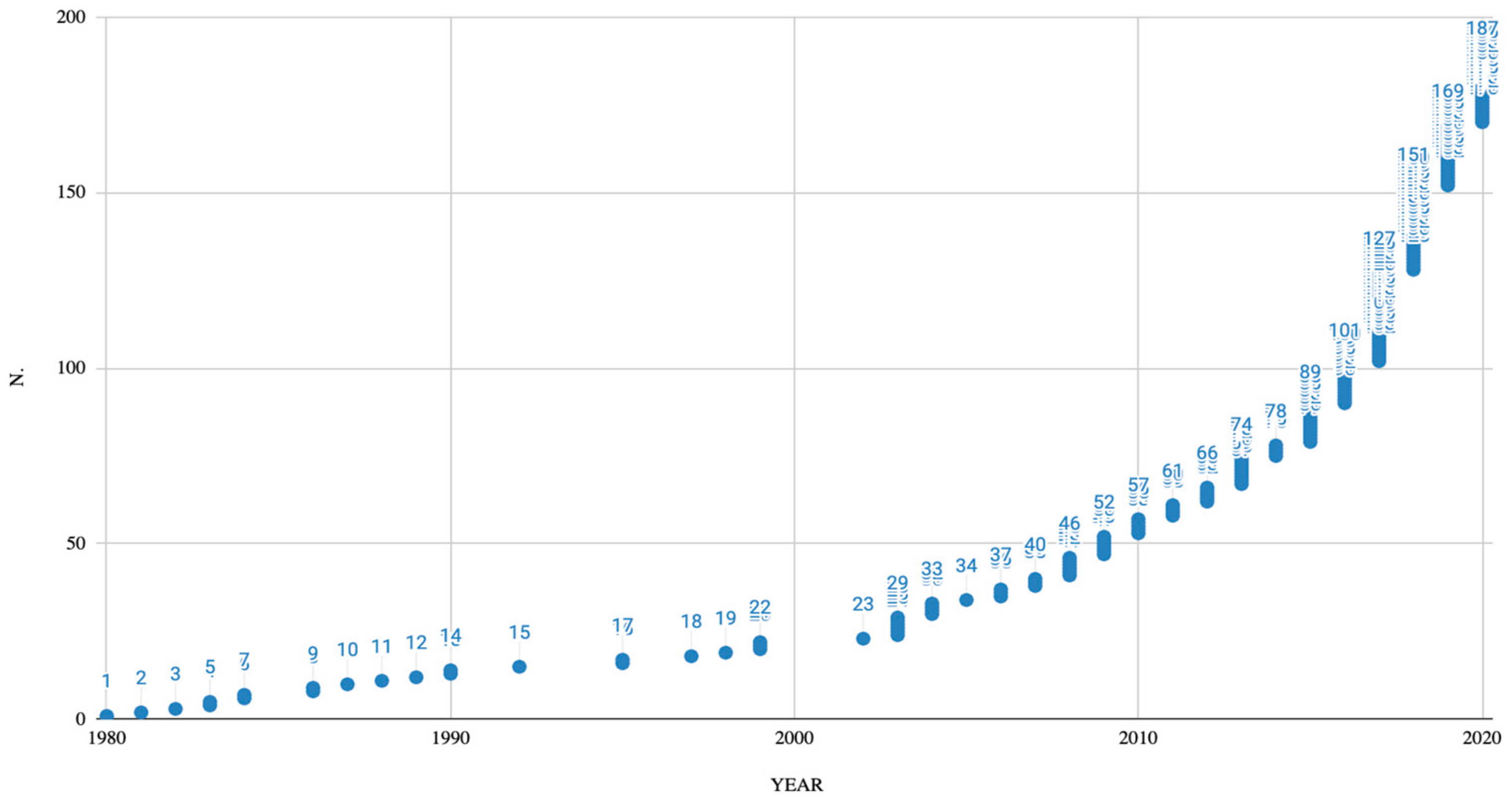

During the period under review (1980–2020), scientific production on Social Impact Models started in 1980 and underwent changes in 2003 and 2010. The number of publications in journals on the topic increased significantly between 2015 and 2020 (Figure 1). The data confirm the above. This field of research is constantly evolving, and the horizons are becoming wider and wider.

4. Six Studies in the Search for SIA Models

First of all, we must clarify that we use the term “model” to mean a named, documented process that is used to assess either the actual social and/or environmental impact and that, in the literature we analysed, the terms “approach”, “method” and “model” are used interchangeably.

Six main attempts at SIA model mapping were found from both academics and practitioners. Those doing the mapping have had different approaches to grouping the SIA models, and they have used a variety of sources. Table 2 shows how the authors grouped the models mapped. It is interesting to notice that the groups are presented ex ante in the description of the models—based either on the process or on the usage—while the last mapping from Grieco et al. [6] clusters them ex post using variables identified from previous studies. The authors use the terms models, methods and systems to mean “the ways” of assessing social impact.

Although the labelling of the SIA groups is different between authors, there are similarities, such as the emergence of models from quality systems, models based on monetisation and models from rating systems.

The first mapping study [5] aims to provide a measurability framework for the double bottom line approach. The authors tried to respond to the need for more tangible accountability for the social impact created for each invested or granted dollar. Their approach can be defined as “investor driven”, and the groups that they identify are thought of as having a three-step scale: the models that provide information only on the process, the models that inform about the social impact and the models that enable the transformation of the social impact information into financial metrics in order to combine the social and financial dimensions into a blended evaluation. They consider four key aspects in order to identify coherent groups of SIA models (the authors refer to them as “models/methods”): the completeness of the IVC along the sequence input-activities-output-outcome-goal alignment, the purpose of the assessment, the data feasibility and the possible sectors of application.

