The Theory of Reasoned Action to CSR Behavioral Intentions: The Role of CSR Expected Benefit, CSR Expected Effort and Stakeholders

1

College of Economics and Management, Nanjing University of Aeronautics and Astronautics, Nanjing 210016, China

2

Department of Information Management, Da-Yeh University, Changhua 51591, Taiwan

3

College of Management, Da-Yeh University, Changhua 51591, Taiwan

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(12), 4462; https://doi.org/10.3390/su10124462

Submission received: 23 September 2018

/

Revised: 22 November 2018

/

Accepted: 23 November 2018

/

Published: 28 November 2018

(This article belongs to the Special Issue Corporate Social Responsibility (CSR) in Developing Countries: Current Trends and Development)

Abstract

:During the past several years, many governments and non-government organizations in the world made efforts to promote policies and activities regarding corporate social responsibility and proposal of relevant regulations. However, scandals of international financial organizations and transnational corporations are enduring issues, which threaten to reduce social responsibility to a mere corporate slogan. This is not only the basis for sustainable operations but, also it is a vital academic issue. Understanding the factors behind the intention of a corporation’s social responsibility practice is a problem that governments and other governance organizations urgently need to solve and is also an issue that scholars and other relevant workers need to pay attention to and investigate. This study tries to discuss the behavioral intention behind social responsibility practices, and to point out exogenous factors, corresponding with theory of reasoned action, among the factors proposed by literature regarding corporate social responsibility. Then we apply structural equation modelling to analyze each hypothesis of the study. Finally, the results show several determinants which empirically affect behavioral intentions towards social responsibility practices. This study serves as a supplement for present literature, which did not clearly explain the reason why corporations hesitate to put social responsibility into action. In addition, although the theory of reasoned action was widely used to discuss the motive of various reasoned actions, the current study might be a pioneer in using theory of reasoned action to discuss the behavioral models for corporate social responsibility practices and discussing the applicability of the theory of reasoned action based on empirical data.

1. Introduction

Classical economic theory holds that a society can best determine its needs through the market as long as companies use resources as efficiently as possible to provide products and services that society needs; just by selling at the price consumers are willing to pay, the company has fulfilled its social responsibilities. In 1924, American scholar Oliver Sheldon proposed the concept of corporate social responsibility. He linked corporate social responsibility with the responsibility of business operators to meet the various human needs inside and outside the industry [1]. At the time, only considering economic factors, CSR was regarded as an instrumental purpose of obtaining economic benefits, thus providing employment opportunities and satisfying shareholder interests. This is the best example of fulfilling social responsibility. With changes of time, the definition of CSR became diversified, and relevant definitions, theories, and empirical studies have flourished. The most formal and widely-accepted definition comes from World Business Council for Sustainable Development (WBCSD), holding that Corporate Social Responsibility is the continuing commitment by business to behave ethically and to contribute to economic development while improving the quality of life of the workforce and their families, as well as the local community and society at large.

During the past several years, many governments and non-government organizations in the world have made efforts to promote policies and activities regarding CSR and to propose relevant regulations; however, the scandals of international financial organizations and transnational corporations never cease to exist. For example: Manipulation of Enron’s financial statements, WorldCom’s accounting scandal, British Petroleum’s oil spill, the manipulation of Libor by Barclays and Deutsche Bank, scandals of 2009 financial crisis, the Volkswagen emissions scandal, and Toshiba’s accounting scandal. Each of these episodes has threatened to invalidate CSR. The impacts and disquiets resulting from all these events, on the one hand, stirred the suspicion of corporate morality among governments and the public, especially the stakeholders; on the other hand, the public demanded that corporations take CSR as a real commitment. Corporations are expected not only to earn profits, but also to take a commitment to sustainable management and development for the public, the corporate organization, and the environment. As the result, understanding the factors behind the intention of corporate CSR practices is a problem that governments and other governance organizations urgently need to solve and is also an issue that scholars and other relevant workers need to pay attention to and investigate thoroughly.

As Porter and Kramer indicated [2], if a corporation can create a management strategy to achieve its social and economic targets at the same time, it will then acquire competitive advantages over its opponents. A corporation cannot only rely only on strategy, technology, and innovation to elevate its competiveness; in fact, putting ethics and responsibility into action is also a critical factor. By putting CSR into practice, a corporation not only fulfils its obligations and responsibilities to the society and environment, but also, according to related strategy studies, it enhances its competitive advantages and brand image, which might make operational performance, profits, and performance in the stock market better [3,4,5,6,7]. Recently many transnational corporations, such as IBM, Walmart, and Apple, etc., began to ask their suppliers to abide by the CSR requirements; only after that can they can become business partners [8].

Although lots of scholars have conducted studies about the factors behind a corporation’s intention to put CSR into practice, most of them merely discuss the relationship between CSR and a specific given factor [9]. In fact, there is a possibility that all of these factors simultaneously affect the CSR practices, which make studies considering only single factor seem insufficient. In addition, past studies mainly focused on pulling force, such as the benefits and competitiveness brought by CSR, and directly used corporate financial data to carry out the analyses. Actually, the key factor deciding if a corporation will put CSR into practice is individuals’ cognition, attitudes, and intentions towards the behavior, and so we need to switch our focus to the psychological mechanisms and processes between key CSR practitioners, reasons to accept practices, and behaviors of acceptance [10,11]. The Theory of Reasoned Action (TRA), a branch of social psychology, predicts an individual’s behavioral intention (BI) and the behavior of participating in or carrying out a specific activity according to his/her attitude and subjective norms. Lately TRA is widely accepted and has been successfully applied to studies in various fields.

Our study tries to discuss the behavioral intentions behind CSR practices and to point out exogenous factors corresponding with TRA among the factors proposed by the literature regarding CSR. The rest of this study includes five parts. The first is a review of prior related literature. Then, based on the literature, we propose an initial model which will then be further validated through empirical surveys. The last two parts are the discussion and conclusions.

2. Literature Review

2.1. Corporate Social Responsibility, CSR

There have been disagreements and controversies among scholars about the relationship between corporations and society for a long time. Bowen mentioned [12] the obligations of businessmen to pursue policies, to make decisions, or to follow lines of action which are desirable in terms of the objectives and values of our society. As McGuire further indicated [13], social responsibility urges corporations to assume certain responsibilities to society which extend beyond their economic and legal obligations. Carroll established aspects and priorities of CSR, and he thought that a business’s responsibilities to societal stakeholders include economic, legal, ethical, and philanthropic responsibilities [14]. The most formal and widely-accepted definition of CSR comes from the WBCSD; that is the view that corporate social responsibility is the continuing commitment by business to behave ethically and to contribute to economic development while improving quality of life for the workforce and their families, as well as for the local community and society at large. For example, improving working environments and benefits for employees, paying attention to human rights, avoiding sexual and racial discrimination, supporting rights and interests of consumers by pursuing quality products and services, averting insider trading, protecting small shareholders and creditors, sponsoring public interest activities in the community, addressing pollution, and paying attention to environmental and social innovations. In accordance with recent studies, our study defines CSR as the view that a corporation address the welfare of other stakeholders while pursuing wealth for shareholders; as the result, policies, measures, and procedures regarding commercial ethics, community involvement, environmental problems, corporate governance, human rights, markets, and working circumstances, etc., will be integrated into the management, supply chain, and decision-making process of the corporation [10,14,15].

CSR research can be mainly divided into three streams. The first one is testing the connection between CSR and financial or sales performance [4,16,17,18,19]; the connection between CSR and stock value [20,21,22,23]. The second takes CSR as the basis for building and maintaining good credits [24,25], as an instrument to win competitiveness [26,27,28], and as a way to win the loyalty of customers [29,30]. That is, CSR practices will develop positive attitudes of customers towards the corporation [31,32]. The final stream discusses the factors leading to CSR practices, which are relatively rare. For example, Powell, Davies and Norton discussed the impact of organizational climate on ethical empowerment and engagement with CSR [33]. Rupp and Mallory systemically review literature related to outcomes of practicing CSR [9], even though previous studies do not pay much attention to the intentions of CSR practice, especially from the top manager’s or business owner’s perspective.

