Disclosure Compliance with Different ESG Reporting Guidelines: The Sustainability Ranking of Selected European and Hungarian Banks in the Socio-Economic Crisis Period

Abstract

:1. Introduction

2. Relevant Literature

3. Results and Discussion

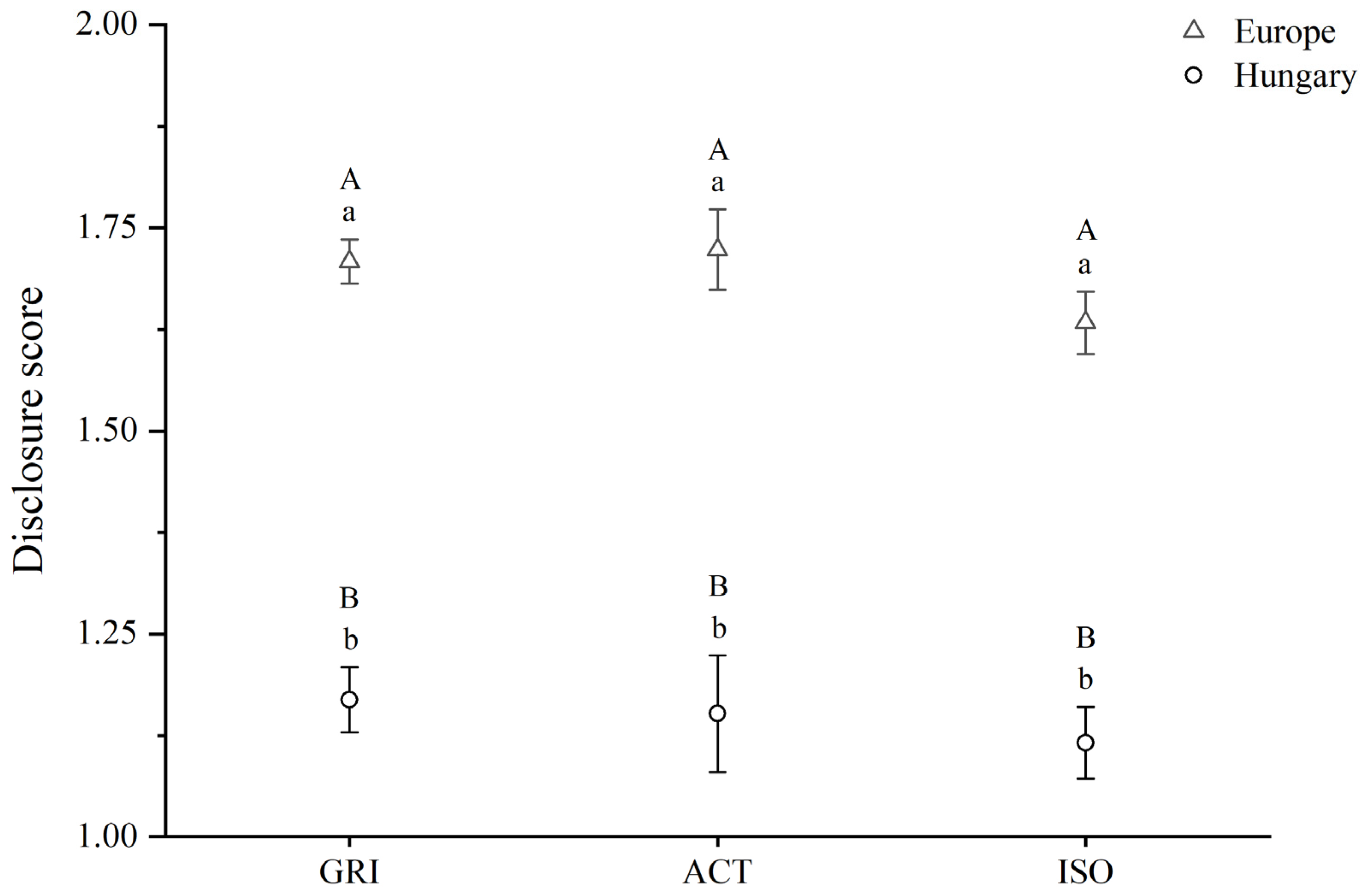

3.1. General Compliance with Reporting Guidelines

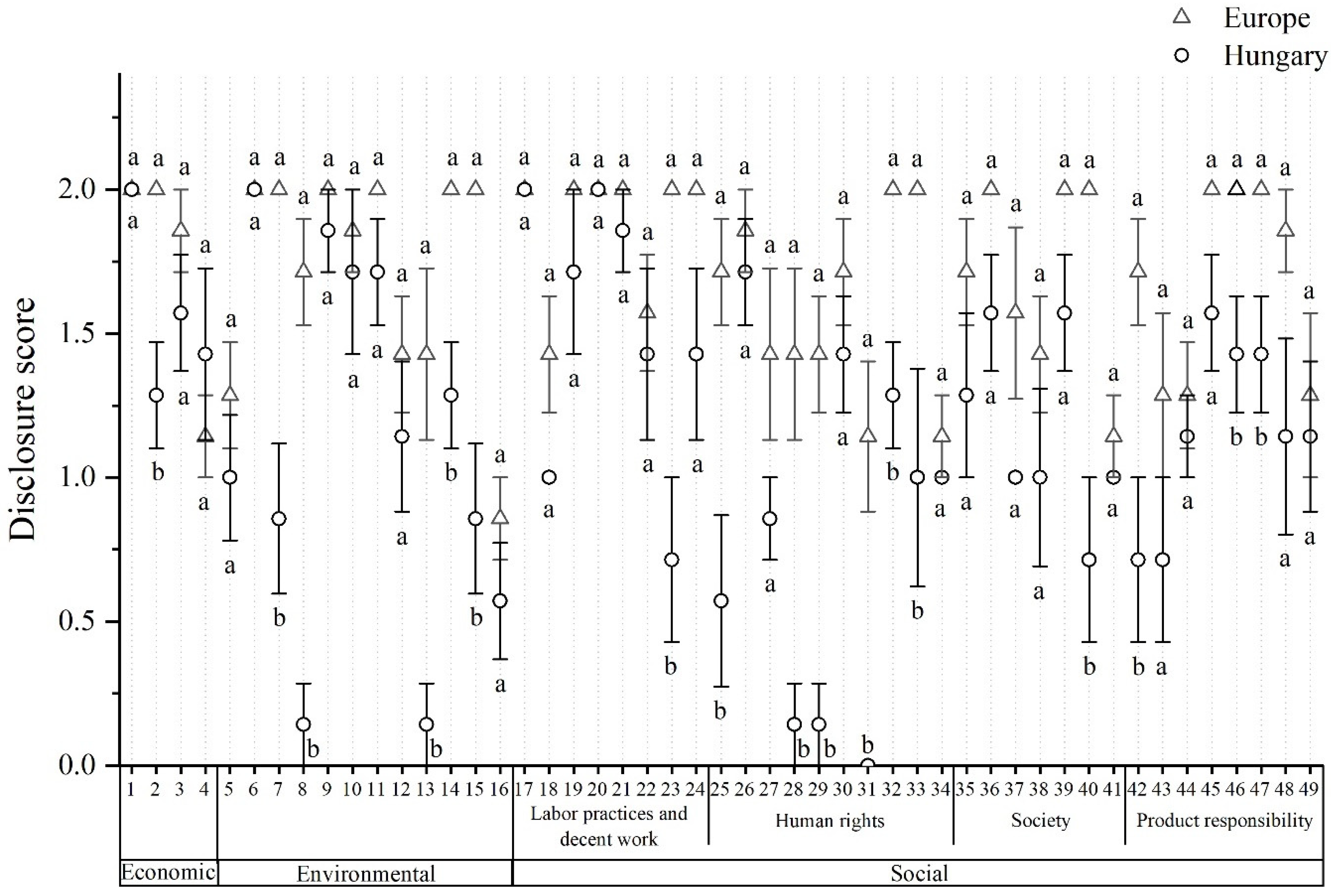

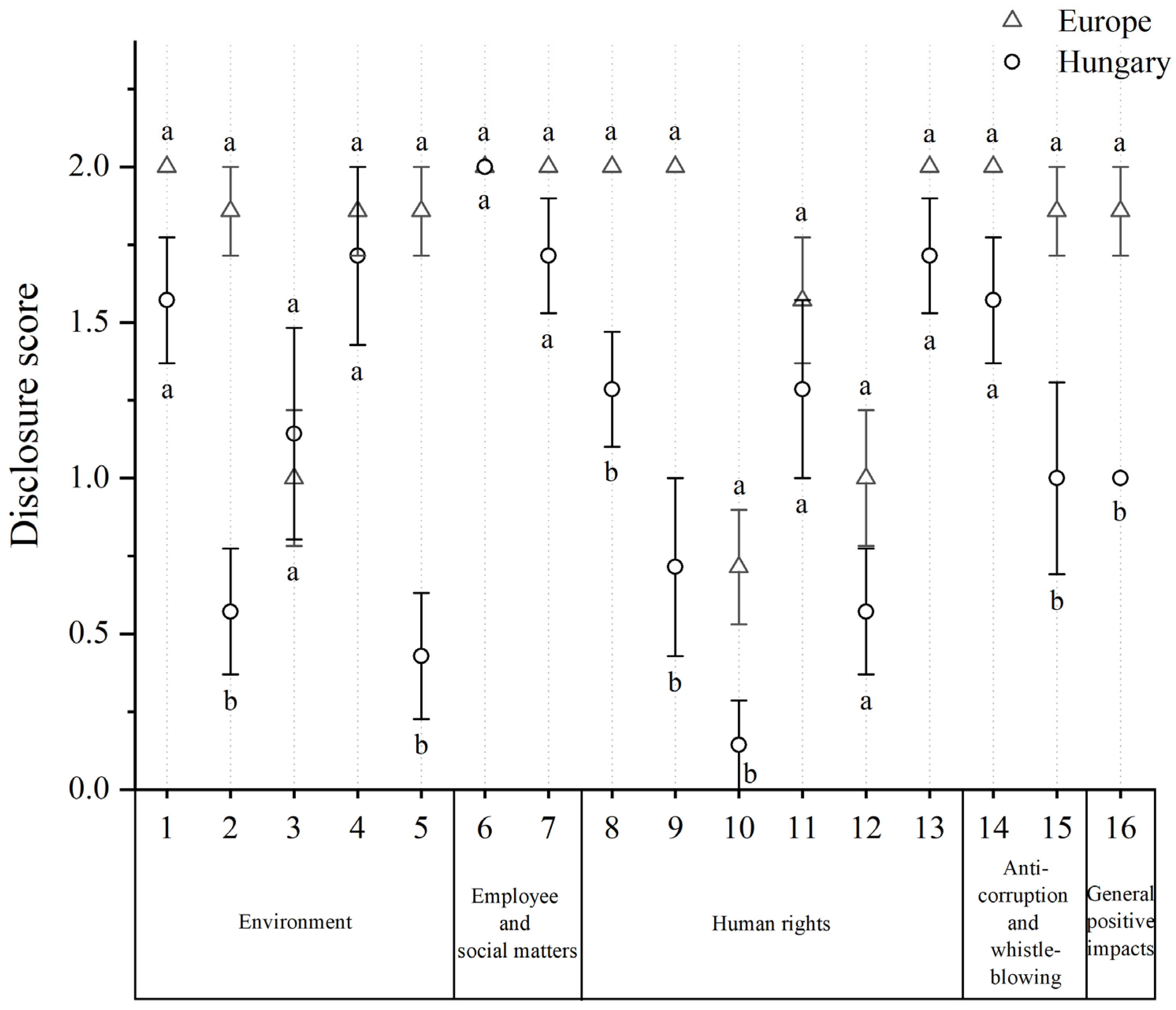

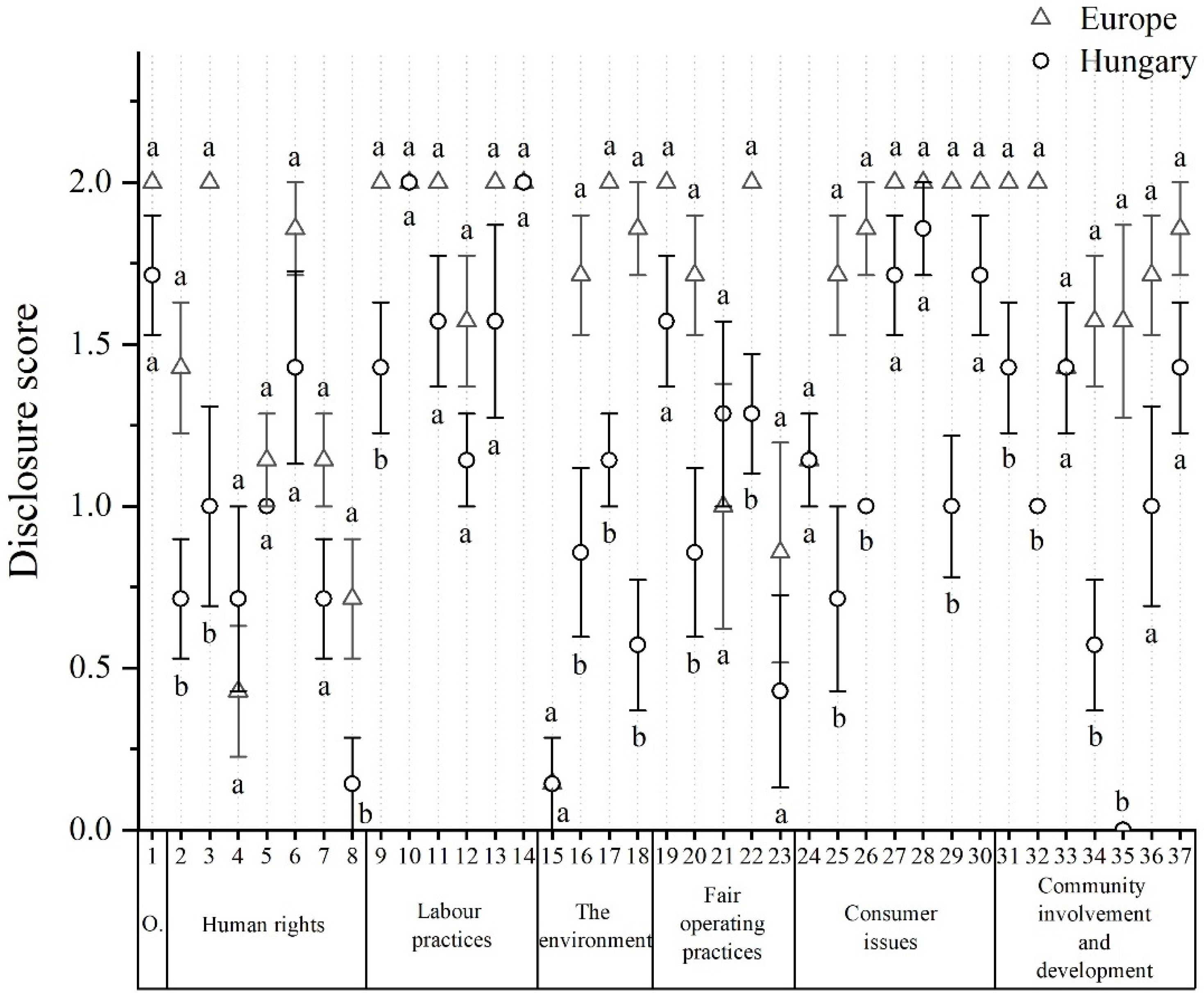

3.2. Compliance with the Aspects of Guidelines

