Abstract

Intellectual capital has become the one indispensable asset of organizations. Managing its human, relational, and structural components is of the essence of modern business.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

- Capital theory

- Factors of production

- Human capital

- Intangible assets

- Intellectual capital management

- Intellectual capital statements

- Managing Intellectual capital

- Measuring intangibles

- Relational capital

- Resources

- Structural capital

- Value creation

- Value extraction

- Value reporting

- Valuing intangibles

In a Word Intellectual capital has become the one indispensable asset of organizations. Managing its human, relational, and structural components is of the essence of modern business.

Karl Marx Redux

Karl Marx would be amused. He longed for the day when the workers would own the means of production. Now they do.

—Charles Handy

Following Smith (2010),Footnote 1 factors of production —the inputs or resources needed to turn out goods and services (and contribute to a nation’s wealth)—were for long classified into (i) land (or natural resources); (ii) labor (or human effort); and (iii) capital stock (or machinery, tools, and buildings). (The classical economists did not include money since they did not think it was used to directly turn out goods and services.)Footnote 2 Although early interest can be traced to the seventeenth century, certainly in the work of William Petty, only in the last 50 years has been capital theory distinguished human capital Footnote 3 (the stock of knowledge in individuals) from labor. More recently still, starting in the early 1990s, knowledge has been recognized as a factor of production in its own right.

The Wealth of Knowledge

Stewart (1997),Footnote 4 for one, has come to believe that knowledge is the most important factor in the modern economy and the key to achieving competitive advantage in a globalizing world. (Obviously, conventional assets have not disappeared and will not.) If they know what they know,Footnote 5 the knowledge that individuals and organizations hold (and hopefully fructify) can advance their purposes by enhancing the valueFootnote 6 of other factors of production . Certainly, however, this requires that the nature of knowledge assets be understood at something more than skin depth.

Define: Intellectual Capital

We make doors and windows for a room. But it is the spaces that make the room livable. While the tangible has advantages, it is the intangible that makes it useful.

—Lao Tzu

Born of the information revolution, knowledge management has arisen in response to the belated understanding that intellectual capital is a core asset of organizations and that it should be circumscribed better.Footnote 7 From this perspective, it is the growing body of tools, methods, and approaches, inevitably underpinned by values, by means of which organizations can bring about and maximize a return on knowledge assets, aka intellectual capital.Footnote 8 That, Thomas Stewart explained pithily (yet broadly) is organized knowledge that can be used to generate wealth.Footnote 9 (Conversely, it also helps to think of what intellectual capital is not, that is, monetary or physical resources .)

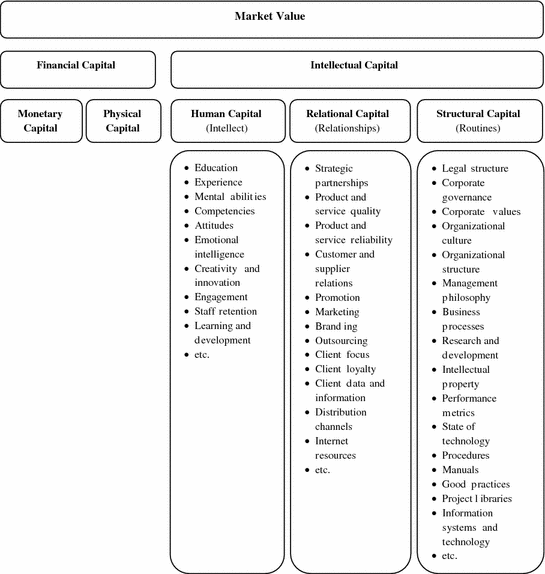

More specifically, aggregated intellectual capital comprisesFootnote 10

-

Human capital —the cumulative capabilities and engagement of an organization’s personnel, rooted in tacit and explicit knowledge, that can be invested to serve the joint purpose.

-

Relational (or customer) capital —the formal and informal external relationships, counting the information flowsFootnote 11 across and knowledge partnerships in them, that an organization devises with clients, audiences, and partners to cocreate products and services, expressed in terms of width (coverage), channels (distribution), depth (penetration), and attachment (loyalty).

