Abstract

This paper analyzes bargaining outcomes when agents do not have stationary time preferences (as represented by a constant discount factor) but are pressed by firm deadlines. We consider a dynamic model where traders with heterogeneous deadlines are matched randomly into pairs who then bargain about the division of a fixed surplus. A trader leaves the market when an agreement has been reached or when his deadline expires. Our analysis encompasses both the case of perfect and imperfect information about the partner’s deadline. We define, characterize and show the existence of a stationary equilibrium configuration. We characterize when delay occurs and when deadlines are missed in equilibrium and show that the payoffs of traders are strictly increasing and concave in own deadline, unless bargaining takes place under imperfect information and no delay occurs, in which case all pairs immediately agree on an almost even split. We provide comparative statics exercises and illustrate our results by some examples.

Similar content being viewed by others

Notes

See Cai (2000).

For example, Jennings et al. (1996) detail the application of Advanced Decision Environment for Process Tasks (ADEPT) agents in British Telecom’s customer quote business process. Chavez and Maes (1996) consider MIT’s Kasbah experiment (where agents bought and sold goods on behalf of people). In both cases deadlines were central to the design of the bargaining agents. See also Sandholm and Vulkan (2000) for a general discussion of the role of deadlines in e-commerce applications using software agents.

See Sobel and Takahashi (1983) and Admati and Perry (1987) for examples of delay through signalling and Haller and Holden (1990) and Sákovics (1993) for examples of delay through threats using multiplicity of equilibria. Exceptions are, among others, Merlo and Wilson (1995) in an environment where the bargaining set changes over time in a stochastic manner and Fershtman and Seidmann (1993) who allow for endogenous commitments to not accept proposals that are worse than previously rejected proposals.

Our model and results are readily extended to allow for unequal numbers of buyers and sellers, and also for asymmetric distributions of deadlines for buyers and sellers. In order to save on notation and to improve the exposition, we postpone discussion of the more general model to Sect. 3.5 and confine ourselves here to the symmetric case.

There are some exceptions though. Manea (2012) analyzes matching and bargaining models where inflow distributions are not necessarily stationary.

For convenience we denote \(w_0=0\).

The responder would be indifferent between accepting and rejecting but the proposer would not be willing to make that proposal if he expected it to be accepted with positive probability.

One should realize that payoffs arise endogenous in this model and one cannot rely on generic inflow distributions or discount factors to avoid this case of double indifference.

We do not use the term stationary subgame perfect equilibrium, as that would implicitly refer to strategies. As argued above, the strategies cannot always be pinned down exactly.

This follows from the fact that \(h(i)=1-(\delta /2)^i\) is an increasing and concave function of \(i\), together with a well-known property of second-order stochastic dominance.

For example, it is impossible to have an equilibrium without delay \((z,w,A)\) where \(z=p\) and \(A_{ij}=1\) for all \(i,j\), and, for the same parameters \(\delta \) and \(p\), an equilibrium in which traders with deadline \(N\) disagree with positive probability less than 1. The latter would yield a stationary distribution \(q\) with \(\textit{WA}(q,\delta )<\textit{WA}(p,\delta )\). Moreover, it is easily established that for an inflow distribution \(q\), there would exist an equilibrium without delay with exactly the same payoffs as in the equilibrium with delay. (Such payoffs would satisfy the third condition of the Equilibrium definition.) However, because \(\textit{WA}(q,\delta )<\textit{WA}(p,\delta )\), the latter equilibrium without delay would yield any type of trader a strictly higher payoff than the original equilibrium without delay, and this is impossible.

That is, buyers with a value below and sellers with a cost above the competitive price.

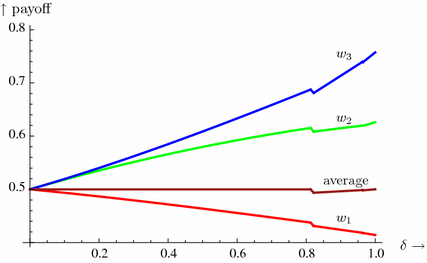

This happens for \(\delta \in (\delta _1,\delta _2)\) and \(\delta \in (\delta _3,\delta _4)\). The latter is difficult to notice in the graph because the interval is very short.

