Prospects and Obstacles for Green Hydrogen Production in Russia

1

Department of Electrical Engineering, Saint Petersburg Mining University, 21st Line of the VI, 2, 199106 Saint Petersburg, Russia

2

Department of Strategic Development, RusHydro, 7 Malaya Dmitrovka Street, 127006 Moscow, Russia

3

Department of Economics, Organization and Management, Saint Petersburg Mining University, 21st Line of the VI, 2, 199106 Saint Petersburg, Russia

4

Instituto Superior Técnico, Universidade de Lisboa, Av. Rovisco Pais, 1049-001 Lisbon, Portugal

*

Author to whom correspondence should be addressed.

Energies 2021, 14(3), 718; https://doi.org/10.3390/en14030718

Submission received: 9 December 2020

/

Revised: 24 January 2021

/

Accepted: 27 January 2021

/

Published: 30 January 2021

(This article belongs to the Collection Renewable Energy and Energy Storage Systems)

Abstract

:Renewable energy is considered the one of the most promising solutions to meet sustainable development goals in terms of climate change mitigation. Today, we face the problem of further scaling up renewable energy infrastructure, which requires the creation of reliable energy storages, environmentally friendly carriers, like hydrogen, and competitive international markets. These issues provoke the involvement of resource-based countries in the energy transition, which is questionable in terms of economic efficiency, compared to conventional hydrocarbon resources. To shed a light on the possible efficiency of green hydrogen production in such countries, this study is aimed at: (1) comparing key Russian trends of green hydrogen development with global trends, (2) presenting strategic scenarios for the Russian energy sector development, (3) presenting a case study of Russian hydrogen energy project «Dyakov Ust-Srednekanskaya HPP» in Magadan region. We argue that without significant changes in strategic planning and without focus on sustainable solutions support, the further development of Russian power industry will be halted in a conservative scenario with the limited presence of innovative solutions in renewable energy industries. Our case study showed that despite the closeness to Japan hydrogen market, economic efficiency is on the edge of zero, with payback period around 17 years. The decrease in project capacity below 543.6 MW will immediately lead to a negative NPV. The key reason for that is the low average market price of hydrogen ($14/kg), which is only a bit higher than its production cost ($12.5/kg), while transportation requires about $0.96/kg more. Despite the discouraging results, it should be taken into account that such strategic projects are at the edge of energy development. We see them as an opportunity to lead transnational energy trade of green hydrogen, which could be competitive in the medium term, especially with state support.

1. Introduction

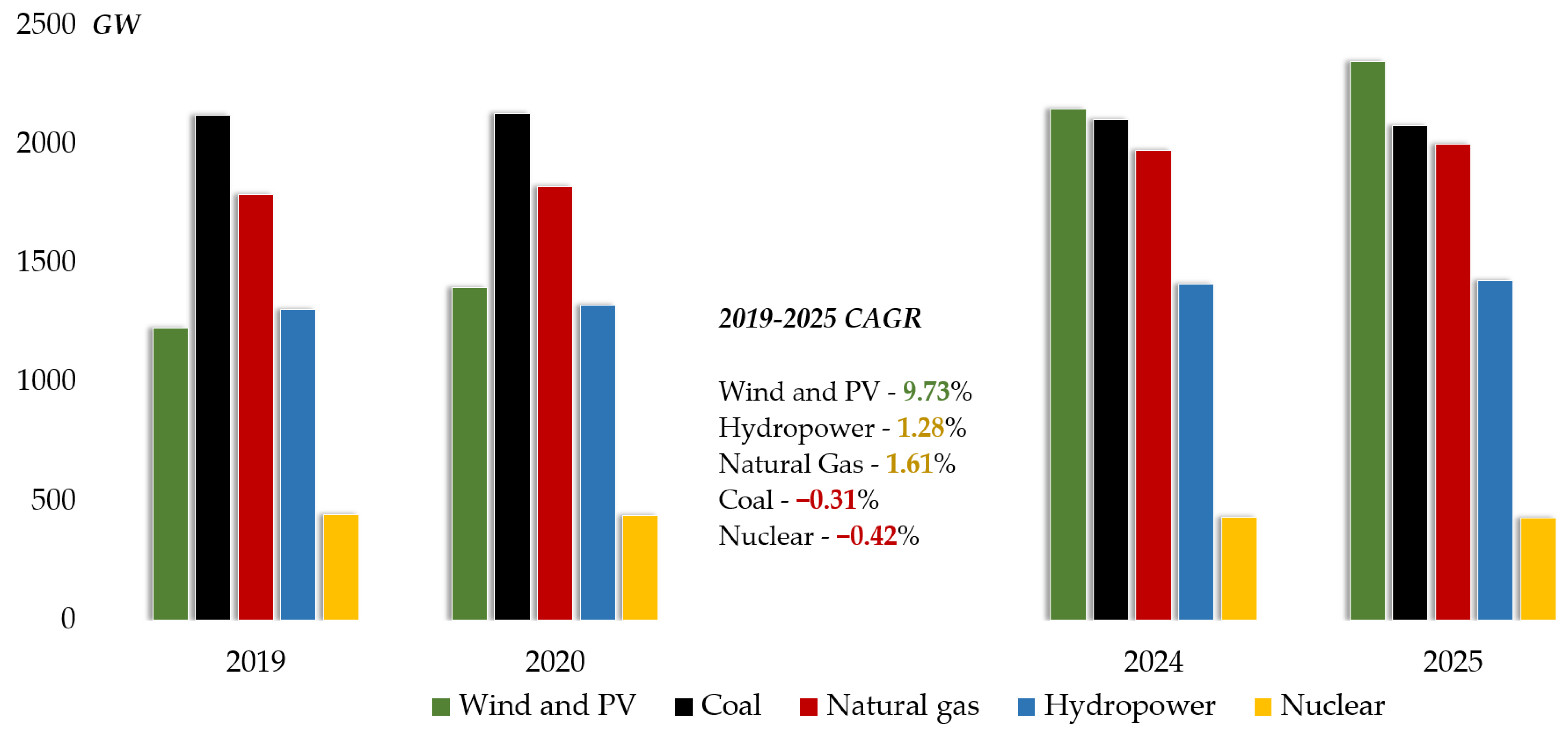

The development of renewable energy sources (RESs), which quickly adapted to the challenges of the COVID-19 crisis, continues at an increasing pace today. Thus, according to the forecast of the International Energy Agency (IEA), it is assumed that RESs will overtake coal and become the largest source of electricity production in the world by 2025, while providing a third of global energy consumption and reaching a record capacity of 271 GW, and by 2040, the share of RESs will make up more than half of all generating capacity in the world [1]. This forecast is very optimistic but confirms the relevance of this topic. Figure 1 shows the forecast of the total electric capacity of the main sources until 2025 based on the IEA analytical data, which shows a noticeable increase in the share of RESs in the short term, which is primarily due to the economic incentives, the development of technologies and reduction of their cost [2], the increased demand for local energy sources (including as heat energy sources), and the implementation of climate protection programs.

Also, according to the IEA, hydropower, which provides the largest share of renewable energy, will continue to supply half of the world’s renewable energy. In this paper, hydropower is considered as a RES, given the renewable nature of the primary energy source. The second and third places will be occupied by solar and wind power generation.

Speaking of the development of the RES market, it should be noted that throughout the world it is provided mainly through large-scale public investment, taxes, and other forms of support. Not surprisingly, the annual growth of alternative generation is measured in double digits [3]. However, an equally important factor in consumption growth is cheapening of the “clean” energy due to the development of technologies. In turn, the entry of the largest suppliers of RES technologies into new markets allows access to international capital and reduces costs.

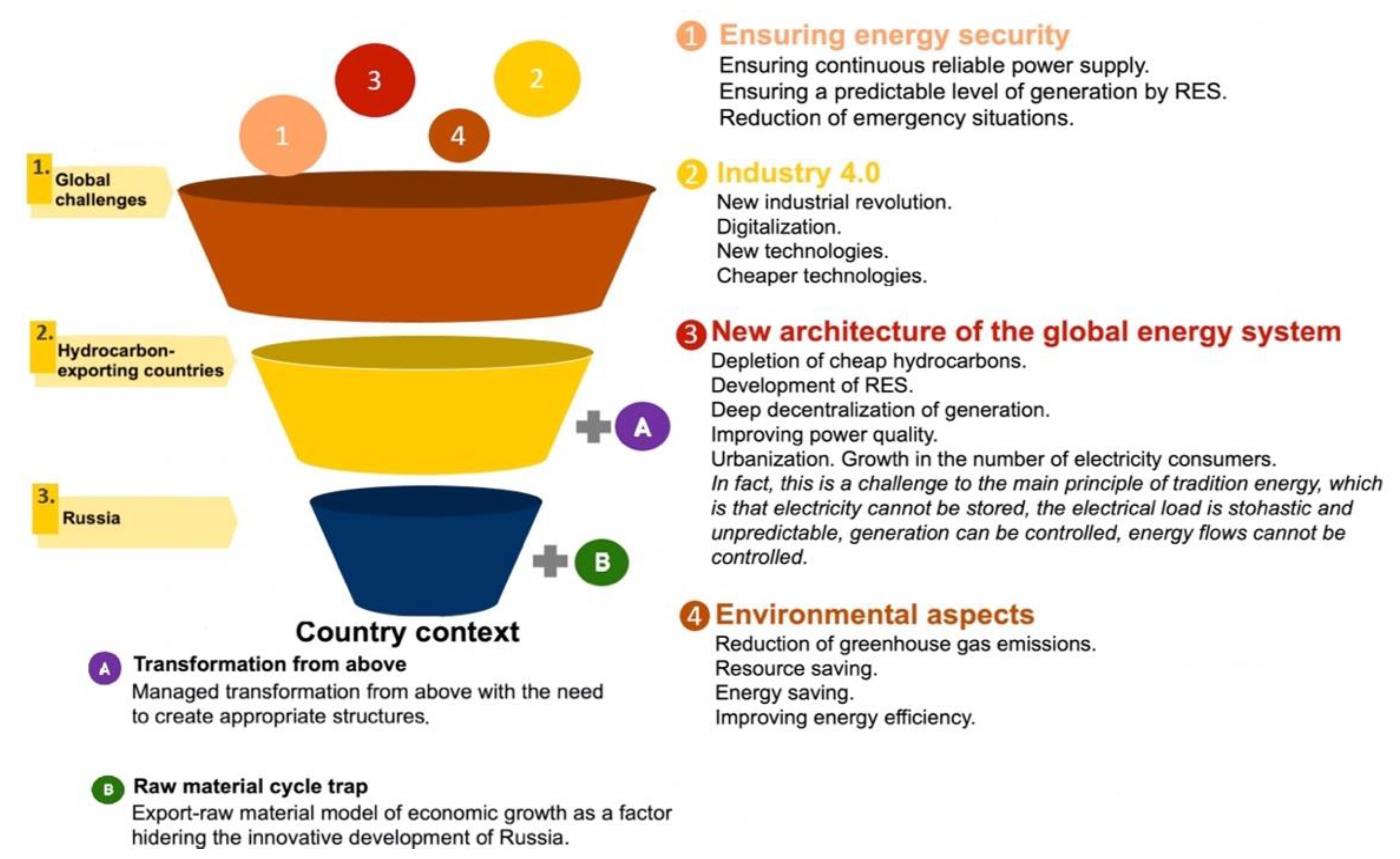

The involvement of resource countries in the development of renewable energy can be visually presented in the form of a funnel (Figure 2), where complementary global trends are refracted through the prism of opportunities and needs specific to the BRICS countries, and then directly to Russia. At the same time, of course, global trends are also refracted by the local context formed by a combination of economic, political, social, and other factors. In the figure below, global trends and challenges are indicated by numbers 1–4, and the context is indicated by letters A and B. The determination of the consequences and windows of opportunity for Russia, as well as the impact on the development of renewable energy, is based on the mutual overlapping of all these conditions, respectively.