-

Structural (or organizational) capital —the collective capabilities of an organization—many of them codified, packaged, and systematized, including its governance, values, culture, management philosophy, business processes, practices,Footnote 12 research and development, intellectual property,Footnote 13 performance metrics, and information systems, as well as, the systems for leveraging them.

Fig. An intellectual capital model. Source Author

Managing Intellectual Capital

The greatest achievement of the human spirit is to live up to one’s opportunities and make the most of one’s resources.

—Marquis de Vauvenargues

Intellectual capital management is the active management of intellectual capital resources with multiplicative effects. The schemes that can be applied singly or across the three types relate to

-

Value creation —the strategic generation of knowledge and its conversion into valuable forms.Footnote 14

-

Value extraction —the strategic conversion of created value into useful forms.Footnote 15

-

Value reporting —the accurate reflection of the value of intellectual capital—once the what, why, how, when, and where of qualitative and quantitative measurement, as well as its responsibility center, have been decided—for both analysis and decision making,Footnote 16 internally by senior management and externally by clients, audiences, and partners.Footnote 17

Naturally, managing intellectual capital effectively rests on balancing value creation, extraction, and reporting to meet the goal of the organization.

Moving from First- to Third-Generation Thinking …

The continuing rise of knowledge-based economies demands that organizations devise new—or at least parallel—systems for measuring qualitative, nonfinancial items of intellectual capital to supplement traditional, quantifiable, financial measures of their fitness for purpose. Intellectual capital and its hidden capabilities are now visualized and there is a discourse we can all engage in.Footnote 18 To date, however, the measurement of intellectual capital remains relatively new, with a smattering of organizations, more often than not in Scandinavian countries, actually using measurement systems since the mid-1990s. There are a dozen disclosure systems, of which three or four are popular.Footnote 19 The basic objectives are comparable but taxonomies are not aligned: therefore, a second body of work for unreported assets would concentrate on standardizing voluntary reporting frameworks, including their boundaries and associated vocabulary; shedding light on the why, what, and how of reporting on intellectual capital with performance metrics that serve both as a management and a communication toolFootnote 20; and replacing rhetoric with actionable statements.Footnote 21 A third wave would broaden the context of measurement to move beyond simple causal maps and amplify efforts to build future capabilities.

… With Early Steps

A problem well stated is a problem half-solved.

—Charles Kettering

The five generic reasons why organizations (ought to) seek to measure intellectual capital are to (i) formulate strategy, (ii) assess strategy execution, (iii) make diversification and expansion decisions, (iv) broaden justification for compensation (and other benefits), and (v) communicate measures to internal and external stakeholders. The business case for managing intellectual capital is becoming stronger: in knowledge-based economies, investments that compound intangible assets have a better return than those in other factors of production .Footnote 22 In the final analysis, the only thing limiting progress is the willingness of organizations to define, measure, analyze, improve, and control.Footnote 23 Intellectual capital might then, on the word of Ulrich (1998), truly equal competence times commitment. Paraphrasing further, earnest responses to 10 effective questions will according to Petty and Guthrie (2000) help achieve visible benefits.

-

What motivates the organization to want to measure its intellectual capital?

-

What are the current and anticipated effects of reporting intellectual capital?

-

Is generating information on intellectual capital feasible from a cost-benefit perspective?

-

Within the organization, who is best positioned to measure and manage intellectual capital?

-

How might current methods of measuring intellectual capital be improved?

-

What is the extent of demand for intellectual capital reporting by stakeholders?

-

Is information on intellectual capital transparent, robust, reliable, and verifiable?

-

In what manner are current gaps in information a barrier to better management of intellectual capital and improved decision-making?

-

What specific difficulties are associated with the development of a reporting system on intellectual capital and how might they be overcome?

-

Where should information on intellectual capital be presented?

Notes

- 1.

Adam Smith (1723–1790), a Scottish political economist and social philosopher, laid the intellectual framework that explained the free market. The magnum opus he published in 1776, The Wealth of Nations, is considered the first modern work of economics.

- 2.