While the first mapping study emphasises the monetisation capacity of the SIA models, the second one [47] intends to shed light on the function of each model. The three possible functional types are rating systems, which are models using a fixed set of indicators and the impact investment’s quality or potential quality, summarised by a score or symbol; assessment systems, which are models that use a fixed or customised set of indicators at a point in time, evaluate characteristics, practices and/or results of portfolio investments but do not provide explicit tools to manage the tracking of operational data by the organisation over time; and management systems, which are models that provide tools for organisations to manage detailed operational information about drivers of impact. Olsen and Galimidi [47] used three variables provided by Clark et al. [5] (purpose, data feasibility and sector) and three new variables. The first of these new variables relates to the methodological approach adopted by the SIA model, the second investigates the types of data management required by the SIA models, and the third looks into the presence of verification criteria, thus improving the credibility of the results provided by the model.

The third mapping study provided by Zappalà and Lyons [39] identified three groups of SIA models under a different point of view related to the connections between the SIA process and conventional managerial processes. The first is connected to the accounting and auditing process, and it enables the understanding of the social impact on the surrounding community and beneficiaries and builds accountability by engaging with key stakeholders. The second is connected to a logical framework and project management processes, and it provides a systematic and visual way for individuals to present and share their understanding of the relationships among the resources available to operate their programme (inputs), the activities that they plan to do (strategies) and the changes or results that they hope to achieve (outcomes and impact). The third is explicitly named “social return on investment” and is connected to financial management and investor relationship processes, providing a single number that is the result of a ratio between the monetary value of the positive changes achieved through the activities and the budget invested. Zappala and Lyons [39] used eight variables, of which three are new compared with those used by Olsen and Galimidi [47]. The scope of the analysis here is split into two: clarity of purpose and scope. The presence of comparative impact data or information and the materiality analysis are the two new variables.

The fourth mapping study by Rinaldo [48] is focused on the tools provided by scholars and practitioners in order to improve the organisational capacity to measure and evaluate social impact. She identified three types of tools: monitoring and evaluation tools, quality systems and outcome tools. The monitoring and evaluation tools can inform about what data to collect, when to collect it and who will collect it. This information can provide proof that a performance goal has been met, or it can support social impact measurement. The quality tools focus on how things are done. They look at how an organisation is run, how staff are managed and customer care. A set of standards are defined and used to gauge areas for improvement. Some quality tools focus on how activities are carried out, and others also require evidence about the results of these activities. This evidence requirement would have the additional benefit of providing information for impact measurement. The outcome tools are used to measure and record the progress that a beneficiary makes and pinpoint areas of future need. They make it possible to assess the changes made in a consistent and standardised way. Outcome tools provide information that can be drawn together to give an overview of the change achieved by a service or project. They are therefore a key part of the impact measurement process. The variables used by Rinaldo [48] are for investigating the usability of these tools in terms of cost-efficiency and cost-effectiveness, so they investigate the cost of each tool, its complexity, the time required to embed it within organisational processes, how demanding the tool is for the staff in terms of the training required to implement it and the provision (and its cost) of the support required to process it.

In the fifth mapping study, Maas and Liket [13] used the same groups provided in [5]. Nevertheless, they improved the analysis by considering a larger number of models (30 vs. 9 models) and a more consistent set of variables and by introducing the time frame variable in the analysis. The capacity to determine the time factor of the models opens new perspectives for the SIA, making the measurement and evaluation process circular: social impact forecasting as an ex ante evaluation of the expected results, social impact monitoring as an ongoing step for checking the intermediary data and the ex post evaluation for informing about the changes achieved and the improvement areas to stimulate as drivers for the next strategic planning cycle. Another relevant variable that Maas and Liket [13] added is related to the different perspectives that SIA models can assume. When they originate from business (micro perspective), for example, they include indicators that differ from the indicators used for assessing the impact on the urban/rural territory (meso perspective), and even more different are the indicators used when the perspective is wider and encompasses socioeconomic dimensions at the country or regional level (macro perspective). Depending on the perspective used, different indicators will be used, and therefore, different impacts will be measured.

The latest and most comprehensive mapping study [6] employed a combination of the variables used prior to 2015 to carry out a hierarchical cluster analysis. More specifically, Grieco et al. [6] integrated six variables with those identified by previous authors and added one more variable that refers to the developer of the SIA model (actors involved in the development of SIA models). Table 3 summarises the variables used and their references.

Applying these variables to the SIA models mapped (i.e., 76) resulted in four clusters:

- o

- Cluster 1 (Simple Social Quantitative) contains models based on quantitative indicators. These models are easy, applicable to any sector and intend to produce a quantitative measure of the social impact and of the impact on employees with a retrospective time frame.

- o

- Cluster 2 (Holistic Complex) contains models characterised by a holistic purpose, and this explains the presence of both qualitative and quantitative variables. The aim of these models is to provide evidence to obtain funding, so they focus on reporting and communication of the results achieved. These are also applicable to any sector, but in this case, the complexity is high.

- o

- Cluster 3 (Qualitative Screening) consists of models based on qualitative variables and are usually focused on holistic impacts. They are retrospective and have a basic level of complexity.

- o

- Cluster 4 (Management) contains models based on qualitative or quantitative variables that aim to measure different types of impacts. They are used for managerial or certification reasons. Usually, they are applied to ongoing activities.

