An Integrated Framework for Sustainable Development in Agri-Food SMEs

1

GNOSIS Mediterranean Institute for Management Science, School of Business, University of Nicosia, 2417 Nicosia, Cyprus

2

Department of Marketing, School of Business, University of Nicosia, 2417 Nicosia, Cyprus

*

Authors to whom correspondence should be addressed.

Sustainability 2023, 15(12), 9387; https://doi.org/10.3390/su15129387

Submission received: 24 May 2023

/

Revised: 7 June 2023

/

Accepted: 9 June 2023

/

Published: 11 June 2023

(This article belongs to the Special Issue Innovation in SMEs and Sustainable Development: The Current Situation and the Way Forward)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:The primary objective of this study is the development of an integrated framework for sustainable development in agri-food Small and Medium Enterprises (SMEs) with a variety of production types. Dealing with the significant research problem of defining a successful record-keeping system, as this is the foundation of an integrated information framework in agri-food SMEs, this research identifies and explicates the several conceptual, methodological, organizational, and technical concerns related to the data collection, processing, and recording, as well as information generation in agri-food SMEs. Two main fields of research are distinguished: the micro-level, which is related to the monitoring of agri-food SMEs, and the macro-level, which relates to the collection, processing, and collective interpretation of different types of data. The findings show how the creation of a database for all levels of analysis, primarily business analyses, followed by an analysis of the development of the agri-food sector, as a whole and by individual regions and branches, etc., constitutes the basis for the effective operation and ongoing improvement of an integrated framework for the sustainable development of agri-food SMEs. Methodologically, this study employs the system approach, system analysis, and synthesis sequence to produce business, economic, and social findings of theoretical and practicable worth to scholars, executives, and decision makers.

1. Introduction

Given that 8.9% of the world’s population experience food insecurity [1], creating a sustainable economic system in the agri-food sector is one of the biggest issues facing authorities. Sustainable development has been included in a number of worldwide and regional projects in order to transform society, reorganise markets, focus on information and technology advancements, and improve social systems.

Over the past 40 years, there has been an increase in the interest in conceptualising sustainable development and the methodological challenges associated with its evaluation [2]. According to Leyva et al. [3], the main objectives of sustainable agriculture are to: (a) improve the health of farmers and consumers (through organic farming and food security); (b) maintain the stability of the environment (through biological pest control and fertilisation techniques); (c) work to ensure long-term benefits for farmers; and (d) take into account the needs of both the present and future generations. The agri-food industry faces a struggle with sustainability because of its implications for climate change, soil erosion, water consumption, and energy use. It is also a driving force for competition and innovation [4]. It is possible to gain insight into the dynamics of resilience in agriculture by analysing human well-being [5] or yield over time [6].

There are many factors that must be taken into account when developing sustainable approaches, including the relative importance of agri-food in economies, the current level of intensification in agricultural production, and the opportunities and constraints presented by the availability of agricultural resources, as well as the needs of individuals in communities. The organisation of agriculture and the resources for advancing sustainability processes will unavoidably change in a variety of contexts. The sustainable development of the agri-food sector will require constant adjustments, innovation, and developments in tactics, legislation, and technology to help those who work in the agri-food sector to improve productivity and production.

Since it produces the vast majority of the world’s food, the agri-food sector needs to be sustainable [7]. A stronger agri-food industry is crucial for nations’ abilities to thrive sustainably, since it helps to fulfil humanity’s basic needs. Innovation is seen as essential to sustainability. However, innovation has become a lucrative opportunity for managers because it gives the agri-food sector a competitive edge and adds value to the food supply chain. Innovation has the potential to assist agri-food SMEs with a number of challenges by providing quantifiable advantages for sustainability and profitability.

The following layout is used for this paper’s structure: Section 1 introduces the investigated topic, while Section 2 describes the theoretical context and research aim. Section 3 explains the methodology utilised for the development of the integrated framework for sustainable development in the agri-food sector, and the next section (4) presents the results of this. Section 5 encompasses the discussion, and Section 6 the conclusions.

2. Theoretical Contextualisation and Research Aim

Along the agri-food supply chain, numerous innovations have been implemented to cut costs, implement new technologies, enhance food quality, develop new products, adhere to best manufacturing practices, ensure cleaner production, optimise processes, adopt lean manufacturing, extensively valorise food by-products, recycle food waste, and recover energy, etc. Bigliardi and Galanakis [8] analysed innovation classification in the food industry. They highlighted a few models for food sector innovation, concentrating on examples of food innovation driven by sustainability (such as food waste recovery and packaging materials).

The ability of agri-food enterprises to retain and improve their competitiveness is largely dependent on sustainable product innovation [9]. Numerous factors, both internal and external to the companies, have influenced the development of sustainable products in the agri-food sector. Regulations and customer demands make up a large portion of the external drivers [10], whereas internal factors refer to a company’s incentives and ability to develop, manufacture, and offer sustainable products. Examples of these internal factors include financial and human resources, technological competence, knowledge, managerial concerns, and organisational culture [11].

This has successfully encouraged manufacturing companies to reinvent their production techniques, management frameworks, and innovation capabilities. The development of a manufacturing company’s capacity for sustainable innovation is a complicated process that calls for multiple forms of collaborative digital transformation connectivity [12].

In order to integrate sustainability into their strategy and business models, organisations need to utilise open innovation to strengthen their competitive edge [13]. In an effort to address this research topic, notably, in the food industry, Bogers et al. [14] used an integrated point of view. Various approaches could be used by agri-food businesses to operate sustainably. Identifying socially conscious businesses in the food sector is an undertaking with a high level of complexity [15].