2.2. Theory of Reasoned Action, TRA

When analyzing individual’s behaviors, the Intention Model is considered a great reference model, which claims that behavioral intention is closer to behavioral manifestation than attitude, belief, and affection; as the result, understanding of behavioral intention is a prerequisite for predicting or explaining an individual’s behaviors or the reasons for it. Thus, Fishbein and Ajzen developed TRA [34]. Since TRA was introduced, it has been applied to a variety of fields of social behavior, from marketing to application of information system [35,36] and E-commerce transactions [37], etc. In recent years, TRA has been extensively used to investigate the intention of ethical behaviors, such as treating drug abuse [38], predicting and explaining sexual behaviors of African adolescents [39], discussing the environment-protecting measures of the wine industry [40], predicting and explaining cyberbully behaviors by university students [41], studying factors behind moral behaviors of Information Technology (IT) [42], and discussing positive and negative factors behind corporate moral education [43]. Therefore, many scholars consider TRA to be the best indicator to predict and explain the intention behind a certain behavior.

In our study, behavioral intention refers to the degree to which the top manager or owner of business intends to put CSR into action, attitude towards CSR refers to the evaluation of value gained from CSR practices, and subjective norms are the social pressures perceived from CSR practices and the strength from the expectation of stockholders.

2.3. Role of CSR Expected Benefit, CSR Expected Effort and CSR Stakeholder

The motivations of CSR practices include not only obligations and responsibility to the society and environment, but also, according to studies on strategy, acquiring competitive advantages and brand images and improving corporate performance, profits and stock value [3,4,5,6,7]. Actually, corporate competitiveness is not merely decided by strategy, technology, and innovation, and fulfillment of ethics and responsibility is also critical. As Porter and Kramer indicated, if a corporation can create a management strategy to achieve its social and economic targets at the same time, it will acquire competitive advantages over its opponents [2].

In the view of stakeholders, Park and Ghauri [44] and Park, Chidlow and Choi [8] study whether the opinions of main and secondary stakeholders in overseas branches of Korean corporation can effectively affect CSR practices. CSR has roots in Social Stakeholder Theory, and the success of a CSR strategy depends on if it can satisfy the social stakeholders of the corporation, including consumers, employees, partners, government, media, social groups, and community [14]; in other words, if a corporation cannot satisfy the CSR standards or requirements of the social stakeholders, the latter will ask the corporation to fulfill its CSR. Thus, in the view of the whole idea and the push and pull framework, the advantages brought by CSR, e.g., financial benefits, improved credits, profit increase, and new market opportunities, is the pulling force; the concern, demand, or pressure from social stakeholders over the corporation is the pushing force. Both are important factors bearing weight on predicting or explaining CSR practices.

Applying stakeholder concept to company planning, corporate policy, and CSR study, Freeman thinks that CSR theories are usually based on Stakeholder Theory and define stakeholders as groups or individuals who can affect the execution of the organization’s policy, or whom are affected by the policy. These including direct stakeholders (i.e., shareholder, employee, customer, and supplier), advocates for environmental protections, competitors, government, media and other groups or individuals [45]. Through communication, negotiation, and cooperation with stakeholders, a corporation will find that stakeholders will affect the concept and model of CSR strategy [46]. A group of scholars, in the view of Stakeholder Theory, studied stakeholder influence on CSR; Carroll thinks that the corporation shall not only be responsible to shareholders, but also accountable to employees, society, suppliers, investors, and other stakeholders, because all stakeholders bear the risks of the corporate operations [14]. Thus, international organizations and local society also demand the corporation to be responsible not just to shareholders, but to all the stakeholders.

3. Research Methodology

3.1. Research Model

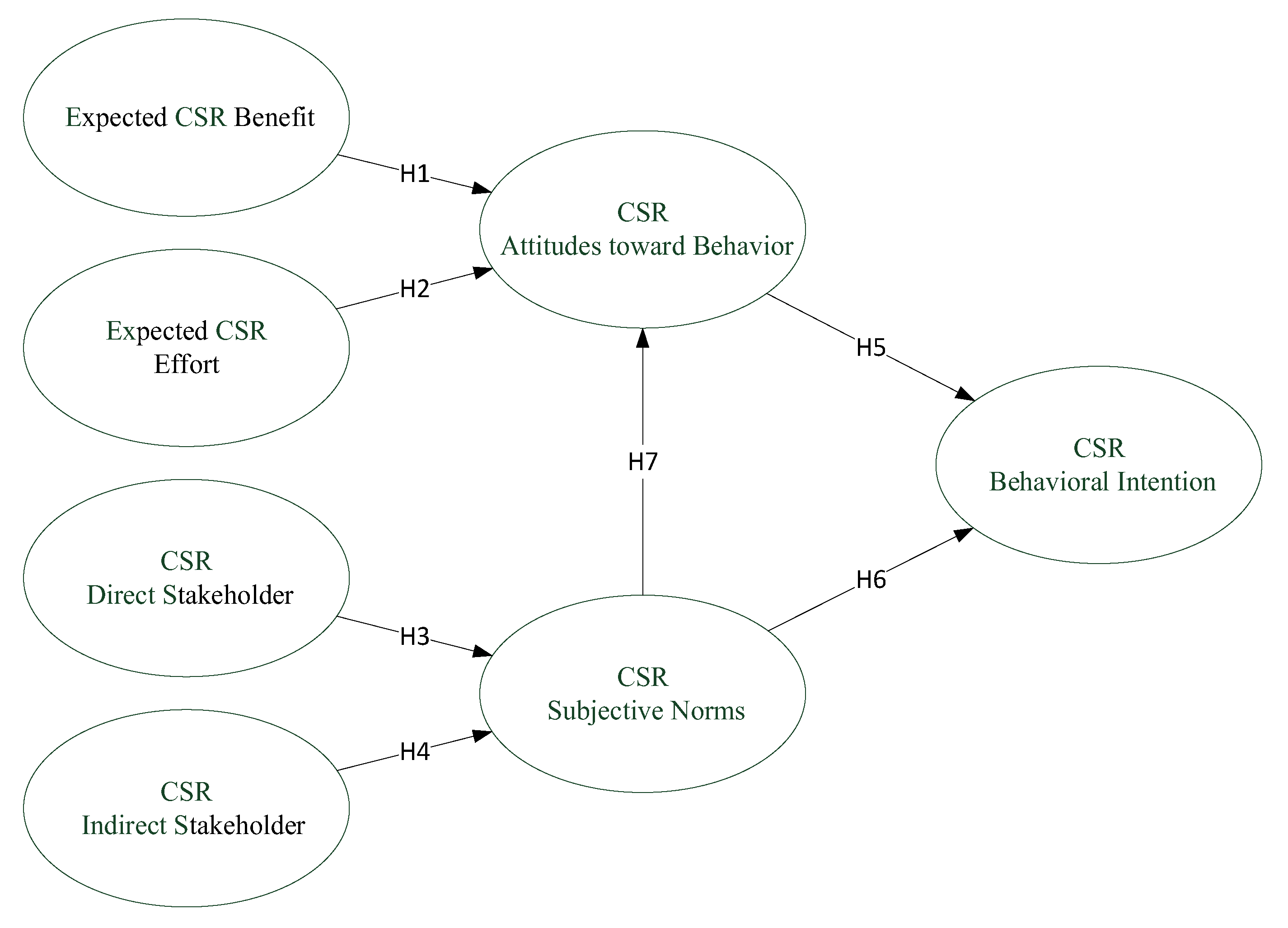

Our research model takes TRA as the core theory to investigate the behavioral intention of CSR practices (see Figure 1), and according to factors proposed by studies regarding CSR, we posit exogenous factors corresponding to TRA, such as replacing the two exogenous factors of the attitude aspect of TRA, behavioral belief and outcome evaluation, by expected benefit and expected effort. The main reason for this is that, while deciding if a corporation puts CSR into action, there are two concerns: Whether it needs to extensively change organizational regulations and institutional structures, i.e., the expected effort; and if it can acquire competitive advantages through CSR practices, i.e., the expected benefit. We replace the two exogenous factors of the subjective norms aspect of TRA, the normative belief and motivation to comply, by direct stakeholders and indirect stakeholders, and the main reason is that, while deciding whether a corporation puts CSR into action, the corporation’s leadership usually needs to take opinions of groups that have frequent face-to-face interactions with the corporation, i.e., direct stakeholders (such as consumers, managers, employees, and partners), and groups that have no or less frequent face-to-face interaction with the corporation, i.e., indirect stakeholders (including government, media, social organization, and community), into consideration. According to other scholars, the supervision by stakeholders is a vital factor to push a corporation to put CSR into action [47,48].

