Effects of IPO Offer Price Ranges on Initial Subscription, Initial Turnover and Ownership Structure—Evidence from Indian IPO Market

Abstract

:1. Introduction

2. Literature Review & Hypotheses Development

2.1. Literature Review

2.1.1. IPO Subscription

2.1.2. Initial Trading (Listing Day Trading)—First Day Trading Ratio (FDTR)

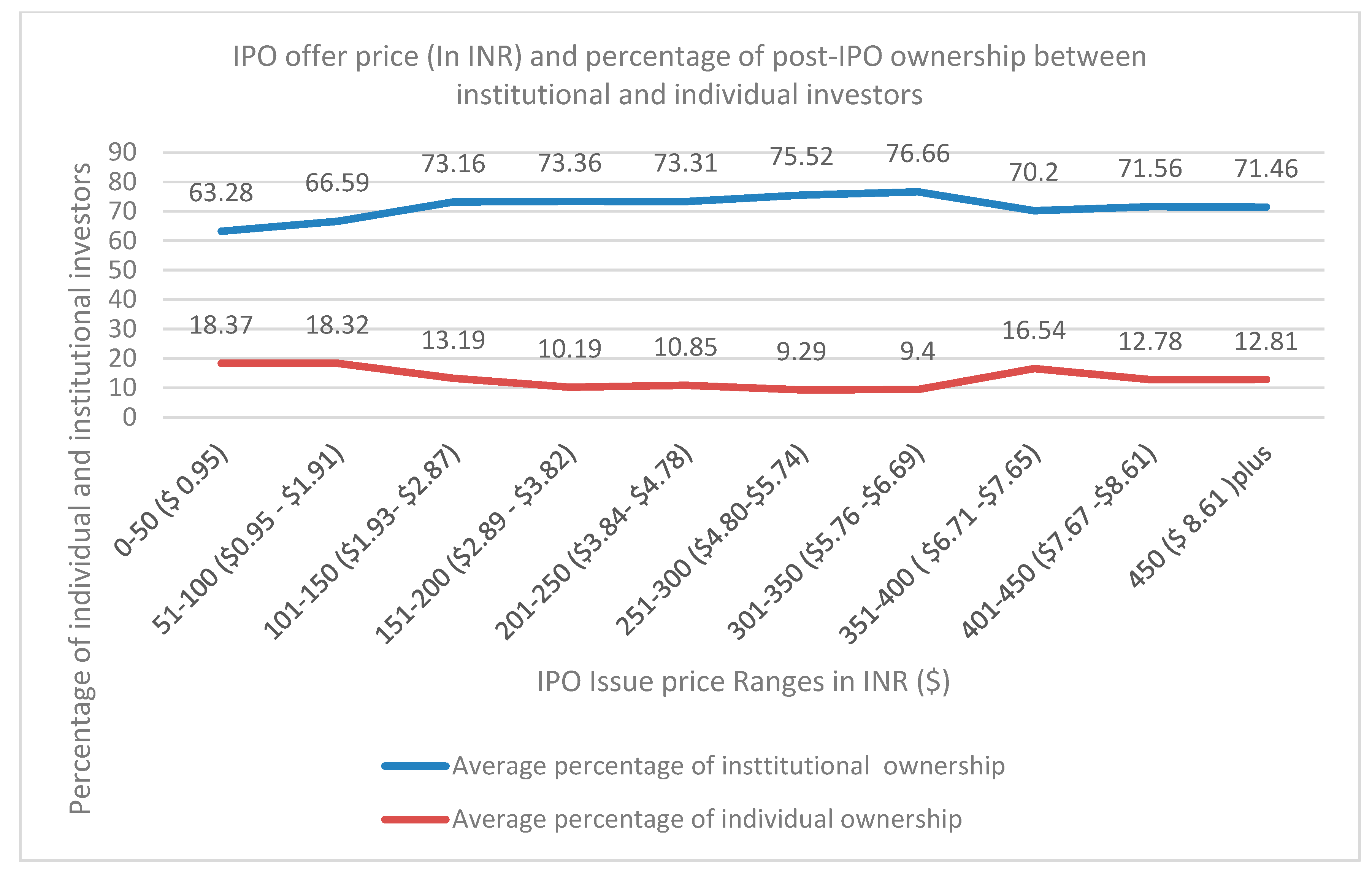

2.1.3. Percentage Ownership among Individual and Institutional Investors Post-IPO Listing

2.1.4. IPO Offer Prsice and Pre IPO Financial of a Company

2.2. Hypotheses Development

2.2.1. IPO Pre-Listing Stage—Full Subscription/Oversubscription

2.2.2. IPO Post Listing Stage—Initial Trading and Post-IPO Ownership Structure

3. Sample, Research Methodology, and Models

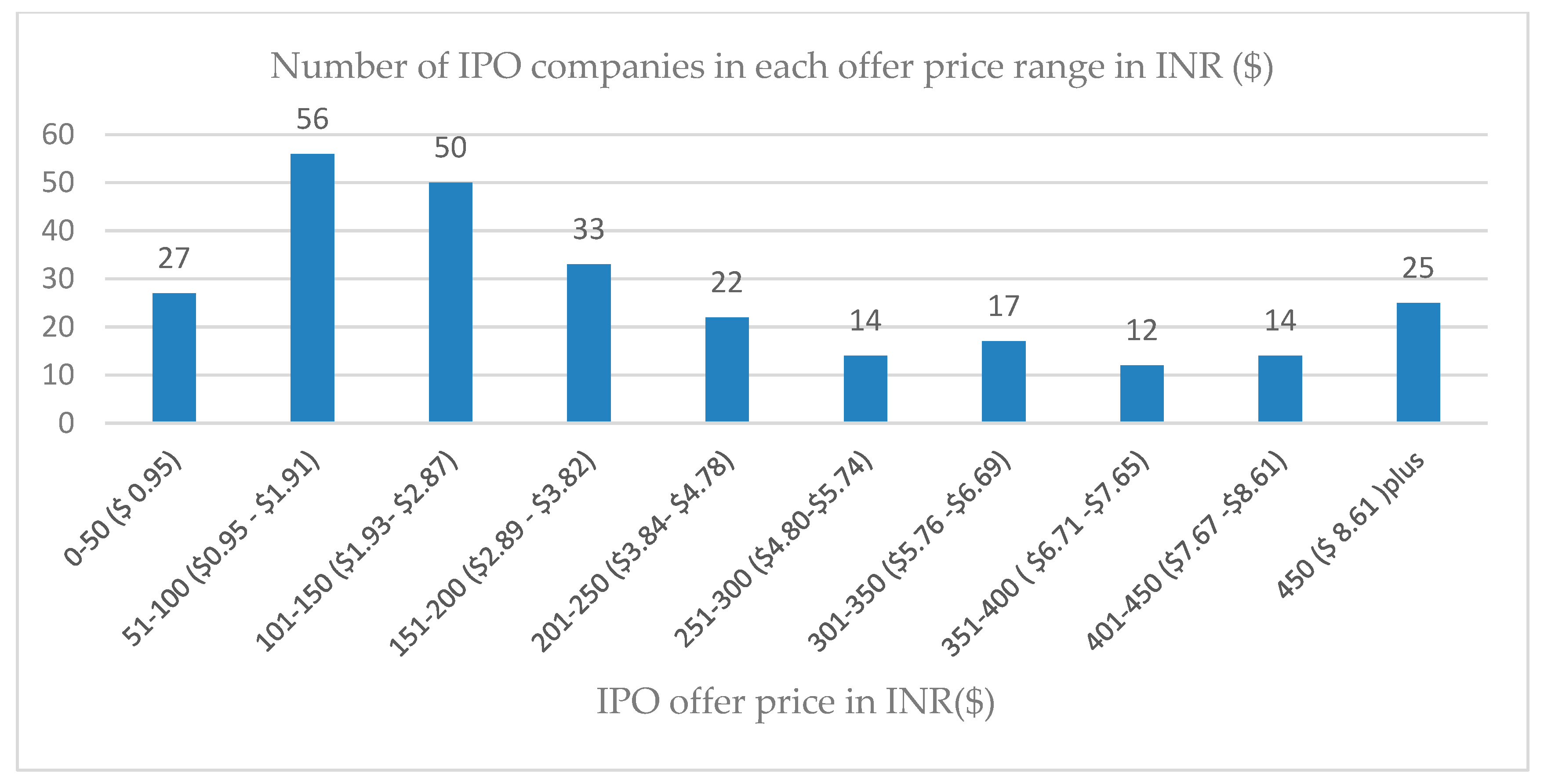

3.1. Sample Description

3.2. Research Methodology and Regression Models

3.2.1. Investor Demand at the Pre-IPO Listing Stage—Models

3.2.2. Investor Participation after the IPO Listing—Models

4. Regression Results and Discussion

4.1. Regression Results (Firth Logistic Regression)—The Effect of IPO Offer Price Range and Issue-Specific Characteristics on IPO Full Subscription or Oversubscription among Investor Categories (for Results, See Appendix A)