As of February 2020, 189 countries have acceded to the Paris Agreement, which aims to keep the average temperature increase significantly below 2 °C and ideally no higher than 1.5 °C, increasing the ability to adapt to the effects of climate change and move towards low-carbon development. The parties to the agreement voluntarily set ambitious targets for reducing net CO2 emissions into the atmosphere: as of September 2019, 65 countries and the European Union have declared their commitment to carbon neutrality by 2050. Many of them have either already launched a CO2 trading system or other forms of carbon pricing and “carbon charges” or are planning to do so in the near future. The investment community is also keeping pace with the regulators—more than 70% of investors are now systematically assessing the sustainability aspects of companies and for many of them, it can be critical in avoiding investments.

A particular example of accelerated development of the RES is the agreement between Saudi Arabia and the Japanese corporation SoftBank Group. It envisions an investment of about $200 billion in the country’s solar energy as part of the 2030 solar plan and aims to build 200 GW of solar power plants by 2030, which provides about 50% of the installed capacity of the world’s solar energy [4].

To sum it up, the sketch of the problem is that after many years of huge investments in renewable energy we face a new, perhaps an even more complicated task—scaling up created facilities. On the one hand, we have relatively encouraging results in cost decrease and increased ERoEI. On the other hand, to implement wide scale use of renewable energy we must create a new energy delivery infrastructure. One of the most promising and discussable solution of this problem is the production of hydrogen. Unfortunately, today there are too many theories in this area and the lack of practical studies. As such, this study is aimed at: (1) comparing key Russian trends of green hydrogen development with global trends, (2) presenting strategic alternatives for the Russian energy sector development, (3) presenting a case study of the Russian hydrogen energy project «Dyakov Ust-Srednekanskaya HPP» in Magadan region, using the example of a RusHydro company.

The rest of this study is organized in the following way. In Section 2, we show the global perspective on the prospects of further renewable power generation development. The key issue of such development is the necessity of network power accumulator systems (Section 2.1), which is extremely deep and wide research problem. The large-scale production of the hydrogen is considered by many countries as a possible and flexible solution of this problem, which is reviewed in Section 2.2. Section 3 is dedicated to a Russian perspective of these issues (Section 3.1 and Section 3.2) and, as a concluding remark, we show the view on Russian green hydrogen strategic pathways (Section 3.3). Section 4 is aims to show the possibility of the successful and cost-effective integration of hydrogen energy storage in a hydro power plant (Magadan region, Russia). The last section contains the discussion of this experience and conclusions.

2. Global Perspective

2.1. Diffusion of RESs into Existing Energy System through the Development of Power Accumulators

The stochasticity of RES power generation determines the critical importance of developing technologies for energy accumulation and storage in order to reduce the need to maintain excess capacity reserves.

In addition to market formation and the need to stabilize RES generation, one of the key prerequisites for the development of energy storage technologies is the daily unevenness of the load schedule. Thus, to cover the morning and evening maximum, it is necessary to maintain a certain amount of capacity reserves, which, in its turn, must be paid for by the consumer. As a result, during maximum load hours, the growth of the unregulated electricity price is also fixed. On the other hand, there is a need to reduce the output during night hours due to a decrease in demand for electricity, which is a difficult task in the presence of a large amount of production of small-size large power plants in the total daily power balance. In addition, operation in variable modes, even if they are implemented, leads to increased specific fuel consumption, and forced capacity reduction leads to a decrease in Installed Capacity Utilization Factor (ICUF) and, consequently, to a decrease in economic efficiency. In particular, by 2050, China plans to increase the capacity of nuclear power plants to 250 GW, while, according to estimates by The Energy Research Institute [5], industrial storage systems with a total capacity of about 113 GW will be needed to regulate this capacity. In addition, an example of the use of power accumulators is frequency regulation in order to balance supply and demand in the minute phase [6]. For example, Tesla’s Hornsdale Power Reserve (100 MW/129 MWh), commissioned in South Australia (≈2% of the installed capacity of the region’s power system), is included in the Frequency Control and Ancillary Services System (FCAS). The power accumulator’s capacity is split 70/30 to ensure network security and arbitration in the wholesale market. In the first four months of operation, the drive accounted for 55% of market revenue, with prices down 90%, according to McKinsey [7]. The only state where prices on the FCAS market fell was South Australia, and consumer savings over the period amounted to about $35 million.

Network power accumulators (NEAs) open up fundamental new opportunities for the development of the electric power industry, in particular, RESs, and will significantly change the modern architecture of the electric power and capacity market by removing the mandatory condition regarding the simultaneity of generation and consumption of electricity, as well as the active introduction of technologies for demand management and price arbitration.

The integration of RESs in the energy system covers a number of opportunities for the use of NEAs, which significantly differ depending on technical requirements. For large-scale wind and solar farms, there are several options for using energy accumulators: to smooth out short-term fluctuation and to protect against rapid increase or decrease in output power. These systems can also be used to maintain stable voltage levels. Long-term storage systems can facilitate large-scale integration of RESs in several directions at once. RESs can improve efficiency, reduce volatility, and provide a hedging process for RESs generation projections. NEAs also provide an opportunity to shift production peaks to off-peak demand. They can also be used to reduce the cost of network infrastructure construction as a reserve capacity, by improving the efficiency and reliability of existing RES equipment. A greater economic effect is achieved when the NEAs are located directly in the RES facility and are integrated into the production cycle.

NEAs can be used to avoid reducing wind energy when the electrical system is unable to absorb the electricity generated. Such situations may occur when the network has insufficient capacity or due to the inability to dispatch and turn on the power due to excessive generation or high fluctuations. In turn, the types and kinds of NEAs are selected according to the specifics of each project. The generated energy of local RES generators can be stored and used when and where it is necessary. Based on this approach, the system regulator can get additional benefits from subsidies due to the larger coverage area, and end users can reduce their dependence on centralized power supply.

Currently, almost all the developed and developing countries are actively pursuing a policy of forming national markets for energy storage systems, considering energy storage as one of the key areas of energy development and intensively developing production of energy storage systems aimed at saturation of domestic and foreign markets. At the same time, the main growth driver is technological progress, which helps reduce the cost of storage systems to an acceptable level for consumers, while improving their performance [8,9]. According to the Report prepared by the IEA for the G20, Japan [10] the electrical efficiency (LHV) of electrolyzers will increase at the following rate (%, today/by 2030/long term): Alkaline–63–70/65–71/70–80; Proton Exchange Membrane (PEM)–56–60/63–68/67–74; Solid Oxide Electrolysis Cells (SOEC)–74–81; 77–84/77–90. The development of technologies will make it possible to increase the efficiency coefficient, reduce operating costs, as well as reduce the effect of growing wear and tear of storage elements and preserve their ability to accumulate and store the required amount of electricity.

According to the forecasts of the Center for Strategic Development, the volume of the world market of electric power storage systems by 2025 is estimated at USD73.3 billion [11]; McKinsey Global Institute has included this type of technologies into the list of 12 most significant ones for the development of the world energy sector [12]. In turn, GuideHouse Insights (previously—Navigant Research) predicts an increase in the annual input of drive capacity for RESs from about 2 GW in 2018 to 24 GW in 2026, i.e.,12 times over eight years, with a proportional increase in annual revenues to USD 24 billion by 2026 [13].

At the same time, the forecast of Bloomberg New Energy Finance (BNEF) [14] suggests that the market for “battery” storage will develop along a path that is similar to the dynamics of the market of photovoltaic solar energy in the period of 2000–2015, during which the installed capacity of solar generation has “doubled seven times.” In total, by 2030, according to the forecast of BNEF, 125 GW of energy storage will be built with a total capacity of 305 GW*h (excluding hydropower plants), the volume of investments will amount to USD 103 billion.

2.2. Prerequisites for Green Hydrogen Development

The climate agenda continues to be considered as a priority by countries and the world community as a whole [15,16,17,18,19,20]. Decarbonization is becoming the most important driver of the growing demand for the ability of energy systems to adapt consumption to the optimal schedule for generation. These sources of flexibility comprise energy storage, including hydrogen. This role of hydrogen energy imposes a specific environmental requirement on hydrogen production technologies: they must be carbon-free (“green hydrogen”). Therefore, no scenarios of global demand for hydrogen fuel consider natural gas and coal as the main raw material for hydrogen production.

For example, the federal government of Germany forecasts that by 2030 the demand for hydrogen in the country will be about 90–110 Twh. To cover part of this demand, by 2030, generating plants with a total capacity of up to 5 GW should be built in Germany, including the necessary marine and onshore power generation. This corresponds to the production of green hydrogen up to 14 Twh and the required amount of renewable energy up to 20 Twh [21].

Hydrogen is one of the most important raw materials of modern chemical and petrochemical industry. It is obtained in various ways, which can be grouped into physical, electrochemical and chemical methods.

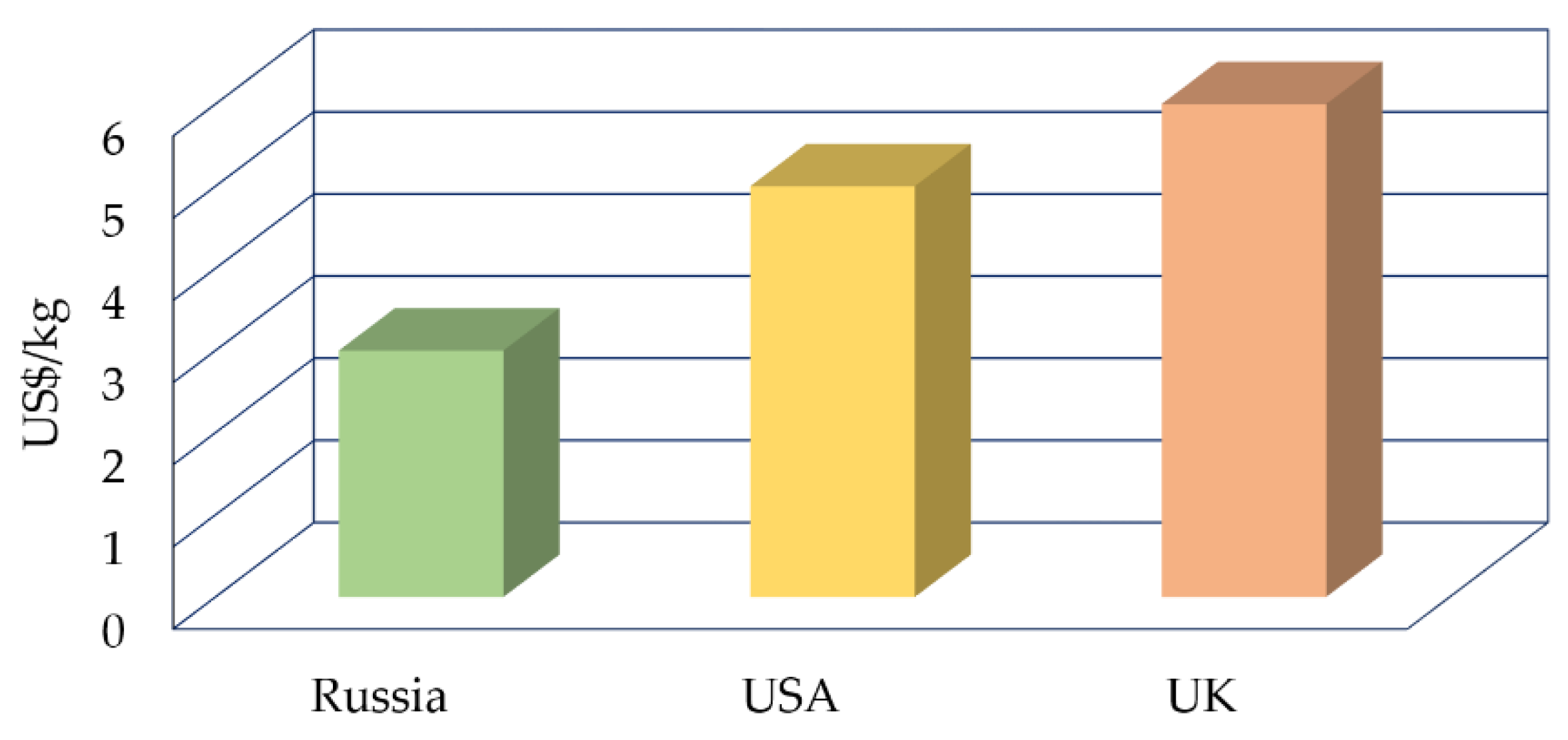

According to IRENA estimates, the target bar of hydrogen price for the buyer with delivery to the place of consumption (CIF prices, Figure 3) depending on the national hydrogen energy program is in the range of 3–6 US dollars per kg by 2025 with the prospect of reducing to 2 US dollars per kg on the horizon until 2040.