Research has shown that, under certain circumstances, behavioral intention is the best indicator for predicting individual’s behaviors [34,49,50], and that behavioral intention is highly correlated with actual behaviors, whose average correlation coefficient is up to 0.54 [51]. As the result, our study only discusses the behavioral intention of CSR rather than actual behaviors; by doing so, we can avoid a situation where our respondents take it as a CSR behavior survey and refuse to respond.

3.2. Hypotheses Regarding External Constructs

3.2.1. Impacts Caused by Corporate Expected CSR Benefit and Effort on Corporate Attitude towards Putting CSR into Action

Attitude towards a specific behavior refers to a positive or negative evaluation by an individual while performing the behavior. In our study, the specific behavior refers to CSR practice. Attitude towards behavior is a composite of behavioral belief and outcome evaluation; to be more specific, it is the attitude forming after the conceptualization of an individual’s evaluation of a specific behavior, and it is usually considered as a function of the individual’s salient beliefs towards the behavioral outcome. In other words, the individual’s attitude towards behavior equals behavioral belief, multiplied by the outcome evaluation. The so-called behavioral belief means belief in or evaluation of the possible outcome while conducting a specific behavior.

CSR practice is a social interaction between the corporation and all its stakeholders; therefore, we can clarify the interaction through Economic Exchange Theory. According to the theory, the corporation will rationally consider its self-interest and then decide whether to do something. The corporation needs to pay cost and time for CSR practices, such as education for employees, welfare, security and hygiene, love and protection for the earth, public interest activities, etc., and without expected benefits, most corporations will not (directly and indirectly) spend their precious resources towards these ends [52]. If a corporation’s leadership thinks that CSR practices will bring expected benefits, including visible rewards like performance elevation and new market developments, and invisible rewards like corporate image, competitiveness increase, and corporate evaluation, etc., then this might compel them to put CSR into action.

Some relevant studies show that CSR practice is not only to fulfill responsibility and obligation but also to enhance corporate competiveness and brand image and make sales and stock performance better [3]. In fact, increasing competitiveness should not merely depend on strategy, technology and innovation; realization of ethics and responsibility are also important. As Porter and Kramer said [2], if a corporation can create a management strategy to achieve its social and economic targets at the same time, it will acquire competitive advantages over its opponents. As to competition on the market, intra-industry competition recently has become common, and, to maintain their competiveness, the corporations carry out activities regarding CSR for the sake of establishing their positive images. In addition, many transnational corporations ask their suppliers to abide by CSR requirements before building a commercial partnership with the supplier.

According to Technology Acceptance Model (TAM), perceived ease of use means degree of ease to use a certain system perceived by an individual [53]. If an individual finds that an information system is easy to learn and operate, this belief in the ease of use will affect the individual’s attitude while using the system. Unified Theory of Acceptance and Use of Technology (UTAUT) [54] defines performance expectancy as the degree to which an individual believes that using the system will help him or her to attain gains in job performance, which is composed of perceived usefulness, extrinsic motivation, job-fit, relative advantage, and outcome expectation. Our study hypothesizes that while deciding on putting CSR into action, the corporation will carefully evaluate whether it needs to extensively change its present charter, institution, corporate culture, operation procedures, equipment, and technology, etc. Only when the corporation perceives that there is compatibility between the CSR practices and present operations and that there is no need to make an extensive change does putting CSR into action become an attractive option for the corporation. Expected effort will affect corporate attitudes towards CSR practices. Based on the analysis above, our study hypothesizes:

Hypothesis 1 (H1).

Expected benefits of CSR practice will significantly positively affect managers/owners’s attitudes towards CSR practices.

Hypothesis 2 (H2).

Expected efforts of CSR practices will significantly positively affect managers/owners’s attitude towards CSR practices.

3.2.2. Impacts Caused by Subjective Norms Based on Stakeholder’s Opinions on CSR Practice

The so-called subjective norm refers to the opinions of important individuals or groups over whether an individual should carry out a behavior [55]. According to past studies, different reference groups will have different impacts on the individual [56]. Our study defines subjective norms as the opinions and pressure from stakeholders perceived by the corporation while putting CSR into action, and as the degree to which the corporation complies with expectations of stakeholders. In the past, Many scholars implied, in the view of Stakeholder Theory and corporate management, that supervision over corporate commercial activities by stakeholders is a vital factor that elevates corporate intention to put CSR into action [47,48]. Donaldson and Davis, based on Stewardship Theory, clarify that the management should do the right thing rather than merely consider how a policy will influence performance, because it is impossible for a corporation to keep growing and surviving without the support of stakeholders [57]. Support from and identity of stakeholders is the basis for sustainable development, so the corporation will adapt its activities for the identities of stakeholders. According to all these studies, we find that a corporation needs the support and identities of stakeholders to achieve sustainable development [58]; thus, a corporation needs to actively put its CSR into action. Due to what we mentioned above, we know that being responsible for stakeholders is a prerequisite for a corporation, and a positive relationship between CSR and stakeholders is built in this way [59]. Our study posits that opinions and pressures from stakeholders over CSR practices positively affects subjective norms perceived by the corporation, and that different stakeholders will cause different interactions, which can be divided accordingly into direct stakeholder and indirect stakeholder actions. “Direct stakeholders” refers to the groups that have frequent face-to-face interactions with the corporation, such as consumers, managers, employees, and partners, who might produce behavioral norms for CSR practices. On the other hand, “indirect stakeholders” refers to groups that have no or less frequent face-to-face interaction with the corporation, including governments, media, social organizations, and the community, who might produce social norms for CSR practices. Our study thus hypothesizes:

Hypothesis 3 (H3).

Direct stakeholder’s perception about CSR has a positive impact on CSR subjective norms.

Hypothesis 4 (H4).

Indirect stakeholder’s perception about CSR has a positive impact on CSR subjective norms.

3.3. Hypotheses Regarding TRA Constructs

Impacts Caused by Corporate Attitude towards CSR Practice and Subjective Norm on Behavioural Intention

Commercial operation that is compatible with sustainable development serves as the basis for CSR; that is, the corporation should take into account, in addition to its own finance and operation situation, its impacts on the society and environment. CSR practice is not only fulfilling corporate responsibilities and obligations to society and environment, but also it is intended to enhance corporate brand image, competitive edge, and to improve sales and stock performance [3,4,7].

Ajzen and Fishbein claimed that behavioral intention refers to the possibility to carry out a specific behavior by an individual, which reflects the intention of the individual to carry out the behavior [60]. TRA makes a clear claim that attitudes towards behavior and subjective norms influence behavioral intention; the latter influences the actual behavior. Since TRA was developed, it has been successfully and widely applied to predict the intention of social behavior, including in marketing [36,61], use of information system, [35] and E-commerce transaction [37]. In recent years, TRA has been extensively used to investigate the intention of ethical behaviors, such as studying factors behind moral behaviors of IT [42] and discussing positive and negative factors behind corporate moral education [43]. According to these studies, the Theory of Planned Behavior is the best indicator to predict and explain the intention of a certain behavior [62].

