Abstract

During the U.S. subprime mortgage crisis, credit default swaps (CDS) played a pivotal role and became an influential booster. However, most studies only study the systemic risk of CDS in the interbank market and do not quantify how CDS speculation affects the systemic risk. Therefore, to study the impact of CDS speculation on the systemic risk, this paper constructs a multi-layered complex network, which includes bank-firm-CDS sellers to reproduce speculation in the CDS market. Then, the impact of different CDS speculation ratios and regulatory ratios on the banking systemic risk of a multi-layered complex network are investigated separately under different credit shocks. The results show that the systemic risk is positively correlated with the CDS speculation ratio, and that speculation adversely influences system stability, although it is profitable for some banks. Moreover, the effectiveness of the regulation is affected by the size of credit shocks, if credit shocks are large, the systemic risk is negatively related to regulatory ratios. Because the regulation system on CDS sellers limits the expansion of the CDS market, reduces the counterparty risk for banks, and makes the banking system more stable. Instead, if credit shocks are low, strict regulation has the potential to increase the systemic risk. The study provides a novel perspective on utilizing rational credit risk mitigation instruments to prevent systemic risks.

Similar content being viewed by others

Data Availability

The data that support the findings of this study are available from the corresponding author upon request.

References

Acharya, V. V., Pedersen, L. H., Philippon, T., & Richardson, M. (2017). Measuring systemic risk. The Review of Financial Studies, 30(1), 2–47.

Adrian, T., & Brunnermeier, M. K. (2016). CoVaR. The American Economic Review, 106(7), 1705.

Aldasoro, I., & Alves, I. (2018). Multiplex interbank networks and systemic importance: An application to European data. Journal of Financial Stability, 35, 17–37.

Allen, F., & Gale, D. (2000). Financial Contagion. Journal of Political Economy, 108(1), 1–33.

Al-Own, B., Minhat, M., & Gao, S. (2018). Stock options and credit default swaps in risk management. Journal of International Financial Markets, Institutions and Money, 53, 200–214.

Andreoli, A., Ballestra, L. V., & Pacelli, G. (2018). Pricing credit default swaps under multifactor reduced-form models: A differential quadrature approach. Computational Economics, 51, 379–406.

Augustin, P., Subrahmanyam, M. G., & Tang, D. Y. (2016). Credit Default Swaps: Past, Present, and Future. Annual Review of Financial Economics, 8, 175–196.

Bakoush, M., Gerding, E. H., & Wolfe, S. (2019). Margin requirements and systemic liquidity risk. Journal of International Financial Markets, Institutions and Money, 58, 78–95.

Bartram, S. M., Conrad, J., & Lee, J. (2022). Credit default swaps around the world. The Review of Financial Studies, 35(5), 2464–2524.

Bo, L., & Capponi, A. (2015). Counterparty risk for CDS: Default clustering effects. Journal of Banking & Finance, 52, 29–42.

Bomfim, A. N. (2022). Credit Default Swaps. Finance and Economics Discussion Series, 2022,023. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS.2022.023

Brunetti, C., Harris, J. H., Mankad, S., & Michailidis, G. (2019). Interconnectedness in the interbank market. Journal of Financial Economics, 133(2), 520–538.

Cao, J., & Wen, F. (2019). The impact of the cross-shareholding network on extreme price movements: Evidence from China. Journal of Risk, 22(2), 79–102.

Cao, J., Wen, F., Stanley, H. E., & Wang, X. (2021). Multilayer financial networks and systemic importance: Evidence from China. International Review of Financial Analysis, 78, 101882.

Cetina, J., Paddrik, M., & Rajan, S. (2018). Stressed to the core: Counterparty concentrations and systemic losses in CDS markets. Journal of Financial Stability, 35, 38–52.

Clemente, G. P., & Cornaro, A. (2022). A multilayer approach for systemic risk in the insurance sector. Chaos, Solitons & Fractals, 162, 112398.

Cont, R., & Minca, A. (2016). Credit default swaps and systemic risk. Annals of Operations Research, 247, 523–547.

Delli Gatti, D., Gallegati, M., Greenwald, B., Russo, A., & Stiglitz, J. E. (2010). The financial accelerator in an evolving credit network. Journal of Economic Dynamics and Control, 34(9), 1627–1650.

D’errico, M., Battiston, S., Peltonen, T., & Scheicher, M. (2018). How does risk flow in the credit default swap market? Journal of Financial Stability, 35, 53–74.