According to Ribeiro-Navarrete et al. [16], Heredia et al. [17], and Zhai et al. [18], innovations help to enhance resource allocation and lower costs. Because of improved equipment utilisation and decreased stocks, there has been a better use of resources and a decrease in capital needs. Internally, digital transformation enables businesses to achieve more effective delivery, production, organisation, and docking, while preventing needless wastes of time, people, and resources.

SMEs can embrace environmental and social practices more easily because of the adoption of lean management practices (LMP) and (SOI) sustainability-oriented innovation [19]. The main influences of intermediary success on the promotion of corporate sustainability in small and medium-sized firms, according to Quartey and Oguntoye [20], are programme restrictions, external profiles, the context of small- and medium-sized enterprises, impact strategies, and service networks. Schaltegger et al. [21] created a theoretical framework to examine co-evolutionary business model development for innovators in the sustainable niche and traditional consumer enterprises.

Research initiatives for achieving sustainability in SMEs and family-owned enterprises and the impact of the cultural and social environment on SMEs’ participation were recommended by Martins et al. [22]. Sustainable business model innovation (BMI) in the agri-food sector, in terms of its theoretical and practical approaches to sustainability, need to take in account its complexity [23].

In order to identify the key practises of sustainability, including their values, transparency, internal viewers, environment, connections with suppliers, customer and consumer interactions, and connections with the community, Schmidt et al. [24] examined the performance of SME manufacturing. To establish their growth goals, limit supply risks, and lower their overall costs, Pattanasak et al. [25] performed research on essential elements and placed special emphasis on financial resources and networking as important metrics for performance [26].

A knowledge map of the conceptual architecture of sustainability and financial performances in SMEs was provided by Bartolacci et al. [27]. Obstacles to achieving sustainability in SMEs were discovered by Jaramillo et al. [28], who categorised them “sector”, “sustainability tool”, and “internal/external”. These obstacles can be included in subsequent qualitative and quantitative investigations of the challenges in this sector. According to Vasileiou and Morris [29], sustainability aims to balance social, economic, and environmental objectives with human well-being.

Slijper et al. [30] investigated the broad patterns that show how the agri-food sector manages change, risk, and uncertainty, and they compared the business resilience across various farm types and European nations, assessing whether the features of a farm have an influence on resilience, flexibility, and transformation. As opposed to transformation, which implies an important modification to the primary objective of a business, adaptation is a producer’s ability to modify their production processes [31]. Dantsis et al. [32], Van Passel and Meul [33], and Sauvenier et al. [34] applied one of the most common methodologies used in agricultural sustainability studies based on sustainability indicators. Daskalopoulou and Petrou [35] investigated a variety of farm structures seen within a particular type of farming household. Competitiveness and profitability drive economic growth and boost income for agricultural holdings and farmers’ well-being. The agri-food sector is variable in terms of the resources and relationships between its production factors [36]. The methodology for determining the profitability in the agri-food sector is still under development [37].

The four key channels of SME innovation processes in the agri-food sector are lower communication costs, data analysis, operational transformations, and lower entry barriers. These four channels are linked to a number of transformations. According to Jung and Gómez-Bengoechea [38], these changes are linked to an improved company performance in terms of innovation, cost-cutting, and new income prospects. These changes can also lead to increased productivity and sustainability.

Castro and Chousa [39] considered that suitable tools for evaluating a company’s financial and economic situation and directing the decision making processes of businesses and financial markets should incorporate sustainability issues within their logic, under some sort of scheme or framework that permits the evaluation of a company’s sustainable management system and the impact of sustainability issues on their financial performance. According to Figurek and Vukoje [40], an appropriate approach may improve the efficiency of managing the costs in the agri-food sector. One of the primary principles of the agri-food community seems to be the potential of a united strategy with harmonized data in agri-food SMEs. Based on Rodionovna and Nastin Aleksandrovich [41], the competitiveness of agri-food businesses is influenced by the calibre of the goods produced, the costs of production, and the selling prices. This also correlates with the level of industrial efficiency and adequate framework in this sector. The agri-food sector faces a number of serious challenges:

- The growing demand for food,

- The decreasing area for cultivation due to the increasing number of inhabitants,

- The declining agricultural productivity due to the degradation of natural resources,

- The increasing market (international competition).

The above contextual analysis underlines that high-quality production and economic data are required in order to make strategic decisions in the agri-food industry. The activity of all economic entities, especially agri-food producers, depends on reliable information. Additionally, producers’ immediate access to information is crucial for them to make responsible choices, carry out their production activities, and ultimately survive and be sustainable in an increasingly competitive market. Therefore, establishing an integrated framework for sustainable development in agri-food SMEs is crucial if a higher productivity and output are to be realised, and is imperative for achieving the much desired global necessity of sustainability in this most crucial of sectors.

In this context, the creation of an appropriate methodological approach for describing the actual circumstances in agri-food SMEs is required for determining the economic, financial, technological, and other elements influencing their advancement, and therefore the development of their sustainability.

3. Methodology

This study employed the system approach [42] and the methods of system analysis [43]. A systems-based approach guards against overlooking limitations and potential synergies by improving the knowledge of the interdependencies between the important components of agri-food systems at different scales. A systematic approach, along with strategically chosen methodological concepts, was required in order to create a complete knowledge base for the agri-food sector. A system analysis and methodological procedures made it possible to segment the system down into its constituent parts, in order to examine how each component affected it.