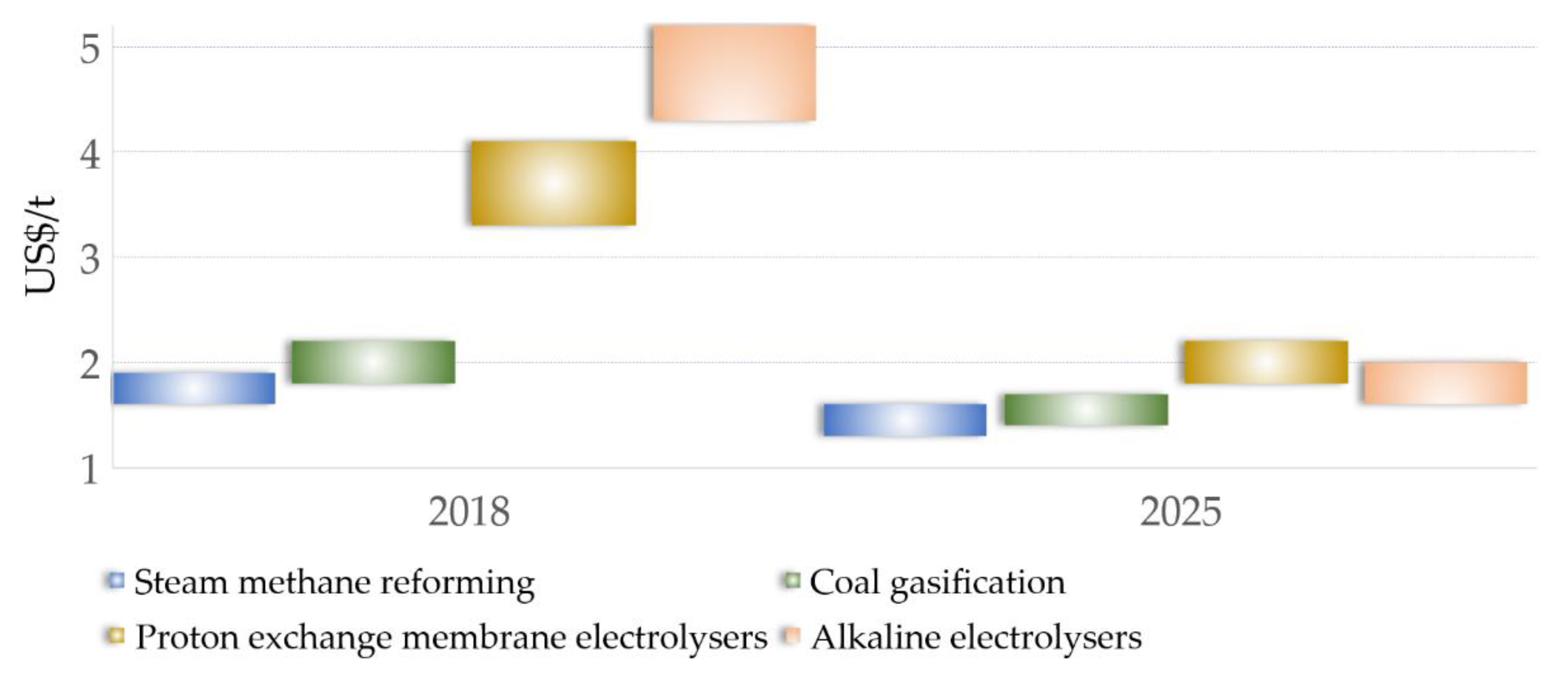

A comparative analysis of the present hydrogen production cost (LCoH, Levelized cost of hydrogen) of the hydrogen price component for the consumer, in the case of the listed hydrogen production methods (Figure 4), shows the expediency of choosing either a cheap or environmentally friendly and universal technology.

Nevertheless, the significant development of electrolysis technologies and the reduction of hydrogen electrolysis costs are expected in 2025 and further. It should be noted that two electrolysis technologies, both based on alkaline and solid polymeric membrane electrolytes, are being developed in parallel, and often manufacturers try to offer both technologies in their portfolio. The forecast for improvement of cost performance of water electrolysis, with the account of the scale effect in the transition to higher unit capacity electrolysis is shown in Figure 5.

The key technological barriers to hydrogen energy development include tasks related to achieving competitive technical and economic performance by the main hydrogen technologies:

- Decrease in the cost of hydrogen production based on “carbon-free” technologies, including those that allow hydrogen production only from water and electricity.

- Creation of scalable technology of large-capacity hydrogen transportation with acceptable technical and economic indicators [25].

- Decrease of capacity cost and present value of hydrogen fuel cell electricity generation.

Overcoming the technological barrier in the field of hydrogen production technology development is, to a large extent, reduced to engineering and technological tasks of further improvement of alkaline and solid polymer electrolyzers.

Hydrogen is an extremely volatile and flammable gas with a very low condensation temperature and the ability to embitter metals. For this reason, the storage and transport of hydrogen, especially in large quantities, is still a non-trivial and technologically unsolved task [25]. The storage and transport of hydrogen is the key technological barrier that can fundamentally change the market. At present, the following methods of hydrogen storage are offered, which allow for the reversible accumulation of hydrogen:

- Compressed under pressure up to 700 bar in steel or composite cylinders and containers

- In liquefied form in cryogenic tanks at −252 °C

- In chemically bound form in liquid organic hydrides (LOHC)The essence of the method consists in hydrogenation of organic matter, for example, toluene, as a rule, of aromatic nature, and obtaining in this way a hydrogen-containing chemical compound, significantly different in its properties from hydrogen, for example, methylcyclohexane. This substance is then catalytically dehydrated, the hydrogen is extracted, and the original substrate is returned to the process.

- In reversibly sorbing or hydrogen containing hydrides of metals and complex alloys within this storage method, two lines are being actively developed. One is associated with the use of reversible hydrogen sorbing at a pressure of up to 8 bar of complex hydrides, desorption of which occurs at low pressure. The second is the production of aqueous solutions of alkali metal borhydrides stabilized due to creation of highly alkaline pH, which are irreversibly dehydrated with decomposition on catalysts.

- Chemically bound in the form of ammonia NH3

The synthesis of ammonia by Gaber-Bosch has been thoroughly studied, used in large-tonnage industry since the 1930s, and the process has been optimized to the maximum achievable efficiency. Nevertheless, this method is the least mastered and technologically developed, as the difficulty lies in obtaining hydrogen from ammonia or using ammonia directly as fuel. None of these options has been brought to the industrial use stage.

The main technical characteristics of these storage methods are given in Table 1. At present, the most active works on the development of technologies and industrial realization of a number of the specified directions are moving in Japan and Australia.

Cryogenic storage with transportation of liquid hydrogen is more costly, but at the same time remains the only industrially developed technology of large-capacity transportation of hydrogen.

To a large extent, the technological barrier to storage and transportation of hydrogen is to simultaneously increase the mass content of hydrogen in the carrier up to 10% or more and to make the range of operating temperatures and pressures as close as possible to the natural conditions of the system operation, requiring neither ultra-high nor ultra-low temperatures and high pressures.

The fuel cells are the most promising way to generate electricity and heat from hydrogen due to their relatively high efficiency (55% and above). Two main lines of this technology development are being developed: low-temperature (with operating temperatures up to 100–120 °C) fuel cells with proton exchange membranes and high-temperature (with operating temperatures of 500–900 °C) fuel cells based on ion-conducting ceramics.

Despite the significant improvement of fuel cell performance, its cost parameters still significantly lose out to traditional generation. A particularly significant technological barrier is the reduction in the cost of capacity, which should be no more than USD 40 per kW, provided that mass production is at the level of 0.5 million fuel cell batteries per year. The cost of the Toyota Mirai fuel cell battery in 2016 was USD 183 per kW. According to the forecast of the U.S. Department of Energy, the cost of fuel cell capacity with PEM by 2025 may decline to USD 36 per kW, provided the production of at least 500 thousand fuel cell batteries.

3. Russian Perspective

3.1. Diffusion of RESs into Existing Energy System through the Development of Power Accumulators

Taking into account the current situation in the industry, the development of power storage systems will significantly reduce the severity of problems associated with the classical “bottlenecks” of the system power industry, including the Unified Energy System (UES) and isolated zones and individual power plants, as well as the issues of the formation and maintenance of electricity production and consumption [18,27,28]. Thus, equalization of the electricity demand schedule and reduction of cyclic peaks will allow for reducing the volume of forced reserves of the power system capacity, including the network capacity, and, accordingly, the cost of their maintenance. In turn, the optimization of modes of operation of equipment, especially for thermal power generation and the reduction of necessary maneuverability will allow for the reduction of specific operating costs (including fuel costs) and CO2 emissions. In addition, this will extend the service life of existing equipment, while reducing the need to build new facilities [29]. In the case of network equipment, network losses will naturally be decreased by reducing the volume of overflows. Also, the development of industrial storage of electricity will expand the possibilities for generating renewable energy, which is characterized by a variable level of available capacity.

There are settlements in Russia that are not connected to the Unified National Electric Network (UNEN). The majority of such facilities are located in hard-to-reach areas of the Far North and the Far East with undeveloped road and energy infrastructure [30]. Therefore, the technological connection of remote communities to the UNEN is either technically unsustainable or economically unjustified. The electricity supply to consumers in such communities is provided by local power systems. In this connection, it is expedient to develop renewable energy sources in isolated areas, where the cost of organic fuel amounts to 40–60% in the structure of the cost of electricity, and the introduction of hybrid units allows reducing the need for fuel and its costs [31].

About 63% (525 MW) of installed capacity of power generation facilities in isolated and hard-to-reach areas is concentrated in four regions: The Republic of Sakha (Yakutia), Kamchatka Krai, Krasnoyarsk Krai, and Yamalo-Nenets Autonomous District. The highest average regional specific power generation costs at power generation facilities in isolated and hard-to-reach areas are in the Republic of Sakha (Yakutia)-42.7 RUB/kWh (around 0.62 USD/ kWh). At the same time, the fuel balance of the power plants contains 90% of diesel fuel, which is imported from other regions of Russia under complicated logistic schemes, which leads to both higher costs and longer delivery terms [32].

An additional factor that determines the necessity to develop energy storage systems is the imbalance in the location of generation facilities in the country. Russia has a great potential for generation of electricity, including based on existing hydroelectric power plants (HPPs), which are not currently in demand under the conditions of the current specifics and territorial organization of industry in the country. This circumstance is a prerequisite for consideration of issues related to energy accumulation, including hydrogen fuel, as well as its use as an energy transportation tool.

3.2. Prerequisites for Green Hydrogen Development

The Russian production capacity for electricity accumulation in hydrogen fuel, estimated by the EnergyNet CPI on the basis of the value of potential electricity production at generating facilities loaded significantly below their installed capacity, is 2–3.5 million tons per year [26].