4.2. Regression Results (OLS Regression)—The Effect of IPO Offer Price Ranges and IPO Issue Characteristics on First-Day Trading Ratio (FDTR) (for Results, See Appendix B)

4.3. Regression Results—The Effect of IPO Offer Price Ranges, Promotor Holding and Financial/Non-Financial Controls on Post-IPO Ownership Structure between Individual and Institutional Investors (for results, See Appendix C

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Firth Logit Regression Model | Dependent Variable—If the IPO Issue Is Oversubscribed, Takes the Value of 1; Otherwise 0; N = 200 | ||

|---|---|---|---|

| Independent Variables-Coef (Coef Range) (p-Value) | RII (Retail) | NII | QIB |

| Dummy_0–50 | −0.891 (−1.548, −0.036) (0.028) | −1.43 (−2.12, −0.46) (0.001) | −1.83 (−2.38, −0.28) (0.001) |

| Dummy_51–100 | 0.175 (−0.50, 1.03) (0.670) | −0.804 (−1.49, 0.128) (0.068) | −1.21 (−1.67, 0.24) 0.013 |

| Dummy_101–150 | 0.238 (−0.12, 1.24) (0.587) | 0.551 (0.178, 2.15) (0.352) | −0.189 (−0.30, 1.46) (0.714) |

| Dummy_151–200 | −0.545 (−1.49, 0.089) (0.208) | −0.415 (−1.74, 0.23) (0.427) | 0.102 (−0.81, 1.16) (0.862) |