The purpose of these methodological concepts was to identify key elements and create an integrated, conceptual framework for sustainable development in agri-food SMEs using a systematic methodology. The synthesis method was also used and divided into two basic phases. In the first phase, a selection of the relevant facts was obtained by applying the analysis method to examine the conditions and the characteristics essential for designing a record-keeping system within the integrated framework for sustainable development in the agri-food sector. In the second phase, relationships were compared and the chosen pertinent facts were integrated into a logical whole, from which it was possible to identify the crucial components for the creation of this integrated framework.

To develop the integrated framework, the comparative analysis and synthesis approaches were employed in the investigation of new conceptual and methodological solutions. There were two main stages to the synthesis process. The first regarded the collection of appropriate information, which was conducted after the analysis of the circumstances, characteristics, and other elements necessary for designing a record system. The second regarded the analysis of linkages and the integration of related information into a logical unit, from which important elements were formed that had a decisive impact on the creation of a comprehensive framework in agri-food SMEs.

The data provided by agri-food SMEs constituted the foundation of the integrated framework, and a model for gathering, storing, and analysing data was created as part of the process. The model was based on a record system (data on capacity, production structure, raw material procurement, and subsidies, etc.), with a focus on the records of costs and outcomes for specific productions. It efficiently compiled not only standard statements, but also a wide range of other analytical reports (primarily calculations based on analytical data, followed by reports on costs and outcomes by individual branches and product groups, costs by individual production stages, the profitability of particular business ventures, and data needed to optimize the production structure).

One of the most significant research goals, therefore, was to define an effective record-keeping system that could serve as the foundation for an integrated information framework in agri-food SMEs.

An Integrated Framework for Sustainable Development in the Agri-Food Sector

Information and communication technology (ICT) and economic systems are two particularly complex elements that are necessary for sustainability [44]. With the help of crucial supporting technologies such as data-driven systems, machine learning, artificial intelligence, and deep learning, Warke et al. [45] provided a framework in the field of smart manufacturing. A user could monitor, simulate, control, optimise, and spot flaws and trends within an ongoing process by developing customised and economical processes to meet client demands. Organisational characteristics, situational characteristics, technological characteristics, and individual characteristics have impacted the deployment of AI technologies by SMEs for sustainability purposes, with technological and leadership support acting as moderators [46,47].

In order to transition from a multi-dimensional strategy based on the interrelationships between input, output, and outcomes to an approach focused on evaluating the links between input and output, firms have deployed a number of communication tools [48]. In order to create new knowledge, entities need to exchange information [49]. Additionally, deliberate efforts must be made to connect science with practical decision making and its execution. Thematic analyses of the responses identified network inclusiveness, which includes value chain coverage and digital acceptance, as an additional factor to take into account for maximising the sector-wide benefits of an integrator network for digital services in agriculture [50]. Hanafizadeh et al. stated [51] that “software and programmes on the web that act as mediators between the service providers and service recipients” might be considered as technological platforms.

The prerequisite for SMEs to make quality decisions in the agri-food sector is based on adequate information about the activities and economic results that were achieved in the past period. In order for agri-food SMEs to have such information, it is necessary to have an adequate integrated framework of the information in the agri-food sector. By receiving quality information, it is possible to mitigate the risks of agri-food production. In this sense, it is necessary to monitor certain indicators that show the success of a manufacturer’s business and influence future decision making.

Finding economic, financial, technological, and other variables for the development of agri-food production, as well as its sustainability, requires the establishment of an effective methodological approach to describe the real state and outcomes of SMEs in the agri-food sector. The layout of this integral information framework (Figure 1) highlights the significance of the data integration procedure, which serves as the cornerstone of the sector’s information system. This conceptual framework may be used to describe the fundamental task of information flow analysis, in order to examine all the variables that may have a big influence on an agri-food company. The framework begins with the producer, who serves as the foundation of the entire system by choosing information sources and making judgements. The likelihood of enhancing the organisational and managerial aspects of leadership is higher if external information is integrated with internal information.

The effective utilisation of the resources at hand is a prerequisite for the survival and development of SMEs in the agri-food sector. This entails good production management that relies on the availability of reliable production and economic data on commercial events. The various techniques make use of a high-frequency data-collecting platform to disclose the complementary aspects of the link between fluctuations and well-being [52].

When combined with other production elements such as land, labour, and capital, the knowledge obtained from finished production processes may be considerably helpful for agri-food SMEs to operate more successfully. The plans’ integration of past information and estimated population numbers allows for the quality monitoring and timely modification of complex production processes in the agri-food sector.

An integrated framework that supports SMEs in developing an effective agri-food policy needs a lot of information about (a) economic forces (production volume, raw material input amounts, prices, and invested financial resources), (b) human resources (labour), and (c) natural resources (including water and climate).

Data on capacity, the volume of production, invested inputs, pricing, and internal and external realisations, etc., are the main outputs of monitoring the production activities in the agri-food sector. However, it can be difficult to make the right decisions, i.e., to choose the best alternative solutions without first analysing the production processes in agri-food SMEs. Based on previous manufacturing operations, a thorough analysis of the right alternative selections needs to be conducted. It is vital to obtain both natural and financial data on production activities in order to analyse the actualised operations. In this regard, it is important to implement the proper business-tracking procedures and include them when documenting production activities and their outcomes. The major goal of the previously described idea is to improve the agri-food sector’s efficiency, in order to encourage the sustainable development of SMEs in this sector.