5. Model Mapping

Previous mappings have used different approaches to grouping SIA models and a variety of sources, and therefore, they have analysed a variable number of models. It is important to underline that the purpose of some of the previous mapping was not to collect all models developed but to become a practical guidance for assessing social impact. These mappings aimed to become a reference point for those who have to choose what kind of SIA model to implement according to the purpose of the assessment. As already described, the very first list of models was developed by Clark et al. [5] and was based on grey literature and interviews with key stakeholders. Indeed, the interest in systematising SIA models emerged from practitioners and, over time, has gained importance in academic studies. As shown in Table 4, the number of models has varied over time, as well as the number of patterns identified. It is possible to observe a growing trend in the number of models listed, aside from Zappalà and Lyons [39], who decided not to count the models but to approach them directly by dividing them into groups based on their main characteristics.

Ninety-eight social impact measurement models were identified. Appendix A provides the names of the models mapped. In comparison with the latest mapping by Grieco et al. [6], 22 new models were found, 52 were confirmed, and 24 have been renamed but are coherent with the previous list. In addition, their study, as in former SIA mappings, does not include models that assess only the internal organisational efficiency, models that cannot be linked to an organisation (for instance, policy evaluation models are not listed) or models for which the information is too little to be included.

It is important to underpin that there is a semantic issue concerning SIA models; therefore, this mapping, as with the former ones, has to be considered as partial and not exhaustive. Aside from specific models that are establishing themselves as reference points, most of the models might have different names but actually reproduce the same process and consider the same variables to assess social impact. This is the reason why 24 of the latest mappings have been identified; even if the name of the model itself might have changed over time and with different research parameters (for instance, other databases), other names might be found. The most used model is social return on investment (SROI) and other monetisation models that have been developing around it. Another two very common models come from management systems and quality systems such as EMAS (Eco-Management and Audit Scheme) and EFQM (European Foundation for Quality Management Excellence Model).

It is interesting to observe a new category of models related to the issue of sustainability and finance. Among the 22 new models, 10 of them are related to the assessment of environmental, social and governance (ESG) performance [49], and 5 of them are associated with sustainable development goals (SDGs) and sustainability assessment. In terms of ESG, it is crucial to consider the latest OECD (2020) report that underlines the variety of ESG scores and ratings and the complexity of this kind of assessment. The OECD report cites many hundreds of indexes and ratings to assess ESGs that correspond to a similar number of firms providing this service, even though there are only three main market players. The ESG models listed in our mapping are just a small portion of the high number of rating systems that are rapidly developing in consultancy firms and investment funds. Those mapped are the ones that were already mentioned in academic or grey literature involving the discourse on SIA models. This opens up future research questions that could investigate the relationship between SIA studies, sustainability and finance. In particular, ESGs might have an important role in the development of “alternative” finance, since they are identified in the OECD report [50] as a measure for social impact investing and sustainable and responsible investing (SRI).

The other important topic of new models relates to sustainability and expands the already listed Global Reporting Initiative (GRI) type of model. There are five models that focus on the assessment of SDGs. SDGs are a global framework with a shared and specific set of targets; it is interesting that different types of SIA models are arising to assess if and how an organisation is contributing to the reaching of global targets.

The novelty of this mapping comprises the emergence of sustainability as a new keyword of SIA models in relation to both finance and enterprise assessment.

6. Discussion and Conclusions

6.1. Contributions to the Literature

The authors show that the analysis conducted consisted of two steps. First, six major mappings of SIA models between 2004 and 2015 were analysed. As a second step, 98 models were identified. The year 2015 was very important scientifically for the topic because the policy context of sustainability changed with the inclusion of the SDGs [51].

Until now, the research in this field has almost never led to shared solutions, and this finds direct evidence in the plurality of models adopted for social impact measurement and evaluation, representative of highly differentiated approaches and tools. This condition is generated by the fragmentation among SIA models and the variety is high, apart from the very few models that present a clear methodology and features, e.g., the SROI [8], most models are not standardized (at least in the process) [9]. This variety certainly covers a wider range of dimensions for assessing social value and accommodates the diversity of each entity (from for-profit companies to social enterprises, from benefit companies to non-profits), but at the same time, it has the limitation of making it much more difficult to scale assessments [52]. The fuzziness of SIA models also affects impact finance, which should be the system in which these news metrics are considered [53].

For this reason, the purpose of this paper is to provide a literature review of SIA models and an update of the latest mapping from 2015. The analysis of previous studies was critical to better understand how to interpret the mapping and to question how to expand this research study. In fact, the other six mapping studies revealed clusters, groups and variables. The model grouping or clustering usually consists of three main labels: (1) models that come from performance/management system studies, of which the most used is EMAS; (2) models that come from auditing/quality system studies, of which the most used is EFQM; and (3) models that aim to monetise the outcome, called monetisation models, of which the most known and used is SROI. In the 98 models analysed, we can identify these groups, although we cannot yet fully describe the characteristics and frequencies. The next step in this research study was to perform a cluster analysis of our group by selecting some of the variables from previous studies. From our perspective, it appears that a fourth group/cluster of patterns may emerge, and that is the one related to sustainability. As mentioned in the previous mapping, the topic of sustainability was present through the inclusion of GRI among SIA models but did not have specific importance. From our mapping, sustainability seems to be the main driver of the 22 new models found. The meaning of sustainability is determined by the emergence of new systems in finance requiring specific metrics and in relation to the global agenda towards sustainable development. Further research should focus on the relationship between social impact studies and sustainability studies as two frameworks that could partially overlap and integrate. The integration of the two perspectives consists primarily of a theoretical problem [54].

This brings to light how impactful the grafting of global organisations is to provide a direction for innovation in terms of social impact.

6.2. Implications for Managers

As we have shown with this research, the SIA process is widely implemented and is capturing increasing interest from both scholars and practitioners. In this article, we analysed the models of SIA to understand their main characteristics and the emerging pathways that may determine the future research agenda on this topic [55].