| Dummy_201–250 | 0.071 (−0.97, 0.90) (0.888) | 0.072 (−1.31, 1.02) (0.906) | −0.254 (−1.26, 0.92) (0.689) |

| Dummy_251–300 | −0.218 (−1.52, 0.86) (0.727) | 0.906 (−1.44, 2.16) (0.544) | 0.339 (−1.45, 2.17) (0.728) |

| Dummy_301–350 | 0.495 (0.95, 1.91) (0.506) | −0.110 (−1.68, 1.26) (0.885) | 1.22 (−1.57, 4.22) (0.418) |

| Dummy_351–400 | −0.212 (−1.78, 1.26) (0.789) | −1.38 (−2.99, −0.024) (0.068) | 0.941 (−2.04, 3.92) (0.547) |

| Dummy_401–450 | 0.628 (−1.10, 2.46) (0.68) | 0.032 (−1.73, 1.90) (0.972) | −1.21 (−3.13, 0.93) (0.261) |

| IPO Issue Size | −0.0001504 (−0.0002584, 3.05) (0.023) | −0.0001745 (−0.0002775, −8.75) (0.010) | 0.0051 (0.0031823, 0.008878) (0.000) |

| IPO Underpricing (MAU) | 0.004999 (−0.001329, 0.010282) (0.088) | 0.0000741 (−0.0013297, 0.010282) (0.979) | 0.0063 (0.0006169, 0.0119556) (0.026) |

| Intercept (p-value) | 1.189 (0.594, 1.59) (0.000) | 1.94 (1.21, 2.43) (0.000) | 0.444 (−1.07, 0.809) (0.322) |

| Wald chi2 | 19.05 | 25.11 | 58.53 |

Appendix B

| Independent Variables IPO Price Ranges (Low to High) & Firm-Specific Variables Coef (Coef Range) (p-Value) | Dependent Variables—First-Day Trading Ratio (FDTR) Regression Coefficients (OLS Regression) |