To note, notwithstanding their agrarianist philosophy, the French physiocrats—such as François Quesnay (1694–1774) and Anne-Robert-Jacques Turgot (1727–1781)—who succeeded the mercantilists and immediately preceded the classical economists had identified entrepreneurship (or enterprise) to tally four factors. The prime advocate of a labor theory of value, Karl Marx (1818–1883), a German philosopher, sociologist, economic historian, journalist, and revolutionary, believed that all production belongs to labor because workers alone create value in society. Later schools, including the neoclassical economists, have continued to argue over which factor, including entrepreneurship, is the most important; proposed further distinctions of capital, e.g., fixed, working, and financial capital, as well as additions such as the state of technology and human capital; and, as we shall see, made intellectual capital the object of interest in sundry disciplines other than economics.

- 3.

Human capital refers to the stock of knowledge, skills, and experience embodied in labor. (Some bring in health, values, behaviors, and motivation.) It is the sum total of attributes, in general cultivated by a worker through education and experience, that determine his or her value in the marketplace.

- 4.

A brief account of the early days of the intellectual capital movement must cite the pioneering contribution of Hiroyuki Itami who brought out Mobilizing Invisible Assets in Japanese in 1980. In 1986, Karl-Erik Sveiby published the Know-How Company in Swedish. Chronologically, Brian Hall, David Teece, Leif Edvinsson, Hubert Saint-Onge, and Patrick Sullivan were other precursors of work on value creation, value extraction, and value reporting. The frequency and specificity of contributions to the field—theme might be a better word—have multiplied since its inception in the 1980s. (The dates suggest that managing intellectual capital was perhaps the first coherent theme that emerged under the discipline of knowledge management, even if collaboration between knowledge management and intellectual capital management researchers leaves something to be desired).

- 5.

Knowledge equates with the meaningful links that, through experience or association, people make in their minds between data and information and their application in action in specific situations. It only becomes an asset if some useful order is created so it may be formalized, captured, and leveraged in actionable value propositions that accomplish something that could not be done before.

- 6.

Value is (i) a fair return or equivalent in goods, services, or money for something exchanged; (ii) the monetary worth of something: market price; (iii) relative worth, utility, or importance; (iv) a numerical quantity that is assigned or is determined by calculation or measurement; and/or (v) something (as a principle or quality) intrinsically valuable or desirable.

- 7.

The intangible (but, at the commonly cited rate of 80% of an organization's value, nonetheless very precious) assets that make up intellectual capital are not normally ascribed a value in an organization's balance sheet. (Put differently, they are roughly—but not exactly—the difference between the market and book value of its equity.) Yet, they are used to manufacture goods or provide services and are expected to create value (as well they do through, say, profit generation from products, services, or intellectual property; strategic positioning; acquiring the innovations of others when new personnel joins; customer loyalty; cost reductions; or improved productivity). The notion of intellectual capital provides a conceptual platform from which to view, analyze, and (hopefully) quantify them.

- 8.

The steps involved in capitalizing return might involve, say, acquiring, developing, utilizing, and exploiting knowledge assets.

- 9.

Although everyone agrees that intellectual capital underpins organizational performance, there is a regrettable—yet unavoidable—lack of consensus over definitions of it owing to the diversity of disciplinary and interdisciplinary views from which it is examined. Usefully, Marr (2005) elucidates economics, strategy, accounting, finance, reporting, marketing, human resource, information systems, legal, and intellectual property perspectives. The interdisciplinary views he brings to the subject are interfirm, public policy, knowledge-based, and epistemological.

- 10.

Most models of intellectual capital assume a three-way distinction. However, they differ in the names and levels of aggregation. Structural capital is sometimes segregated into according to what has been formalized, e.g., business processes, and what has not, e.g., organizational culture. Pell-mell, and unmanageably so hence the usefulness of discriminating between them, the constituents of intellectual capital include competencies, experience, know-how, knowledge, skills; creativity, innovation; computer programs, databases, information systems, technologies; business processes, methodologies; designs, documents, drawings, publications; intra-organization and inter-organizational relationships; brands, trademarks, etc.

- 11.

As you would expect, information flows and the perceptions they shape influence corporate reputation.

- 12.