Du, W., Gadgil, S., Gordy, M. B., & Vega, C. (2019). Counterparty risk and counterparty choice in the credit default swap market. Available at SSRN 2845567.

Duffie, D. (2010). Is there a case for banning short speculation in sovereign bond markets? Financial Stability Review, 14, 55–59.

Frijns, B., & Zwinkels, R. C. (2020). Absence of speculation in the European sovereign debt markets. Journal of Economic Behavior & Organization, 169, 245–265.

Glasserman, P., & Young, H. P. (2015). How likely is contagion in financial networks? Journal of Banking & Finance, 50, 383–399.

Hao, Q., Shen, J. H., & Lee, C. C. (2023). Risk contagion of bank-firm loan network: evidence from China. Eurasian Business Review, 1–21.

Hasan, I., & Wu, D. (2015). How large banks use CDS to manage risks: bank-firm-level evidence. Available at SSRN 2617495.

Heath, A., Kelly, G., Manning, M., Markose, S., & Shaghaghi, A. R. (2016). CCPs and network stability in OTC derivatives markets. Journal of Financial Stability, 27, 217–233.

Heise, S., & Kühn, R. (2012). Derivatives and credit contagion in interconnected networks. The European Physical Journal B, 85, 1–19.

Huang, X., Zhou, H., & Zhu, H. (2009). A framework for assessing the systemic risk of major financial institutions. Journal of Banking & Finance, 33(11), 2036–2049.

Iori, G., Jafarey, S., & Padilla, F. G. (2006). Systemic risk on the interbank market. Journal of Economic Behavior & Organization, 61(4), 525–542.

Jiang, S., & Fan, H. (2021). Systemic risk in the interbank market with overlapping portfolios and cross-ownership of the subordinated debts. Physica a: Statistical Mechanics and Its Applications, 562, 125355.

Leventides, J., Loukaki, K., & Papavassiliou, V. G. (2019). Simulating financial contagion dynamics in random interbank networks. Journal of Economic Behavior & Organization, 158, 500–525.

Li, J. Y., & Tang, D. Y. (2016). The leverage externalities of credit default swaps. Journal of Financial Economics, 120(3), 491–513.

Liu, A., Paddrik, M., Yang, S. Y., & Zhang, X. (2020). Interbank contagion: An agent-based model approach to endogenously formed networks. Journal of Banking & Finance, 112, 105191.

Minton, B. A., Stulz, R., & Williamson, R. (2009). How much do banks use credit derivatives to hedge loans? Journal of Financial Services Research, 35, 1–31.

Nanumyan, V., Garas, A., & Schweitzer, F. (2015). The network of counterparty risk: Analyzing correlations in OTC derivatives. PLoS ONE, 10(9), e0136638.

Oehmke, M., & Zawadowski, A. (2017). The anatomy of the CDS market. The Review of Financial Studies, 30(1), 80–119.

Oehmke, M., & Zawadowski, A. (2015). Synthetic or real? The equilibrium effects of credit default swaps on bond markets. The Review of Financial Studies, 28(12), 3303–3337.

Osano, H. (2020). Credit default swaps and market information. Journal of Financial Markets, 48, 100498.

Raimbourg, P., & Salvadè, F. (2021). Rating announcements, CDS spread and volatility during the European sovereign crisis. Finance Research Letters, 40, 101663.

Riccetti, L. (2022a). Agent-based multi-layer network simulations for financial systemic risk measurement: A proposal for future developments. International Journal of Microsimulation, 15(2), 44–61.

Riccetti, L. (2022b). Systemic risk analysis and SIFI detection: Mechanisms and measurement. Journal of Risk Management in Financial Institutions, 15(3), 245–259.

Riccetti, L., Russo, A., & Gallegati, M. (2013). Leveraged network-based financial accelerator. Journal of Economic Dynamics and Control, 37(8), 1626–1640.

RPS Submitter, B. D. F., Henricot, D., & Piquard, T. (2022). Credit Default Swaps and Credit Risk Reallocation. Banque de France Working Paper No. 860, Available at SSRN, https://doi.org/10.2139/ssrn.4011975

Schuldenzucker, S., Seuken, S., & Battiston, S. (2020). Default ambiguity: Credit default swaps create new systemic risks in financial networks. Management Science, 66(5), 1981–1998.

Shan, C., Tang, D. Y., Yan, H., & Zhou, X. (2021). Credit default swaps and bank regulatory capital. Review of Finance, 25(1), 121–152.