|---|---|

| Dummy_(0–50) | −1.473 (−2.63, −0.275) (0.015) |

| Dummy_(51–100) | 0.160 (−0.814, 1.172) (0.752) |

| Dummy_(101–150) | −0.060 (−1.072, 0.986) (0.908) |

| Dummy_(151–200) | 0.649 (−0.704, 1.961) (0.256) |

| Dummy_(201–250) | 0.609 (−1.655, 1.80) (0.368) |

| Dummy_(251–300) | 0.058 (−1.462, 1.614) (0.947) |

| Dummy_(301–350) | −0.013 (−2.281, 1.812) (0.987) |

| Dummy_(351–400) | −0.01331 (−4.544, 3.362) 0.987 |

| Dummy_(401–450) | 0.611 (−0.007, 0.0752) (0.760) |

| log (IPO Issue Size) | −1.77 (−2.503, −1.030) (0.000) |

| market-adjusted underpricing | 1.53 (0.809, 2.266) (0.000) |

| percentage of promotor holdings | 0.0059 (−0.016, 0.0290) (0.609) |

| percentage of individual holdings | 0.040 (0.007, 0.0752) (0.019) |

| Intercept | 8.48 (4.884, 11.912) (0.000) |

| F-value (p-value) | 0.0000 |

| Adj. R-square | 0.28 |

Appendix C

| Independent Variable IPO Price Ranges (Low to High); Non-Financial Variables (Issue Specific) and Financial Variables (Firm-Specific) Coef. (p-Value) | Regression Model 1: Dependent Variable: (Percentage of Individual Shareholding Immediately after the IPO) Regression Coefficients (OLS Regression) N-200 | Regression Model 2: Dependent Variable: Percentage of the Individual Shareholding Immediately after the IPO Regression Coefficients (OLS Regression) N-200 |

|---|---|---|

| Dummy_0–50 | 9.925 (3.073, 16.777) (0.005) | −6.14 (−16.197, 3.899) (0.229) |

| Dummy_(51–100) | 4.22 (−1.289, 9.732) (0.132) | 1.32 ( −6.751, 9.408) (0.746) |

| Dummy_(101–150) | 0.385 (−4.917, 5.687) (0.886) | 4.97 (−2.793, 12.748) (0.208) |

| Dummy_(151–200) | −2.54 (−8.570, 3.478) (0.405) | 5.22 (−3.771, 14.214) (0.253) |

| Dummy_(201–250) | −1.20 (−8.649, 6.235) (0.749) | 0.516 (−10.387, 11.421) (0.926) |

| Dummy_(251–300) | −0.790 (−10.581, 9.001) (0.874) | 7.33 (−10.387, 11.421) (0.314) |

| Dummy_(301–350) | −9.15 (−17.756, −0.558) (0.037) | 14.83 (2.2308, 27.429) (0.021) |

| Dummy_(351–400) | −2.55 (−25.099, 19.997) (0.824) | −1.18 (−34.230, 31.853) (0.943) |

| Dummy_(401–450) | −5.38 (−18.569, 7.795) (0.421) | 8.36 (−10.954, 27.680) (0.394) |

| α percentage of promotor holdings (after the IPO listing) | −0.244 (−0.347, −0.1408) (0.000) | 0.65 (0.501, 0.803) (0.000) |

| IPO issue size (million INR) ***** | −6.47 (−0.0000171, 4.15) (0.231) | 0.0000116 (−3.996, 0.0000271) (0.144) |

| market-adjusted underpricing (MAU) ***** | −1.07 (−4.841, 2.694) (0.574) | 2.10 (−3.427, 7.627) (0.454) |

| Minimum Lot Size (in INR) ***** | 0.0000639 (−0.000349, 0.000476) (0.761) | 0.0001913 (0.533) |

| EPS (3-year weighted average before the IPO) ****** | −0.013 (−0.055, 0.0278) (0.517) | 0.0175 (−.0433, 0.0784) (0.570) |

| IPO offer price to earnings (weighted average 3 years) ratio ****** | −0.0047 (−0.0248, 0.0152) (0.638) | 0.0123 (−0.0169, 0.0417) (0.407) |