In particular, we noted that the last academic work that attempted to summarise the scientific production on SIA is a 6-year-old paper [6], and since then, the number of publications on this topic has steadily increased, thus suggesting a need for a new systematisation of the literature.

The results show that the benefits of the SIA topic are growing, and without a doubt, companies need to equip themselves with good assessment tools. Managers must also anticipate the need for information by their stakeholders, and therefore, it is essential to identify an excellent reporting tool that may require dedicated efforts and procedures [56,57]. Based on this study’s preliminary evidence, and if supported by further research, business decision makers can improve the effects of their actions internally and externally, even when reflection on best practices is not perceived as urgent. The findings suggest that these micro-processes can be supported by an entrepreneurial attitude that allows business managers to regularly take stock and be ready to act quickly by being aware of their company’s financial and non-financial data, especially in a language that is clearly accessible. Too often, smaller companies entering the market do not have the time or resources to make these assessments, and this can lead to inefficiencies that last longer than necessary, resulting in wasted resources and poor returns, as well as reduced opportunities for learning and adapting practices.

As mentioned earlier, the OECD report discusses many hundreds of indices and ratings to assess ESGs that correspond to a similar number of companies providing this service, although there are only three main players in the market. The ESG models listed in our mapping are only a small part of the large number of rating systems that are rapidly developing in advisory firms and investment funds. It is therefore crucial for managers to equip themselves with professionals who know how to anticipate problems and manage this type of know-how.

6.3. Limitations and Future Research

The scenario demonstrated has strong illustrative and exploratory potential, and the steps identified in this study can be adapted to other contexts [58].

The purpose of our exploratory study is to provide insights that other scholars can draw upon and explore further in the theory development process. Therefore, this study invites scholars to investigate the transferability of our insights and provides several promising avenues for future research.

Our contribution has some limitations. First, SIA models have a fragmentation problem in their taxonomy, so it is possible that some models may not have been found, or others may have been created and not intercepted through the four databases searched. Particularly with regard to the grey literature, it is very difficult to capture the continued innovation around SIA models [59,60].

These findings provide the basis for providing support to the scientific research sector, third sector agents, investors and all stakeholders working with social entrepreneurs to better understand what research and SEs will need to focus on to generate social impact [61,62,63]. Researchers question whether the focus on social impact can generate transparency and accountability in all non-profit [64] but also for-profit contexts, as the current literature provides us with additional distinctions in this category: for impact and without impact.

Second, the listed models have not yet been investigated through a cluster analysis to identify key characteristics. Furthermore, the methodology adopted may be a limitation in that it requires some discretion on the part of the researchers and, consequently, introduces the potential for bias in conducting the analysis.

However, this paper offers quantitative results on the SIA model, whereas most studies focus on qualitative insights. Limitations arising from the methodology can be addressed in future research by, for example, extending the analysis to a different sample of reports or, even more importantly, supplementing the cluster identification with a field analysis that would allow for a deeper understanding of actual practices [4].

The findings highlight this study as an opportunity to direct future research to fill gaps in the literature. Since the SDGs are goals to be achieved by 2030 (2030 Agenda), evidence of these gaps can increase awareness of scientific production and thus facilitate the achievement of the goals. In this sense, the literature places SIA at the centre of social innovation [4].

Third, to reach more general conclusions, the 2030 goals towards which the world is racing seem to be set by large institutions and public bodies. This brings to light how impactful the work of global organisations is in providing direction for social impact innovation [65].

The generation of social impact creates a need for reporting on this data and thus for identifying good reporting tools on the global goals that humanity must now aim for.

In conclusion, with the aim of mapping SIA models, addressing these issues contributes to the achievement of sustainable goals, crystallises the academic studies in this field and demonstrates the evolution of the perception of assessment models in the literature. This research confirms that it plays a central role in the topic of the innovation-oriented social impact of the entire ecosystem. This condition increases accountability, transparency and stakeholder engagement. Stakeholders will be able to better understand the strong values of the company itself and all the partnerships that are normally created to achieve its goals, in line with SDG 17.

Author Contributions

Conceptualization, L.C., L.P.; methodology, L.C.; data curation, A.M.; validation, L.P., L.C.; writing—original draft preparation, L.C. (Section 3, Section 4 and Section 5), L.P. (Section 1, Section 2 and Section 5), D.I. (Section 6); writing—review and editing L.P., L.C.; resources, D.I., A.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

| SIA MODELS | |||

| 1 | AA1000AP | 47 | Logic model builder |

| 2 | Acumen Lean Data | 48 | LuxFLAG ESG Label |

| 3 | Acumen scorecard | 49 | Measuring impact framework |

| 4 | Anticipated Impact Measurement and Monitoring (AIMM) | 50 | Methodology for impact analysis and assessment |

| 5 | AtKisson compass assessment for investors | 51 | MetODD-SDG |

| 6 | Best available charitable option | 52 | MicroRate |

| 7 | Bridges Ventures Impact Radar | 53 | Movement above the US$1 a day threshold |

| 8 | CERISE-IDIA | 54 | MSCI ESG Ratings Methodology |

| 9 | Charity analysis framework | 55 | Ongoing Assessment of Social Impacts (OASIS) |

| 10 | Cost per impact | 57 | Outcome star |

| 11 | Cradle-to-cradle certification | 58 | Practical quality assurance system for small organisations (PQASSO)/Trusted Charity |