Fig. 2

Equilibrium payoffs for the three types, and average payoff for new trader

Mortensen and Wright (2002), Satterthwaite and Shneyerov (2007), and Shneyerov and Wong (2010b) also allow for distributions of buyer’s valuations and seller’s costs in a dynamic matching and bargaining model, but their main focus is on the convergence of equilibria of such model to Walrasian equilibria as frictions (such as transaction costs) disappear.

References

Admati AR, Perry M (1987) Strategic delay in bargaining. Rev Econ Stud 54:345–364

Anwar AW, Sákovics J (2007) A decentralized market for a perishable good. B.E. J Theor Econ 7(1) (Contributions), Article 7

Bester H, Sákovics J (2001) Delegated bargaining and renegotiation. J Econ Behav Organ 45:459–473

Bose G (1996) Bargaining economies with patient and impatient agents: equilibria and intermediation. Games Econ Behav 14:149–172

Burtraw D (1992) Strategic delegation in bargaining. Econ Lett 38:181–185

Cai H (2000) Bargaining on behalf of a constituency. J Econ Theory 92:234–273

Chavez A, Maes P (1996) Kasbah: an agent marketplace for buying and selling goods. In: Proceedings of the first international conference on the practical application of intelligent agents and multi-agent technology, London, April 1996

Damiano E, Li H (2005) Unravelling of dynamic sorting. Rev Econ Stud 72:1057–1076

Duffie D, Gârleanu N, Pedersen LH (2005) Over-the-counter markets. Econometrica 73:1815–1847

Fershtman C, Seidmann D (1993) Deadline effects and inefficient delay in bargaining with endogenous commitment. J Econ Theory 60:306–321

Gale D (1987) Limit theorems for markets with sequential bargaining. J Econ Theory 43:20–54

Gale D (2000) Strategic foundations of general equilibrium: dynamic matching and bargaining games. Cambridge University Press, Cambridge

Haller H, Holden S (1990) A letter to the editor on wage bargaining. J Econ Theory 52:232–236

Hurkens S, Vulkan N (2006) Dynamic matching and bargaining: the role of deadlines. Barcelona GSE Research Network WP, 188

Jackson MO, Palfrey TR (1998) Efficiency and voluntary implementation in markets with repeated pairwise bargaining. Econometrica 66:1353–1388

Jennings NR, Faratin P, Johnson MJ, Norman TJ, O’Brien P, Wiegand ME (1996) Agent-based business process management. Int J Coop Inf Syst 5:105–130

Ma CA, Manove M (1993) Bargaining with deadlines and imperfect player control. Econometrica 61:1313–1339

Manea M (2012) Bargaining in dynamic markets with multiple populations. Mimeo, MIT

Merlo A, Ortalo-Magné F (2004) Bargaining over residential real estate: evidence from England. J Urban Econ 56:192–216

Merlo A, Wilson C (1995) A stochastic model of sequential bargaining with complete information. Econometrica 63:371–399

Mortensen DT, Wright R (2002) Competitive pricing and efficiency in search equilibrium. Int Econ Rev 43:1–20

Moreno D, Wooders J (2002) Prices, delay, and the dynamics of trade. J Econ Theory 104:304–339

Ponsati C (1995) The deadline effect: a theoretical note. Econ Lett 48:281–285

Rubinstein A (1982) Perfect equilibrium in a bargaining model. Econometrica 50:97–109

Rubinstein A, Wolinsky A (1985) Equilibrium in a market with sequential bargaining. Econometrica 53:1133–1150

Sákovics J (1993) Delay in bargaining games with complete information. J Econ Theory 59:78–95

Samuelson L (1992) Disagreement in markets with matching and bargaining. Rev Econ Stud 59:177–185