Fishbein and Ajzen claim that there is no direct relation between attitudes towards objects and behavior; on the contrary, attitude towards behavior has a direct relation with the occurrence of behavior; that is, the more positive an individual’s attitude towards a behavior, the stronger the individual’s intention to perform the behavior [34]. At the same time, Ajzen points out that the more concrete and specific the attitude is, the more significant the relationship between attitude and behavior [55]. As the result, we can predict an individual’s intention to carry out a behavior by evaluating his/her attitude towards the behavior. Accordingly, a corporate leader’s attitudes towards CSR practices have a positive impact on their behavioral intention.

The Theory of Planned Behavior claims that the stronger the subjective norms perceived by an individual is, the stronger his/her intention is. If other individuals have a positive evaluation of CSR practices, this might strengthen the corporation’s behavioral intention. On the other hand, if other individuals do not approve CSR practices, or even have a negative evaluation, this might weaken the corporation’s behavioral intention. As the result, our study posits that the subjective norms perceived by a corporation will positively influence its intention to put CSR into action.

To be specific, attitude towards behaviors and subjective norms will affect the behavioral intention of an individual to carry out a specific behavior. In addition, Ajzen and Driver found that subjective norms have no direct effect on behavioral intention; on the contrary, it indirectly affects intention through attitude [63]. Our study posits that subjective norms will influence attitude while putting CSR into action. According to above studies, we assert:

Hypothesis 5 (H5).

A manager’s/owner’s attitude towards CSR has a positive impact on CSR behavioral intention.

Hypothesis 6 (H6).

Subjective norms perceived by a manager /owner have a positive impact on CSR behavioral intention.

Hypothesis 7 (H7).

Subjective norms perceived by a manager /owner have a positive impact on attitude towards CSR.

3.4. Research Instrument and Data

In order to design our own scale, we took the following scales as a reference, including expected CSR benefits from Bock and Kim [52]; expected CSR effort from Davis [53]; impacts caused by direct/indirect stakeholder from Park et al. [8]; and subjective norm, CSR attitude toward behavior, and CSR behavioral intention from Ajzen [64]. We deleted the items that, in the context of our study, are hard to be defined and measured according to our goals and the suitability; in this way, we make our questionnaire easier to respond to. We put the operational definition of each factor into Table 1. As for the content, all the items, except for the basic profile for the company, possess an interval scale, which, based on the Likert scale, can be divided into 7 levels: Strongly disagree, disagree, kind of disagree, neither agree nor disagree, kind of agree, agree, strongly agree. We respectively and orderly gave them 1–7 points as the standard for evaluation, on the premise that the intervals between each level are the same, and the higher the point, the stronger the degree to which the respondent identifies with the item.

To assure the meaning, representativeness, and completeness of the questionnaire, although all items in our study were taken from other literature, we discussed with other CSR and TRA experts about the content during the period between completing the draft and conducting pilot testing. In this way, we reviewed the content and adjusted obscure items. In order to establish the reliability of each construct, we conducted pilot testing, and the subjects were students of EMBA (most of them founders or owners of business) in two universities of central Taiwan. We sent 85 questionnaires and retrieved 70. There were 68 effective samples from pilot testing after removing 2 ineffective questionnaires. Cronbach’s α of each item was above 0.7, which means that the questionnaire is reliable to some extent. As for validity analysis, factor loading of each item is over 0.5, which meets the requirements and means that the design of questionnaire reflects the constructs in our study.

Our study adopts two survey methods, using both paper and online questionnaires. Online questionnaire surveys were conducted through the CSRone Platform, and the period for response was between 15 May and 30 June (one and a half months). On the other hand, the objects of paper questionnaire survey are the top 2000 Taiwanese corporations ranked by CommonWealth magazine in 2014, and we sent out the questionnaires through prepaid return envelopes with a period of response between 1 August and 30 September (two months).

4. Results

4.1. Descriptive Results

Our study takes both paper questionnaires (2000 questionnaires) and online questionnaires. We took back 63 online questionnaires and 204 paper questionnaires, which are 267 questionnaires in total. After removing 49 ineffective questionnaires that were incomplete and failed to pass reverse question tests, there were 218 effective questionnaires. To understand the sample distribution, we analyzed the background of respondents: Of the industrial background, the first is the electronics industry (23%); the second is others (18.81%); the third is the chemical industry (9.17%), which shows that electronics industry contains not only the majority of Taiwanese industries, but also is more concerned about CSR. Regarding working experience, 75.61% of the respondents have 5-year-and-above experience, which demonstrates that most of the respondents know the total development of the company quite well. Relating to occupation, 77.98% are managers, and 55.86% are from middle or high management, which shows that responding corporations are concerned about CSR issues; as the result, the information revealed by questionnaire is meaningful. Relating to company capital, the majority are companies whose capital is less than 2 billion and 500 million, whose employees are less than 500 persons, and whose history is more than 20 years.

4.2. Test Results

We first conducted reliability and validity analyses after collecting the questionnaires, which assured us that the results of statistical analysis based on the data are meaningful. So-called reliability means that the scale is reliable or has stability, which can be divided into external and internal consistency. To evaluate the external consistency, we need to conduct two or more measurements and evaluate if there is consistency between the results; however, we did not repeat the measurement. As the result, our study only discusses internal consistency; that is, if all the items for the same aspect are consistent. Our study adopts composite reliability (CR) to test the reliability of each aspect. According to the suggestions by Fornell and Larcker [65], the CR value of each aspect should be more than 0.7, and every aspect in our study reaches this standard, which shows that the scale used in is reliable to some extent. Validity means that an instrument can correctly measure the degree of characteristics and functions that the researcher wants to evaluate, or the correctness of the evaluation. Thus, the higher the validity of a questionnaire, the higher the ability of the result to demonstrate the true characteristics of the objects. Construct validity is a common instrument to evaluate validity, which refers to the ability of the content of an instrument to evaluate the necessary abstract concepts or characteristics. Convergent validity and discriminant validity are commonly applied to conduct an evaluation. The former evaluates the convergent degree of each aspect and whether correlated factors will return to the same aspect degree; the latter refers to the correlation between different factors or aspects, which is mainly used to evaluate if each item was appointed to suitable aspects. In our questionnaire, the factor loadings of all the items are above 0.5, as Table 2 shows; this means that our questionnaire possesses a good convergent validity [65]. By contrast, discriminant validity is used to test the differentiation degree of each item between different aspects; the higher the differentiation degree, the clearer the differentiation between aspects. Except for the AVE of the CSR direct stakeholder (0.495) which is bit of lower than 0.5, AVE values of the other aspects are larger than 0.5. We can confirm whether each aspect in our study has an acceptable discriminant validity by testing if the square of correlation coefficient between an aspect and the other aspects is smaller than the AVE value of the aspect, and as Table 3 shows, the AVE value of each aspect is larger than all the corresponding square of correlation coefficients in the same row of the table, which means that each aspect has a good discriminant validity.