The total production potential of Russia in the field of hydrogen fuel, the disclosure of which does not require the construction of new generating facilities, can be estimated at 2–3.5 million tons of hydrogen per year, thus occupying 10–15% of the global market on the horizon of 2030, which is comparable to the country’s share in the world oil and gas markets [33].

A significant share of “locked” capacities that can be used for hydrogen production is concentrated in Russia in Siberia and the Far East, in close proximity to the most import-oriented Asian, in particular, Japanese markets. As part of this vector, it becomes possible to create industrial clusters for production and transportation of hydrogen and corresponding creation of new generating assets under conditions of export of hydrogen based on low-carbon generation, and first, hydro generation. Russia has competitive advantages if it enters the global hydrogen fuel market. This is primarily due to the logistical proximity of the regions of the Far Eastern Federal District to foreign markets for the sale of hydrogen, as well as the availability of a resource base. Also, first we can talk about the Japanese market, which is interested in hydrogen energy [10]. The sale price of hydrogen in Japan, taking into account the estimated costs of creating and operating an industrial asset for the production of hydrogen in the Far East, is only USD 3.4/kgH2. According to IEA research, by 2030, it will be more profitable for Japan to buy hydrogen than to produce it domestically (the ratio of USD 5.5/kgH2 (from Australia) to USD 6.5/kgH2 (own production).

The possibility to develop the domestic hydrogen fuel market in Russia is also determined by the possibility to use energy storage in the hydrogen cycle to increase energy supply efficiency in remote and isolated areas. Such territories are mainly concentrated in the Far North and regions of the Far East Federal District.

At the same time, remote and isolated areas often have a significant potential for renewable energy, but their effective use requires large capacity energy storage systems [34]. Storage of energy in the hydrogen cycle allows not only the use of RESs an effective means of replacing expensive diesel fuel in these territories, but also makes it possible to form local systems for the production and transportation of hydrogen as an energy carrier, which will reduce the transport shoulder of the “northern import,” decrease the cost of energy, and lower the required amount of budget subsidies. According to the Moscow Institute of Physics and Technology, Russia (MIPT) Arctic Technologies Institute, the cost of ownership of the power supply system of an isolated settlement with the capacity of 100 kW is 27% lower than that of a hybrid system combining wind power generation, backup diesel generators, and hydrogen cycle power storage systems. At the same time, hydrogen can be produced not only at the place of its consumption, but also delivered within the region from production centers with great opportunities for renewable energy use to end users. With the development of technologies, the cost of producing energy based on hydrogen using RES in remote areas will become cheaper. However, at the same time, we believe that there is no point in producing hydrogen in remote regions and using it as a source. In this context, hydrogen can be effectively used only as a storage device. It is possible to supply RES in the regions to power this region, however, as noted in the article, the stochasticity of electricity generation dictates the need to create a system of energy storage systems. For these regions, the creation of hydrogen storage is promising. It makes no sense to lay a pipeline for hydrogen there due to the high cost and low reliability. With the use of renewable energy sources in conjunction with hydrogen storage, there is now a good alternative due to the price and safety.

3.3. Vision of Russian Energy Scenarios

While studying the development of RESs in Russia, we proposed distinguishing three scenarios, two of which describe conservative and optimistic options for the development of the Russian power industry, taking into account the technological evolution, which implies gradual cheapening of equipment and standardization [35]. The third scenario (high-tech) is based on the hypothesis of revolutionary technological development of new technologies, innovative solutions to existing problems, while the risks preventing their use or development under current conditions will be removed (Table 2).

The conservative scenario assumes that hydrocarbon fuel will remain the main source of energy resources in the strategic perspective and that international environmental requirements will not be toughened, as well as the level of sanctions pressure. The demand for primary energy will increase as a result of higher living standards, while the cost of energy resources will be quite high [36,37]. In these conditions, large gas and, to a lesser extent, coal generation will remain the basis of the electric power industry. The share of renewable energy sources will be insignificant, despite higher growth rates as compared to other types of generation.

A large-scale modernization of the centralized energy sector is planned, while maintaining administrative regulation and the dominant position of large energy holdings. Local power engineering and some elements of the smart grid technology will be used mainly to solve private issues related to energy efficiency improvement.

The main direction of technological development of the industry will be increasing the efficiency of power plants. Typical solutions will be thermal insulation and installation of energy efficient devices and equipment. One of the main conditions to increase the competitiveness of Russian industrial enterprises will be to increase the efficiency of energy consumption [38].

The investments in energy development under this scenario will be made by a small number of large players with a significant role of state participation and regulation.

The optimistic scenario assumes that hydrocarbons will also remain the main energy resource in the foreseeable future. However, the projected passage of hydrocarbon production peaks in the next 35–40 years makes it necessary to ensure timely preparedness for post-carbon energy. The latter, most likely (taking into account existing trends), will be based on a new institutional environment formed on the basis of global and local climate agreements, tax and customs tariffs, and new technological standards.

Favorable environmental and economic conditions will boost the demand for natural gas. However, RESs will also grow much more dynamically than in the conservative scenario under the influence of growing demand for electricity, adoption of new environmental standards and cheaper equipment. At the same time, the volatility of electricity generation based on RESs will make the development of energy accumulation and storage technologies crucial.

The mass withdrawal of consumers from local power supply systems will result in a smaller number of consumers having to bear the cost of maintaining the centralized power system. The efficiency of large-scale power generation will be reduced, and it will lose its dominant role in the energy system. The upgrading of existing facilities and implementation of steam-gas cycle may slow down this process but will not change the trend itself.

The development of small power generation [39] and renewable energy sources will define the advanced technological milestones of this scenario, which are to increase energy efficiency with new carbon-free energy technologies (primarily wind and solar), fast reactor nuclear power plants, “smart houses,” energy storage systems, hybrid units, robotic devices, and new-class turbines. The market of energy service companies will gain dynamic development, gradually transforming the energy market into the market of energy supply and engineering services.

As a result of this scenario, by 2030, two sectors will be formed: traditional power production primarily focused on energy efficiency, and new energy, whose development will be stimulated by the state.

Under this scenario, Russian companies with the involvement of scientific teams may implement large-scale work to create domestic and localize advanced foreign technologies and production facilities for renewable energy generation and energy storage systems. At the same time, increasing the installed capacity of generating facilities based on renewable energy sources will have a negative impact on the load of thermal power plants and lead to the need to transform the heat supply system in the country.

Russian companies such as Rosatom, RusHydro, Rusnano, and Rosseti, that have both the necessary resources and competences, may be interested in promoting this scenario.

The high-tech scenario assumes that renewable resources will take the lead in the energy sector, with the main task of scaling them up and achieving economic efficiency in comparison with other energy sources. First, it will be due to the radical cheapening of solar and wind power generation. Natural gas will retain its significance, but compliance with stringent environmental requirements will be an important condition for its application. The key competencies in this scenario are being developed in such countries as the U.S., Germany, France, Japan, South Korea, and China.

The scenario assumes dynamic development of four fundamental elements that will change the architecture of energy: (1) demand management, (2) energy storage technologies, (3) active energy complexes, and (4) industry digitalization. The contours of the Russian power system will change towards the formation of a large number of self-supporting production and consuming cells, bounded by main lines (primarily based on large hydropower), which will become a source of backup power and a source of energy for large energy-intensive industries. Changes in the basic parameters of the energy system operation will lead to the formation of its new economics.

The main technological changes in the electric power industry will be aimed at the formation of a new “post-industrial” power industry, the market of services, and in the future, the market of technologies [40]. A noticeable niche in these markets will be occupied by companies that collect and analyze data, provide services for energy supply and saving [41].

The technological base of this scenario includes virtual and augmented reality technologies, micro grids and “smart power systems,” energy storage systems, robotic devices, Building Information Modeling (BIM) technologies, computing technologies for data analysis, “flexible” power generation technologies, fuel cell generators, the Internet of Things [41,42]. One of the most important technologies is electric transport, the large-scale development of which will require significant investments in the relevant infrastructure. The spread of electric vehicles with the possibility of their integration into the power distribution grid will contribute to the load equalization of the power system.

Communication with power consumers will obviously move away from power supply companies to other operators, who will gain control over the power platform for communication with power consumers. Similar processes are observed in other sectors of the economy. Thus, the world’s largest transport company Uber is not the owner of vehicles; the most popular media company Facebook does not create content; the largest retailer Alibaba does not have stores; the largest provider of temporary residence services Airbnb does not own real estate [43]. Energy companies will be engaged in the supply of electricity, and the owners of the “energy platform” will interact with users.

To embed Russia in this scenario, it is necessary to accelerate the formation of engineering competencies, which in the future will be the object of “export” of high-tech services and a source of income. Russian companies that may be interested in this scenario include Tavrida Electric, Energy, Rosatom, Rosnano, and partly RusHydro and Rosseti.

4. Case Study in Magadan Region

The project under consideration («Dyakov Ust-Srednekanskaya hydroelectric power plant (HPP)» (DUS)) on the example of a RusHydro company, which is one of the largest Russian energy company and leader in national renewable energy market with total capacity around 40 GW and annual power generation more than 140 billion kWh. The capacity of DUS hydrogen production is estimated by the North-West Center for Strategic Research to be about 34.5 thousand tons per year. This HPP with an installed capacity of 570 MW is located on the Kolyma River in the Magadan Region and is the most interesting project to accumulate generated electricity in the form of hydrogen. At the same time, the Magadan Region has a relatively short transport shoulder to Japan, which is a promising market for hydrogen.

Since the maximum capacity of the electrolysis plant that serves as a ballast load for the Ust-Srednekanskaya HPP is 531 MW, which significantly exceeds the capacity of commercial water electrolyzers, the calculation of indicators of the electrolysis plant operation mode is based on relative indicators of the power-to-gas process. The power-to-gas process family is used in energy storage and production systems of hydrogen, methane and synthesis gas, as well as heat energy. Efficiency of the process depends on its technological features, final product, application of gas compression systems and its nominal pressure. Characteristics of electrolyzers are presented in Table 3.

