Case

Supplementary Resources

Abstract

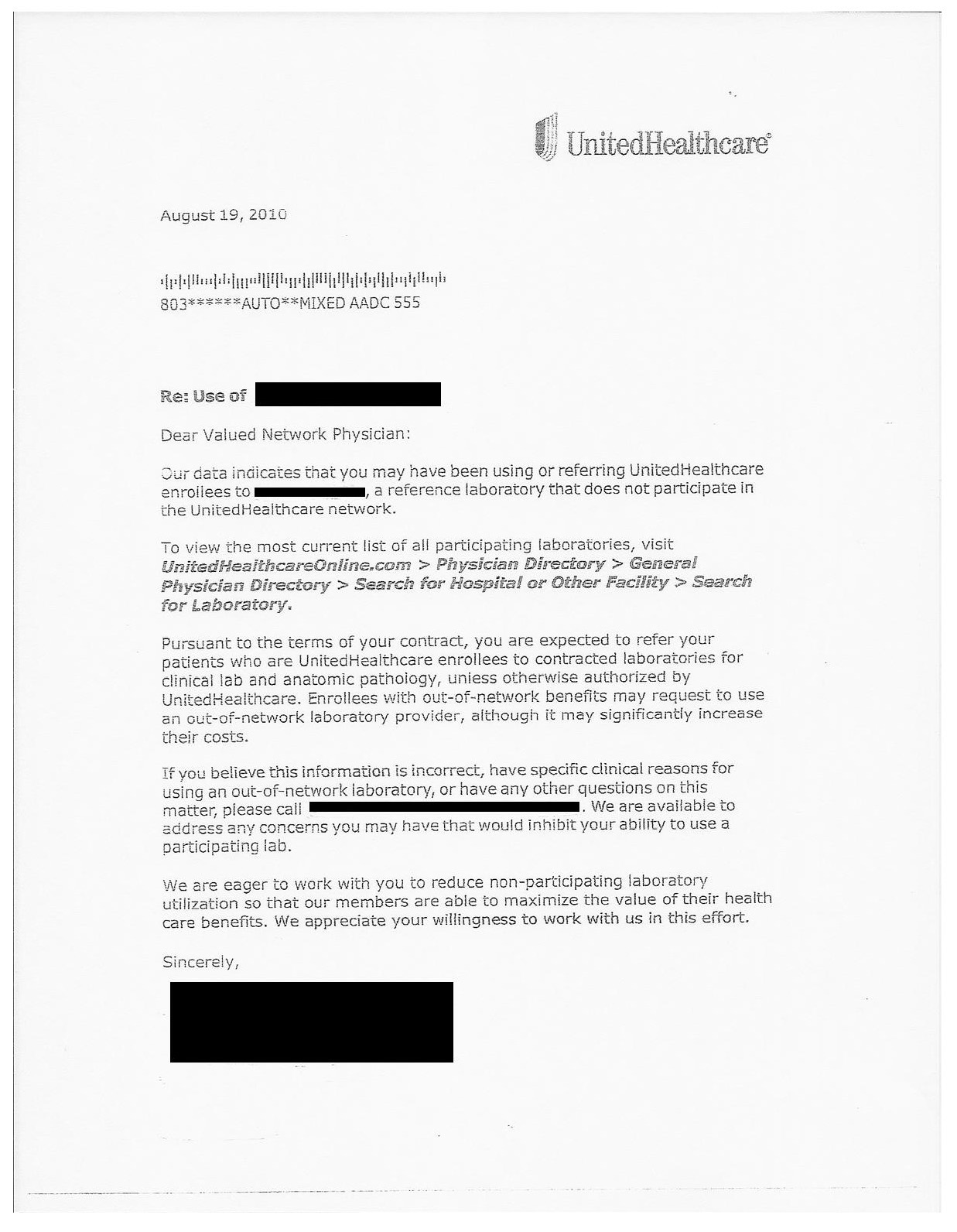

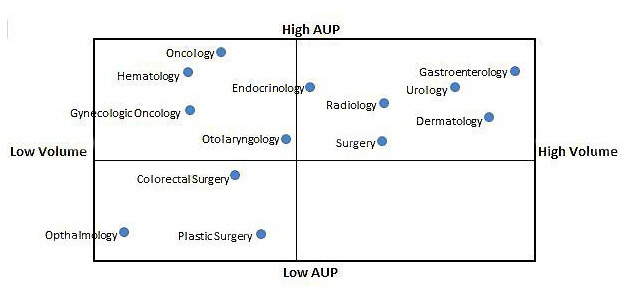

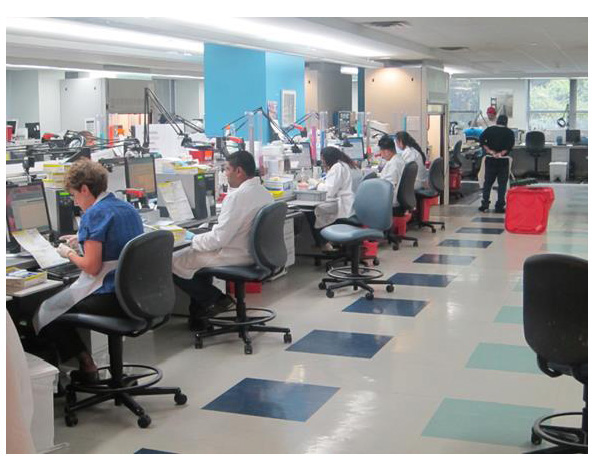

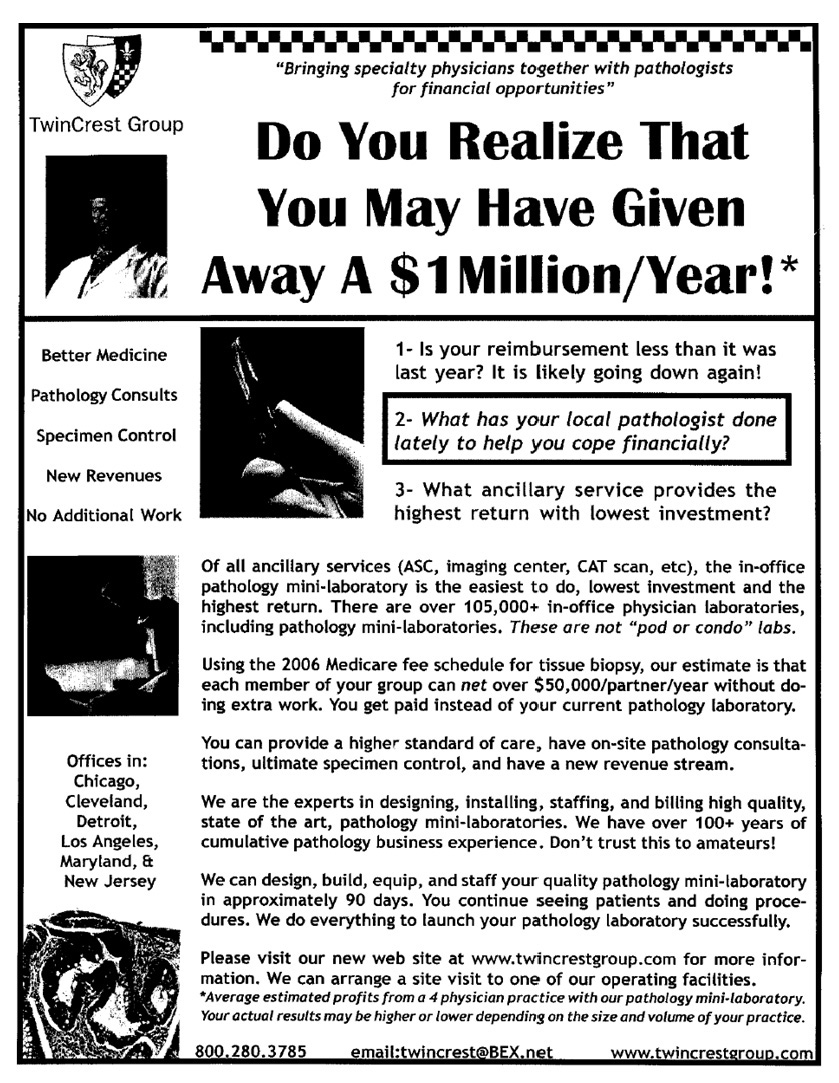

In the beginning of 2007, Dr. Carlos Urmacher, the Chief Medical Officer of CBLPath, and David Bryant, President and Chief Operating Officer of CBLPath, found themselves in the curious position of having their clients ask for their help in reducing the amount of work they were sending to CBLPath. The company was not alone in this situation. Throughout the country, large medical groups were “insourcing” pathology. CBLPath was a medium-sized commercial anatomic pathology lab, serving medical practices on the east coast of the United States. Like other anatomic pathology labs, CBLPath had established relationships with medical practices that needed to have tissue samples (biopsies) analyzed for the presence of disease. Physicians would take biopsies of suspect tissue and courier them to CBLPath's labs. At the lab, the tissue would be prepared for analysis and then scrutinized by pathologists. Having arrived at a diagnosis, the pathologist would issue a written report to the physician. Since Urmacher took an equity stake and went to work for CBLPath in 2000, the company had emphasized high quality medical service. CBLPath employed a large number of pathologists committed to accurate diagnosis and intensive consulting with physicians. When Bryant joined the company from a competitor, CBLPath added increased customer service and a knowledgeable sales force to its operations. In the intervening years, “high touch” service and medical expertise became central to CBLPath's