4.3. Structural Model

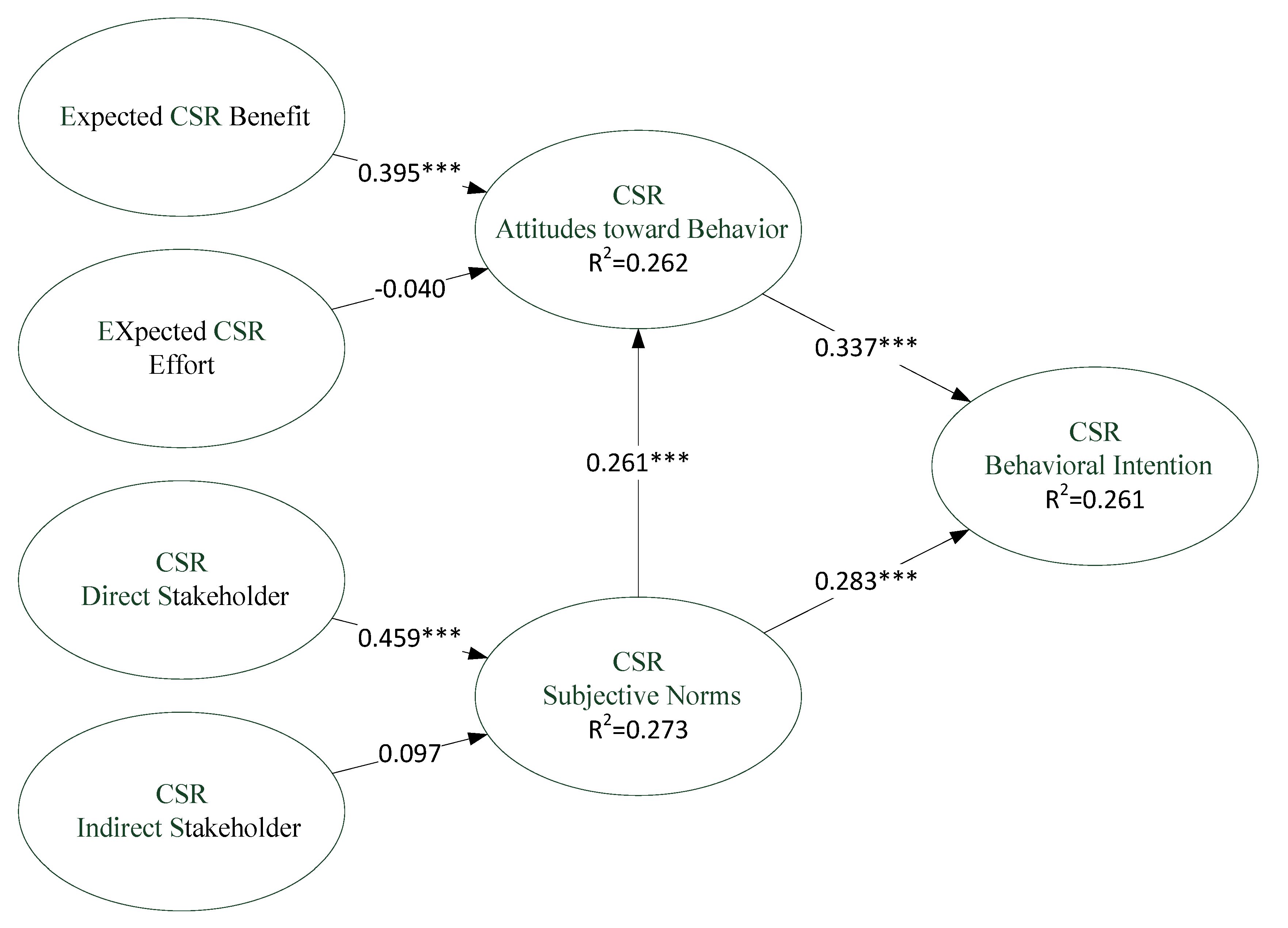

Our study adopts structural model to test the research model; in structural model, the strength of influence between variables can be revealed through testing the path coefficient (β). R2 shows how much variance can be explained by dependent variables, just like the explanation power in regression models. Figure 2 shows the result of partial least squares (PLS): The model fits (R2) show that it accounts for 26%, 27%, and 26% of the variance in CSR attitudes toward behavior, CSR subjective norms, and CSR behavioral intentions, respectively, which indicated an acceptable level of explanation power. Regarding the correlation between corporate attitude towards CSR practice and expected benefits, the β of H1 is 0.395 (p < 0.001); thus, H1 cannot be rejected. H2 was rejected, because corporate expected effort has a negative but insignificant impact on corporate attitude towards CSR. As for the correlation between subjective norms about CSR and corporate direct stakeholders, β of H3 is 0.459 (p < 0.001), which cannot be rejected. However, H4 was rejected, because the impact caused by indirect stakeholders on the subjective norms about CSR was insignificant. As for the impact caused by attitude, subjective norms, and behavioral intention to CSR practice, β of H5 is 0.337 (p < 0.001); β of H6 is 0.283 (p < 0.001); β of H7 is 0.261 (p < 0.001); thus, H5, H6 and H7 cannot be rejected.

5. Discussion

5.1. CSR Expected Benefit Vs. TRA Constructs Attitude

Expected benefit has a significant impact on corporate attitude towards CSR practices, which affects the behavioral intention. Thus, if a government wants to promote a successful CSR policy, it should not just regulate the corporations to perform CSR, otherwise CSR will not be taken seriously. After all, most corporations are pursuing economic interests, so they will not put CSR into action for nothing. According to Economic Exchange Theory, a corporation expects to elevate its credits, which might attract consumers, especially the individuals who identified with CSR practices, rather than for a feedback of visible interests. Among this, the government should play a leading role by providing a variety of policies and motivations inducing corporations to put CSR into action, and encouraging Taiwanese corporations to publish reports about CSR. In addition, the government can also cooperate with relevant organizations, such as the Taiwan Institute of Sustainable Energy, and commend the corporation for CSR practice, such as Taiwan Corporate Sustainability Awards. As for the media, it can enhance corporate visibility, attract great employees, and elevate production, which is beneficial to the acquirement of orders, brand-building, and sales, by making a positive coverage about CSR practices and praising the positive behavior by the corporations. This builds on good corporate image and facilitates accumulation of invisible assets for corporations.

5.2. CSR Expected Effort Vs. TRA Constructs Attitude

Expected effort cannot promote the correct attitude towards CSR practice and even has negative effects, although not significant, which means corporations require extra efforts to practice CSR or need a significant change in business operation and regulation. This demonstrates that the government did not provide sufficient assistance and instruction to promote CSR in order to reduce the effort of corporations to practice CSR. Taking Taiwan as an example, there are a lot of competent authorities regarding CSR, including the Ministry of Labor, Environmental Protection Administration, Ministry of Economic Affairs and Ministry of Justice, etc., and the CSR affairs are mainly the responsibility of Department of Investment Services, Ministry of Economic Affairs, which means that there is little coordination between departments or ministries.

To achieve the effects of unified management and actual fulfilment, we suggest taking other states that are more concerned about CSR as a reference, and to establish a unit specializing in conducting the coordination, the comprehensive CSR policy, and total CSR planning, and to unify the regulations regarding CSR which are compatible with corporation organization, such as the Federal Ministry of Labor and Social Affairs serving as the coordination unit in Germany and the CSR workshop held by the Department of Trade and Industry of UK. Simultaneously, we need to build a culture that is concerned about CSR.

5.3. CSR Direct Stakeholder Vs. TRA Constructs Subjective Norms

Corporate direct stakeholders have a significant impact on the subjective norms that affect behavioral intentions of CSR practices. In the past, most corporations considered CSR as a mere instrument to win publicity; thus, it cannot be effectively put into action. Therefore, a corporation can start from education for employees, especially the employees at the basic level, which tells them the reason why the corporation performs CSR and the benefits brought by CSR practices, and builds a culture that makes them identify with CSR. This pushes employees to actively participate in CSR activities and to become partners of the corporation. Reducing perception differences between individuals can help ensure that CSR is more than a mere slogan.

5.4. CSR Indirect Stakeholders Vs. TRA Constructs Subjective Norms

Corporate indirect stakeholders cannot influence the subjective norms about CSR. According to a study on the ways of presentation of website of Taiwanese corporations, most of Taiwanese corporations still think that the main function of a corporation is to sell product, and that the sales increase represents the increase of corporate value. Doubtlessly, sales increase or cost decrease is the main source for the increase of corporate value, but support from employees, consumers, suppliers, and local inhabitants can also elevate the value of a corporation. As the result, in the aspect of subjective norms, not only direct stakeholders serve as the main pushing force of CSR practices, but also indirect stakeholders can create shared value with the corporation [66]. Once corporate leadership understands this concept, it will realize how to create shared value with indirect stakeholders, which will include the value created by indirect stakeholders into the core value of corporation. Thus, Taiwanese corporate leaders will no longer view the corporation as a mere supplier of products, and will not narrow-mindedly treat suppliers, consumers, shareholders, and employees. If the company takes itself as a creator of value, it can consider everything in a more open-minded way, and it can observe not only how all stakeholders interact in competitive circumstances, but also how different stakeholders influence the corporate operation from political, social, and technological aspects [2].