Sandholm T, Vulkan N (2000) Bargaining with deadlines. In: Proceedings of the national conference on artificial intelligence (AAAI), Orlando, FL

Satterthwaite M, Shneyerov A (2007) Dynamic matching. Two-sided incomplete information, and participation costs: existence and convergence to perfect competition. Econometrica 75:155–200

Segendorff B (1998) Delegation and threat in bargaining. Games Econ Behav 23:266–283

Serrano R (2002) Decentralized information and the Walrasian outcome: a pairwise meetings market with private values. J Math Econ 38:65–89

Shimer R, Smith L (2000) Assortative matching and search. Econometrica 68:343–369

Shneyerov A, Wong A (2010a) The rate of convergence to perfect competition of matching and bargaining mechanisms. J Econ Theory 145:1164–1187

Shneyerov A, Wong A (2010b) Bilateral matching and bargaining with private information. Games Econ Behav 68:748–762

Sobel J, Takahashi I (1983) A multistage model of bargaining. Rev Econ Stud 50:411–426

Ståhl I (1972) Bargaining theory. Stockholm School of Economics, Stockholm

Vayanos D, Wang T (2007) Search and endogenous concentration of liquidity in asset markets. J Econ Theory 136:66–104

Yildiz M (2004) Optimism, deadline effect, and stochastic deadlines. Mimeo, MIT

Acknowledgments

Hurkens gratefully acknowledges financial support from the Spanish Ministry of Economy and Competitiveness, through grant ECO2012-37065, from AGAUR through grant 2014SGR510 and through the Severo Ochoa Programme for Centres of Excellence in R&D (SEV-2011-0075). We thank the editor, two anonymous referees, Yossi Feinberg, Zvika Neeman, Larry Samuelson and various seminar audiences for helpful comments.

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper replaces and joins two earlier papers by the same authors, namely “Dynamic Matching and Bargaining: The Role of Private Deadlines” and “Dynamic Matching and Bargaining with Heterogeneous Deadlines”.

Appendix

Appendix

Proof of Proposition 2

Let \(Z=\{ z \in \mathfrak {R}_{+}^{N} : \sum _i z_i \ge 1 \text{ and } z_i\le N+1-i \}\) and let \(W=\{ w \in \mathfrak {R}_{+}^{N} : w_1 \le w_2 \le \cdots \le w_N \le 1 \}\). Let \(\mathcal {M}\) denote the set of all symmetric \(N \times N\) matrices with entries in the interval \([0,1]\). Consider the following correspondence \(G: Z \times W \rightarrow Z \times W \times \mathcal {M}\):

and the following mapping \(H: Z \times W \times \mathcal {M} \rightarrow Z \times W\):

where

and

Note that \(\tilde{z}_{i}\le p_i +z_{i+1}\le 1+N+1-(i+1)=N+1-i\) and that \(\tilde{w}_{i}\le \tilde{w}_{i+1} \le 1\) when \(w_{i-1}\le w_i\) so that \(H\) really maps into \(Z \times W\).

We now combine \(G\) and \(H\) to construct a correspondence \(F: Z \times W \rightarrow Z \times W\) as follows:

\(F\) is an upper semi-continuous correspondence from a non-empty, compact, convex set \(Z \times W\) into itself such that for all \((z,w) \in Z \times W\), the set \(F(z,w)\) is convex and non-empty. Convexity of \(F(z,w)\) is of course immediate in the case of a singleton set. Suppose \((\tilde{z},\tilde{w})=H(z,w,A)\) and \((\tilde{z}^{\prime },\tilde{w}^{\prime })=H(z,w,A^{\prime })\) are two different elements of \(F(z,w)\) and let \(\alpha \in [0,1]\). By the definition it follows immediately that \(\tilde{w} = \tilde{w}^{\prime }=\alpha \tilde{w} +(1-\alpha )\tilde{w}^{\prime }\). On the other hand,