| 12 | Dalberg Approach | 59 | Progress out of poverty index |

| 13 | DTA Fit for purpose | 60 | Prove it! |

| 14 | Eco-mapping | 61 | Public value scorecard |

| 15 | EFQM | 62 | Quality first |

| 16 | EMAS | 63 | RobecoSam 3 step SDG Framework |

| 17 | Environmental, Social and Governance (ESG) Scores | 65 | SASB Standard |

| 18 | EPIC | 67 | SDG Impact Practice Standard |

| 19 | ESG Disclosure score | 68 | Social accounting and audit |

| 20 | ESG Relevance Score | 69 | Social Business Scorecard |

| 21 | ESG Risk Rating | 70 | Social enterprise balanced scorecard |

| 22 | European Impact Investing Luxembourg | 71 | Social enterprise mark |

| 23 | Expected return | 73 | Social Impact Measurement for Local Economies (SIMPLE) |

| 24 | Family of measures | 74 | Social rating |

| 25 | Finance Initiative Impact Radar | 75 | Social return assessment |

| 26 | FMO ESG Toolkits | 76 | Social return on investment |

| 27 | FTSE ESG Ratings | 77 | Social Value Maturity Index |

| 28 | Global Alliance for Banking on Values (GABV) | 78 | Social value metrics |

| 29 | Global Impact Investing Rating System (GIIRS) | 79 | Sopact-tool |

| 30 | GOGLA Impact Metrics | 80 | SPI4 |

| 31 | GRI sustainability reporting framework | 82 | Standard Ethics Rating (SER) |

| 32 | HIP Rating | 83 | Star social firm |

| 33 | HIPSO Harmonized Indicators for Private Sector Operations | 84 | Success measures data system |

| 34 | VALORIS method | 85 | The B impact rating system |

| 35 | Impact Analysis for Corporate Finance & Investments (Tool prototype) | 86 | The big picture |

| 36 | Impact Due Diligence Tools | 87 | The Committee on Sustainability Assessment (COSA) Methodology |

| 37 | Impact Management Project (IMP) Five Dimensions | 88 | The FINCA client assessment tool |

| 38 | Impact Multiple of Money (IMM) | 89 | The Impact Due Diligence Guide |

| 39 | Impact Risk Classification (IRC) | 90 | The SRI LABEL |

| 40 | Impact-Weighted Accounts | 91 | Third sector performance dashboard |

| 41 | Inrate ESG Impact Rating Methodology | 92 | TIMM |

| 42 | Inventory of Business Indicators (SDG Compass) | 94 | Trucost |

| 43 | IRIS + (and IRIS) | 96 | Volunteering impact assessment toolkit |

| 44 | ISS ESG Corporate Rating | 97 | Wallace assessment tool |

| 45 | ISS SDG Impact rating | 98 | Y Analytics |

| 46 | LM3 | ||

References

- OECD. Policy Brief on Social Impact Measurement for Social Enterprises. In Policies for Social Entrepreneurship; European Commission Luxembourg: Luxembourg, 2015; ISBN 978-92-79-47475-0. Available online: https://www.oecd.org/social/PB-SIM-Web_FINAL.pdf (accessed on 15 April 2021).

- Young, D.R.; Searing, E.A.; Brewer, C.V. The Social Enterprise Zoo: A Guide for Perplexed Scholars, Entrepreneurs, Philanthropists, Leaders, Investors, and Policymakers; Edward Elgar Publishing: Cheltenham, UK, 2016. [Google Scholar]

- OECD. International Migration Outlook 2018; OECD Publishing: Paris, France, 2018. [Google Scholar] [CrossRef]

- Tang, M.; Liao, H.; Wan, Z.; Herrera-Viedma, E.; Rosen, M.A. Ten Years of Sustainability (2009 to 2018): A Bibliometric Overview. Sustainability 2018, 10, 1655. [Google Scholar] [CrossRef]

- Clark, C.; Rosenzweig, W.; Long, D.; Olsen, S. Double Bottom Line Project Report: Assessing Social Impact in Double Bottom Line Ventures; Working Paper Series No. 13; University of California: Berkeley, CA, USA, 2004. [Google Scholar]

- Grieco, C.; Michelini, L.; Iasevoli, G. Measuring value creation in social enterprises: A cluster analysis of social impact assessment models. Nonprofit Volunt. Sect. Q. 2015, 44, 1173–1193. [Google Scholar] [CrossRef]

- Lyon, F.; Sepulveda, L. Mapping social enterprises: Past approaches, challenges and future directions. Soc. Enterp. J. 2009, 5, 83–94. [Google Scholar] [CrossRef] [Green Version]

- Then, V.; Schober, C.; Rauscher, O.; Kehl, K. Social Return on Investment Analysis; Springer: Berlin, Germany, 2017. [Google Scholar]

- Corvo, L.; Pastore, L. The Usefulness of Sharing Social Impact Data. Early Findings from an International Benchmarking on SROI Assessments. J. Entrep. Organ. Divers. (JEOD) Creat. Commons Attrib. 2020, 9, 45–61. [Google Scholar] [CrossRef]

- Massey, A.; Johnston-Miller, K. Governance: Public governance to social innovation? Policy Politics 2016, 44, 663–675. [Google Scholar] [CrossRef] [Green Version]

- Klemelä, J. Licence to operate: Social Return on Investment as a multidimensional discursive means of legitimating organisational action. Soc. Enterp. J. 2016, 12, 387–408. [Google Scholar] [CrossRef]

- Emerson, J. The Blended Value Proposition: Integrating Social and Financial Returns. Calif. Manag. Rev. 2003, 45, 35–51. [Google Scholar] [CrossRef] [Green Version]

- Maas, K.; Liket, K. Social impact measurement: Classification of methods. In Environmental Management Accounting and Supply Chain Management; Springer: Berlin/Heidelberg, Germany, 2011. [Google Scholar]