4. Results

For the purpose of building an information framework to determine production methods, it is crucial to document business events. The planning of production operations and decision making are both essential for the proper development of the production cycle. Due to ignorance about the right approach to documenting these business events, producers have some difficulty in delivering the essential information. In agri-food SMEs, where management functions (organising, realising, and controlling) are frequently the responsibility of one person, whose primary purpose is to ensure sustainable production, the task of documenting business events must also be carried out, but this is often overlooked.

Record-keeping is a methodical process for keeping track of the daily data on agri-food SMEs’ operations, including financial and production data. Records demonstrate the overall sustainability and financial success of an individual business. These data identify the agri-food sector’s strong and weak points and provide an overview for making strategic decisions.

The layout of the form is intended to include all the crucial details about agri-food SMEs, including their members, the total area and structure of the agricultural land they own and lease, their facilities, their long-standing plantations, the machinery and equipment owned by the producer, their crop and vegetable crops, the number of animals, products, and activities that earned money for the SMEs in a particular year, and their farm liabilities. The major goal is for management to use this information to obtain insight into the business operations of agri-food SMEs. Consequently, in addition to analytical information about their available funds, it is necessary for SMEs to include the financial aspects of their business (the value of their resources, the value of their production and other operations from which the SMEs have produced income, their annual costs, their amount of subsidies, and other recognised income). The costs of all hired or purchased inputs utilised in their production during the course of a year are included in their operating expenditures.

The nature and scale of production dictate the financing requirements. Additionally, according to Barry and Ellinger [53], the following distinguish agri-food finance from other economic sectors:

- relatively small businesses, but with developing integration,

- a significant proportion of capital resources, such as land, buildings, and equipment,

- extended and biologically driven production cycles,

- a greater reliance of smaller production units on non-farm revenue,

- finance that is relationship-driven but information-intensive,

- an emphasis on food products as opposed to commodities,

- a reliance on international exports and environmental awareness.

Having adequate records that give an overview of the consumption and planned purchases of basic raw materials is necessary in order to monitor the costs associated with production processes and the quantities that need to be fully or continuously procured. Without these details, the production process cannot be fully realised.

Obtaining information is a challenging task, since it is essential to gather data through sufficient recordings, displays, and processing [54]. The appropriateness of records is shown not only by the business actions or events that have been carried out, but also by the monitoring, research, analysis, and control of the production process, and by the results of their effective implementation. This article presents the process of recording that is required for the ongoing collection of both quantitative and qualitative data.

4.1. System-Based Approach to Record-Keeping

The International Institute for Sustainable Development quantifies and simplifies aspects that are difficult to comprehend into a reasonable quantity of relevant information, which can be used to make judgements and decisions [55]. This is even more essential in the food industry due to the perishable nature of the items and the requirement for making immediate selections. By applying the appropriate technology, managers may monitor product flow, help with data analysis, and make timely decisions to boost productivity and achieve a higher output that will benefit end-users [56]. In order to facilitate decision making and problem solving, management frequently implements a variety of procedures. Production will benefit from close monitoring, a longer period of storage, and an improved comprehension of the supply demand cycle for goods delivery.

The conceptual Sustainability Green Industry 4.0 (SGI 4.0) framework aids in the structuring and evaluation of traditional green processes, in connection to Industry 4.0 and sustainability. This includes determining which technologies (big data, cyber-physical systems, the Industrial Internet of Things, and smart systems) and green processes (logistics, manufacturing, and product design) are essential for reaching a greater degree of sustainability [57]. Müller et al. [58] investigated the relevance of Industry 4.0-related opportunities and challenges as drivers for Industry 4.0 implementation in the context of sustainability, taking a differentiated view on varying company sizes, industry sectors, and companies’ roles. The elements of Industry 4.0, such as big data, the Internet of Things, and smart factories, have favourable roles in increasing information technology (IT) deployment, which adds to long-term sustainability [59].

To achieve long-term profitability and sustainable production, agri-food producers should have the ability to manage their production processes and distribution. The changing economic circumstances associated with agri-food production are usually unexpected and cannot be significantly modified. Therefore, every activity in the agri-food business must be well planned, structured, and directed towards its goal. Due to this dynamism and unpredictability, high levels of knowledge and preparation are needed to find effective solutions for adjusting the production processes in agri-food SMEs to new circumstances. Hence, knowledge management and acquisition are essential for an agri-food business to completely develop a competitive advantage.

Biological processes that affect the activities for increasing production are what give rise to the unique characteristics that define the agri-food sector. These specificities limit the ability of agri-food producers to register and record the business changes that occur throughout their operations and affect the economic outcomes of some types of agri-food production. This is why collecting data during agri-food operations is more difficult than with other activities, and it is vital to adapt the current data management systems to the unique requirements of the agri-food sector.

Data collection is a painstaking process that calls for maintaining accurate records and displaying and processing data. The appropriateness of these records can be seen not only in business events or realised actions, but also in the monitoring, research, analysis, and control of the production process and its results. Both in terms of the extent and calibre of the data gathered, the official statistical method for monitoring corporate holdings is unsatisfactory. Adopting an approach that enables the ongoing monitoring of the financial and production metrics of agri-food SMEs is therefore important.

In order to identify the economic, technological, and other elements that will enhance the business sustainability of agri-food SMEs, it is essential to use the right scientific approach, which takes into consideration real situations and outcomes. To have the sufficient knowledge to make business decisions in this sector, SME agri-food producers are required to continually document all their business operations. The availability of essential information is necessary to ensure consistency between the decision making process and the anticipated outcomes that result from the choices made.