Silva, T. C., da Silva Alexandre, M., & Tabak, B. M. (2018). Bank lending and systemic risk: A financial-real sector network approach with feedback. Journal of Financial Stability, 38, 98–118.

Sinka, P., & Zeitsch, P. J. (2022). Hedge effectiveness of the credit default swap indices: A spectral decomposition and network topology analysis. Computational Economics, 60(4), 1375–1412.

Taşkın, D., & Sarıyer, G. (2020). Use of derivatives, financial stability and performance in Turkish banking sector. Quantitative Finance and Economics, 4(2), 252–273.

Thornton, J., & Di Tommaso, C. (2018). Credit default swaps and regulatory capital relief: Evidence from European banks. Finance Research Letters, 26, 255–260.

Wang, X., Hou, S., & Shen, J. (2021a). Default clustering of the nonfinancial sector and systemic risk: Evidence from China. Economic Modelling, 96, 196–208.

Wang, H., Yuan, Y., Li, Y., & Wang, X. (2021b). Financial contagion and contagion channels in the forex market: A new approach via the dynamic mixture copula-extreme value theory. Economic Modelling, 94, 401–414.

Yang, H. X., Wang, W. X., Xie, Y. B., Lai, Y. C., & Wang, B. H. (2011). Transportation dynamics on networks of mobile agents. Physical Review E, 83(1), 016102.

Funding

This study was supported by the National Natural Science Foundation of China (71971054) and the Shanghai Natural Science Foundation of China (19ZR1402100).

Author information

Authors and Affiliations

Contributions

All authors contributed to the study conception and design. MT: Writing – original draft, conceptualization, methodology, calculation, and analysis. HF: Supervision, giving comments. All authors have read and agreed to the final manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix: Stability Test and Sensitivity Analysis

Appendix: Stability Test and Sensitivity Analysis

1.1 Robustness Test of the Reserve Requirement Ratio \(\chi\)

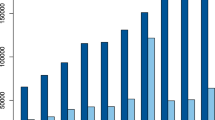

This paper constructed a multilayer network model with bank-firm-CDS sellers to study the impact of speculation and regulation on systemic risk in the CDS market, but further tests are needed for the robustness of the multilayer network model. With the development of the financial system, the reserve requirement has gradually evolved into an important monetary policy tool. Considering that the reserve requirement ratio affects the size of banks' credit, which in turn may affect systemic risk under credit shocks. Based on this, this paper varied the reserve requirement ratio (\(\chi = \left[ {0.15,0.25} \right]\)) while controlling other parameters constant and observed the number of defaults in the three networks, as shown in Table 3 and Fig. 10.

Number of defaults for three networks with different reserve requirement ratios \(\chi\)

We found that the number of defaults decreases as \(\chi\) increases in the same bank network. This is because the increase in the reserve requirement ratio affects the ability of banks to expand credit, thus reducing credit risk. Although the change in \(\chi\) leads to a change in the number of defaults in the network, the conclusion of the paper remains unchanged: speculation in the CDS market increases systemic risk; regulation of the CDS market reduces systemic risk. Therefore, the model results in this paper are robust to changes in the reserve requirement ratio.

1.2 Sensitivity Analysis of Margin Parameter

The amount of margin required from a CDS seller is related to the volatility of the CDS market price. The higher the market price volatility, the higher the margin required from the CDS seller. Therefore, it is necessary to investigate the sensitivity of the market price volatility parameter to the model results. This paper varied the CDS market price volatility (\(\sigma_{c} = \left[ {0.01,0.1} \right]\)) while controlling other parameters constant and observed the number of defaults in the banking system, as shown in Fig. 11.

In Fig. 11, the number of defaults in the system increases slightly as \(\sigma_{c}\) rises. The number of defaults is more sensitive to \(\sigma_{c}\) when \(\sigma_{c}\) is larger. But overall, the sensitivity of \(\sigma_{c}\) is low and has little effect on the simulation results. This indicates that the model in this paper has good stability.

Number of defaults under different CDS market price volatility \(\sigma_{c}\)

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Tang, M., Fan, H. Dynamic Multilayer Network for Systemic Risk and Bank Regulation Based on CDS. Comput Econ (2023). https://doi.org/10.1007/s10614-023-10508-x

Accepted:

Published:

DOI: https://doi.org/10.1007/s10614-023-10508-x