- Nicholls, A. Measuring Impact in Social Entrepreneurship: New Accountabilities to Stakeholders and Investors? ERSC Seminar, Local Government Research Unit: London, UK, 2005. [Google Scholar]

- Dietz, T. Theory and method in social impact assessment. Sociol. Inq. 1987, 57, 54–69. [Google Scholar] [CrossRef]

- Vanclay, F. Conceptual and methodological advances in social impact assessment. The international handbook of social impact assessment. Concept. Methodol. Adv. 2003, 1–9. [Google Scholar] [CrossRef]

- Bakar, A.A.; Osman, M.M.; Bachok, S.; Zen, I. Social impact assessment: How do the public help and why do they matter? Procedia-Soc. Behav. Sci. 2015, 170, 70–77. [Google Scholar] [CrossRef] [Green Version]

- Hervieux, C.; Voltan, A. Toward a systems approach to social impact assessment. Soc. Enterp. J. 2019, 15, 264–286. [Google Scholar] [CrossRef]

- Arvidson, M.; Lyon, F. Social Impact Measurement and Non-profit Organisations: Compliance, Resistance, and Promotion. Volunt. Int. J. Volunt. Nonprofit Organ. 2014, 25, 869–886. [Google Scholar] [CrossRef]

- Manzoor, F.; Wei, L.; Nurunnabi, M.; Subhan, Q.A.; Shah, S.I.A.; Fallatah, S. The Impact of Transformational Leadership on Job Performance and CSR as Mediator in SMEs. Sustainability 2019, 11, 436. [Google Scholar] [CrossRef] [Green Version]

- Porter, M.E.; Kramer, M.R. The Big Idea: Creating Shared Value. How to reinvent capitalism—And unleash a wave of innovation and growth. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Porter, M.E.; Hills, G.; Pfitzer, M.; Patscheke, S.; Hawkins, E. Measuring Shared Value: How to Unlock Value by Linking Business and Social Results; by FSG Creative Commons Attribution-NoDerivs 3.0. 2012. Available online: https://www.hbs.edu/ris/Publication%20Files/Measuring_Shared_Value_57032487-9e5c-46a1-9bd8-90bd7f1f9cef.pdf (accessed on 15 April 2021).

- Kozień, A. The Principle of Sustainable Development as the Basis for Weighing the Public Interest and Individual Interest in the Scope of the Cultural Heritage Protection Law in the European Union. Sustainability 2021, 13, 3985. [Google Scholar] [CrossRef]

- Emerson, J.; Wachowicz, J.; Chun, S. Social return on investment: Exploring aspects of value creation in the nonprofit sector. In Social Purpose Enterprises and Venture Philanthropy in the New Millennium; Investor Perspectives, REDF Workshop; REDF: San Francisco, CA, USA, 2000; Volume 2, pp. 130–173. Available online: https://redf.org/wp-content/uploads/REDF-Box-Set-Vol.-2-SROI-Paper-2000.pdf (accessed on 15 April 2021).

- Latané, B. The psychology of social impact. Am. Psychol. 1981, 36, 343. [Google Scholar] [CrossRef]

- Bergmann, T.; Utikal, H. How to Support Start-Ups in Developing a Sustainable Business Model: The Case of an European Social Impact Accelerator. Sustainability 2021, 13, 3337. [Google Scholar] [CrossRef]

- Clark, C.; Brennan, L. Entrepreneurship with social value: A conceptual model for performance measurement. Acad. Entrep. J. 2012, 18, 17. [Google Scholar]

- Yang, C.-L. Building a Performance Assessment Model for Social Enterprises-Views on Social Value Creation. Sci. J. Bus. Manag. 2014, 2, 1. [Google Scholar] [CrossRef]

- Ebrahim, A.S.; Rangan, V.K. The Limits of Nonprofit Impact: A Contingency Framework for Measuring Social Performance. SSRN Electron. J. 2010. [Google Scholar] [CrossRef] [Green Version]

- Bagnoli, L.; Megali, C. Measuring Performance in Social Enterprises. Nonprofit Volunt. Sect. Q. 2009, 40, 149–165. [Google Scholar] [CrossRef]

- Dart, R. The legitimacy of social enterprise. Nonprofit Manag. Leadersh. 2004, 14, 411–424. [Google Scholar] [CrossRef]

- Ruttman, R. New ways to invest for social and environmental impact. In Investing for Impact: How Social Entrepreneurship Is Redefining the Meaning of Return; Credit Suisse with Schwab Foundation for Social Entrepreneurship: Zurig/Davos, UK, 2012; Available online: https://www.longfinance.net/media/documents/cs_impactinvesting_2012.pdf (accessed on 15 April 2021).

- Esposito, P.; Brescia, V.; Fantauzzi, C.; Frondizi, R. Understanding Social Impact and Value Creation in Hybrid Organizations: The Case of Italian Civil Service. Sustainability 2021, 13, 4058. [Google Scholar] [CrossRef]

- Nicholls, A. ‘We do good things, don’t we?’: ‘Blended Value Accounting’ in social entrepreneurship. Account. Organ. Soc. 2009, 34, 755–769. [Google Scholar] [CrossRef]

- Nicholls, A. Institutionalizing social entrepreneurship in regulatory space: Reporting and disclosure by community interest companies. Account. Organ. Soc. 2010, 35, 394–415. [Google Scholar] [CrossRef]

- Di Fabio, A.; Peiroó, J.M. Human Capital Sustainability Leadership to Promote Sustainable Development and Healthy Organizations: A New Scale. Sustainability 2018, 10, 2413. [Google Scholar] [CrossRef] [Green Version]

- Esteves, A.M.; Franks, D.M.; Vanclay, F. Social impact assessment: The state of the art. Impact Assess. Proj. Apprais. 2012, 30, 34–42. [Google Scholar] [CrossRef]

- Richmond, B.J.; Mook, L.; Jack, Q. Social accounting for nonprofits: Two models. Nonprofit Manag. Leadersh. 2003, 13, 308–324. [Google Scholar] [CrossRef]

- Zappalà, G.; Lyons, M. Recent Approaches to Measuring Social Impact in the Third Sector: An Overview; Centre for Social Impact: Sydney, NSW, Australia, 2009; Available online: https://www.socialauditnetwork.org.uk/files/8913/2938/6375/CSI_Background_Paper_No_5_-_Approaches_to_measuring_social_impact_-_150210.pdf (accessed on 15 April 2021).