Formal and informal practices determine how business processes are handled and how work flows through an organization. They comprise, for example, virtual networks, tacit rules of behavior or workflows, and process manuals that lay out codified procedures and rules.

- 13.

Intellectual property, very broadly, means the legal industrial property and copyright secured from the use of notable mental capacity in the artistic, industrial, literary, and scientific fields. To wit, creations of the mind such as inventions and scientific discoveries; literary and artistic works and their production, performance, and broadcast; and symbols, names, images, and designs can receive legal protection, for instance, by means of copyright and related rights, design rights, geographical indications, industrial designs and integrated circuits, patents, protection against unfair competition, trademarks, and trade secrets. It is no curiosity that explicit rights should be associated with intellectual property and not so readily with other forms of intellectual capital: the latter are frequently (though not always) a process, not an outcome, and are therefore more intangible. (In comparison, when patenting an intellectual property, the owner must make a full disclosure of characteristics by including a specification (description and claims), relevant drawings, prototypes, etc. that clearly define it.) For these reasons, intellectual property usually has a life, certainly in the case of patents, and can often be traded. (Then again, it does not necessarily provide competitive advantage.).

- 14.

Knowledge Solutions that promote tools, methods, and approaches to create value pertain to action learning, appreciative inquiry, asking effective questions, building communities of practice, building networks of practice, coaching and mentoring, creating and running partnerships, critical thinking, drawing mind maps, engaging staff in the workplace, the Five Whys technique, harnessing creativity and innovation, identifying and sharing good practices, learning and development for management, leading top talent in the workplace, learning in strategic alliances, managing corporate values, the reframing matrix, the SCAMPER technique, sparking innovations in management, sparking social innovation, social network analysis, and working in teams.

- 15.

Knowledge Solutions that advance tools, methods, and approaches to extract value have to do with conducting after-action reviews and retrospects, conducting exit interviews, conducting peer assists, enriching policy with research, harvesting knowledge, learning from evaluation, learning lessons with knowledge audits, linking research to practice, the Most Significant Change technique, picking investments in knowledge management, and staff profile pages.

- 16.

Without reporting systems, on what basis other than guesswork can one invest new capital into worthy, but intangibles-reliant, ventures?

- 17.

Knowledge Solutions that advertise tools, methods, and approaches to report value refer to auditing knowledge, disseminating knowledge products, focusing on project metrics, e-learning in the workplace, monthly progress notes, outcome mapping, output accomplishment and the design and monitoring framework, the perils of performance measurement, sector and thematic reporting, showcasing knowledge, social reminiscing, storytelling, and taxonomies for development.

- 18.

In the first phase, the bulk of effort was expended on raising awareness of the potential of intellectual capital in creating and managing sustainable competitive advantage.

- 19.

Robert Kaplan and David Norton introduced the Balanced Scorecard in 1992 to help organizations view themselves also from perspectives of learning and growth, business processes, and clients, in addition to finance, for each of which objectives, indicators, targets, and measures should be specified. (This said, the learning and growth perspective has been something of a black hole, with organizations plugging the gap with human resource-related measures, prompting Kaplan and Norton (2004) to posit in 2004 a new definition of intangible assets, viz., human capital, information capital, and organizational, that might have made more of existing classifications.) In 1995, Leif Edvinsson devised the Skandia Navigator, which embodies the same set of concerns as the scorecard but also considers what processes the organization has to nurture personnel. In 1997, Karl-Erik Sveiby devised the Intangible Assets Monitor, which invites application of growth, efficiency, and stability indicators across the accepted tripartite model; unlike the Balanced Scorecard, no financial targets are to be set. (At about the same time, Göran and Johan Roos advertised their proprietary Intellectual Capital Index providing a dynamic view of how intellectual stocks can change over time—by simplifying categories into indices, the index aims to predict returns as investment strategies shift).

- 20.

Measurement, a quantitatively expressed reduction of uncertainty based on one or more observations, is at the end of the day more about the process of measuring than it is about hard numbers. When designing measurement systems, a rule of thumb is that it is better to be roughly right than precisely wrong. At appropriate levels of control, the common criteria used to improve effectiveness are (i) time, (ii) cost, (iii) resources, (iv) scope, (v) quality, and (vi) actions. It is critical to understand an organization's context; epistemology; and value creation, -extraction, and -reporting pathways if they are to serve as benchmarks.