Manufacturers therefore need to carefully monitor their business activities and document all their production-related business actions in an event log (Figure 2). The phases involved in documenting these economic occurrences are as follows:

- Gathering information and entering it into the relevant fields in the worksheet,

- Indicating the date when revenue was obtained or when products were realised, and including the expenses of the inputs used in the productive activities,

- Making notes to explain the actions taken in the event, where a more thorough presentation is required to produce recorded data of a better calibre.

The management of production operations, the planning of upcoming production activities, and decision making procedures all depend on daily the record-keeping of business events. Producers can evaluate the effectiveness of their actualised production procedures by using accurate information. The potential of creating a report based on these data that provides an overview and analysis of the economic repercussions of particular types of production would significantly aid in the planning of future business operations.

These data are also essential for producers to identify the elements that contribute to decreased outputs and negative economic outcomes. With quality records that give thorough details about the inputs and outputs of production, it is possible to identify the critical points or problems that arise in production activities and to adopt corrective measures. It is crucial that recording data on business operations is based on a consistent methodology that is supported by trustworthy and organised documentation. Business operation records are an organised depiction of the business processes that occur in agri-food SMEs during a specific time period. The proposed methodology requires four types of records, which are:

- The available capacity,

- The production costs of crops and livestock,

- The plant and animal products,

- The accounts, credits, debits, and payments, etc., received.

These records may be used to build reports on certain cost categories of the activities carried out, the number of working hours devoted to each sort of production, suppliers, and clients, etc.

These data serve as the foundation for creating a summary report that includes information on crop or livestock outputs, monthly evaluations of spent concentrate, labour hours, and the sales of harvested plants and animal products, among others. The financial components (the value of the assets, the value of production and other activities from which the household income was created, the costs, the amount of subsidies, and other realised revenue) must be included, in addition to quantitative information on the resources that are accessible.

4.2. Crop Production

A summary record of crop files includes quantitative information on the stocks at the beginning of the period, the area seeded, the total production price, the average yield per hectare, and, of course, the total value of the outputs generated, or the production of the crops represented on the holding. The basis for deciding potential changes in the upcoming period will be provided by an overview of the used arable land in one location and the average yields (in terms of increases or decreases in the area under crops with yields that are higher or lower than anticipated, or compared to the yields of earlier years). It is vital to enter these data in the logbook in a chronological sequence when business events occur, such as the purchase of plant materials and labour payments. This method makes it feasible to obtain monthly sub-sums.