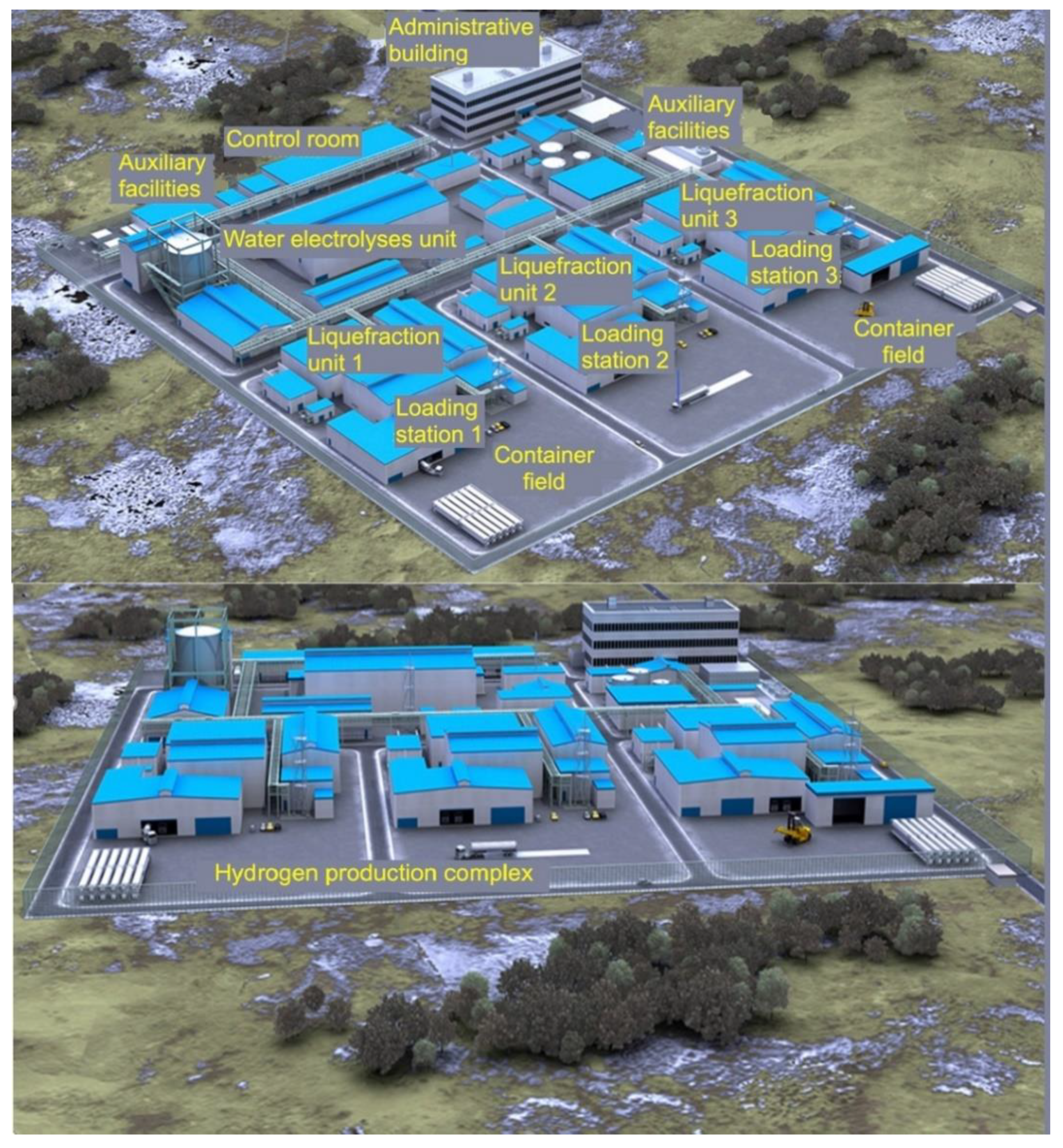

The project envisages construction of a pilot complex (Figure 6). Liquefied hydrogen transportation is planned to be carried out in specialized containers or tankers. The project is primarily aimed at the Japanese market. This is because the main advantage is the short transport distance from the HPP, the direct distance of only about 2000 km by air. Currently, delivery by pipeline transport is impossible since the existing technologies are not yet perfect and unreliable. In this term using of sea transport seems promising either: (1) based on low temperatures and transportation of liquefied hydrogen by tankers. One such successful example is the World’s First Liquefied Hydrogen (LH2) LNG Carrier, which was launched in the Japanese port of Kobe [44]. This was reported by Kawasaki Heavy Industries (KHI), which built the vessel. KHI is also building an LNG bunkering tanker for JV K-Line, Chubu Electric Power, Toyota Tsusho Corporation, and Nyk Line of a similar design; (2) by tanker, but not using low temperatures, due to the complexity of the supply and maintenance process, but with the help of ammonia-green ammonia tanker. However, the article does not aim to define the most cost-effective way of hydrogen fuel transportation, assuming that containerized shipping is considered the most preferable; however, it is obvious that with increasing hydrogen production it is reasonable to use larger vessels.

The proposed pilot project will be able to provide new jobs for residents of the respective region, which is an additional advantage of our research.

The hydrogen complex consists of the following elements:

- Plants for water electrolysis: a device for producing hydrogen by means of electrolysis of purified water.

- Liquefaction plants: devices for liquefaction of purified hydrogen by deep cooling

- Liquefied hydrogen storage tanks: Liquefied hydrogen storage tanks are also used to transport liquefied hydrogen.

- Container filling lines for hydrogen: transport lines used to transfer hydrogen from the liquefying plants to the tanks.

- Other buildings and structures.

An alkaline system of water electrolysis is offered, as this technology is well enough tested on large scale industrial projects and has comparatively low cost and long service life of the equipment used in this system of water electrolysis.

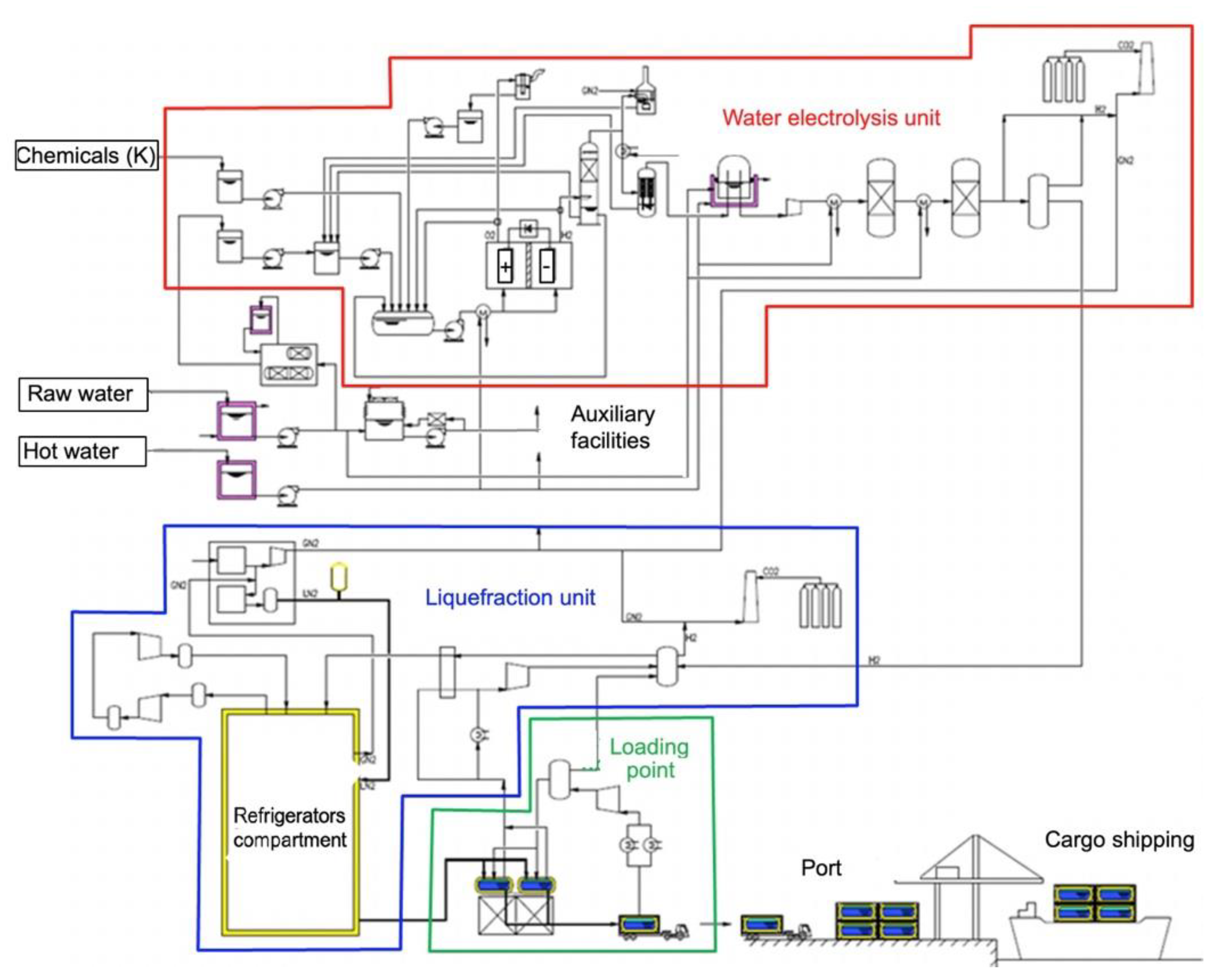

The diagram shown in Figure 7 shows the process of hydrogen production. The production of hydrogen is carried out with the help of water electrolysis units; further, the received hydrogen gets into liquefaction units, where the process of liquefaction takes place. The liquefied hydrogen is transferred along the lines to specialized containers/reservoirs. In their turn, filled containers are delivered to the port, where they are further loaded on a specialized transport vessel.

Because the Ust-Srednekanskaya HPP is located at a considerable distance from the sea, the cost of transporting equipment and the cost of construction are increasing. Under these conditions, construction of the complex at the site located near the Ust-Srednekanskaya HPP with subsequent transportation of hydrogen will be performed in specialized containers to the loading station. In the event of an increase in hydrogen production, the produced fuel may be transported by pipeline to the port and undergo liquefaction in liquefaction units at the loading base located in the port area.