| return on net worth (weighted average 3 years ratio to the IPO) ****** | 0.0485 (−0.057, 0.154) (0.367) | 0.0726 (−0.0830, 0.228) (0.358) |

| net asset value (before the IPO) ****** | −0.00305 (−0.0380, 0.031) (0.863) | −0.0014 (−0.0482, 0.0545) (0.964) |

| β0 constant | 27.84 (18.516, 37.173) (0.000) | 22.264 (9.492, 36.891) (0.000) |

| F-statistic (p-value) | 0.000 | 0.0000 |

| Adj. R2 | 0.31 | 0.40 |

References

- Agarwal, Sumit, Chunlin Liu, and S. Ghon Rhee. 2006. Investor demand for IPOs and after market performance: Evidence from the Hong Kong stock market. Journal of International Financial Markets, Institutions & Money 18: 176–90. [Google Scholar]

- Aggarwal, Reena, and Pietra Rivoli. 1990. Fads in the initial public offering market? Financial Management 19: 45–57. [Google Scholar] [CrossRef]

- Aggarwal, Rajesh, Sanjai Bhagat, and Srinivasan Rangan. 2009. The Impact of Fundamentals on IPO Valuation. Financial Management 38: 253–84. [Google Scholar] [CrossRef] [Green Version]

- Bartov, Eli, Partha Mohanram, and Chandrakanth Seethamraju. 2002. Valuation of internet stocks. An IPO perspective. Journal of Accounting Research 40: 321–46. [Google Scholar] [CrossRef] [Green Version]

- Birru, Justin, and Baolian Wang. 2016. Nominal Price Illusion. Journal of Financial Economics 119: 578–98. [Google Scholar] [CrossRef]

- Black, Bernard S. 1992. Institutional investors and corporate governance: The case for institutional voice. Journal of Applied Corporate Finance 5: 19–32. [Google Scholar] [CrossRef]

- Booth, James R., and Lena Chua. 1996. Ownership dispersion, costly information and IPO under-pricing. Journal of Financial Economics 41: 291–310. [Google Scholar] [CrossRef]

- Brennan, Michael J., and Julian Franks. 1997. Under-pricing, ownership and control in initial public offerings of equity securities in the UK. Journal of Financial Economics 45: 391–413. [Google Scholar] [CrossRef]

- Chalk, Andrew J., and John W. Peavy III. 1987. Initial public offerings: Daily returns, offering types and the price effect. Financial Analysts Journal 43: 65–69. [Google Scholar] [CrossRef]

- Chowdhry, Bhagwan, and Ann Sherman. 1996. International differences in oversubscription and underpricing of IPOs. Journal of Corporate Finance 2: 359–81. [Google Scholar] [CrossRef]

- Clarke, Jonathan, Arif Khurshed, Alok Pande, and Ajai K. Singh. 2016. Sentiment traders & IPO initial returns: The indian evidence. Journal of Corporate Finance 37: 24–37. [Google Scholar]

- Cotter, Julie, Michelle Goyen, and Sherryl Hegarty. 2005. Offer pricing in Australian industrial public offers. Accounting and Finance 45: 95–125. [Google Scholar] [CrossRef]

- Del Guercio, Diane. 1996. The distorting effect of the prudent-man laws on institutional equity investments. Journal of Financial Economics 40: 31–62. [Google Scholar] [CrossRef]

- Dyl, Edward A., and William B. Elliott. 2006. The Share Price Puzzle. The Journal of Business 79: 2045–66. [Google Scholar] [CrossRef]

- Falkenstein, Eric G. 1996. Preferences for stock characteristics as revealed by mutual fund portfolio holdings. Journal of Finance 51: 111–35. [Google Scholar] [CrossRef]

- Fernando, Chitru S., Srinivasan Krishnamurthy, and Paul A. Spindt. 2004. Are share price levels informative? Evidence from the ownership, pricing, turnover, and performance of IPO firms. Journal of Financial Markets 7: 377–403. [Google Scholar] [CrossRef]

- Franks, Julian, and Colin Mayer. 1997. Corporate ownership and control in the UK, Germany and France. Journal of Applied Corporate Finance 9: 30–45. [Google Scholar] [CrossRef]