5.5. Relationship between TRA Constructs

CSR is not a short-term and sales-orientation measure, but it is a long-term cultivation of the relationship between a corporation and consumers, which can impress the consumers and build the loyalty, and it has long-term impacts on the credits of the company or brand [67]. Thus, the corporate perception of CSR will affect the CSR practice. Our study proved H5, i.e., corporate attitude towards CSR significantly affect its behavioral intention, and this result matches what is claimed by Mazereeuw-van der Duijn Schouten et al. through discussing attitude towards CSR and behavioral intention based on Theory of Planned Behavior [68].

Generally speaking, an individual carries out a behavior because he/she thinks that the behavior is positive or he/she thinks that salient individuals or groups will expect him/her to do it [60]. Sandve and Øgaard proved that subjective norms have a significant impact through conducting selection experiment regarding CSR [69]. Our study proved that the stronger the subjective norms about CSR perceived by a corporation, the more evident the intention to put CSR into action; i.e., the more the social expectation felt by the corporation, the higher the intention to listen to the opinions of reference groups. The corporations tend to focus on most relevant physical interests and ignore the long-term benefits of social groups; as a result, the government should cultivate a corporate consciousness of CSR and encourage consumers to buy products from corporations that are concerned about CSR. The correct subjective norms among the public will be strengthened by the regulation/measures taken, and by public opinion inspired by the government and social groups.

TRA tells us that an individual’s attitude and the subjective norms perceived by him/her will affect his/her behavioral intention, and many scholars used this model to make precise predictions of consumers’ intentions to purchase a product. Our result tells that corporate perception of subjective norms affects its attitude towards CSR practices. Furthermore, both attitude towards a behavior and subjective norm about a behavior have a statistically significant impact on behavioral intention, which can account for 26.1% of variance. As the result, we demonstrate that TRA could be used to predict the participation in and performance of a specific activity by individuals and groups.

6. Conclusions and Limitation

As recent development of global economy, consciousness of environmental protection and human rights has been raised. Thus, CSR gradually became a global concern, and governments asked corporations to fulfil relevant commitments, which make CSR a trend under globalization and an issue bearing academic importance. Some corporations might be doubtful and hesitate due to the costs of CSR. Lots of scholars have conducted studies on corporations’ intentions behind CSR [70]. Recently, scandals of international financial organization and transnational corporations are widespread, and Taiwan also experiences problems like food security, environmental security, employees’ rights, corporate management, and corruption of senior management, which not only worsened corporate operation and image but also indicated that CSR might just be neglected. But why? In the past, few scholars paid attention to a corporation’s intention to conduct CSR, and some only focused on studying a single factor without taking the whole story into consideration [9,71]. Others focused on internal pulling forces, that is, the relative advantages brought by CSR, and directly carried out studies based on corporate financial data without empirical evidence. TRA uses an individual’s attitude and subjective norms to predict his/her behavioral intention and behavior, such as participating in or carrying out a specific activity, and it is now widely accepted and successfully applied to studies in various fields. Based on TRA, along with studies regarding relevant factors, our study set out to construct a comprehensive model for understanding corporate behavioral intention towards CSR, and we apply structural equation modeling to analyze each hypothesis of our study. Generally speaking, our study serves as a supplement for the present literature, which did not clearly explain the reason why corporations hesitate while putting CSR into action. Although TRA was widely used to discuss the motive of various reasoned actions, our study might be a pioneer in using TRA to discuss the behavioral model for CSR practices and discussing the applicability of TRA based on empirical data.

The response rate was quite low, because CSR practice is not popular in all businesses, so few managers are willing to fill out questionnaires. In addition, it is not easy to reach top managers to fill out questionnaires. Thus, we suggest further studies could collect data through more qualitative research methods, such as observing a corporation’s activities, strategies, and specific behaviors through in-depth interviews.

Author Contributions

For research articles with several authors, a short paragraph specifying their individual contributions must be provided. The following statements should be used “conceptualization, M.C., L.C.T. and C.F.K.; methodology, C.F.K.; software, C.F.K.; validation, L.C.T. and C.F.K.; formal analysis, C.F.K.; investigation, C.Y.H.; resources, C.Y.H.; data curation, C.Y.H.; writing—original draft preparation, L.C.T. and C.F.K.; writing—review and editing, C.F.K.; visualization, C.F.K.; supervision, M.C.; project administration, L.C.T.; funding acquisition, M.C.

Funding

This research was funded by The National Social Science Fund of China, grant number17BGL055 and Ministry of Science and Technology of Taiwan, grant number 104-2221-E-212 -006 -MY2, 107-2410-H-212-001.

Acknowledgments

The authors would like to thank Editors and four reviewers for many helpful comments and suggestions.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Sheldon, O. The Philosophy of Management; Sir Isaac Pitman and Sons Ltd.: London, UK, 1924; pp. 70–99. [Google Scholar]

- Porter, M.; Kramer, M. Strategy and society: The link between corporate social responsibility and competitive advantage. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Lee, M.D.P. A review of the theories of corporate social responsibility: Its evolutionary path and the road ahead. Int. J. Manag. Rev. 2008, 10, 53–73. [Google Scholar] [CrossRef]

- Mikołajek-Gocejna, M. The relationship between corporate social responsibility and corporate financial performance—Evidence from empirical studies. Comp. Econ. Res. 2016, 19, 67–84. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Org. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Perrini, F.; Pogutz, S.; Tencati, A. Corporate social responsibility in Italy: State of the art. J. Bus. Strateg. 2006, 23, 65. [Google Scholar]

- Wang, H.; Tong, L.; Takeuchi, R.; George, G. Corporate social responsibility: An overview and new research directions thematic issue on corporate social responsibility. Acad. Manag. J. 2016, 59, 534–544. [Google Scholar] [CrossRef]

- Park, B.I.; Chidlow, A.; Choi, J. Corporate social responsibility: Stakeholders influence on MNEs’ activities. Int. Bus. Rev. 2014, 23, 966–980. [Google Scholar] [CrossRef]

- Rupp, D.E.; Mallory, D.B. Corporate social responsibility: Psychological, person-centric, and progressing. Annu. Rev. Organ. Psychol. Organ. Behav. 2015, 2, 211–236. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility: A review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Wang, Q.; Dou, J.; Jia, S. A meta-analytic review of corporate social responsibility and corporate financial performance: The moderating effect of contextual factors. Bus. Soc. 2016, 55, 1083–1121. [Google Scholar] [CrossRef]

- Bowen, H.R. Social Responsibilities of the Businessman; University of Iowa Press: Iowa City, IA, USA, 2013. [Google Scholar]

- McGuire, J.W. Business and Society; McGraw-Hill: New York, NY, USA, 1963. [Google Scholar]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Tsoutsoura, M. Corporate Social Responsibility and Financial Performance; UC Berkeley: Berkeley, CA, USA, 2004. [Google Scholar]

- Luo, X.; Bhattacharya, C.B. Corporate social responsibility, customer satisfaction, and market value. J. Mark. 2006, 70, 1–18. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Sofian, S.; Saeidi, P.; Saeidi, S.P.; Saaeidi, S.A. How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. J. Bus. Res. 2015, 68, 341–350. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef] [Green Version]

- Høvring, C.M. Corporate social responsibility as shared value creation: Toward a communicative approach. Corp. Commun. 2017, 22, 239–256. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.B. Corporate social responsibility in the multinational enterprise: Strategic and institutional approaches. J. Int. Bus. Stud. 2006, 37, 838–849. [Google Scholar] [CrossRef] [Green Version]