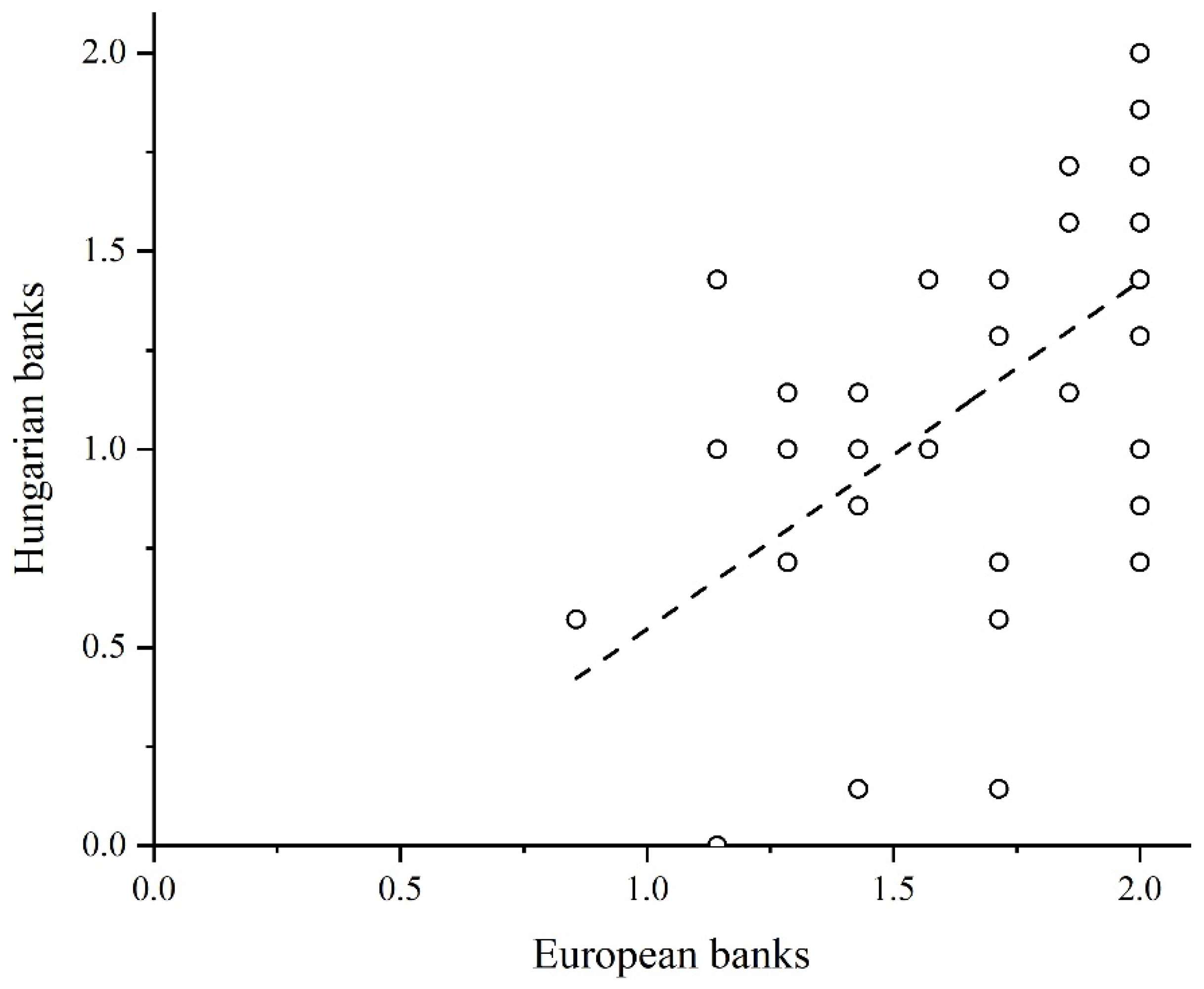

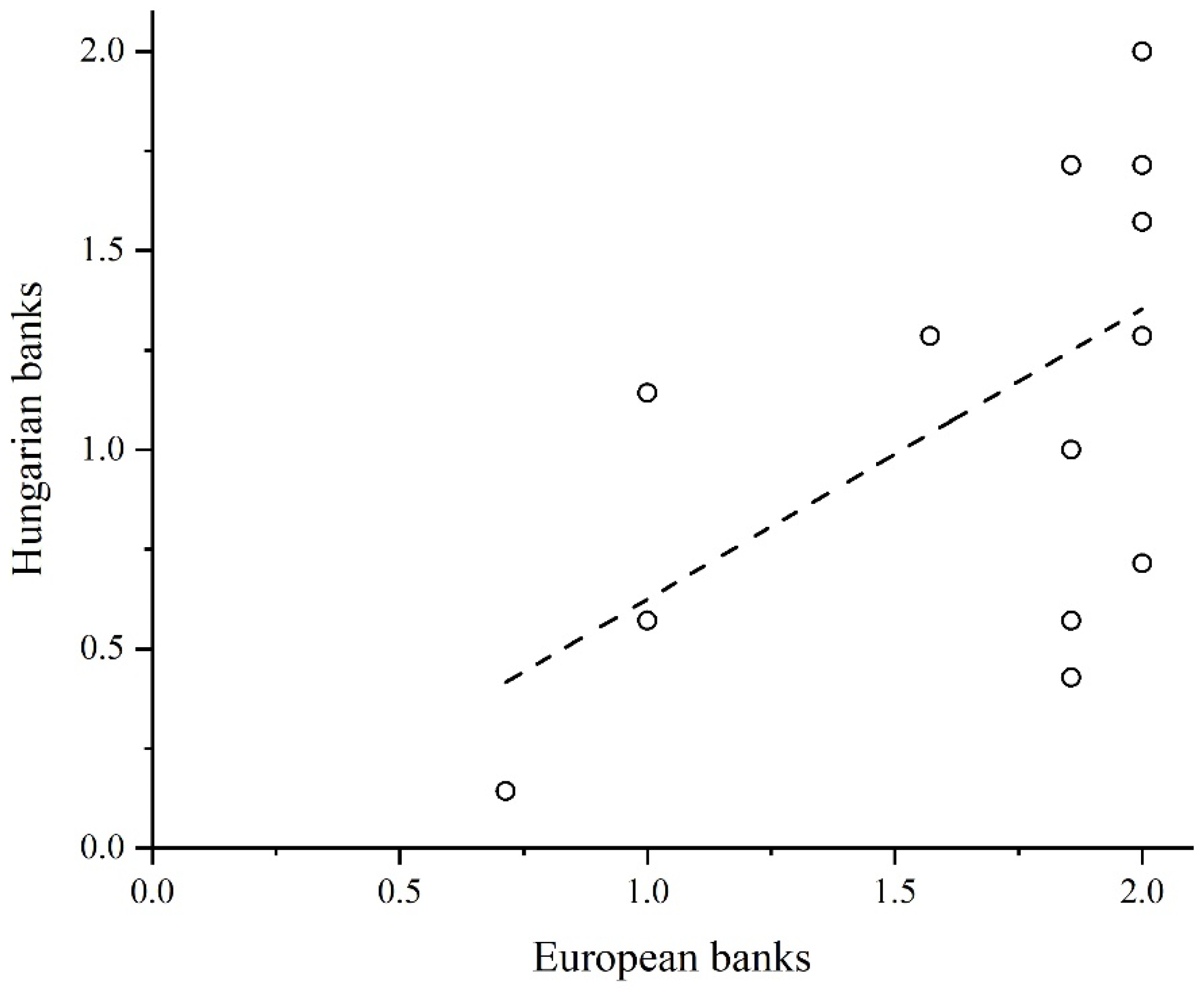

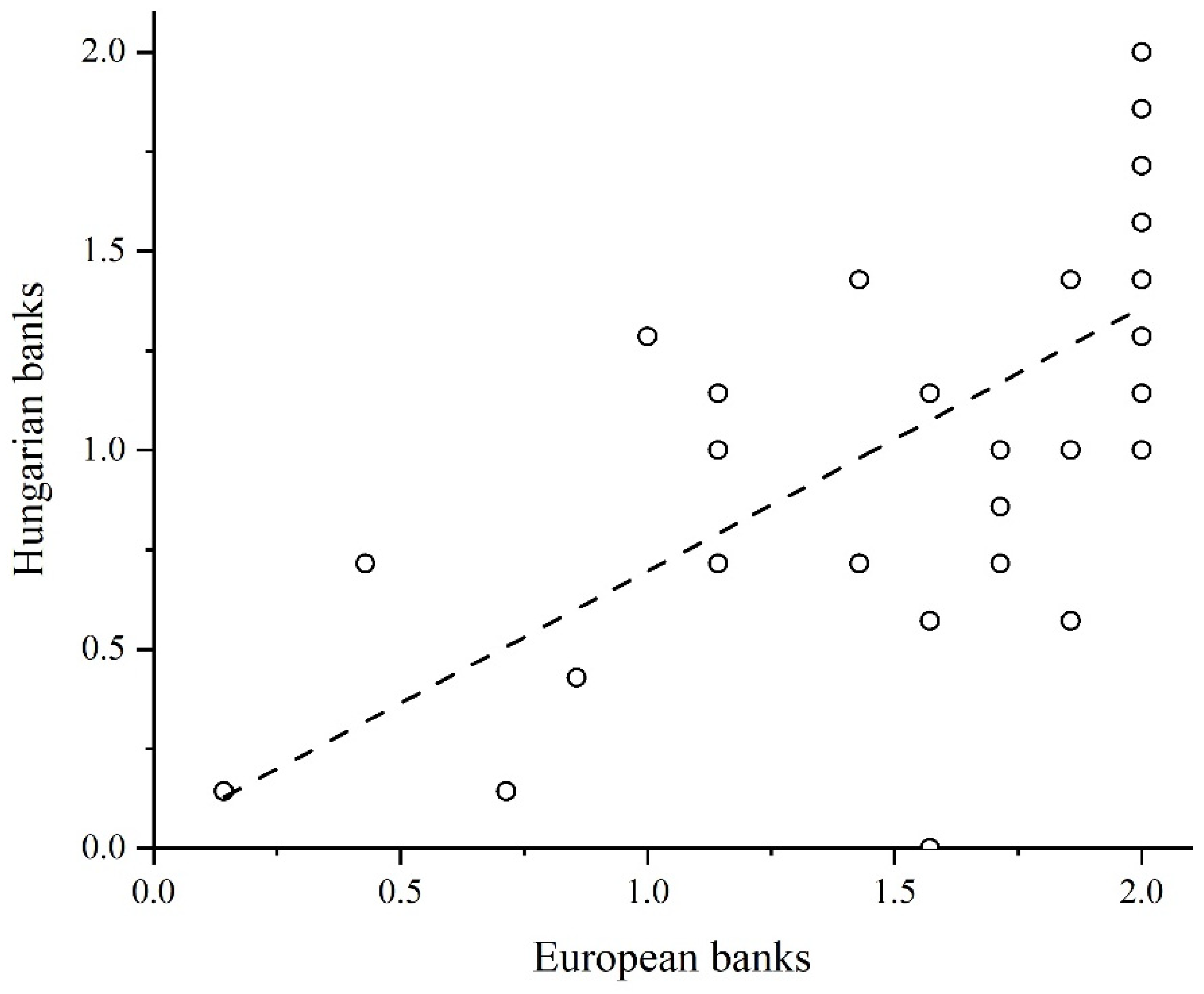

3.3. Correlation in Compliance between the Bank Groups

4. Materials and Methods

4.1. Data Collection

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| GRI | ACT | ISO | |

|---|---|---|---|

| 1 | Economic performance | Climate change | Organizational governance |

| 2 | Market presence | Use of natural resources | Due diligence |

| 3 | Indirect economic impact | Polluting discharges | Human rights risk situations |