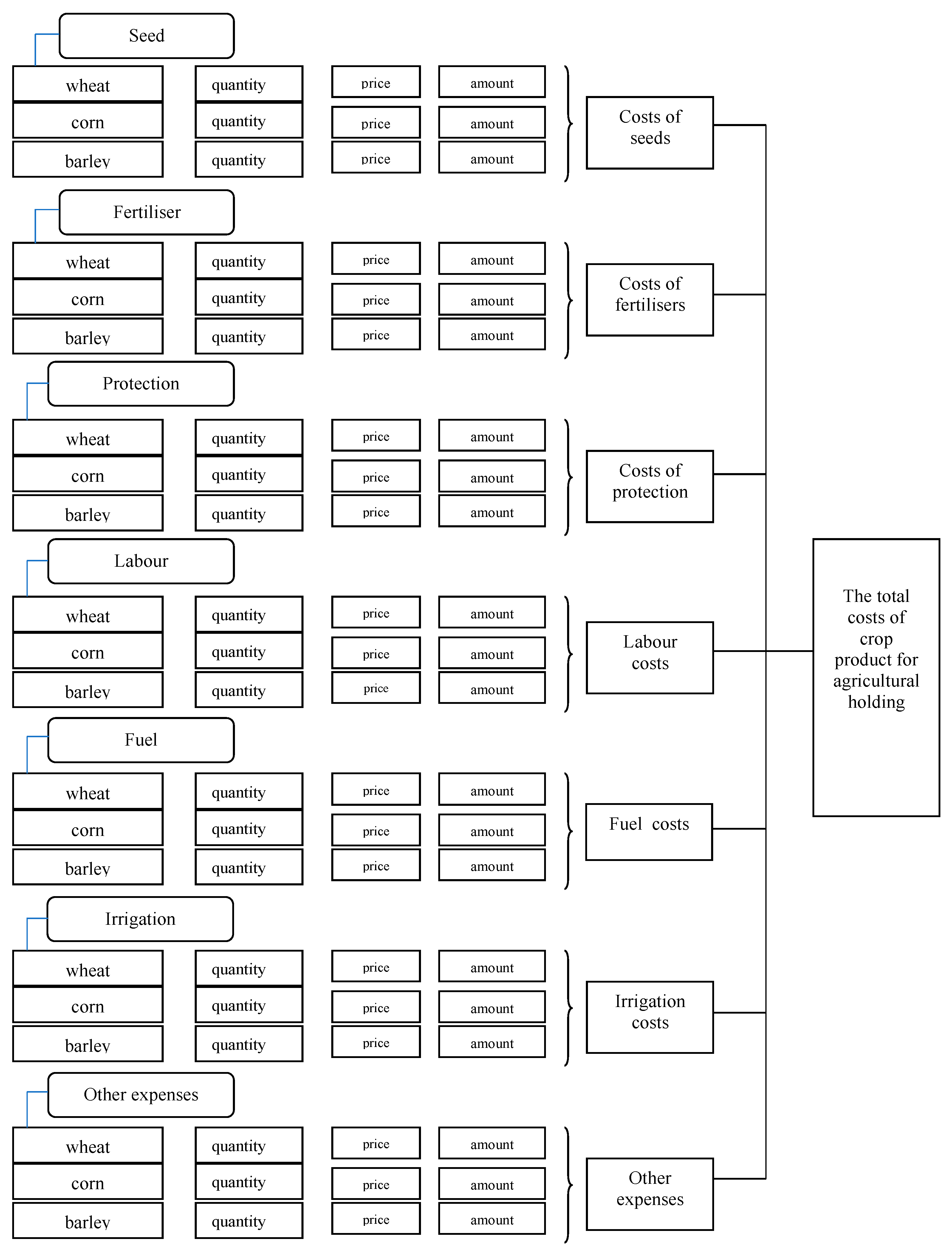

It is necessary to keep track of all materials and inputs (seeds, fertilisers, organic fertilisers, and protection), as well as the labour costs of non-farm employees, in order to increase the farm’s efficiency, to obtain timely information on the financial outcomes of individual production lines, and to calculate their gross margins. With a need to specify the type of fertiliser (NPK, UREA, KAN, or other fertilisers), seeds, protective equipment, and hired labour used, specific sections of the table regarding the inputs invested in crop production are made with the intention of recording data on the mineral fertiliser used separately for each crop. This part also includes information on the costs of fertiliser, seeds, and protective agents, etc., in addition to data on their raw material quantities (Figure 3).

4.3. Livestock Production

Producers may find out more about their inputs, including the purchase of concentrated and other feed, the purchase of animals, and the number of working hours or working days of hired labour, by keeping an eye on the business activities involved in the manufacture of livestock products. Instead of relying on generalised projections of the farm’s performance, such knowledge is crucial for creating realistic budgets for future sustainable initiatives. When recording business events in the log book, it is necessary to be more specific about what kind and category of livestock these were for, for example, the purchase of concentrate, if more than one type of livestock production is represented in the holding. Additionally, in the category of other costs, it is necessary to specify whether veterinarian costs were incurred as a result of the treatment of a specific number of heads in fattening pigs or the fattening of other animals, etc., in order to perform a qualitative analysis of all types of production.

It is essential for producers to maintain proper records of animal categories, weight, pricing, amount sold, home consumption, and mortality, in order to efficiently implement business operations linked to livestock production and monitor the economic impacts of the actions conducted. The production and economic activities related to pig production have to be recorded separately for farming enterprises that also raise pigs. Farmers must keep track of the progression of each respective category of livestock with respect to their higher categories based on the production they are managing, in order to always have a clear picture of the current and anticipated expenditures and income.

Data on variations, in terms of increases and decreases in the number of heads, are also needed for a producer’s analysis. Changes resulting in a decrease in the number of cattle include sales, moving into a higher category, slaughter, consumption within the household, and death. Both quantitative and value-based data should be kept track of for these changes. In order to assess the economic impacts of the many livestock production types owned by the holding, separate records must be kept for each type.

The primary inputs in livestock production include food and nutritional supplements, which are correlated with the yields attained. If the growth is found to be inappropriate, it is imperative to act quickly and alter the composition, or at least some components, of the feed rations. This information is obtained by comparing the composition of the nutritional rations and the production or growth over the proper period of time.

By correctly recording the food consumed, it is possible to take the composition of this food into consideration when comparing weight increases or milk outputs. It is important to have proper knowledge on the prior make-up of these nutritious meals before opting to alter their structure or quantity.

Because of this, it is crucial for farmers who raise animals to record the compositions of the rations used. Financial considerations should undoubtedly be taken into account, which means that the units and total values must be recorded. The system has to be segmented depending on production units, such as different types of crops, animals, and other expenditure categories [60].

4.4. Identifying the Location of Costs

The recording of economic events on farms must be approached seriously and responsibly by agricultural producers, given that each type of agricultural production represents a complex system with unique dynamics of its production activities and input investments on the one hand, and the realisation of its outputs on the other. A constant record is required of the quantitative and value indicators that relate to the invested inputs and realised outputs for each type of agricultural production, if the objective is to maintain the production level already attained or to raise it. Agricultural producers must devote some time to these tasks, since they often forget to keep track of their farm’s business activity when performing specific seasonal tasks.

Using agricultural production as an example, the next step in this decision making should be with information on: (1) the areas intended for agricultural production; (2) the yield achieved in previous years; (3) the prices of the raw materials or inputs; (4) the issues that have led to low yields; and (5) the market rates and sales for specific agricultural crops.

Planning and organising subsequent production activities requires different types of knowledge. For example, the producer must know about agricultural production, which refers to the quantity produced or the yield. The producer must also understand the dynamics of investment, or the consumption of inputs, starting with the amount of seeds, fertilisers, and protective agents. Knowledge of the time invested by formal and informal workers is also important.