We conclude that \(\alpha H(z,w,A)+(1-\alpha ) H(z,w,A^{\prime })=H(z,w,\alpha A+(1-\alpha ) A^{\prime }) \in G(z,w)\). Then applying Kakutani’s fixed point theorem delivers the required result. \(\square \)

Proof of Proposition 3

We first show that \(w_i\) is increasing in \(i\). Obviously, \(0=w_0 < w_1\). Assume that \(w_0 < w_1 < \cdots < w_i\) for some \(i\ge 1\). It is immediate that then \(w_{i+1}>w_i\) because (by the induction step) \(w_i > w_{i-1} \) and \(\max \{\delta w_i, 1-\delta w_{j-1}\} \ge \max \{\delta w_{i-1}, 1-\delta w_{j-1}\}\) for all \(j\).

To show that \(w_i\) is concave in \(i\), let \(J=\{ j : \delta w_{i} > 1-\delta w_{j-1} \}\) and \(J^{\prime }=\{ j: \delta w_{i+1}>1-\delta w_{j-1}\ge \delta w_i \}\). We then have

\(\square \)

Proof of Corollary 4

The first statement follows immediately from the fact that traders with deadline 1 face an outside option of \(w_0=0\) in case of disagreement, together with the observation that \(\delta w_{j-1} <1\), so that \(1-\delta w_{j-1}>w_0\) and \(A_{i 1}=1\).

-

(i)

Let \(A_{ij}<1\). Then \(\delta (v_{i-1}+v_{j-1}) \ge 1\). Concavity implies that \(\delta (v_i+v_{j-2})>\delta (v_{i-1}+v_{j-1}) \ge 1)\), so that \(A_{i+1, j-1}=0\).

-

(ii)

Let \(A_{i+1, j-1}>0\). Then by the previous result it follows that \(A_{ij}=1\).

\(\square \)

Proof of Proposition 5

Suppose there exists an equilibrium without delay when the inflow distribution is \(p\). Let \(\bar{p}_1\) be uniquely defined by \(\bar{p}_1 (\delta /2)+(1-\bar{p}_1)(\delta /2)^N=1-WA(p,\delta )\). Let \(\bar{p}\) denote the extreme inflow distribution with fraction \(\bar{p}_1\) of traders with deadline 1 and fraction \(1-\bar{p}_1\) traders with deadline \(N\). By definition of \(\bar{p}_1\), this alternative inflow distribution satisfies \(WA(\bar{p},\delta )=WA(p,\delta )\) and thus must result in the same payoffs for all types as the original inflow distribution. On the other hand, when there are just two types and there is no delay, payoffs must satisfy the following equalities:

Using that no delay implies that \(\delta v_{N-1}\le 1/2\), it follows immediately that \(v_1 > 1/4\), \(v_{N-1}<3/4\), and \(v_N<2 v_1\). \(\square \)

Proof of Proposition 6

There is no delay if and only if \(2 \delta v_{N-1} \le 1\), where \(v_{N-1}\) is as defined in Proposition 5. \(\square \)

Proof of Corollary 8

-

(i) Let \(p^{\prime }\) first-order stochastically dominate \(p\). Then \(WA(p,\delta ) < WA(p',\delta )\). Therefore

$$\begin{aligned} \frac{1}{2\delta }\ge \frac{1-(\frac{1}{2}\delta )^{N-1}}{2WA(p,\delta )} \ge \frac{1-(\frac{1}{2}\delta )^{N-1}}{2WA(p^{\prime },\delta )}. \end{aligned}$$From Proposition 5 it follows that \(v_j(p,\delta )/v_j(p^{\prime },\delta )=WA(p^{\prime },\delta )/WA(p,\delta ) > 1\).

-

(ii) Let \(p^{\prime }\) second-order stochastically dominate \(p\). Then \(WA(p,\delta ) < WA(p',\delta )\) and the statement follows from Propositions 5 and 6.