| 4 | Procurement practices | Waste | Avoidance of complicity |

| 5 | Materials | Biodiversity and ecosystem conservation | Resolving grievances |

| 6 | Energy | Employees and workforce | Discrimination and vulnerable groups |

| 7 | Water | Social matters | Civil and political rights |

| 8 | Biodiversity | General human rights reporting criteria | Economic, social, and cultural rights |

| 9 | Emissions | Human rights in supply chains | Fundamental principles and rights at work |

| 10 | Effluent and waste | High risk areas for civil and political rights | Employment and employment relationships |

| 11 | Products and services | Impacts on indigenous and local communities | Conditions of work and social protection |

| 12 | Compliance | Conflict resources | Social dialogue |

| 13 | Transport | Data protection | Health and safety at work |

| 14 | Overall | Anti-corruption | Human development and training in the workplace |

| 15 | Supplier environmental assessment | Whistleblowing channels | Prevention of pollution |

| 16 | Environmental grievance mechanisms | General and sectorial positive impacts by products/sources of opportunity | Sustainable resource use |

| 17 | Employment | Climate change mitigation and adaptation | |

| 18 | Labor/management relations | Protection of the environment, biodiversity, and restoration of natural habitats | |

| 19 | Occupational health and safety | Anti-corruption | |

| 20 | Training and education | Responsible political involvement | |

| 21 | Diversity and equal opportunity | Fair competition | |

| 22 | Equal remuneration for women and men | Promoting social responsibility in the value chain | |

| 23 | Supplier assessment for labor practices | Respect for property rights | |

| 24 | Labor practices grievance mechanisms | Fair marketing, factual and unbiased information and fair contractual practices | |

| 25 | Investment | Protecting consumers’ health and safety | |

| 26 | Non-discrimination | Sustainable consumption | |

| 27 | Freedom of association and collective bargaining | Consumer service, support, and complaint and dispute resolution | |

| 28 | Child labor | Consumer data protection and privacy | |

| 29 | Forced and compulsory labor | Access to essential services | |

| 30 | Security practices | Education and awareness | |

| 31 | Indigenous rights | Community involvement | |

| 32 | Assessment | Education and culture | |

| 33 | Supplier human rights assessment | Employment creation and skills development | |

| 34 | Human rights grievance mechanisms | Technology development and access | |

| 35 | Local communities | Wealth and income creation | |

| 36 | Anti-corruption | Health | |

| 37 | Public policy | Social investment | |

| 38 | Anti-competitive behavior | ||

| 39 | Compliance | ||

| 40 | Supplier assessment for impacts on society | ||

| 41 | Grievance mechanisms for impacts on society | ||

| 42 | Customer health and safety | ||

| 43 | Product and service labeling | ||

| 44 | Marketing communications | ||

| 45 | Customer privacy | ||

| 46 | Compliance | ||

| 47 | Product portfolio | ||

| 48 | Audit | ||

| 49 | Active ownership |

4.2. Statistical Analysis

5. Conclusions and Policy Implications

Limitations and Further Research Directions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Agoraki, Maria-Eleni K., Georgios P. Kouretas, and Francisco Nadal De Simone. 2023. The performance of the euro area banking system: The pandemic in perspective. Review of Quantitative Finance and Accounting. [Google Scholar] [CrossRef]

- Ahmad, Hadiqa, Muhammad Yaqub, and Seung Hwan Lee. 2023. Environmental-, social-, and governance-related factors for business investment and sustainability: A scientometric review of global trends. Environment, Development and Sustainability 26: 2965–87. [Google Scholar] [CrossRef] [PubMed]

- Al Amosh, Hamzeh, and Saleh F. A. Khatib. 2023. ESG performance in the time of COVID-19 pandemic: Cross-country evidence. Environmental Science and Pollution Research 30: 39978–93. [Google Scholar] [CrossRef]

- Alliance for Corporate Transparency. 2019. The Alliance for Corporate Transparency Research Report 2019: An Analysis of the Sustainability Reports of 1000 Companies Pursuant to the EU Non-Financial Reporting Directive. Available online: https://www.sustentia.com/wp-content/uploads/2020/07/2019-Research-Report-Alliance-for-Corporate-Transparency_compressed.pdf (accessed on 1 June 2023).

- Ananzeh, Husam, Mohannad Obeid Al Shbail, Hamzeh Al Amosh, Saleh F. A. Khatib, and Shadi Habis Abualoush. 2023. Political connection, ownership concentration, and corporate social responsibility disclosure quality (CSRD): Empirical evidence from Jordan. International Journal of Disclosure and Governance 20: 83–98. [Google Scholar] [CrossRef]

- Andrieș, Alin Marius, and Nicu Sprincean. 2023. ESG performance and banks’ funding costs. Finance Research Letters 54: 103811. [Google Scholar] [CrossRef]

- Aureli, Selena. 2017. A comparison of content analysis usage and text mining in CSR corporate disclosure. The International Journal of Digital Accounting Research 17: 1–32. [Google Scholar] [CrossRef]

- Azmi, Wajahat, M. Kabir Hassan, Reza Houston, and Mohammad Sydul Karim. 2021. ESG activities and banking performance: International evidence from emerging economies. Journal of International Financial Markets, Institutions and Money 70: 101277. [Google Scholar] [CrossRef]

- Barclays plc. 2022. Barclays PLC Annual Report 2021. Available online: https://home.barclays/content/dam/home-barclays/documents/investor-relations/reports-and-events/annual-reports/2021/Barclays-PLC-Annual-Report-2021.pdf (accessed on 28 June 2023).

- Beck, A. Cornelia, David Campbell, and Philip J. Shrives. 2021. Content analysis in environmental reporting research: Enrichment and rehearsal of the method in a British–German context. The British Accounting Review 42: 207–22. [Google Scholar] [CrossRef]

- Boros, Anita, Csaba Lentner, Vitéz Nagy, and Dávid Tőzsér. 2023. Perspectives by green financial instruments—A case study in the Hungarian banking sector during COVID-19. Banks and Bank Systems 18: 116–26. [Google Scholar] [CrossRef]

- Borowski, Piotr F. 2022. Mitigating climate change and the development of green energy versus a return to fossil fuels due to the energy crisis in 2022. Energy 15: 9289. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Nga Nguyen, Vu Quang Trinh, and Thanh Vu. 2023. Market reaction to the Russian Ukrainian war: A global analysis of the banking industry. Review of Accounting and Finance 22: 123–53. [Google Scholar] [CrossRef]

- Broadstock, David C., Kalok Chan, Louis T. W. Cheng, and Xioawei Wang. 2021. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance Research Letters 38: 101716. [Google Scholar] [CrossRef] [PubMed]