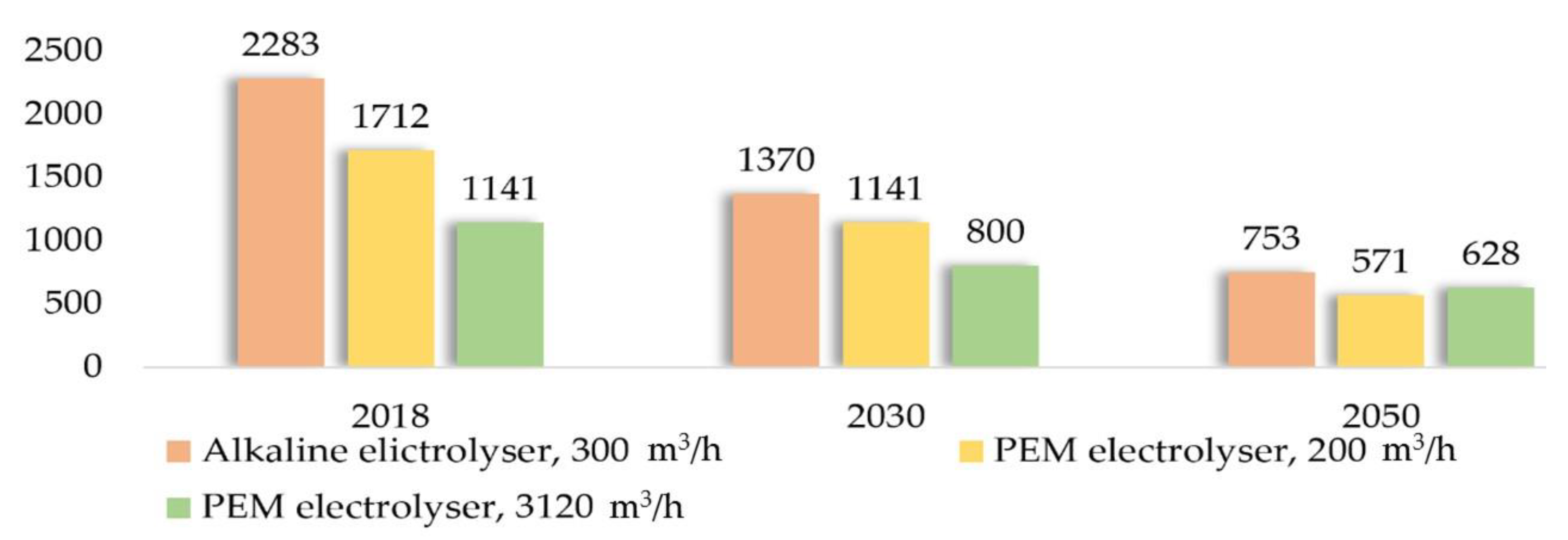

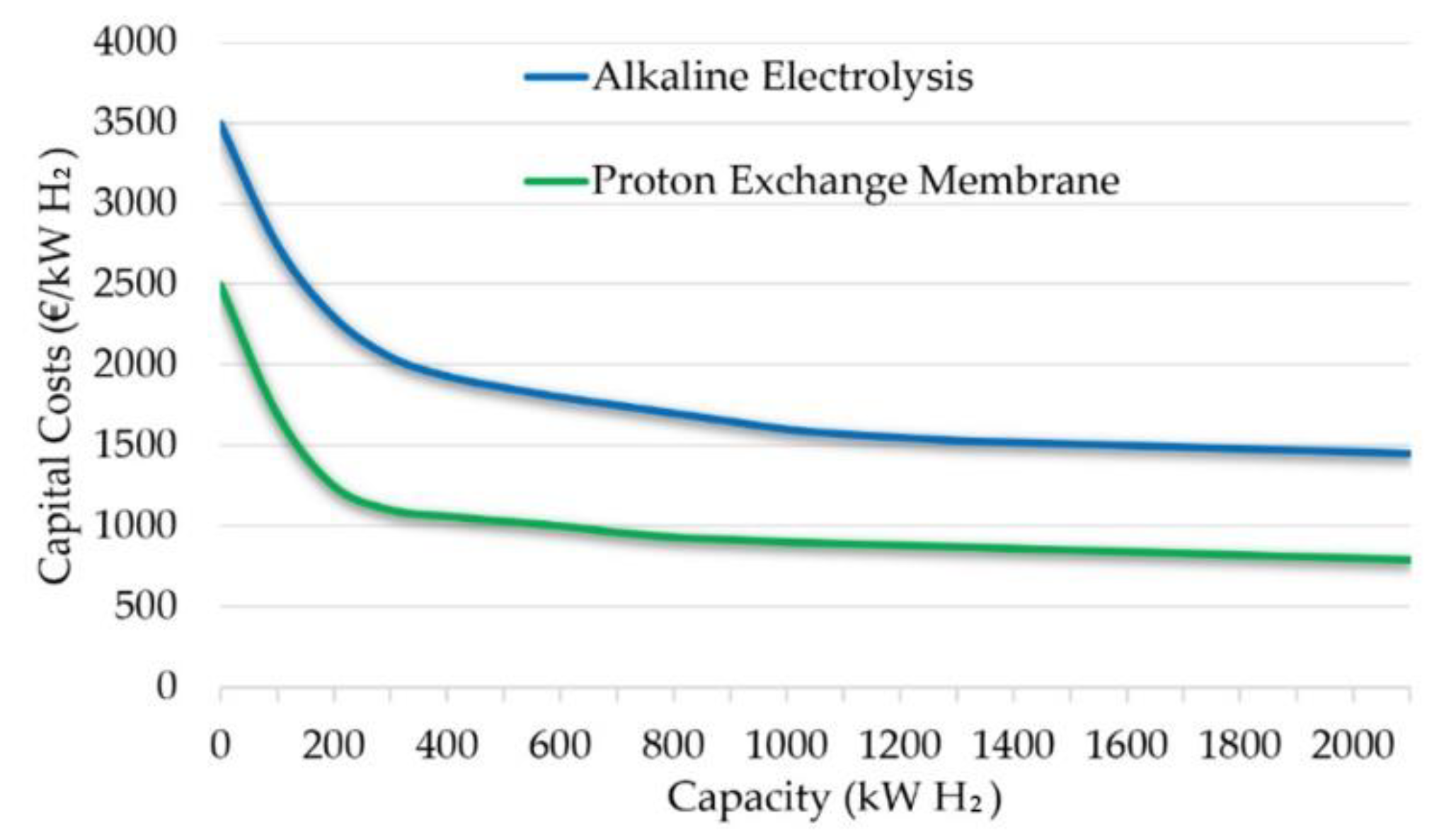

The amount of capital costs for electrolysis depending on the capacity of the electrolysis unit and the technology used is shown in Figure 8. Since capital cost of electrolysis with application of proton-exchange membrane technology is on the average 1.57 times lower than that of alkaline electrolyzers, it is the one to be considered in the calculation.

An example of calculation of the mass of produced hydrogen by the electrolysis plant is given in Table 4 for the maximum number of electrolyzers, 30 pcs. In the case that the quantity of electrolyzers is less than maximum, maximum power consumption is limited by the installed capacity of electrolyzers:

where is the installed capacity of the electrolysis plant; is the number of electrolysers installed at the electrolysis plant; is the rated capacity of the electrolysis plant (in this example 18.12 MW).

The mass of produced hydrogen relative to the number of electrolyzers. installed at the electrolysis plant is shown in Table 5.

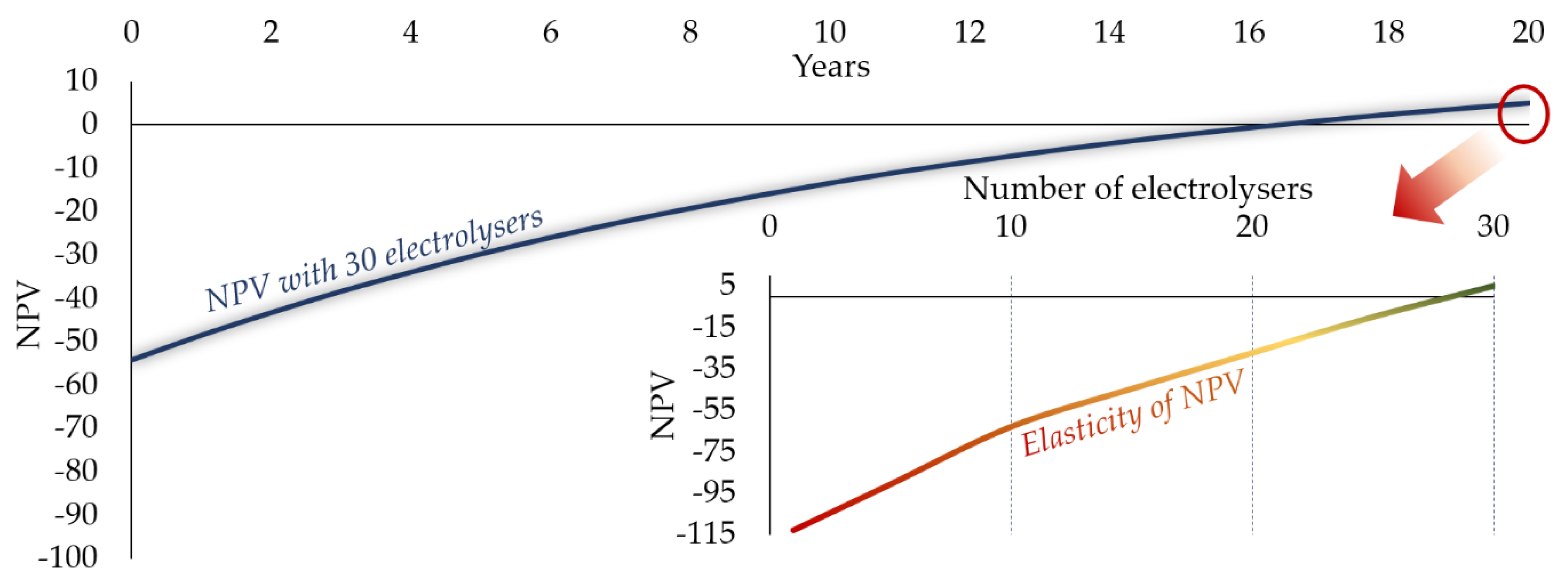

The economic criterion for choosing the installed capacity of the electrolysis plant is the maximum net discounted income (Net Present Value (NPV)) for the accounting period (taken equal to 20 years). The cost of hydrogen on the world market for 2020 ranges from $12.85/kg to $16.00/kg (from 888.22 to 1105.95 rubles/kg at the current exchange rate). The typical price is $ 13.99/kg–967 rubles/kg. The calculation of economic indicators is carried out in an iterative manner, depending on the number of electrolyzers installed at the electrolysis plant. NPV of the electrolysis plant in billion rubles (the exchange rate for December 2020 is 0.014 USD) the cumulative total is shown in Figure 9.

The obtained results have shown that the proposed electrolysis plant achieves payback and positive NPV (net present value) with the number of electrolyzers close to the maximum. The highest NPV is achieved at the maximum number of 30 electrolyzers, = 543.6 MW. Thus, the proposed specific solution could be one of the possible ways to ensure the operational efficiency of the plant, as well as to generate additional income for RusHydro Group. However, estimated cost of hydrogen production is $12.5/kg. Taking into account that the transportation cost is $0.96/kg, the gap between average market price and total expenses is extremely low, which makes this project a relatively risky investment, from the financial point of view.

5. Discussion

The conducted analysis shows that the formation of new energy sector is based on renewable energy development, smart network infrastructure and energy storage systems, which, along with other technological solutions, will create its innovative architecture. Competitiveness in the “new” energy sector will largely depend on engineering competencies that determine the ability to create innovative concepts [45] and apply new technological solutions [46].

This article describes three main scenarios of power engineering development (conservative, optimistic and high-tech), which describe different variants of industry construction. The analysis of the strategic documents of the Russian power industry (Table 6) shows the necessity of changes in the part of formation of technological competences, aimed at implementing energy transition. The Russian power industry is going to develop according to the optimistic scenario with significant share of elements from the conservative scenario. Unfortunately, the high-tech scenario is neither fully nor partially visible in Russian strategic documents, which is explained by the lack of interaction and cooperation of the main stakeholders (authorities, companies, research institutes, and some others) [47].

To maintain Russia’s energy competitiveness, it is necessary to take large-scale actions of the state and companies to create an effective environment for advanced technologies and production facilities development, as well as work to form engineering competencies that could be a part of high-tech services export, which correlates with aims of innovative development of the national economy [48].

The present energy transition which is focused on the replacement of hydrocarbon fuels with RES is a fundamental challenge of the 21st century, which is required unconventional approaches [49] to be overcame. Further development of renewable electricity generation will require the creation of new sustainable storage and transport facilities [50], and what is more important, the provision of attractiveness of such solutions [51].

Accumulation of electric energy in the hydrogen cycle for the purpose of further supply of hydrogen as an energy carrier is a promising line of energy storage systems development, which was showed in this paper and correlates with similar studies [52]. However, the development of new “RES + Hydrogen” energy infrastructure requires proper attention to the creation of several markets, associated with hydrogen economy ecosystems [53], since there are various controversial issues, related not only to a specific application, like hydrogen transport [54], but also to a theoretical aspects of energy paradigm replacement [55].

6. Conclusions

This study contains an analysis of the key trends of renewable energy development and prospects for its further scaling through an implementation of green hydrogen solutions and an involvement of resource-based countries in energy transition processes. Russia was considered as an example of such countries and analyzed in three directions to be compared with Global renewable energy industry: (1) diffusion of RESs into existing energy system through the development of power accumulators; (2) prerequisites for green hydrogen development; (3) possible strategic scenarios of energy industry development.

The study also covers technical and economic analysis of pilot green hydrogen production project, located in Magadan region (Russia). This project is possible for implementation by the Russian company RusHydro, included in the Top-5 hydropower companies in the world and based on hydropower plant, with an installed capacity of 570 MW and planned hydrogen production capacity around 34.5 thousand tons per year. The choice of the “HPP + hydrogen production” combination is explained by the availability of free capacity in the region’s energy system, which provides hydrogen plant with guaranteed electricity with the possibility of scaling the production volume. Such stability could not be provided by any other RES. Another reason is the production of green hydrogen with a low carbon footprint as a part of the global strategy to achieve carbon neutrality. In addition, power generation at HPPs is one the most competitive energy solution, in terms of costs. Despite this, our calculations show that economic efficiency of the project is questionable: (1) total costs of hydrogen production ($12.5/ kg) and transportation ($0.96/ kg) are only 4% lower than average market price ($14/ kg); (2) NPV is on the edge of zero; (3) the payback period is near 17 years; (4) the decrease in project capacity below 543.6 MW (less than 10%) will immediately lead to a negative profitability.