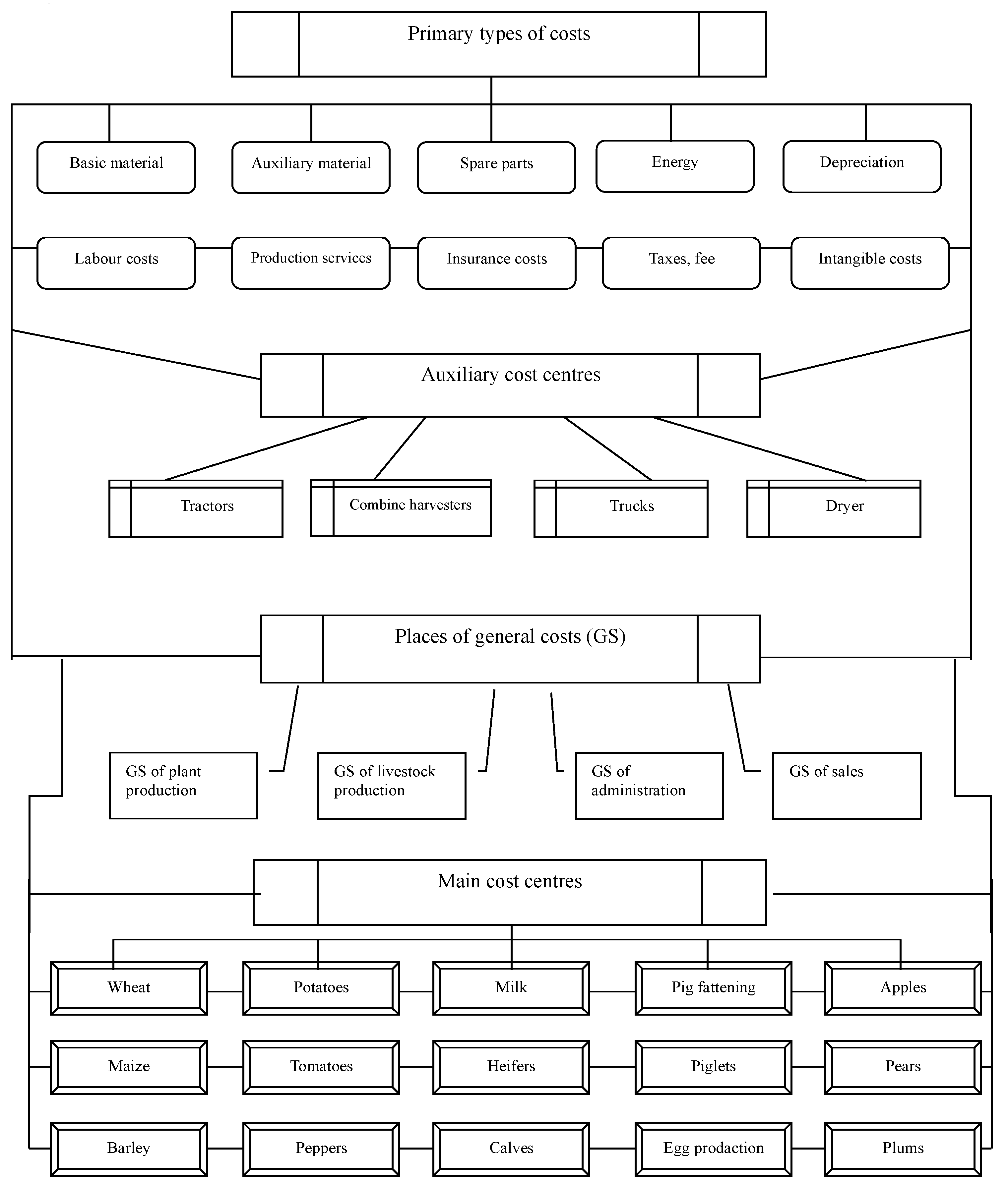

Due to the presence of several forms of agricultural outputs, heterogeneous or mixed agricultural farms require a more sophisticated approach when it comes to assessing and determining the outcomes of their overall operations. Depending on their type of agricultural output, these farms generate a variety of agricultural products and consume a variety of inputs, all of which must be properly recorded. Agricultural producers must participate more actively in the creation of an integrated framework for sustainable development. This includes keeping more detailed records of the inputs they use, as well as the products they actually create, according to their kind of production. Given the significant contribution of mixed farms or farms with multiple lines of agricultural production, it is necessary to track the costs from where they were incurred. Due to the concurrent expansion of several productions, agricultural farms have more cost centres. According to the method of inclusion, the cost centres in the agriculture sector can be classified into three groups: main, auxiliary, and general cost centres (Figure 4). The grouping of costs by location actually represents the breakdown of the total costs into these three groups of cost locations (MT). Of course, the most significant are the main costs (individual production lines), and depending on the size and type of the farm, auxiliary and general costs appear.

Individual lines of production (corn, wheat, potatoes, plums, milk production, and pig fattening, etc.) represent the main areas of costs, i.e., they include the costs of basic activities, especially for plants (e.g., arable land, fruit production, viticultural, and vegetable production) and livestock production (e.g., milk production, pig fattening, and egg production). Direct costs are linked to the main location, i.e., the production line to which they refer, while indirect (auxiliary and general) costs are allocated to the main cost locations in the following stages. In the final effect, all the costs end up in the main cost centres, upon the basis of which analytical calculations are later made. Without placing the records of these agricultural costs in the right location, it is not possible to precisely calculate these costs. As the agricultural economy represents a production system that is made up of several subsystems, i.e., production lines, which have impacts on its operations, it is necessary to analyse all the individual lines and look at how they participate in the achieved results.

4.5. Recording and Calculating Direct and Indirect Costs

The costs of individual products should be divided into either direct or indirect costs and then transferred to the appropriate cost bearers. Identifying the occurrence of individual costs according to the lines of production and allocating them properly is the goal of creating realistic and high-quality calculations for individual productions, i.e., cost bearers. Recording these costs is also performed in the appropriate rows and columns of the logbook, which indicate the individual cost centres.