- Fung, Joseph KW, Louis TW Cheng, and Kam C. Chan. 2005. The Impact of the costs of subscription on measured IPO returns: The Case of Asia. Journal of Corporate Finance 10: 45. [Google Scholar] [CrossRef] [Green Version]

- Ghicas, Dimitrios C., Nikolaos Iriotis, Aphroditi Papadaki, and Martin Walker. 2000. Fundamental analysis and valuation of IPOs in the construction industry. International Journal of Accounting 35: 227–41. [Google Scholar] [CrossRef]

- Gompers, Paul A., and Andrew Metrick. 2001. Institutional investors and equity prices. Quarterly Journal of Economics 116: 229–51. [Google Scholar] [CrossRef]

- Ibbotson, Roger G., and Jay R. Ritter. 1995. Initial public offerings. In Handbooks in Operations Research and Management Science. Amsterdam: North-Holland Publishing, vol. 9, pp. 993–1016. [Google Scholar]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect theory: An analysis of decision under risk. Econometrica, Econometric Society 47: 262–93. [Google Scholar] [CrossRef] [Green Version]

- Kahneman, Daniel, and Amos Tversky. 1984. Choices, values, and frames. American Psychologist 39: 341–50. [Google Scholar] [CrossRef]

- Kim, Moonchul, and Jay R. Ritter. 1999. Valuing IPOs. Journal of Financial Economics 53: 409–37. [Google Scholar] [CrossRef]

- Kim, Jeong-Bon, Itzhak Krinsky, and Jason Lee. 1995. The role of financial variables in the pricing of Korean initial public offerings. Pacific-Basin Finance Journal 3: 449–64. [Google Scholar] [CrossRef]

- Klein, April. 1996. The association between the information contained in the prospectus and the price of initial public offerings. Journal of Financial Statement Analysis 2: 23–40. [Google Scholar]

- Krigman, Laurie, Wayne H. Shaw, and Kent L. Womack. 1999. The persistence of IPO mispricing and the predictive power of flipping. Journal of Finance 54: 1015–44. [Google Scholar] [CrossRef]

- Leland, Hayne E., and David H. Pyle. 1977. Informational Asymmetries. Financial Structure, and Financial Intermediation. The Journal of Finance 32: 371–87. [Google Scholar] [CrossRef]

- Ljungqvist, Alexander, and William Wilhelm Jr. 2006. Does prospect theory explain IPO market behavior? Journal of Finance 60: 1759–90. [Google Scholar] [CrossRef] [Green Version]

- McInish, Thomas H., and Robert A. Wood. 1992. An analysis of intraday patterns in bid/ask spreads for NYSE stocks. Journal of Finance 47: 753–76. [Google Scholar] [CrossRef]

- Mello, Antonio S., and John E. Parsons. 1998. Going public and the ownership structure of the firm. Journal of Financial Economics 49: 79–10. [Google Scholar] [CrossRef]

- Miller, Robert E., and Frank K. Reilly. 1987. An examination of mispricing, returns and uncertainty for initial public offerings. Financial Management 16: 33–38. [Google Scholar] [CrossRef]

- Neupane, Suman, and Sunil S. Poshakwale. 2012. Transparency in IPO mechanism: Retail investors’ participation, IPO pricing and returns. Journal of banking & Finance 36: 2064–76. [Google Scholar]

- Pelham, Brett W., Tin T. Sumarta, and Laura Myaskovsky. 1994. The easy path from many too much: The numerosity heuristic. Cognitive Psychology 26: 103–33. [Google Scholar] [CrossRef] [Green Version]

- Ritter, Jay R. 1984. Signalling and the valuation of unseasoned new issues: A Comment. Journal of Finance 39: 1231–33. [Google Scholar] [CrossRef]

- Rock, Kevin. 1986. Why new issues are under-priced. Journal of Financial Economics 15: 187–221. [Google Scholar] [CrossRef]

- Sahoo, Seshadev, and Prabina Rajib. 2012. Determinants of pricing IPOs: An empirical investigation. South Asian Journal of Management 19: 59–87. [Google Scholar]

- Schreiner, Andreas. 2007. Equity valuation using multiples: An empirical investigation, Deutsche Universitats-Verlag. Wiesbaden: GWV Fachverlage GmbH. [Google Scholar]