- Min, M.; Desmoulins-Lebeault, F.; Esposito, M. Should pharmaceutical companies engage in corporate social responsibility? J. Manag. Dev. 2017, 36, 58–70. [Google Scholar] [CrossRef]

- Shiu, Y.M.; Yang, S.L. Does engagement in corporate social responsibility provide strategic insurance-like effects? Strateg. Manag. J. 2017, 38, 455–470. [Google Scholar] [CrossRef]

- Keh, H.T.; Xie, Y. Corporate reputation and customer behavioral intentions: The roles of trust, identification and commitment. Ind. Mark. Manag. 2009, 38, 732–742. [Google Scholar] [CrossRef]

- Kang, C.; Germann, F.; Grewal, R. Washing away your sins? Corporate social responsibility, corporate social irresponsibility, and firm performance. J. Mark. 2016, 80, 59–79. [Google Scholar] [CrossRef]

- Bansal, P.; Hunter, T. Strategic explanations for the early adoption of ISO 14001. J. Bus. Ethics 2003, 46, 289–299. [Google Scholar] [CrossRef]

- Bansal, P.; Clelland, I. Talking trash: Legitimacy, impression management, and unsystematic risk in the context of the natural environment. Acad. Manag. J. 2004, 47, 93–103. [Google Scholar]

- Khanna, M.; Anton, W.R.Q. What is driving corporate environmentalism: Opportunity or threat? Corp. Environ. Strategy 2002, 9, 409–417. [Google Scholar] [CrossRef]

- Martínez, P.; del Bosque, I.R. CSR and customer loyalty: The roles of trust, customer identification with the company and satisfaction. Int. J. Hosp. Manag. 2013, 35, 89–99. [Google Scholar] [CrossRef]

- Walsh, G.; Bartikowski, B. Exploring corporate ability and social responsibility associations as antecedents of customer satisfaction cross-culturally. J. Bus. Res. 2013, 66, 989–995. [Google Scholar] [CrossRef]

- Brown, T.J.; Dacin, P.A. The company and the product: Corporate associations and consumer product responses. J. Mark. 1997, 61, 68–84. [Google Scholar] [CrossRef]

- Sen, S.; Bhattacharya, C.B. Does doing good always lead to doing better? Consumer reactions to corporate social responsibility. J. Mark. Res. 2001, 38, 225–243. [Google Scholar] [CrossRef]

- Powell, S.M.; Davies, M.A.; Norton, D. Impact of organizational climate on ethical empowerment and engagement with corporate social responsibility (CSR). J. Brand Manag. 2013, 20, 815–839. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Belief, Attitude, Intention and Behavior: An Introduction to Theory and Research; Addison-Wesley, Reading: Boston, MA, USA, 1975. [Google Scholar]

- Mishra, D.; Akman, I.; Mishra, A. Theory of reasoned action application for green information technology acceptance. Comput. Hum. Behav. 2014, 36, 29–40. [Google Scholar] [CrossRef]

- Oliver, R.L.; Bearden, W.O. Crossover effects in the theory of reasoned action: A moderating influence attempt. J. Consum. Res. 1985, 12, 324–340. [Google Scholar] [CrossRef]

- Korzaan, M.L. Going with the flow: Predicting online purchase intentions. J. Comput. Inf. Syst. 2003, 43, 25–31. [Google Scholar]

- Roberto, A.J.; Shafer, M.S.; Marmo, J. Predicting substance-abuse treatment providers’ communication with clients about medication assisted treatment: A test of the theories of reasoned action and planned behavior. J. Subst. Abuse Treat. 2014, 47, 307–313. [Google Scholar] [CrossRef] [PubMed]

- Doswell, W.M.; Braxter, B.J.; Cha, E.; Kim, K.H. Testing the theory of reasoned action in explaining sexual behavior among African American young teen girls. J. Pediatr. Nurs. 2011, 26, e45–e54. [Google Scholar] [CrossRef] [PubMed]

- Marshall, R.S.; Akoorie, M.E.; Hamann, R.; Sinha, P. Environmental practices in the wine industry: An empirical application of the theory of reasoned action and stakeholder theory in the United States and New Zealand. J. World Bus. 2010, 45, 405–414. [Google Scholar] [CrossRef]

- Doane, A.N.; Pearson, M.R.; Kelley, M.L. Predictors of cyberbullying perpetration among college students: An application of the theory of reasoned action. Comput. Hum. Behav. 2014, 36, 154–162. [Google Scholar] [CrossRef]

- Leonard, L.N.; Cronan, T.P.; Kreie, J. What influences IT ethical behavior intentions—Planned behavior, reasoned action, perceived importance, or individual characteristics? Inf. Manag. 2004, 42, 143–158. [Google Scholar] [CrossRef]

- Baden, D. Look on the bright side: A comparison of positive and negative role models in business ethics education. Acad. Manag. Learn. Educ. 2014, 13, 154–170. [Google Scholar] [CrossRef]

- Park, B.I.; Ghauri, P.N. Determinants influencing CSR practices in small and medium sized MNE subsidiaries: A stakeholder perspective. J. World Bus. 2015, 50, 192–204. [Google Scholar] [CrossRef]

- Freeman, R.E. Stakeholder Management: Framework and Philosophy; Pitman: Mansfield, MA, USA, 1984. [Google Scholar]

- Bendell, J. In whose name? The accountability of corporate social responsibility. Dev. Pract. 2005, 15, 362–374. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Jackson, G. The cross-national diversity of corporate governance: Dimensions and determinants. Acad. Manag. Rev. 2003, 28, 447–465. [Google Scholar] [CrossRef]

- Driver, C.; Thompson, G. Corporate governance and democracy: The stakeholder debate revisited. J. Manag. Gov. 2002, 6, 111–130. [Google Scholar] [CrossRef]

- Steel, R.P.; Ovalle, N.K. A review and meta-analysis of research on the relationship between behavioral intentions and employee turnover. J. Appl. Psychol. 1984, 69, 673–686. [Google Scholar] [CrossRef]

- Triandis, H.C. Interpersonal Behavior; Brooks/Cole Pub. Co.: Salt Lake City, UT, USA, 1977. [Google Scholar]

- Sheppard, B.H.; Hartwick, J.; Warshaw, P.R. The theory of reasoned action: A meta-analysis of past research with recommendations for modifications and future research. J. Consum. Res. 1988, 15, 325–343. [Google Scholar] [CrossRef]

- Bock, G.-W.; Kim, Y.-G. Breaking the myths of rewards: An exploratory study of attitudes about knowledge sharing. In Proceedings of the PACIS 2001 Proceedings, Seoul, Korea, 20–22 June 2001; p. 78. [Google Scholar]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behavior. Org. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Burnkrant, R.E.; Page, T.J., Jr. The structure and antecedents of the normative and attitudinal components of Fishbein’s theory of reasoned action. J. Exp. Soc. Psychol. 1988, 24, 66–87. [Google Scholar] [CrossRef]

- Donaldson, L.; Davis, J.H. CEO Governance and Shareholder Returns: Agency Theory or Stewardship Theory; Australian Graduate School of Management, University of New South Wales: Randwick, Australia, 1990. [Google Scholar]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Acc. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Freeman, R.E. Stakeholder theory and corporate responsibility: Some practical questions. In 3rd Annual Colloquium of the European Academy of Business in Society; Vlerick Leuven Gent Management School: Gent, Belgium, 2004. [Google Scholar]

- Ajzen, I.; Fishbein, M. Understanding Attitudes and Predicting Social Behavior; Prentice-Hall: Englewood Cliffs, NJ, USA, 1980. [Google Scholar]

- Warshaw, P.R. A new model for predicting behavioral intentions: An alternative to Fishbein. J. Mark. Res. 1980, 17, 153–172. [Google Scholar] [CrossRef]

- Hagger, M.S.; Chatzisarantis, N.L.; Biddle, S.J. A meta-analytic review of the theories of reasoned action and planned behavior in physical activity: Predictive validity and the contribution of additional variables. J. Sport Exerc. Psychol. 2002, 24, 3–32. [Google Scholar] [CrossRef]