- Bruno, Michelangelo, and Valentina Lagasio. 2021. An overview of the European policies on ESG in the banking sector. Sustainability 13: 12641. [Google Scholar] [CrossRef]

- Buallay, Amina. 2019. Is sustainability reporting (ESG) associated with performance? Evidence from the European banking sector. Management of Environmental Quality 30: 98–115. [Google Scholar] [CrossRef]

- Cardillo, Giovanni, Ennio Bendinelli, and Giuseppe Torluccio. 2023. COVID-19, ESG investing, and the resilience of more sustainable stocks: Evidence from European firms. Business Strategy and the Environment 32: 602–23. [Google Scholar] [CrossRef]

- Carnevale, Concetta, and Maria Mazzuca. 2014. Sustainability report and bank valuation: Evidence from European stock markets. Business Ethics 23: 69–90. [Google Scholar] [CrossRef]

- Carnini Pulino, Silvia, Mirella Ciaburri, Barbara Sveva Magnanelli, and Luigi Nasta. 2022. Does ESG disclosure influence firm performance? Sustainability 14: 7595. [Google Scholar] [CrossRef]

- Chauvey, Jean-Noël, Sophie Giordano-Spring, Charles H. Cho, and Dennis M. Patten. 2015. The normativity and legitimacy of CSR disclosure: Evidence from France. Journal of Business Ethics 130: 789–803. [Google Scholar] [CrossRef]

- Chiaramonte, Laura, Alberto Dreassi, Claudia Girardone, and Stefano Piserà. 2022. Do ESG strategies enhance bank stability during financial turmoil? Evidence from Europe. The European Journal of Finance 28: 1173–211. [Google Scholar] [CrossRef]

- CIB Bank Zrt. 2022. A CIB Csoport 2021. évi Üzleti és vezetőségi jelentése. Available online: https://www.cib.hu/document/documents/CIB/kommunikacio/evesjelentesek/IFRS_2021_CIB-Group__HU-220325.pdf (accessed on 28 June 2023).

- Citigroup Inc. 2022. 2021 Environmental, Social & Governance Report. Available online: https://www.citigroup.com/rcs/citigpa/akpublic/storage/public/Global-ESG-Report-2021.pdf (accessed on 28 June 2023).

- Connelly, Brian L., S. Trevis Certo, R. Duane Ireland, and Christopher R. Reutzel. 2011. Signaling theory: A review and assessment. Journal of Management 37: 39–67. [Google Scholar] [CrossRef]

- Cosma, Simona, Andrea Venturelli, Paola Schwizer, and Vittorio Boscia. 2020. Sustainable development and European banks: A non-financial disclosure analysis. Sustainability 12: 6146. [Google Scholar] [CrossRef]

- CSRD. 2022. Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 Amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC, and Directive 2013/34/EU, as Regards Corporate Sustainability Reporting. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32022L2464 (accessed on 27 June 2023).

- Darnall, Nicole, Hyunjung Ji, Kazuyuki Iwata, and Toshi H. Arimura. 2022. Do ESG reporting guidelines and verifications enhance firms’ information disclosure? Corporate Social Responsibility and Environmental Management 29: 1214–30. [Google Scholar] [CrossRef]

- Deegan, Craig Michael. 2019. Legitimacy theory: Despite its enduring popularity and contribution, time is right for a necessary makeover. Accounting, Auditing & Accountability Journal 32: 2307–29. [Google Scholar] [CrossRef]

- Delgado-Ceballos, Javier, Natalia Ortiz-De-Mandojana, Raquel Antolín-López, and Ivan Montiel. 2023. Connecting the Sustainable Development Goals to firm-level sustainability and ESG factors: The need for double materiality. BRQ Business Research Quarterly 26: 2–10. [Google Scholar] [CrossRef]

- Desalegn, Goshu, Mária Fekete-Farkas, and Anita Tangl. 2022. The effect of monetary policy and private investment on green finance: Evidence from Hungary. Journal of Risk and Financial Management 15: 117. [Google Scholar] [CrossRef]

- Deutsche Bank AG. 2022. Non-Financial Report 2021. Available online: https://investor-relations.db.com/files/documents/annual-reports/2022/Non-Financial_Report_2021.pdf (accessed on 28 June 2023).

- Di Tommaso, Caterina, and John Thornton. 2020. ESG scores effect bank risk taking and value? Evidence from European banks. Corporate Social Responsibility and Environmental Management 27: 2286–98. [Google Scholar] [CrossRef]

- Dinh, Tami, Anna Husmann, and Gaia Melloni. 2023. Corporate sustainability reporting in Europe: A scoping review. Accounting in Europe 20: 1–29. [Google Scholar] [CrossRef]

- Doğan, Mesut, and Mustafa Kevser. 2021. Relationship between sustainability report, financial performance, and ownership structure: Research on the Turkish banking sector. Istanbul Business Research 50: 77–102. [Google Scholar] [CrossRef]

- Dudás, Fanni, and Helena Naffa. 2021. Do ESG metrics reflect crisis resilience of equities during the COVID-19 pandemic? Economy and Finance 8: 371–88. [Google Scholar] [CrossRef]

- Ersoy, Ersan, Beata Swiecka, Simon Grima, Ercan Özen, and Inna Romanova. 2022. The impact of ESG scores on bank market value? Evidence from the U.S. banking industry. Sustainability 14: 9527. [Google Scholar] [CrossRef]

- European Financial Reporting Advisory Group (EFRAG). 2021. Appendix 4.6: Stream A6 Assessment Report. Current Non-Financial Reporting Formats and Practices. Available online: https://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FSiteAssets%2FEFRAG%2520PTF-NFRS_A6_FINAL.pdf (accessed on 12 June 2023).

- Ferreira Quilice, Thiago, Luciana Oranges Cezarino, Marlon Fernandes Rodriguez Alves, Lara Bartocci Liboni, and Adriana Christina Ferreira Caldana. 2018. Positive and negative aspects of GRI reporting as perceived by Brazilian organizations. Environmental Quality Management 27: 19–30. [Google Scholar] [CrossRef]

- Freeman, R. Edward, Sergiy D. Dmytriyev, and Robert A. Phillips. 2021. Stakeholder Theory and the Resource-Based View of the Firm. Journal of Management 47: 1757–70. [Google Scholar] [CrossRef]

- Friedrich, Tim Jan, Patrick Velte, and Inge Wulf. 2023. Corporate climate reporting of European banks: Are these institutions compliant with climate issues? Businsess Strategy and the Environment 32: 2817–34. [Google Scholar] [CrossRef]

- Fundamenta Lakáskassza Lakás-takarékpénztár Zrt. 2022. Fenntarthatósági jelentés 2022. Available online: https://fundamenta.hu/documents/fundamenta-zold-jelentes-2021/ (accessed on 28 June 2023).