-

(iii) Let \(L(\delta )=\delta -\left( \frac{1}{2}\right) ^{N-1} \delta ^{N}-\sum _{i=1}^{N} p_i\left( 1-\left( \frac{1}{2}\delta \right) ^{i}\right) \). We will show that \(L(\delta )\) is increasing for \(\delta < 1\) which proves the claim as Proposition 6 states that there exists an equilibrium without delay if and only if \(L(\delta )\le 0\). Observe that for all natural numbers \(N\) and any \(\delta \in [0,1)\)

$$\begin{aligned} 2^{N-1}-N\delta ^{N-1}>2^{N-1}-N\ge 0 \end{aligned}$$so that

$$\begin{aligned} L'(\delta )&= 1-\frac{N\delta ^{N-1}}{2^{N-1}}+\sum _{i=1}^N p_i\frac{i\delta ^{i-1}}{2^i} > 0. \end{aligned}$$Note that if \(v_1(p,\delta ^{\prime })\le v_1(p,\delta )\), then it would follow from (2) that \(v_i(p,\delta ^{\prime }) < v_i(p,\delta )\) for all \(i>1\). This is impossible because total surplus is equal to 1 in both cases. Hence, we conclude that \(v_1(p,\delta ^{\prime }) > v_1(p,\delta )\). In a similar fashion it can be shown that \(v_N(p,\delta ^{\prime }) < v_N(p,\delta )\).

-

(iv) Suppose there is delay. Then \(w_N>w_{N-1}\ge \delta w_{N-1} \ge 1/2\). Hence, every new trader entering the market (before learning his deadline) expects to obtain strictly more than 1/2. This is not sustainable.

\(\square \)

Proof of Proposition 11

Let \(Z=\{ z \in \mathfrak {R}_{+}^{N} : \sum _i z_i \ge 1 \text{ and } z_i\le N+1-i \} \) and let \(W=\{ w \in \mathfrak {R}_{+}^{N} : w_1 \le w_2 \le \cdots \le w_N \le 1 \}\). Let \(\mathcal {M}\) denote the set of all \(N \times N\) matrices with entries in the interval \([0,1]\) whose row sums are equal to 1. For any \( w \in W\), let \(X(w)=\{\delta w_0, \delta w_1, \ldots , \delta w_{N-1} \}\) denote the set of (potentially optimal) offers. (Here \(w_0=0\).) The entry \( M_{ij}\) of the matrix \(M\) is to be interpreted as the probability with which a proposer with deadline \(i\) offers \(\delta w_{j-1}\).

Consider the following correspondence \(G: Z \times W \rightrightarrows Z \times W \times \mathcal {M}\):

The correspondence \(G\) adds (mixed) strategies of proposers that are myopically optimal. That is, they are optimal given the distribution of deadlines implied by \(z\), and under the further assumptions that a responder with deadline \(j\) accepts proposal \(x\) if and only if \(x \ge \delta w_{j-1}\) and that rejected proposals yield proposer with deadline \(i\) an expected payoff equal to \(w_{i-1}\) one period later.

We furthermore define the following mapping \(H: Z \times W \times \mathcal {M} \rightarrow Z \times W\):

where \(\tilde{z}_N=p_N\) and for \(i<N\),

and, for all \(i\),

The mapping \(H\) recalculates the mass of traders with different deadlines from the proposal strategies given by \(M\) (and given the responders’ strategies described before) and updates the expected payoff of traders. Note that \(\tilde{z}_{i}\le p_i +z_{i+1}\le 1+N+1-(i+1)=N+1-i\) and that \( \tilde{w}_{i}\le \tilde{w}_{i+1} \le 1\) when \(w_{i-1}\le w_i\) so that \(H\) really maps into \(Z \times W\).