- 21.

In 2000 and 2003, the Ministry of Science, Technology, and Innovation in the Government of Denmark gave guidance on formulating intellectual capital statements to help organizations build up, develop, share, and anchor the knowledge that can make their products and services worth more. The four elements of the statements are (i) a knowledge narrative that expresses the ambition to increase the value a user receives from an organization's goods or services, (ii) a set of knowledge management challenges highlighting the knowledge resources that need to be strengthened through in-house development or by sourcing them externally, (iii) a set of initiatives that can be started to do something about the challenges, and (iv) a set of indicators that make it possible to follow up whether the initiatives have been launched or whether the challenges are being met (Danish Ministry of Science, Technology, and Innovation 2003). (The indicators suggested might measure effect, activities, and resource mix.).

- 22.

This is so regardless of whether an organization is in the public or private sector.

- 23.

This can only take place after an organization's critical intellectual capital has been marked out, conceivably also by means of knowledge audits. Then, because many types of intellectual assets are difficult to gauge directly, proxy measures can be used. Consider, for example, the budgets needed to operate (i) human capital—such as the costs of finding and recruiting talent, learning and development, etc.; (ii) relational capital—such as the outlays for promotion, marketing, branding, outsourcing, acquiring product or quality certifications, etc.; and (iii) structural capital—such as the internal and external expenditures for building processes, hiring process development consultants, developing software applications for internal systems, running knowledge management systems, investing in research and development, acquiring and documenting intellectual property rights, etc.

References

Danish Ministry of Science, Technology, and Innovation (2003) Intellectual capital statements—the new guideline. Copenhagen

Kaplan R, Norton D (2004) Strategy maps: converting intangible assets into tangible outcomes. Harvard Business School Publishing

Marr A (ed) (2005) Perspectives on intellectual capital: multidisciplinary insights into management, measurement, and reporting. Butterworth-Heinemann

Petty R, Guthrie J (2000) Intellectual capital review: measurement, reporting, and management. Journal of Intellectual Capital 1(2):155–176

Smith A (2010) An inquiry into the nature and causes of the wealth of nations. General Books

Stewart T (1997) Intellectual capital: the new wealth of organizations. Currency Doubleday

Ulrich D (1998) Intellectual capital = competence × commitment. Sloan Management Review 39(2):15–26

Further Reading

Ehin C (2000) Unleashing intellectual capital. Butterworth-Heinemann

Sullivan P (2000) Value-driven intellectual capital: how to convert intangible corporate assets into market value. Wiley, Inc

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

The opinions expressed in this chapter are those of the author(s) and do not necessarily reflect the views of the Asian Development Bank, its Board of Directors, or the countries they represent.

Open Access This chapter is licensed under the terms of the Creative Commons Attribution-NonCommercial 3.0 IGO license (http://creativecommons.org/licenses/by-nc/3.0/igo/) which permits any noncommercial use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the Asian Development Bank, provide a link to the Creative Commons license and indicate if changes were made.

Any dispute related to the use of the works of the Asian Development Bank that cannot be settled amicably shall be submitted to arbitration pursuant to the UNCITRAL rules. The use of the Asian Development Bank’s name for any purpose other than for attribution, and the use of the Asian Development Bank’s logo, shall be subject to a separate written license agreement between the Asian Development Bank and the user and is not authorized as part of this CC-IGO license. Note that the link provided above includes additional terms and conditions of the license.

The images or other third party material in this chapter are included in the chapter’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2017 Asian Development Bank

About this chapter

Cite this chapter

Serrat, O. (2017). A Primer on Intellectual Capital. In: Knowledge Solutions. Springer, Singapore. https://doi.org/10.1007/978-981-10-0983-9_20

Download citation

DOI: https://doi.org/10.1007/978-981-10-0983-9_20

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-10-0982-2

Online ISBN: 978-981-10-0983-9

eBook Packages: Business and ManagementBusiness and Management (R0)