Moreover, despite the relatively short transportation distance to a promising hydrogen market (Japan), there are a lot of uncertainties and risks associated with this project: (1) the immature and unsafe technologies for transporting and storing hydrogen; (2) the lack of demand for hydrogen fuel both within the country and on the global market (the hydrogen market is still a “buyer market”, so the current price of hydrogen provides only minimal profitability for such projects). Nevertheless, it should be taken into account that such strategic projects are at the edge of energy transition. Many companies are positive in their forecasts of the demand for hydrogen in global markets. As a result, there is an increasing interest in using renewable energy facilities as a testing ground for pilot hydrogen projects. After the emergence of necessary mature and efficient infrastructure technologies, it will be possible to start large-scale implementation of hydrogen production. We see it as an opportunity to lead transnational energy trade of green hydrogen, which could be competitive in the medium term, especially with proper state support.

In case of Russia, our scenarios analysis shows that the energy industry is going to develop according to the optimistic scenario with significant share of elements from the conservative scenario. The transition to a high-tech scenario requires several changes in the process of technological reserves formation, as well as removing institutional and infrastructure risks.

Author Contributions

Conceptualization, L.K. and A.K.; methodology, A.K. and P.T.; validation, L.K. and A.S.; writ-ing—original draft preparation, A.K.; writing—review and editing, L.K., P.T. and A.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- International Energy Agency (IEA). Total Installed Power Capacity by Fuel and Technology 2019–2025, Main Case. Available online: https://www.iea.org/data-and-statistics/charts/total-installed-power-capacity-by-fuel-and-technology-2019-2025-main-case (accessed on 2 December 2020).

- Lazard. Levelized Cost of Storage Analysis 2017. Available online: https://www.lazard.com/perspective/levelized-cost-of-storage-2017/ (accessed on 2 December 2020).

- ExxonMobil. Forecast of Energy Development in 2017 for the Period up to 2040 Inclusive. Available online: https://www.nrcan.gc.ca/sites/www.nrcan.gc.ca/files/energy/energy-resources/ExxonMobil_2017_outlook_for_energy_highlights.pdf (accessed on 2 December 2020).

- Bloomberg; Nereim, V.; Cunningham, S. Saudis, SoftBank Plan World’s Largest Solar Project. 2018. Available online: https://www.bloomberg.com/news/articles/2018-03-28/saudi-arabia-softbank-ink-deal-on-200-billion-solar-project (accessed on 2 December 2020).

- The Energy Research Institute; National Development and Reform Commission. China 2050 High Renewable Energy Penetration Scenario and Roadmap Study. 2015. Available online: https://www.efchina.org/Attachments/Report/report-20150420/China-2050-High-Renewable-Energy-Penetration-Scenario-and-Roadmap-Study-Executive-Summary.pdf (accessed on 2 December 2020).

- Rahmann, C.; Chamas, S.I.; Alvarez, R.; Chavez, H.; Ortiz-Villalba, D.; Shklyarskiy, Y. Methodological Approach for Defining Frequency Related Grid Requirements in Low-Carbon Power Systems. IEEE Access 2020, 8, 161929–161942. [Google Scholar] [CrossRef]

- Renew Economy. The stunning numbers behind success of Tesla big battery. Available online: https://reneweconomy.com.au/the-stunning-numbers-behind-success-of-tesla-big-battery-63917/ (accessed on 2 December 2020).

- Savard, C.; Iakovleva, E.V. A suggested improvement for small autonomous energy system reliability by reducing heat and excess charges. Batteries 2019, 5, 29. [Google Scholar] [CrossRef] [Green Version]

- Vasilkov, O.S.; Dobysh, V.S. Features of Application Hybrid Energy Storage in Power Supply Systems. In Proceedings of the 2019 IEEE Conference of Russian Young Researchers in Electrical and Electronic Engineering (ElConRus), Saint Petersburg/Moscow, Russia, 28–31 January 2019; pp. 728–730. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). The Future of Hydrogen Seizing Today’s Opportunities. Available online: https://www.iea.org/reports/the-future-of-hydrogen (accessed on 2 December 2020).

- Ministry of Energy of the Russian Federation. Concept for the Development of the Electricity Storage Systems Market in the Russian Federation. 2018. Available online: https://minenergo.gov.ru/view-pdf/9013/74739 (accessed on 2 December 2020). (In Russian)

- McKinsey Global Institute. Disruptive Technologies: Advances that will Transform Life, Business, and the Global Economy. 2013. Available online: https://www.mckinsey.com/~/media/McKinsey/Business%20Functions/McKinsey%20Digital/Our%20Insights/Disruptive%20technologies/MGI_Disruptive_technologies_Executive_summary_May2013.pdf (accessed on 2 December 2020).

- Data from GuideHouse Insights. Available online: https://guidehouseinsights.com/reports (accessed on 2 December 2020).

- Bloomberg New Energy Finance. Global Storage Market to Double Six Times by 2030. 2017. Available online: https://about.bnef.com/blog/global-storage-market-double-six-times-2030/ (accessed on 2 December 2020).

- Cherepovitsyn, A.E.; Ilinova, A.A.; Evseeva, O.O. Stakeholders management of carbon sequestration project in the state-business-society system. J. Min. Inst. 2019, 240, 731. [Google Scholar] [CrossRef] [Green Version]

- Kuznetsov, P.A.; Abrmovich, B.N.; Sychev, Y.A.; Mukminova, D.Z. Assessment and data analysis of beneficial implementation of cogeneration modules at mining enterprises to minimize negative influence on the environment. J. Phys. Conf. Ser. 2019, 1333, 032048. [Google Scholar] [CrossRef]

- Gerra, D.D.; Iakovleva, E.V. Sun Tracking System for Photovoltaic Batteries in Climatic Conditions of the Republic of Cuba. In Proceedings of the International Scientific Electric Power Conference, Saint Petersburg, Russia, 23–24 May 2019. [Google Scholar]

- Kirsanova, N.Y.; Lenkovets, O.M.; Nikulina, A.Y. Renewable energy sources (RES) as a factor determining the social and economic development of the arctic zone of the Russian Federation. In Proceedings of the 18th International Multidisciplinary Scientific GeoConference SGEM2018, Albena, Bulgaria, 2–8 July 2018. [Google Scholar] [CrossRef]

- Pashkevich, M.A.; Petrova, T.A. Development of an operational environmental monitoring system for hazardous industrial facilities of Gazprom Dobycha Urengoy. In Proceedings of the International Conference “Complex Equipment of Quality Control Laboratories”, Saint Petersburg, Russia, 14–17 May 2019. [Google Scholar] [CrossRef]

- Pashkevich, M.A.; Matveeva, V.A.; Danilov, A.S. Migration of pollutants from the mining waste disposal territories on the Kola Peninsula. Gorn. Zhurnal 2019, 1, 17–21. [Google Scholar] [CrossRef]

- Federal Ministry for Economic Affairs and Energy. The National Hydrogen Strategy. 2020. Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Energie/die-nationale-wasserstoffstrategie.pdf?__blob=publicationFile&v=12 (accessed on 2 December 2020). (In German)

- The International Renewable Energy Agency (IRENA). Electricity Storage and Renewables: Costs and Markets to 2030. 2017. Available online: http://www.irena.org/-/media/files/irena/agency/publication/2017/oct/irena_electricity_storage_costs_2017.pdf (accessed on 2 December 2020).

- CSIRO. Available online: https://www.csiro.au/en/ (accessed on 2 December 2020).

- Cummins. Sustainability, Plus Performance. Available online: https://www.cummins.com/new-power (accessed on 2 December 2020).

- Litvinenko, V.S.; Tsvetkov, P.S.; Dvoynikov, M.V.; Buslaev, G.V. Barriers to implementation of hydrogen initiatives in the context of global energy sustainable development. J. Min. Inst. 2020, 244, 428–438. [Google Scholar] [CrossRef]

- EnergyNet. Prospects for Russia in the Global Hydrogen Fuel Market. Expert Analytical Report. Moscow. 2018. Available online: https://www.eprussia.ru/upload/iblock/ede/ede334adeb4c282549a71d6fec727d64.pdf (accessed on 2 December 2020).

- Berezikov, S.A. Structural changes and innovation economic development of the Arctic regions of Russia. J. Min. Inst. 2019, 240, 716. [Google Scholar] [CrossRef] [Green Version]

- Savard, C.; Nikulina, A.; Mécemmène, C.; Mokhova, E. The electrification of ships using the Northern Sea Route: An approach. J. Open Innov. Technol. Mark. Complex. 2020, 6, 13. [Google Scholar] [CrossRef] [Green Version]

- Shklyarskiy, Y.; Hanzelka, Z.; Skamyin, A. Experimental study of harmonic influence on electrical energy metering. Energies 2020, 13, 5536. [Google Scholar] [CrossRef]

- Bogachev, V.F.; Gorenburgov, M.A.; Alekseeva, M.B. Systemic Diagnostics of the Arctic Industry Development Strategy. J. Min. Inst. 2019, 238, 450. [Google Scholar] [CrossRef] [Green Version]

- Belsky, A.A.; Skamyin, A.N.; Vasilkov, O.S. The use of hybrid energy storage devices for balancing the electricity load profile of enterprises. Energetika Proc. CIS High. Educ. Inst. Power Eng. Assoc. 2020, 63, 212–222. [Google Scholar] [CrossRef]

- Batueva, D.E.; Shklyarskiy, J.E. Increasing efficiency of using wind diesel complexes through intellectual forecasting power consumption. In Proceedings of the 2019 IEEE Conference of Russian Young Researchers in Electrical and Electronic Engineering (ElConRus), Saint Petersburg/Moscow, Russia, 28–31 January 2019; pp. 434–436. [Google Scholar] [CrossRef]

- NP Market Council. Prospects for Russia in the global Hydrogen Fuel Market. Expert and Analytical Report. 2018. Available online: https://www.np-sr.ru/ru/content/47872-perspektivy-rossii-na-globalnom-rynke-vodorodnogo-topliva-ekspertno-analiticheskiy (accessed on 2 December 2020).

- Belsky, A.A.; Dobush, V.S.; Haikal, Sh.F. Operation of a Single-phase Autonomous Inverter as a Part of a Low-power Wind Complex. J. Min. Inst. 2019, 239, 564–569. [Google Scholar] [CrossRef]

- Kalimullin, L.V. Main trends and scenarios of the development of the world energy. ECO 2019, 49, 66–82. [Google Scholar] [CrossRef]

- The Energy Research Institute of the Russian Academy of Sciences; The Analytical Center for the Government of the Russian Federation. Forecast of the Development of Energy in the World and Russia 2016; Makarova, A.A., Grigorieva, L.M., Mitrova, T.A., Eds.; ERI RAS—ACRF: Moscow, Russia, 2016.

- Yurak, V.V.; Dushin, A.V.; Mochalova, L.A. Vs sustainable development: Scenarios for the future. J. Min. Inst. 2020, 242, 242. [Google Scholar] [CrossRef]

- Litvinenko, V. The Role of Hydrocarbons in the Global Energy Agenda: The Focus on Liquefied Natural Gas. Resources 2020, 9, 59. [Google Scholar] [CrossRef]

- Tcvetkov, P.; Cherepovitsyn, A.; Makhovikov, A. Economic assessment of heat and power generation from small-scale liquefied natural gas in Russia. Energy Rep. 2020, 6, 391–402. [Google Scholar] [CrossRef]

- Yun, J.J.; Kim, D.; Yan, M.-R. Open Innovation Engineering—Preliminary Study on New Entrance of Technology to Market. Electronics 2020, 9, 791. [Google Scholar] [CrossRef]

- Zhukovskiy, Y.; Batueva, D.; Buldysko, A.; Shabalov, M. Motivation towards energy saving by means of IoT personal energy manager platform. J. Phys. Conf. Ser. 2019, 1333. [Google Scholar] [CrossRef]

- Litvinenko, V.S. Digital Economy as a Factor in the Technological Development of the Mineral Sector. Nat. Resour. Res. 2020, 29, 1521–1541. [Google Scholar] [CrossRef]

- Afanasyev, G. Guide to Creative Territory. Technological Companies. 2013. Available online: http://erazvitie.org/article/rukovodstvo-po-kreativnoj-territorii (accessed on 2 December 2020). (In Russian).

