Abstract

We analyze the effects of a prevailing low interest rates regime on investment decisions of insurance companies and on the risk/return profile of participating life insurance policies with different contractually guaranteed minimum annual return. Our analysis is based on German legislation and a stylized insurance company with two cohorts of insured persons having different minimal return guarantees. Our findings shed some light on the non-trivial interrelation between profit distribution, minimum guarantees, and resulting profitability for the different cohorts. Moreover, we investigate the complex role of the risk reserve that allows insurance companies to redistribute profits in time and, less obviously, also between the cohorts.

Similar content being viewed by others

Notes

In Germany this is regulated via the minimum funding ordinance (Mindestzuführungsverordnung), see http://www.gesetze-im-internet.de/mindzv/index.html.

Grosen and Jørgensen [10] state that “many insurers now face claims from distinct groups of liability holders distinguished by different guaranteed interest rates in their policies. This raises the problem of how to avoid inequitable treatment of different classes of policyholders within the same fund. Some companies [...] have tremendous concerns over the definition of a correct and fair distribution policy [...]”.

In practice, insurance companies earn additional money by the difference between true and best-estimate actuarial assumptions, i.e., in their assumptions on administrative costs or mortality. This income is, however, rather stable over time and is thus—for simplicity—neglected in this analysis. Instead, we concentrate on the financial risks.

In Germany, at least \(90\,\%\) of returns have to be distributed to the policyholders (compare the minimum funding ordinance “Mindestzuführungsverordnung”).

In Germany, the regulator tries to (at least) mitigate the unequal treatment by rules (3) and (4): If a high guarantee contract benefits by rules (3) or (4), it might not benefit fully from a high surplus in later years as part of a compensation for the other cotracts.

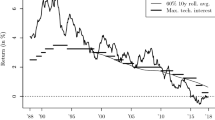

Historic daily data was obtained from Reuters (ticker names: DE10YT=RR, GREXP, and GDAXI).

Mortality tables are, for example, available from the German government agency Statistisches Bundesamt, see https://www.destatis.de.

Note that these also include hidden risk reserves that can be accumulated, for example, by exploiting accounting rules.

References

Bacinello A (2003) Fair pricing of a guarantee life insurance participating contract embedding surrender option. J Risk Insur 70(3):461–487

Barbarin J, Devolder P (2005) Risk measure and fair valuation of an investment guarantee in life insurance. Insur Math Econ 37:297–323

Bauer D, Kiesel R, Kling A, Ruß J (2005) Risk neutral valuation of participating life insurance contracts. Insur Math Econ 39(2):171–183

Bohnert A, Gatzert N (2012) Analyzing surplus appropriation schemes in participating life insurance from the insurer’s and the policyholder’s perspective. Insur Math Econ 50(2):64–78

Bryis E, de Varenne F (1997) On the risk of life insurance liabilities: debunking some common pitfalls. J Risk Insur 64(4):673–694

Døskeland T, Nordahl H (2008) Intergenerational effects of guaranteed pension contracts. In: The Geneva risk and insurance review, vol. 33

Goecke O (2013) Pension saving schemes with return smoothing mechanism. Insur Math Econ 53:678–689

Graf S, Kling A, Ruß J (2011) Risk analysis and valuation of life insurance contracts: combining actuarial and financial approaches. Insur Math Econ 49(10):115–125

Grosen J, Jørgensen P (2000) Fair valuation of life insurance liabilities: the impact of interest rate guarantees, surrender options and bonus policies. Insur Math Econ 26(1):37–57

Grosen J, Jørgensen P (2002) Life insurance liabilities at market value: an analysis of insolvency risk, bonus policy, and regulatory intervention rules in a barrier option framework. J Risk Insur 69(1):63–91

Jaquemod R (ed) (2005) Stochastisches Unternehmensmodell für deutsche Lebensversicherungen. VVW, Karlsruhe

Kling A, Ruß J (2004) Differenzierung der Überschüsse konventioneller Lebensversicherungsverträge mit unterschiedlichem Garantiezins: Betrug treuer Kunden oder finanzmathematische Notwendigkeit? Institut für Finanz-und Aktuarwissenschaften Ulm

Patel J, Read C (1996) Handbook of the normal distribution. In: Statistics: a series of textbooks and monographs, 2nd edn

Vasicek O (1977) An equilibrium characterization of the term structure. J Financ Econ 5(2):177–188

Acknowledgments

We want to thank Alexander Kling, Jochen Ruß, Ralf Werner, and the participants of the 2014 research seminar TU München/University Duisburg-Essen for fruitful discussions on the topic.

Author information

Authors and Affiliations

Corresponding author

Additional information

P. Hieber acknowledges funding by the German Association of Insurance Science (DVfVW).

Appendix: Optimization

Appendix: Optimization

At each time point \(t_{j-1}\), we choose an optimal investment strategy \(\varvec{\pi }_{t_{j-1}} = (\pi ^{(1)}_{t_{j-1}},\pi ^{(2)}_{t_{j-1}},\pi ^{(3)}_{t_{j-1}})\) such that the probability of the portfolio return \(m(t_{j}) := \pi ^{(1)}_{t_{j-1}} r_{t_{j}} + \pi ^{(2)}_{t_{j-1}} b_{t_{j}} + \pi ^{(3)}_{t_{j-1}} \mu _{t_{j}}\) being less than the portfolio guarantee \(g(t_{j-1})\) is minimized, i.e.,

Abbreviating

then \(m(t_{j})\) is normally distributed with mean \(\varvec{\pi }'_{t_{j-1}}\,\varvec{d}\) and variance \(\varvec{\pi }_{t_{j-1}}'\,(\varvec{\sigma }\varvec{\sigma }'\, .\, \Sigma )\,\varvec{\pi }_{t_{j-1}}\) (where . denotes point-wise matrix-multiplication and \('\) transpose). The portfolio guarantee \(g(t_j)\) is a constant. In the following, we write the covariance matrix as \(V:= \varvec{\sigma }\varvec{\sigma }'\, .\, \Sigma\).

If returns are normally distributed, the objective function can easily be evaluated if one recalls basic properties of the truncated normal distribution (see e.g., [13]), i.e.,

where \(\phi (\,\cdot \,)\), respectively \(\Phi (\,\cdot \,)\), denote the density, respectively distribution function, of the standard normal distribution.

Rights and permissions

About this article

Cite this article

Hieber, P., Korn, R. & Scherer, M. Analyzing the effect of low interest rates on the surplus participation of life insurance policies with different annual interest rate guarantees. Eur. Actuar. J. 5, 11–28 (2015). https://doi.org/10.1007/s13385-014-0102-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13385-014-0102-3