identity. Like other pathology labs, CBLPath billed insurance companies (or Medicare) directly for its services. For each test, there was a technical component (TC) of the bill related to preparation of the sample and a professional component (PC) for the pathologist's analysis. In the 2000s, a number of larger medical practices began to insource the TC and/or PC. The economic incentives were obvious. While insurance companies had reduced the amount they were willing to pay for most medical services, the remittances for pathology tests had remained relatively constant.

A number of commercial pathology labs were helping medical practices insource by aiding in the set-up of labs in the practices and/or supplying the TC or PC while the practices performed and billed the rest. Some of CBLPath's largest customers had asked the company to join in a similar arrangement. Until now, CBLPath had resisted. Urmacher and Bryant saw CBLPath's reputation for complete and excellent pathology services as being central to the company's future. But with large numbers of their best customers considering insourcing, Urmacher and Bryant wondered if it wouldn't be better to secure half a revenue stream rather than none.

This case was prepared for inclusion in Sage Business Cases primarily as a basis for classroom discussion or self-study, and is not meant to illustrate either effective or ineffective management styles. Nothing herein shall be deemed to be an endorsement of any kind. This case is for scholarly, educational, or personal use only within your university, and cannot be forwarded outside the university or used for other commercial purposes.

2025 Sage Publications, Inc. All Rights Reserved