- Gerged, Ali Meftah, Rami Salem, and Eshani Beddewela. 2023. How does transparency into global sustainability initiatives influence firm value? Insights from Anglo-American countries. Business Strategy and the Environment 32: 4519–47. [Google Scholar] [CrossRef]

- Global Reporting Initiative. 2013. GRI G4 Financial Services Sector Disclosures. Available online: https://www.globalreporting.org/search/?query=Financial+services (accessed on 1 June 2023).

- Guthrie, James, and Indra Abeysekera. 2006. Content analysis of social, environmental reporting: What is new? Journal of Human Resource Costing & Accounting 10: 114–26. [Google Scholar] [CrossRef]

- Gyura, Gábor. 2020. ESG and bank regulation: Moving with the times. Economy and Finance 7: 366–85. [Google Scholar] [CrossRef]

- Habib, Ahmed Mohamed. 2023. Do business strategies and environmental, social, and governance (ESG) performance mitigate the likelihood of financial distress? A multiple mediation model. Heliyon 9: e17847. [Google Scholar] [CrossRef] [PubMed]

- Hassan, Abeer, Ahmed A. Elamer, Suman Lodh, Lee Roberts, and Monomita Nandy. 2021. The future of non-financial businesses reporting: Learning from the Covid-19 pandemic. Corporate Social Responsibility and Environmental Management 28: 1231–40. [Google Scholar] [CrossRef]

- Helfaya, Akrum, and Mark Whittington. 2019. Does designing environmental sustainability disclosure quality measures make a difference? Business Strategy and the Environment 28: 525–41. [Google Scholar] [CrossRef]

- HSBC Holdings plc. 2022. HSBC Holdings plc Annual Report and Accounts 2021. Available online: https://www.hsbc.com/-/files/hsbc/investors/hsbc-results/2021/annual/pdfs/hsbc-holdings-plc/220222-annual-report-and-accounts-2021.pdf?download=1 (accessed on 28 June 2023).

- IBM Corp. 2021. IBM SPSS Statistics for Windows, Version 28.0. Armonk: IBM Corp. [Google Scholar]

- International Standard (ISO). 2010. ISO 26000:2010. Guidance on Social Responsibility. Available online: https://www.iso.org/iso-26000-social-responsibility.html (accessed on 1 June 2023).

- Intesa Sanpaolo S.p.A. 2022. 2021 Consolidated Non-financial Statement. Available online: https://group.intesasanpaolo.com/content/dam/portalgroup/repository-documenti/sostenibilt%C3%A0/dcnf-2021/eng/DCNF_2021_EN.pdf (accessed on 28 June 2023).

- Jayarathna, Chamari, Duzgun Agdas, Les Dawes, and Marc Miska. 2022. Exploring sector-specific sustainability indicators: A content analysis of sustainability reports in the logistics sector. European Business Review 34: 321–43. [Google Scholar] [CrossRef]

- K&H Bank Zrt. 2022. K&H Csoport fenntarthatósági jelentés 2021. Available online: https://www.kh.hu/documents/20184/490492/K%26H+Csoport+fenntarthat%C3%B3s%C3%A1gi+jelent%C3%A9s+2021.pdf/60598a8d-3bd5-c611-4a5c-8e6a8f1dc0fa?t=1650548503079 (accessed on 28 June 2023).

- Khan, Habib Zaman, Sudipta Bose, Abu Taher Mollik, and Harun Harun. 2021. “Green washing” or “authentic effort”? An empirical investigation of the quality of sustainability reporting by banks. Accounting, Auditing & Accountability Journal 34: 338–69. [Google Scholar] [CrossRef]

- Leszczynska, Agnieszka. 2012. Towards shareholders’ value: An analysis of sustainability reports. Industrial Management & Data Systems 112: 911–28. [Google Scholar] [CrossRef]

- Licandro, Oscar Daniel, Adán Guillermo Ramírez García, Lisandro José Alvarado-Peña, Luis Alfredo Vega Osuna, and Patricia Correa. 2019. Implementation of the ISO 26000 guidelines on active participation and community development. Social Sciences 8: 263. [Google Scholar] [CrossRef]

- Li, Zengfu, Liuhua Feng, Zheng Pan, and Hafiz M. Sohail. 2022. ESG performance and stock prices: Evidence from the COVID-19 outbreak in China. Humanities and Social Sciences Communications 9: 242. [Google Scholar] [CrossRef]

- Loewen, Bradley. 2022. Coal, green growth and crises: Exploring three European Union policy responses to regional energy transitions. Energy Research & Social Science 93: 102849. [Google Scholar] [CrossRef]

- Lopez de Silanes, Florencio, Joseph A. McCahery, and Paul C. Pudschedl. 2019. ESG Performance and Disclosure: A Cross-Country Analysis. Singapore Journal of Legal Studies 2020: 217–41. [Google Scholar] [CrossRef]

- Lloyds Banking Group plc. 2022. Lloyds Banking Group ESG Report 2021. Available online: https://www.lloydsbankinggroup.com/assets/pdfs/who-we-are/responsible-business/downloads/2021-reporting/lbg-esg-report-2021-interactive-final.pdf (accessed on 28 June 2023).

- Magyar Fejlesztési Bank Zrt. 2022. Fenntarthatósági jelentés 2021. Available online: https://www.mfb.hu/backend/documents/MFB_fenntarthatosagi_jelentes_2021_0102.pdf (accessed on 28 June 2023).

- Makarenko, Inna, and Serhiy Makarenko. 2023. Multi-level benchmark system for sustainability reporting: EU experience for Ukraine. Accounting and Financial Control 4: 41–48. [Google Scholar] [CrossRef]

- Masud, Md. Abdul Kaium, Mohammad Sharif Hossain, and Jong Dae Kim. 2018. Is green regulation effective or a failure: Comparative analysis between Bangladesh Bank (BB) Green Guidelines and Global Reporting Initiative Guidelines. Sustainability 10: 1267. [Google Scholar] [CrossRef]

- Menicucci, Elisa, and Guido Paolucci. 2022. ESG dimensions and bank performance: An empirical investigation in Italy. Corporate Governance 23: 563–86. [Google Scholar] [CrossRef]

- Michelon, Giovanna, Silvia Pilonato, and Federica Ricceri. 2015. CSR reporting practices and the quality of disclosure: An empirical analysis. Critical Perspectives on Accounting 33: 59–78. [Google Scholar] [CrossRef]

- Miklaszewska, Ewa, Krzysztof Kil, and Marcin Idzik. 2021. How the COVID-19 Pandemic Affects Bank Risks and Returns: Evidence from EU Members in Central, Eastern, and Northern Europe. Risks 9: 180. [Google Scholar] [CrossRef]

- Mio, Chiara, and Andrea Venturelli. 2013. Non-financial information about sustainable development and environmental policy in the annual reports of listed companies: Evidence from Italy and the UK. Corporate Social Responsibility and Environmental Management 20: 340–58. [Google Scholar] [CrossRef]

- MKB Bank Nyrt. 2022. Fenntarthatósági jelentés 2021. Available online: https://www.mbhbank.hu/sw/static/file/mkb_esg_jelentes_20221116_APPROVED.pdf (accessed on 28 June 2023).