- Stoll, Hans R., and Robert E. Whaley. 1983. Transactions costs and the small firm effect. Journal of Financial Economics 12: 57–80. [Google Scholar] [CrossRef]

- Stoughton, Neal M., and Josef Zechner. 1998. IPO mechanisms, monitoring, and ownership structure. Journal of Financial Economics 49: 45–78. [Google Scholar] [CrossRef]

- Thaler, Richard. 1985. Mental Accounting and Consumer Choice. Marketing Science 4: 199–214. [Google Scholar] [CrossRef]

- Weld, William C., Roni Michaely, Richard H. Thaler, and Shlomo Benartzi. 2009. The nominal price puzzle. Journal of Economic Perspectives 23: 121–42. [Google Scholar] [CrossRef] [Green Version]

- Yong, Othman, and Zaidi Isa. 2003. Initial performance of new issues of shares in Malaysia. Applied Economics 35: 919. [Google Scholar] [CrossRef]

| 1 | The term “reference point” was first coined by Kahneman and Tversky (1979) in their well-known paper about prospect theory. Individual investors may have a reference point in mind regarding the nominal prices for gains and losses while trading in the secondary market. |

| 2 | Framing biases are a behavioral interpretation of the IPO offer price, in which individual investors frame their decisions based on the absolute nominal prices rather the percentage of returns. |

| 3 | The percentage holding of promoters in Indian companies listed on National Stock Exchange stood at 54.46% as on June 30, 2019 and value though, promoter holding in companies listed on NSE his INR 73.33 lakh crore (Source—NSE Infobase—Prime database). |

| IPO Offer Price Range (in INR) ($) | Retail Individual Investor (RII) | Non-Institutional Investors | Qualified Institutional Buyer (QIB) |

|---|---|---|---|

| (NII) | |||

| Number of IPOs Undersubscribed | Number of IPOs Undersubscribed | Number of IPOs Undersubscribed | |

| 0–50 ($ 0.95) | 21 | 20 | 30 |

| 51–100 ($0.95–$1.91) | 18 | 19 | 38 |

| 101–150 ($1.93–$2.87) | 15 | 6 | 20 |

| 151–200 ($2.89–$3.82) | 16 | 8 | 10 |

| 201–250 ($3.84–$4.78) | 7 | 4 | 5 |

| 251–300 ($4.80–$5.74) | 6 | 3 | 1 |

| 301–350 ($5.76–$6.69) | 3 | 4 | 0 |

| 351–-400 ($6.71–$7.65) | 5 | 2 | 1 |

| 401–450 ($7.67–$8.61) | 5 | 11 | 2 |

| Greater Than 450 ($ 8.61) | 10 | 11 | 0 |

| Sample Variables | Obs. | Mean | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|

| Percentage of individual holding (after the IPO) | 200 | 15.86 | 11.80 | 0.27 | 56.67 |

| Percentage of institutional holding (after the IPO) | 200 | 68.52 | 19.15 | 2.05 | 99.18 |

| First-day trading ratio (FDTR) | 200 | 2.18 | 2.24 | 0.0016 | 13.90 |

| Non-Financial (IPO Issue-Specific) | |||||

| Market-adjusted underpricing *** | 200 | 0.15 | 0.44 | 0.78 | 2.46 |

| Minimum lot size in INR ($) | 200 | 6655 ($127) | 3641 ($69.70) | 2600 ($49.47) | 51,600 ($987) |

| IPO offer price in INR ($) | 200 | 215 ($4.12) | 192.22 ($3.68) | 12 ($0.23) | 1310 ($25.08) |

| IPO issue size in million INR ($) | 200 | 44,687 ($855) | 152,850 ($2925) | 378 ($7.24) | 1,547,509 ($29,623) |

| PIPH: Percentage of promotor holdings | 200 | 58.77 | 16.28 | 4.90 | 98.38 |

| Financial (Firm-Specific) Controls | |||||

| EPS (3-year average before the IPO) | 200 | 13.04 | 37.85 | 0.19 | 372.95 |

| IPO offer price to EPS (before the IPO) | 200 | 39.40 | 80.21 | 0.29 | 881.00 |