- View. Japan Launches World’s First Liquid Hydrogen Carrier. Available online: https://www.h2-view.com/story/japan-launches-worlds-first-liquid-hydrogen-carrier/ (accessed on 2 December 2020).

- Dvoynikov, M.; Buslaev, G.; Kunshin, A.; Sidorov, D.; Kraslawski, A.; Budovskaya, M. New Concepts of Hydrogen Production and Storage in Arctic Region. Resources 2021, 10, 3. [Google Scholar] [CrossRef]

- Klimenko, V.V.; Fedotova, E.V.; Tereshin, A.G. Vulnerability of the Russian power industry to the climate change. Energy 2018, 142, 1010–1022. [Google Scholar] [CrossRef]

- Seliverstov, V.E. Strategic planning and strategic errors: Russian realities and trends. Reg. Res. Russ. 2018, 8, 110–120. [Google Scholar] [CrossRef]

- Zemtsov, S.; Barinova, V.; Pankratov, A.; Kutsenko, E. Potential High-Tech Clusters in Russian Regions: From Current Policy to New Growth Areas. Foresight STI Gov. 2016, 10, 34–52. [Google Scholar] [CrossRef]

- Davidson, D.J. Exnovating for a renewable energy transition. Nat. Energy 2019, 4, 254–256. [Google Scholar] [CrossRef]

- Schmidt, O.; Melchior, S.; Hawkes, A.; Staffell, I. Projecting the future levelized cost of electricity storage technologies. Joule 2019, 3, 81–100. [Google Scholar] [CrossRef] [Green Version]

- Rubin, E.S.; Azevedo, I.M.; Jaramillo, P.; Yeh, S. A review of learning rates for electricity supply technologies. Energy Policy 2015, 86, 198–218. [Google Scholar] [CrossRef]

- Khalid, F.; Dincer, I.; Rosen, M.A. Analysis and assessment of an integrated hydrogen energy system. Int. J. Hydrog. Energy 2016, 41, 7960–7967. [Google Scholar] [CrossRef]

- Ball, M.; Weeda, M. The hydrogen economy–vision or reality? Int. J. Hydrog. Energy 2015, 40, 7903–7919. [Google Scholar] [CrossRef]

- Salvi, B.L.; Subramanian, K.A. Sustainable development of road transportation sector using hydrogen energy system. Renew. Sustain. Energy Rev. 2015, 51, 1132–1155. [Google Scholar] [CrossRef]

- Maggio, G.; Nicita, A.; Squadrito, G. How the hydrogen production from RES could change energy and fuel markets: A review of recent literature. Int. J. Hydrog. Energy 2019, 44, 11371–11384. [Google Scholar] [CrossRef]

Figure 1.

Forecast of the total electric capacity until 2025 according to International Energy Agency (IEA) analytical data [1].

Figure 1.

Forecast of the total electric capacity until 2025 according to International Energy Agency (IEA) analytical data [1].

Figure 2.

Structure of global and local challenges.

Figure 3.

Hydrogen cost forecast for end user by 2025, USD per kg. Data from [22].

Figure 3.

Hydrogen cost forecast for end user by 2025, USD per kg. Data from [22].

Figure 4.

Presented hydrogen production cost (LCOH), USD per kg. Data from [23].

Figure 4.

Presented hydrogen production cost (LCOH), USD per kg. Data from [23].

Figure 5.

Cost of water electrolyzers’ capacity, USD per kW. Data from [24].

Figure 5.

Cost of water electrolyzers’ capacity, USD per kW. Data from [24].

Figure 6.

Planned hydrogen complex.

Figure 7.

General block diagram of the hydrogen complex.

Figure 8.

Capital cost of electrolysis depending on capacity of electrolytic unit and technology used.

Figure 8.

Capital cost of electrolysis depending on capacity of electrolytic unit and technology used.

Figure 9.

Net Present Value (NPV) of the electrolysis plant, RUB billion.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Technological characteristics of hydrogen storage methods. Data from [26].

Table 1.

Technological characteristics of hydrogen storage methods. Data from [26].

| Storage Method | Mass Content of Hydrogen | Process Operating Temperatures | Process Operating Pressures |

|---|---|---|---|

| Steel cylinders for compressed hydrogen | Up to 1% | 20–40 °C | 150 bar |

| Composite high-pressure cylinders for compressed hydrogen | 5–7% | 20–40 °C | 350 bar |

| Ultra-high-pressure composite cylinders for compressed hydrogen | 10.5–13.8% | 20–40 °C | 700 bar |

| Cryogenic tanks for liquefied hydrogen | Up to 7.1% | −252 °C | 1 bar |

| Liquid organic hydrides | Up to 7.2% | 180–280 °C | 1–10 bar |

| Reversibly hydrogenated metals and alloys (metal hydrides) | 1.5–7.5% | 100–300 °C | 1–5 bar |

| Liquid ammonia | 17% | 400–600 °C | 350–500 bar |

Table 2.

Energy scenarios.

| Feature | Conservative | Optimistic | High-Tech |

|---|---|---|---|

| The structure of consumption of primary resources | Large share of gas generation, low share of nuclear generation and renewable energy | The prevalence of natural gas, a significant share of nuclear, hydropower generation and RESs | Comparable shares of gas, nuclear, hydropower and RESs |

| Generation structure | Dominance of large generation, the share of small generation is insignificant | The prevalence of large generation, the share of small generation is significant | Comparable shares of large and small generation |

| Main focus | Energy efficiency | Energy efficiency, new carbon-free energy technologies | Digitalization, technology market, distributed generation |

| RESs (without hydro generation) | Low RESs share | Significant share of RESs | RESs are a key type of generation |

| Environmental requirements | Low | Medium | High |

| Energy consumption | High | Low | Medium |

| Investment activity | Narrow circle of investors and a small amount of investment. | Wide range of investors, including the state. Significant volume of investments. | Wide range of investors (state and private). |

Table 3.

Characteristics of different types of electrolyzers.

| Electrolyser Type | Specific Power Consumption, kWh/m3 | Productivity, m3/h | Productivity, m3/h Rated Capacity of the Plant, MW | System LifeTime, Years |

|---|---|---|---|---|

| Alkaline electrolyser | 3.8–4.4 | 2400–3880 | 12.874 | 20 |

| Proton-exchange membrane | 4.53 | 4000 | 18.12 | 20 |

Table 4.

Calculation of hydrogen production volume by electrolysis plant.

| Month | V(H2), m3 | m(H2), kg | |||

|---|---|---|---|---|---|

| 1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 4 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 5 | 112.5 | 112.5 | 61,231.7 | 13,516,932.6 | 1,215,172.2 |

| 6 | 4.0 | 4.0 | 121.4 | 26,790.6 | 2408.5 |

| 7 | 531.0 | 531.0 | 372,588.2 | 82,249,052.2 | 7,394,189.8 |

| 8 | 531.0 | 531.0 | 372,616.3 | 82,255,256.5 | 7,394,747.6 |

| 9 | 192.0 | 192.0 | 116,474.0 | 25,711,690.7 | 2,311,481.0 |

| 10 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 11 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 12 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Year: | - | - | 923,000 MW hr | 203.8 mln. m3 | 18,318.0 t |

* —total monthly consumption of the ballast load, MWh.

Table 5.

Dependence of the mass of hydrogen produced by the electrolysis plant on the number of electrolyzers. installed at the plant.

Table 5.

Dependence of the mass of hydrogen produced by the electrolysis plant on the number of electrolyzers. installed at the plant.

| 1 | 5 | 10 | 15 | 20 | 25 | 30 | |

|---|---|---|---|---|---|---|---|

| m(H2), t | 134.8 | 3539.9 | 7833.5 | 10,663.0 | 13,338.5 | 16,013.9 | 18,318.0 |

Table 6.

The vision of energy progress scenarios in Russia’s strategic documents [A], [B], [C], and [D].

Table 6.

The vision of energy progress scenarios in Russia’s strategic documents [A], [B], [C], and [D].

| Feature | Target Vision According to Strategic Documents | Scenario Matching | |

|---|---|---|---|

| Primary resource consumption structure | The prevalence of natural gas, a significant share of nuclear power generation and renewable energy sources | The share of hydrogeneration in the structure of electric energy production by 2050 will make 18%, the share of nuclear generation is 21% [A]. | Optimistic |

| Energy efficiency | Energy efficiency, development of energy saving and improvement of energy efficiency | Decrease in losses of electric energy in electric grids by 2035 compared to 2018 will decrease by 3.3 percentage points and will amount to 7.3% [A], by 2050 will decrease by 4.6 percentage points and amount to 6% [D]. The specific consumption of equivalent fuel for the supply of electrical energy by 2030 compared to 2017 will decrease by 9.4% and will amount to 287.2 g/kW * h, and by 2050 will decrease by 18 percentage points and amount to 260.1 g/kW * h [D]. | Conservative |

| Generation structure | Large generation dominance, small generation share is insignificant | The basis of the electric power industry will be the existing centralized power supply systems based on large power plants [A]. | Conservative |

| Main focus | Energy efficiency | At an average annual GDP growth rate of 2–3%, the average energy consumption growth rate will be 1.4–1.6% [A]. | Conservative |

| RESs (without hydro generation) | Low share of RESs | The share of RESs in the total structure of electric energy production will be 2% by 2035 [A] and 4% by 2050 [D]. Energy production by RES (excluding HPP) will amount to 25 billion kWh by 2030, and 55 billion kWh by 2050 [D]. | Conservative |

| Hydrogen | Development of production and consumption of hydrogen | Hydrogen exports in 2035 will amount to 2 million tons [A]. The main task is joining the state among the leaders in the production and export of hydrogen [A]. | Optimistic |

| Environmental requirements | Medium | Implementation of provisions aimed at implementing the Paris Climate Accord [A]. Greenhouse gas emissions (million tons of CO2-eq.) in the energy sector by 2050 compared with 2017 to decrease by 6.2% (with a GDP growth of 141%) [D]. | Optimistic |

| Energy consumption level | High | In the case of an average GDP growth rate of 3.2% per year, the average growth rate of energy consumption for the period 2021–2026 will be 1.7% [C]. Electric energy consumption by 2035 will increase by 30% compared to 2015 to the level of 1345.2 billion kWh [B]. | Conservative |

| Investment activity | Investors are mainly of state or quasi-state nature. Significant number of investments. | The main sources of investment will be own funds, attracted funds-loans of Russian financial institutions and funds from the issue of shares [A]. | Optimistic/Conservative |

Source: [A]-draft Energy Strategy of Russia for the period until 2035; [B] General Scheme of electric power industry facilities location until 2035; [CScheme and program for the development of the UES of Russia for 2020–2026; [D]-draft strategy for the long-term development of the Russian Federation with a low level of greenhouse gas emissions until 2050.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kopteva, A.; Kalimullin, L.; Tcvetkov, P.; Soares, A. Prospects and Obstacles for Green Hydrogen Production in Russia. Energies 2021, 14, 718. https://doi.org/10.3390/en14030718

AMA Style

Kopteva A, Kalimullin L, Tcvetkov P, Soares A. Prospects and Obstacles for Green Hydrogen Production in Russia. Energies. 2021; 14(3):718. https://doi.org/10.3390/en14030718

Chicago/Turabian StyleKopteva, Alexandra, Leonid Kalimullin, Pavel Tcvetkov, and Amilcar Soares. 2021. "Prospects and Obstacles for Green Hydrogen Production in Russia" Energies 14, no. 3: 718. https://doi.org/10.3390/en14030718

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.