- Zamagni, S.; Venturi, P.; Rago, S. Valutare l’impatto sociale. La questione della misurazione nelle imprese sociali. Impresa Soc. 2015, 6, 77–97. [Google Scholar]

- Corvo, L.; Pastore, L. The challenge of Social Impact Bond: The state of the art of the Italian context. Eur. J. Islam. Financ. 2019. [Google Scholar] [CrossRef]

- Meneguzzo, M.; Galeone, P. La finanza sociale. In Pubblico, Privato, Non Profit: Le Prospettive Comuni in Europa e in Italia; Rubbettino: Soveria Mannelli, Italy, 2016. [Google Scholar]

- Biancone, P.P.; Radwan, M. Social Finance and Unconventional Financing Alternatives: An Overview. Eur. J. Islam. Financ. 2018. [Google Scholar] [CrossRef]

- Brown, A.; Swersky, A. The First Billion; The Boston Consulting Group, Big Society Capital: London, UK, 2012. [Google Scholar]

- Wilson, K.E. Social Investment: New Investment Approaches for Addressing Social and Economic Challenges. In OECD Science, Technology and Industry Policy Paper; No. 15; OECD Publishing: Paris, France, 2014; Available online: https://ssrn.com/abstract=2501247 (accessed on 15 April 2021).

- Aucamp, I.; Lombard, A. Can social impact assessment contribute to social development outcomes in an emerging economy? Impact Assess. Proj. Apprais. 2017, 36, 173–185. [Google Scholar] [CrossRef]

- Olsen, S.; Galimidi, B. Catalog of Approaches to Impact Measurement: Assessing Social Impact in Private Ventures; Rockfeller Foundation: New York, NY, USA, 2008; Available online: http://www.midot.org.il/Sites/midot/content/Flash/CATALOG%20OF%20APPROACHES%20TO%20IMPACT%20MEASUREMENT.pdf (accessed on 15 April 2021).

- Rinaldo, H. Getting Started in Social Impact Measurement: A Guide to Choosing How to Measure Social Impact; Norwich Guild: Norwich, UK, 2010; Available online: https://www.socialauditnetwork.org.uk/files/8113/4996/6882/Getting_started_in_social_impact_measurement_-_270212.pdf (accessed on 15 April 2021).

- Boffo, R.; Patalano, R. Esg Investing: Practices, Progress and Challenges; Technical Report; OECD: Paris, France, 2020. [Google Scholar]

- OECD. OECD Social Impact Investment 2019: The Impact Imperative for Sustainable Development; OECD Publishing: Paris, France, 2019. [Google Scholar]

- Faraudello, A.; Barreca, M.; Iannaci, D.; Lanzara, F. The Impact of Social Enterprises: A Bibliometric Analysis from 1991 to 2020. Int. J. Financ. Res. 2021, 12, 3. [Google Scholar] [CrossRef]

- Arce-Gomez, A.; Donovan, J.D.; Bedggood, R.E. Social impact assessments: Developing a consolidated conceptual framework. Environ. Impact Assess. Rev. 2015, 50, 85–94. [Google Scholar] [CrossRef]

- Spiess-Knafl, W.; Scheck, B. Impact Investing: Instruments, Mechanisms and Actors; Springer: Berlin, Germany, 2017. [Google Scholar]

- Bonilla-Alicea, R.J.; Fu, K. Systematic Map of the Social Impact Assessment Field. Sustainability 2019, 11, 4106. [Google Scholar] [CrossRef] [Green Version]

- Lenzo, P.; Traverso, M.; Salomone, R.; Ioppolo, G. Social Life Cycle Assessment in the Textile Sector: An Italian Case Study. Sustainability 2017, 9, 2092. [Google Scholar] [CrossRef] [Green Version]

- Biancone, P.P.; Secinaro, S.; Brescia, V.; Iannaci, D. Communication and Data Processing in Local Public Group: Transparency and Accountability. Int. J. Bus. Manag. 2018, 13, 20–37. [Google Scholar] [CrossRef] [Green Version]

- Biancone, P.; Secinaro, S.; Brescia, V.; Iannaci, D. The Popular Financial Reporting between Theory and Evidence. Int. Bus. Res. 2019, 12, 45. [Google Scholar] [CrossRef]

- Welch, E.W. The relationship between transparent and participative government: A study of local governments in the United States. Int. Rev. Adm. Sci. 2012, 78, 93–115. [Google Scholar] [CrossRef]

- Secinaro, S.; Calandra, D.; Petricean, D.; Chmet, F. Social Finance and Banking Research as a Driver for Sustainable Development: A Bibliometric Analysis. Sustainability 2020, 13, 330. [Google Scholar] [CrossRef]

- Baraibar-Diez, E.; Luna, M.; Odriozola, M.D.; Llorente, I. Mapping Social Impact: A Bibliometric Analysis. Sustainability 2020, 12, 9389. [Google Scholar] [CrossRef]