- NFRD. 2014. Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32014L0095 (accessed on 27 June 2023).

- Nieto, María J., and Chryssa Papathanassiou. 2023. Financing the orderly transition to a low carbon economy in the EU: The regulatory framework for the banking channel. Journal of Banking Regulation. in press. [Google Scholar] [CrossRef]

- Nizam, Esma, Adam Ng, Ginanjar Dewandaru, Ruslan Nagayev, and Malik Abdulrahman Nkoba. 2019. The impact of social and environmental sustainability on financial performance: A global analysis of the banking sector. Journal of Multinational Financial Management 49: 35–53. [Google Scholar] [CrossRef]

- Nosratabadi, Saeed, Gergo Pinter, Amir Mosavi, and Sandor Semperger. 2020. Sustainable banking; Evaluation of the European business models. Sustainability 12: 2314. [Google Scholar] [CrossRef]

- Opferkuch, Katelin, Sandra Caeiro, Roberta Salomone, and Tomás B. Ramos. 2022. Circular economy disclosure in corporate sustainability reports: The case of European companies in sustainability rankings. Sustainable Production and Consumption 32: 436–56. [Google Scholar] [CrossRef]

- Origin(Pro), Version 2018. 2018. Origin(Pro), Version 2018. Northampton: OriginLab Corporation. [Google Scholar]

- OTP Bank Nyrt. 2022. Fenntarthatósági jelentés 2021. Available online: https://www.otpbank.hu/static/portal/sw/file/OTP_Csoport_Fenntarthatosagi_jelentes_2021.pdf (accessed on 28 June 2023).

- Primec, Andreja, and Jernej Belak. 2022. Sustainable CSR: Legal and managerial demands of the new EU legislation (CSRD) for the future corporate governance practices. Sustainability 14: 16648. [Google Scholar] [CrossRef]

- Refinitiv. 2022. Environmental, Social and Governance Scores from Refinitiv. Available online: https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/refinitiv-esg-scores-methodology.pdf (accessed on 26 June 2023).

- Rezaee, Zabihollah, Saeid Homayoun, Ehsan Poursoleyman, and Nick J. Rezaee. 2023. Comparative analysis of environmental, social, and governance disclosures. Global Finance Journal 55: 100804. [Google Scholar] [CrossRef]

- Roca, Laurence Clément, and Cory Searcy. 2012. An analysis of indicators disclosed in corporate sustainability reports. Journal of Cleaner Production 20: 103–18. [Google Scholar] [CrossRef]

- Şahin, Zeynep, Fikret Çankaya, and Züleyha Yilmaz Soğuksu. 2016. Content analysis of sustainability reports: A practice in Turkey. Paper presented at 7th European Business Research Conference, Rome, Italy, December 15–16. [Google Scholar]

- Santander Bank, N.A. 2022. ESG Report 2021. Available online: https://www.santander.com/content/dam/santander-com/en/contenido-paginas/nuestro-compromiso/reports/doc-informe-BR-polonia-2021.pdf (accessed on 28 June 2023).

- SFDR. 2020. Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the Establishment of a Framework to Facilitate Sustainable Investment, and Amending Regulation (EU) 2019/2088. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32020R0852 (accessed on 27 June 2023).

- Smit, Anet M., and Johan van Zyl. 2016. Investigating the extent of sustainability reporting in the banking industry. Banks and Bank Systems 11: 71–81. [Google Scholar] [CrossRef]

- Söderholm, Patrik. 2020. The green economy transition: The challenges of technological change for sustainability. Sustainable Earth Reviews 3: 6. [Google Scholar] [CrossRef]

- Takarék Jelzálogbank Nyrt. 2022. Fenntarthatósági jelentés 2021. Available online: https://bet.hu/newkibdata/128775836/TJB_ESG_jelentes_2021_pub.pdf (accessed on 28 June 2023).

- Tamásné Vőneki, Zsuzsanna, and Gabriella Lamanda. 2020. Content analysis of bank disclosures related to ESG risks. Economy and Finance 7: 412–24. [Google Scholar] [CrossRef]

- Thomson Reuters. 2017. Thomson Reuters ESG Scores. Available online: https://www.esade.edu/itemsweb/biblioteca/bbdd/inbbdd/archivos/Thomson_Reuters_ESG_Scores.pdf (accessed on 26 June 2023).

- Wen, Hui, Ken C. Ho, Jijun Gao, and Li Yu. 2022. The fundamental effects of ESG disclosure quality in boosting the growth of ESG investing. Journal of International Financial Markets, Institutions and Money 81: 101655. [Google Scholar] [CrossRef]

- Yin, Xiao-Na, Jing-Ping Li, and Chi-Wei Su. 2023. How does ESG performance affect stock returns? Empirical evidence from listed companies in China. Heliyon 9: e16320. [Google Scholar] [CrossRef]

- Zetzsche, Dirk A., and Linn Anker-Sørensen. 2022. Regulating sustainable finance in the dark. European Business Organization Law Review 23: 47–85. [Google Scholar] [CrossRef]

| 2 | 1 | 0 | |

|---|---|---|---|

| Policies | Policy description specifies key issues and objectives (a separate sub-chapter is dedicated to the aspect with pervasive cross-references to affected areas or representation is integrated into several relevant sections of the document) | Policy is described or referenced (relevancy of the aspect is mentioned/highlighted without in-depth specification) | No information provided (no mention of the aspect throughout the document) |

| Risks | Description of specific risks | Vague risk identification | No risk identification |

| Outcomes | Outcomes in terms of meeting policy targets | Description provided | No description |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tőzsér, D.; Lakner, Z.; Sudibyo, N.A.; Boros, A. Disclosure Compliance with Different ESG Reporting Guidelines: The Sustainability Ranking of Selected European and Hungarian Banks in the Socio-Economic Crisis Period. Adm. Sci. 2024, 14, 58. https://doi.org/10.3390/admsci14030058

Tőzsér D, Lakner Z, Sudibyo NA, Boros A. Disclosure Compliance with Different ESG Reporting Guidelines: The Sustainability Ranking of Selected European and Hungarian Banks in the Socio-Economic Crisis Period. Administrative Sciences. 2024; 14(3):58. https://doi.org/10.3390/admsci14030058

Chicago/Turabian StyleTőzsér, Dávid, Zoltán Lakner, Novy Anggraini Sudibyo, and Anita Boros. 2024. "Disclosure Compliance with Different ESG Reporting Guidelines: The Sustainability Ranking of Selected European and Hungarian Banks in the Socio-Economic Crisis Period" Administrative Sciences 14, no. 3: 58. https://doi.org/10.3390/admsci14030058