| Return on net worth | 200 | 23.79 | 16.97 | 0.44 | 165.00 |

| Net asset value (NAV) before the IPO | 200 | 71.39 | 57.64 | 5.75 | 497.00 |

| Percentage of Individual Holdings (after the IPO) | Percentageof Institutional Holdings (after the IPO) | IPO Offer Price (INR) | IPO Issue Size (in Million INR) | Market-Adjusted Underpricing (MAU) | Percentage Promotor Holding | EPS (3-Year Average before the IPO) | IPO Offer Price to EPS (before the IPO) | Return on Net Worth (before the IPO) | Net Asset Value (after the IPO) | Minimum Lot Size (in INR) | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Percentage of individual holdings (after the IPO) | 1 | ||||||||||

| Percentage of institutional holdings (after the IPO) | −0.6217 | 1 | |||||||||

| IPO offer price (in INR) | −0.2649 | 0.1508 | 1 | ||||||||

| IPO issue size (in million INR) | −0.219 | 0.2691 | 0.134 | 1 | |||||||

| Market-adjusted underpricing (MAU) | −0.0494 | 0.0225 | 0.1065 | 0.042 | 1 | ||||||

| Percentage of promotor holdings (PIPH) | −0.4118 | 0.6138 | 0.003 | 0.3352 | −0.0884 | 1 | |||||

| EPS (before the IPO) | −0.0669 | 0.0937 | 0.148 | −0.0306 | −0.0325 | 0.0586 | 1 | ||||

| IPO offer price to EPS (before the IPO) | −0.1326 | 0.1132 | 0.1059 | 0.0807 | −0.017 | 0.107 | −0.1089 | 1 | |||

| Return on net worth | −0.0829 | 0.1552 | 0.2058 | 0.0076 | 0.0328 | 0.0433 | 0.3432 | −0.2077 | 1 | ||

| Net asset value (before the IPO | −0.1601 | 0.0589 | 0.7425 | −0.0475 | 0.0743 | −0.0413 | 0.0825 | −0.0198 | 0.104 | 1 | |

| Minimum lot size (in INR) | −0.0126 | 0.0425 | 0.2 | −0.0173 | −0.0349 | 0.0144 | 0.0172 | −0.0356 | −0.0234 | 0.1232 | 1 |

| Correlation Matrix | First-Day Trading Ratio | IPO Offer Price | IPO Issue Size | Market-Adjusted Underpricing | Promotor Holdings (%) | Individual Holdings (%) |

|---|---|---|---|---|---|---|

| First-day trading ratio (FDTR) | 1 | |||||

| IPO offer price (In INR) | −0.1181 | 1 | ||||

| IPO issue size (In INR Mn) | −0.4613 | 0.435 | 1 | |||

| Market-adjusted underpricing | 0.2527 | 0.0875 | −0.0504 | 1 | ||

| Percentage of promotor holdings (post listing) | −0.241 | 0.1065 | 0.4631 | −0.1034 | 1 | |

| Percentage of individual holdings (post listing) | 0.3219 | −0.2641 | −0.524 | −0.0801 | −0.4472 | 1 |

| Percentiles across the IPO offer price for the sample. | ||||||

| 25% | 50% | 75% | 90% | 95% | ||

| 75 | 137 | 252 | 468 | 640 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sandhu, H.; Guhathakurta, K. Effects of IPO Offer Price Ranges on Initial Subscription, Initial Turnover and Ownership Structure—Evidence from Indian IPO Market. J. Risk Financial Manag. 2020, 13, 279. https://doi.org/10.3390/jrfm13110279

Sandhu H, Guhathakurta K. Effects of IPO Offer Price Ranges on Initial Subscription, Initial Turnover and Ownership Structure—Evidence from Indian IPO Market. Journal of Risk and Financial Management. 2020; 13(11):279. https://doi.org/10.3390/jrfm13110279

Chicago/Turabian StyleSandhu, Harsimran, and Kousik Guhathakurta. 2020. "Effects of IPO Offer Price Ranges on Initial Subscription, Initial Turnover and Ownership Structure—Evidence from Indian IPO Market" Journal of Risk and Financial Management 13, no. 11: 279. https://doi.org/10.3390/jrfm13110279