- Burdge, R.J. Benefiting from the practice of social impact assessment. Impact Assess. Proj. Apprais. 2003, 21, 225–229. [Google Scholar] [CrossRef]

- Mitzinneck, B.C.; Besharov, M.L. Managing Value Tensions in Collective Social Entrepreneurship: The Role of Temporal, Structural, and Collaborative Compromise. J. Bus. Ethics 2019, 159, 381–400. [Google Scholar] [CrossRef] [Green Version]

- Secinaro, S.; Corvo, L.; Brescia, V.; Iannaci, D. Hybrid organizations: A Systematic Review of the Current Literature. Int. Bus. Res. 2019, 12, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Barman, E. What is the Bottom Line for Nonprofit Organizations? A History of Measurement in the British Voluntary Sector. Volunt. Int. J. Volunt. Nonprofit Organ. 2007, 18, 101–115. [Google Scholar] [CrossRef]

- Aznar-Crespo, P.; Aledo, A.; Melgarejo-Moreno, J.; Vallejos-Romero, A. Adapting Social Impact Assessment to Flood Risk Management. Sustainability 2021, 13, 3410. [Google Scholar] [CrossRef]

Figure 1.

Articles per year.

{kind=link}

Table 1.

Searching and selection of articles from the Web of Science and Scopus databases, 1 December 2020.

Table 1.

Searching and selection of articles from the Web of Science and Scopus databases, 1 December 2020.

| Criteria for Searching and Selecting Articles | Web of Science Database | Scopus Database | Description |

|---|---|---|---|

| Searching articles using the keywords | 101 | 245 | The keywords used for searching are “Social impact assessment” OR “Social performance assessment” OR “Nonfinancial performance assessment” OR “Social return assessment” OR “ESG assessment” OR “Impact investing assessment” AND “Model*”. |

| Selecting documents only in the article and review category | 84 | 214 | Documents in the article and review category were selected since those in other categories are not peer-reviewed or academic contributions. |

| Selecting articles written in English | 82 | 207 | We selected documents that are written in English. |

| Adding articles from both databases | 289 | 82 articles from the Web of Science and 207 from Scopus databases were added to a single spreadsheet. | |

| Removing duplicate documents from the lists in the databases | 231 | 58 duplicates were removed. | |

| Checking Title, Abstract and Keywords | 187 | The focus of 44 articles was not SIA models. | |

| Adding more articles after checking the grey literature (NEF—New economic foundation; Tools and Resources for Assessing Social Impact—TRASI database) | 43 | An additional 43 articles coming from grey literature are focused on SIA models. | |

| Finalizing the number of articles considered for this study | 230 | Finally, we reached 230 articles for consideration in this study. | |

Table 2.

Clusters/groups of SIA models between 2004 and 2015.

| SIA Mapping | ||||||

|---|---|---|---|---|---|---|

| Groups/clusters | Clark et al. [5] | Olsen and Galimidi [47] | Zappalà and Lyons [39] | Rinaldo [48] | Maas and Liket [13] | Grieco et al. [6] |

| (1) Process models/methods | (1) Rating systems | (1) Social Accounting and Audit (SAA) | (1) Monitoring and evaluation tools | (1) Process methods | (1) Simple Social Quantitative | |

| (2) Impact models/methods | (2) Assessment systems | (2) Logic Models | (2) Quality tools | (2) Impact methods | (2) Holistic Complex | |

| (3) Monetisation models/methods | (3) Management systems | (3) Social Return on Investment (SROI) | (3) Outcome tools | (3) Monetisation | (3) Qualitative Screening | |

| - | - | - | - | - | (4) Management | |

Table 3.

Variables and references used by Grieco et al. [6].

Table 3.

Variables and references used by Grieco et al. [6].

| Grieco et al. [6] | |

|---|---|

| Variables | References |

| (1) Data typology | Nicholls [14] |

| (2) Impact typology | Rinaldo [48] |

| (3) Purpose | Clark et al. [5], Rinaldo [48], Maas and Liket [13] |

| (4) Model complexity | Zappalà and Lyons [39], Maas and Liket [13] |

| (5) Sector | Olsen and Galimidi [47] |

| (6) Time frame | Maas and Liket [13] |

| (7) Developer | Identified by the authors [6] |

Table 4.

Summary of SIA mapping (source: authors’ elaboration).

| Authors | Year of Publication | No. of Models Analysed | Emerging Patterns (No.) | Sources |

|---|---|---|---|---|

| Clark et al. [5] | 2004 | 9 | 3 | GL + I |

| Olsen and Galimidi [47] | 2008 | 25 | 3 | GL + I |

| Zappalà and Lyons [39] | 2009 | N.A. | 3 | AL |

| Rinaldo [48] | 2010 | 19 | 3 | GL |

| Maas and Liket [13] | 2011 | 30 | - | AGL + I |

| Grieco et al. [6] | 2015 | 76 | 4 | AGL |

Notes: GL: Grey literature; I: interviews; AL: Academic literature; AGL: Academic and grey literature.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Corvo, L.; Pastore, L.; Manti, A.; Iannaci, D. Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda. Sustainability 2021, 13, 4750. https://doi.org/10.3390/su13094750

AMA Style

Corvo L, Pastore L, Manti A, Iannaci D. Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda. Sustainability. 2021; 13(9):4750. https://doi.org/10.3390/su13094750

Chicago/Turabian StyleCorvo, Luigi, Lavinia Pastore, Arianna Manti, and Daniel Iannaci. 2021. "Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda" Sustainability 13, no. 9: 4750. https://doi.org/10.3390/su13094750

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.