- Ajzen, I.; Driver, B.L. Application of the theory of planned behavior to leisure choice. J. Leis. Res. 1992, 24, 207–224. [Google Scholar] [CrossRef]

- Ajzen, I. Perceived behavioral control, self-efficacy, locus of control, and the theory of planned behavior. J. Appl. Soc. Psychol. 2002, 32, 665–683. [Google Scholar] [CrossRef]

- Fornell, C.R.; Larcker, F.F. Structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–51. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Marin, L.; Ruiz, S.; Rubio, A. The role of identity salience in the effects of corporate social responsibility on consumer behavior. J. Bus. Ethics 2009, 84, 65–78. [Google Scholar] [CrossRef]

- Mazereeuw-van der Duijn Schouten, C.; Graafland, J.; Kaptein, M. Religiosity, CSR attitudes, and CSR behavior: An empirical study of executives’ religiosity and CSR. J. Bus. Ethics 2014, 123, 437–459. [Google Scholar] [CrossRef]

- Sandve, A.; Øgaard, T. Exploring the interaction between perceived ethical obligation and subjective norms, and their influence on CSR-related choices. Tour. Manag. 2014, 42, 177–180. [Google Scholar] [CrossRef]

- Skouloudis, A.; Evangelinos, K. Exogenously driven CSR: Insights from the consultants’ perspective. Bus. Ethics Eur. Rev. 2014, 23, 258–271. [Google Scholar] [CrossRef]

- Skouloudis, A.; Avlonitis, G.J.; Malesios, C.; Evangelinos, K. Priorities and perceptions of corporate social responsibility: Insights from the perspective of Greek business professionals. Manag. Decis. 2015, 53, 375–401. [Google Scholar] [CrossRef]

Figure 1.

The Research Model.

Figure 2.

Results of the PLS Analysis. *** p < 0.001.

{kind=link}

{kind=link}

Table 1.

Operational Definition of Each Construct & Content of Questionnaire.

| Constructs | Operational Definition | Questionnaire Item/Reference |

|---|---|---|

| Expected CSR Benefit | Manager/owner believes that it can acquire visible or invisible rewards through CSR practices. | EB01: CSR brings economic benefits. EB02: CSR elevates value of corporate product or service. EB03: CSR is beneficial to develop new market or enlarge market. [52] |

| Expected CSR Effort | Manager/owner believes that CSR practice does not need to extensively change organizational regulation and institution. | EE01: CSR will not change corporate organization and structure. EE02: CSR is in conformity with corporate culture. EE03: CSR is understandable. [53] |

| CSR Direct Stakeholder | Degree of impacts caused by groups that have frequent interaction with the corporation on perception of CSR practice. | DS01: Consumers are concerned about social problems such as corporate charitable donation. DS02: Corporate manager and employees take CSR as a vital instrument to create corporate value. DS03: Corporate manager and employees believe that corporation needs to make a donation to state, society, and community. DS04: Corporate manager and employees think that ethnics and CSR is vital for corporation to perform. DS05: Investors tend to invest corporate that puts CSR into action [8]. |

| CSR Indirect Stakeholder | Degree of impacts caused by groups that have no or less frequent interaction with the corporation on perception of CSR practice. | IS01: Government can establish effective regulations and encourage corporation to elevate quality of its product and service. IS02: Comparing with other states, public media in Taiwan is more concerned about social role played by corporation. IS03: Community hopes that corporation involves community activities and makes contribution to development of community through non-financial way. IS04: Non-governmental organization can pay attention to and effectively supervise corporate activities. [8] |

| CSR Subjective Norm | Degree of impacts on corporation caused by CSR practice. | SN01: All corporation’s stakeholders like CSR practice. SN02: All corporation’s stakeholders acknowledge CSR practice. SN03: All corporation’s stakeholders support CSR practice. SN04: All corporation’s stakeholders expect CSR practice. [64] |

| CSR Attitude toward Behavior | Manager/owner’s evaluation of CSR practices. | AB01: Putting CSR into action is good. AB02: Putting CSR into action is worthwhile. AB03: Putting CSR into action is wise. [64] |

| CSR Behavioral Intention | Degree of manager/owner’s intention to CSR practices. | BI01: Corporate is glad to put CSR into action. BI02: Corporate wants to put CSR into action. BI03: Corporate do its effort to put CSR into action. BI04: Corporate is glad to recommend other corporates to put CSR into action. [64] |

Table 2.

Construct Reliability and Validity.

| Construct | Indicators | Loadings | CR | AVE |

|---|---|---|---|---|

| Expected CSR benefit | EB01 | 0.805 *** | 0.898 | 0.746 |

| EB02 | 0.92 *** | |||

| EB03 | 0.864 *** | |||

| Expected CSR effort | EE01 | 0.681 *** | 0.75 | 0.504 |

| EE02 | 0.73 *** | |||

| EE03 | 0.722 *** | |||

| CSR direct stakeholder | DS01 | 0.647 *** | 0.829 | 0.495 |

| DS02 | 0.704 *** | |||

| DS03 | 0.748 *** | |||

| DS04 | 0.804 *** | |||

| DS05 | 0.595 *** | |||

| CSR indirect stakeholder | IS01 | 0.7 *** | 0.842 | 0.572 |

| IS02 | 0.828 *** | |||

| IS03 | 0.705 *** | |||

| IS04 | 0.785 *** | |||

| CSR subjective norms | SN01 | 0.843 *** | 0.903 | 0.702 |

| SN02 | 0.887 *** | |||

| SN03 | 0.914 *** | |||

| SN04 | 0.85 *** | |||

| CSR attitudes toward behavior | AB01 | 0.813 *** | 0.928 | 0.764 |

| AB02 | 0.893 *** | |||

| AB03 | 0.896 *** | |||

| CSR behavioral intention | BI01 | 0.852 *** | 0.902 | 0.754 |

| BI02 | 0.849 *** | |||

| BI03 | 0.863 *** | |||

| BI04 | 0.783 *** |

Notes: CR = composite reliability; AVE = average variance extracted. *** p < 0.001. Notes: please refers to Table 1 for indicators.

Table 3.

Square of Correlation Between Constructs.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|

| 1. Expected CSR benefit | 0.746 | ||||||

| 2. Expected CSR effort | 0.112 | 0.504 | |||||

| 3. CSR direct stakeholder | 0.207 | 0.117 | 0.495 | ||||

| 4. CSR indirect stakeholder | 0.254 | 0.092 | 0.352 | 0.572 | |||

| 5. CSR subjective norms | 0.143 | 0.199 | 0.253 | 0.124 | 0.702 | ||

| 6. CSR attitudes toward behavior | 0.076 | 0.110 | 0.266 | 0.136 | 0.161 | 0.764 | |

| 7. CSR behavioral intention | 0.204 | 0.031 | 0.288 | 0.147 | 0.187 | 0.126 | 0.754 |

Notes: Numbers on the diagonal (in boldface) are the average variance extracted. Other numbers are the square of correlation.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Mi, C.; Chang, F.; Lin, C.; Chang, Y. The Theory of Reasoned Action to CSR Behavioral Intentions: The Role of CSR Expected Benefit, CSR Expected Effort and Stakeholders. Sustainability 2018, 10, 4462. https://doi.org/10.3390/su10124462

AMA Style

Mi C, Chang F, Lin C, Chang Y. The Theory of Reasoned Action to CSR Behavioral Intentions: The Role of CSR Expected Benefit, CSR Expected Effort and Stakeholders. Sustainability. 2018; 10(12):4462. https://doi.org/10.3390/su10124462

Chicago/Turabian StyleMi, Chuanmin, FangKai Chang, ChingTorng Lin, and YuHsuan Chang. 2018. "The Theory of Reasoned Action to CSR Behavioral Intentions: The Role of CSR Expected Benefit, CSR Expected Effort and Stakeholders" Sustainability 10, no. 12: 4462. https://doi.org/10.3390/su10124462

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.