We now combine \(G\) and \(H\) to construct a correspondence \(F: Z \times W \rightrightarrows Z \times W\) as follows:

\(F\) is an upper semi-continuous correspondence from a non-empty, compact, convex set \(Z \times W\) into itself such that for all \((z,w) \in Z \times W\) , the set \(F(z,w)\) is convex and non-empty. Convexity of \(F(z,w)\) is of course immediate in the case of a singleton set. Suppose \((\tilde{z},\tilde{w })=H(z,w,M)\) and \((\tilde{z}^{\prime },\tilde{w}^{\prime })=H(z,w,M^{\prime })\) are two different elements of \(F(z,w)\) and let \(\alpha \in [0,1]\). By the definition it follows immediately that \((z,w,\alpha M+(1-\alpha )M^{\prime }) \in G(z,w)\). Because of the linearity in \(M\), it is straightforward that

Hence, \(\alpha (\tilde{z},\tilde{w})+ (1-\alpha ) (\tilde{z}^{\prime },\tilde{w }^{\prime })\in F(z,w)\) and applying Kakutani’s fixed point theorem delivers the required result. \(\square \)

Proof of Proposition 12

First, assume the inequality is satisfied and consider the following strategies. All types offer as a proposer \(\delta /2\) to the opponent and keep \(1-\delta /2\) for themselves. Types with deadlines \(i>1\) accept any proposal that yields them at least \(\delta /2\). Type 1 accepts any proposal that yields him a nonnegative payoff. It is clear that these strategies yield all traders an expected payoff of \(1/2\). Also, given the proposer’s strategies, it is optimal to accept any proposal equal to or above \(\delta /2 \) and to reject (in the case of deadlines higher than 1) any lower proposals. For a trader with deadline 1 it is obviously optimal to accept any nonnegative offer. The only remaining question is whether some trader could do better by making a different proposal. Given the responder’s strategies, the only alternative strategy that could possibly give a higher payoff would be to offer \(0\) (in the hope of being matched with a trader whose deadline is about to expire). Conditional on being a proposer (with deadline \(i>1\)) following the outlined strategy yields \(1-\delta /2\). Offering \(0\) will only be accepted by traders with deadline equal to 1, so this yields an expected payoff of \(p_1\times 1+(1-p_1)\times \delta v_{i-1}= \delta /2 + p_1(1-\delta /2)\). The equilibrium condition is thus

or, equivalently,

Second, suppose the inequality is not satisfied and suppose there exists an equilibrium with \(v_i=v\) for all \(i\). Clearly, \(v\le 1/2\). In such equilibrium offers above \(\delta v\) must be accepted and offers below must be rejected (except for traders with deadline 1 who will accept any nonnegative offer). Therefore, the only offers that can possibly be made in equilibrium are \(\delta v\) and \(0\). If \(0\) is never offered then it follows that \(v=1/2\) but then traders with high deadline are better off offering \(0\) , as we have seen before. Hence, some traders must propose \(0\) with positive probability. But that implies that \(v_i < v_{i+1}\) for all \(i\) as a trader with deadline \(i+1\) can imitate a trader with deadline \(i\) but has an extra chance to get a positive payoff in the event of being proposed \(i\) times an offer of zero. \(\square \)

Proof of Proposition 13

Traders with deadline \(j+1\) can always use the same strategy that traders with deadline \(j\) use. Hence, \(v_{j+1} \ge v_j\). From the previous proposition we know that not all traders receive the same payoff. Hence, for some deadline \( k\) we have \(v_1 \le \cdots \le v_k < v_{k+1} \le \cdots \le v_N\). This implies that a trader with deadline \(k\) cannot imitate the trader with deadline \(k+1\). Hence, there must be a positive probability that a trader with deadline \(k+1\) will still be in the market when his deadline has reduced to 1. This in turn implies that for any trader with deadline \(j<k+1\) there is a positive probability that he will remain in the market for \(j\) periods. In particular, this is the case for a trader with deadline 2. Clearly, this means that delay occurs with positive probability.

First we show that \(v_1<v_2\). This is obvious if the zero offer is made with positive probability, because then a trader with deadline 2 could just mimic the behavior of a trader with deadline 1, except for the case where a zero offer is received, which should be rejected. Similarly, if the trader with deadline 1 makes an offer in equilibrium which is rejected with positive probability, then the trader with deadline 2 can mimic a trader with deadline 1. In case of being chosen as a proposer and the proposal being rejected, the trader with deadline 2 will have another chance to obtain a positive payoff. Hence, also in this case we must have \(v_1<v_2\). So let us assume that the zero offer is not made and that traders with deadline 1 make a proposal that is accepted for sure. Then the lowest offer that can be made in equilibrium equals \( \delta v_1\), which a trader with deadline 2 will accept with probability 1 in equilibrium. We know that a trader with deadline 2 will sometimes delay in equilibrium. This can only happen when he makes a proposal that is rejected by some trader(s), let us say, \(\delta v_{m-1}<\delta v_{N-1}\). We can only have that \(v_1=v_2\) if in fact trader 2, as a proposer, is indifferent between making the offers \(\delta v_{m-1}\) and \(\delta v_{N-1}\). But if this is the case, trader \(k\) can mimic the behavior of a trader with deadline \(k+1\) as long as the remaining deadline is strictly above 1, and make the proposal that is certainly accepted when the deadline has reduced to 1. In this way trader \(k\) can obtain the same payoff as trader \(k+1\), which is a contradiction. Hence, we have established that \(v_1<v_2\).

It follows immediately that for all traders with \(j<k\) that \(v_j<v_{j+1}\). Namely, trader \(j+1\) can mimic trader \(j\) as long as the remaining deadline is above 2, and use the equilibrium strategy of a trader with deadline 2 when the deadline has reduced to 2. In this way trader \(j+1\) guarantees a payoff strictly higher than what trader \(j\) can get.

We thus have either that (i) \(v_1< v_2< \cdots <v_N\) or (ii) there exists a deadline \(j>k\) such that \(v_1<\cdots < v_j=v_{j+1} \le \cdots \le v_N\).

Suppose we are in case (ii). As argued before, it must be the case that there is a positive probability of delay for all traders with deadline \(i\) such that \(1<i<j+1\). Because the trader with deadline \(j+1\) could imitate the trader with deadline \(j\), but cannot do better than him, the zero offer is never made. (Namely, if the zero offer is made with positive probability, then he could do strictly better by not accepting the zero offer when his deadline has reduced to 2.) Consider now the possibility of trader \(j+1\) imitating trader \(j\) for one period. If a deal is concluded, he would obtain the same payoff as the trader with deadline \(j\) in that circumstance. On the other hand, if there is delay (which happens with positive probability, then his future expected payoff is \(v_j>v_{j-1}\). Hence, trader \(j+1\) can guarantee a strictly higher payoff than \(j\) and case (ii) cannot occur. We conclude that in any equilibrium \(v_1<\cdots <v_N\).

Finally, it is straightforward to verify that deadlines are missed in equilibrium when, for example, \(p=(0.99,0.01)\). In this case every proposer will offer zero to the responder, which is only accepted by traders with deadline 1. Hence, with positive probability deadlines are missed. \(\square \)

Proof of Proposition 14

We already know that in an equilibrium without delay all traders make the same offer of \(\delta /2\). Consider an SSPE configuration without delay such that \(v_{j-1}<v_j\) for all \(j\). Denote \( Q_{m}=q_1+\cdots +q_m\) for any \(1 \le m \le N\). Then \(Q_m<Q_{m+1}\) and \(Q_N=1\) .

The first inequality states that a trader with deadline \(j\) weakly prefers to offer \(\delta v_{i-k}\) rather than \(\delta v_{i}\). The last inequality says that a trader with deadline \(j+1\) strictly prefers to offer \(\delta v_{i-k}\) rather than \(\delta v_{i}\). \(\square \)

Rights and permissions

About this article

Cite this article

Hurkens, S., Vulkan, N. Dynamic matching and bargaining with heterogeneous deadlines. Int J Game Theory 44, 599–629 (2015). https://doi.org/10.1007/s00182-014-0446-6

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00182-014-0446-6