The costs of the materials used for production, which, according to actual consumption, can be charged as a whole to individual lines of production (seeds, fertiliser, fodder, and fuel, etc.) are considered to be direct costs. Additionally, included under direct costs in agriculture are those related to individual crops and livestock, such as species, breeds, or categories of livestock.

Unlike direct costs, indirect costs are determined indirectly, and, in the structure of the calculation, they represent the corresponding part of the common costs for several lines of agricultural production. Indirect costs include the costs of the auxiliary and general cost centres. The costs of auxiliary MT (tractors—possibly by category, harvesters, feed mixers, irrigation systems, and dryers, etc.) are, as a rule, very significant for agricultural farms and they depend on the scale and structure of the production.

The categories of expenses include those that arise from the performance of the general farm management, e.g., production planning, sales, and accounting. In addition, this category includes the largest part of the overhead costs (electricity, water, tax, heating, and telephone). In addition, indirect costs arise from the use of common resources, work items, and labour in the execution of production activities (farm machinery, mixing fodder, means of transport, and irrigation systems). The value of the costs incurred upon this basis is determined within the total amount and indirectly distributed to certain lines of agricultural production. Recording plant products is useful for crop use planning.

Crop use planning involves first recording the existing stocks and the expected production, so that agri-food producers can apply these data to plan how to use the crops that will be produced (for livestock feed, sale, household consumption, storage, or compensation for other products or services, etc.).

It is necessary to include a column in the form that allows a view, at any moment, of the state of a particular product, and thus, in a timely manner, allows the producer to notice the need to repurchase it. This record can also serve for products or materials that are not only produced, but also bought, sold, and used on the farm (which could be straw or animal feed, etc.). This record is necessary for each product or material. Farms that have multiple lines of plant production need to keep an ongoing record of their use of plants, with the aim of monitoring quantitative and valuable data on their production.

4.6. Recording the Realisation of Livestock Products

In the section of the event log that is meant to capture information about livestock products, it is crucial to chronologically define the value structure of the animal and livestock product sales. The planning of production activities, especially for purchasing animals or enhancing outputs, benefits greatly from the examination of revenue sources and their timing. When it is necessary to allocate sufficient revenue to periods that require more financial investment, one must identify if these investments are more than the revenues and if it is essential to borrow money. The sales of livestock and livestock-related goods need to be recorded, including not only their quantitative data, but also their selling prices, in order to understand the realised revenues.

Daily records of the amount of milk produced and its selling price should be kept, as should the aforementioned quantitative and price data extracted from the logbook of business events in the section pertaining to the sale prices of livestock products. Their values are added up each month and distributed to the proper final forms. Applying the calculated value of the delivered milk without a premium and the amount of milk sold results in the calculation of the average price of milk. Planning production operations benefit greatly from the examination of revenue sources and their timing, particularly if intending to procure livestock or expand their outputs.

4.7. Recording the Achieved Results

It is necessary to conduct a thorough analysis of the functional relationship between production inputs and the outputs or values obtained. This section provides an overview of the expenses associated with manufacturing processes and the income produced by the investment of inputs in these processes. Basic information on the amounts of plant and animal product production, their usage structures, their sale quantities, their prices, and their total values, etc., are included in the records. The following categories were created based on the structure of the costs that result from the realisation of business operations on a farm:

- the expense of labour and mechanisation

- the cost of raising animals

- the cost of raising plants

- overheads

- insurance premiums

- taxes and other fees

- land-use expenses

The components of each of these categories are provided in the diagram below. For instance, the expenses of plant production include the costs of the seed and planting supplies, fertilisers and soil treatments, and crop protection and maintenance goods.

In order to examine the fundamental components of these costs, determine the cost prices, and identify the processes where specific issues develop, documenting and monitoring the costs that result from the realisation of successful, sustainable production processes are key objectives. Agri-food policies in a market economy heavily rely on the cost analyses and cost pricing of agricultural outputs (Figure 5). Cost prices are an objective economic indicator, whose in-depth research offers important details on both the quantitative and qualitative indicators that are relevant to a specific agricultural output.

The agri-food sector is subject to new demands regarding the accuracy and integration of the planning and management of its production operations, as a result of the advancement and improvement in its techniques and technology [61,62,63], all with the goal of enhancing sustainable development. It is vital to consider the variables that may lower the anticipated yield before beginning the planned production activities, i.e., the outcomes of the operations (verifying the accuracy of mechanisation, biological circumstances, and climatic conditions, etc.). Additionally, rising electricity prices, along with sustained high demand, began to erode producers’ finances [64].

5. Discussion

Innovations are undoubtedly crucial resources throughout sustainability transitions, which provide a valuable framework for exploring how to make innovation policies more successful [65]. The significance of an innovation system stems from the wide range of interactions required for every organisation to innovate [66]. The idea of a national system of innovation might be helpful as a tool for analysis and the fostering of sustainable economic growth and wellbeing [67]. Systems of innovation have been recognised as beneficial analytical tools for better understanding innovation processes, as well as the creation and dissemination of information and knowledge in the economy [68]. Sustainable development is dependent on organisations, institutions, and policies that strive to generate and improve wealth in ways that ensure long-term environmental, social, and economic well-being [69,70].

To determine whether a country’s or sector’s development has been sustainable over time, it is necessary to estimate the changes in its inclusive wealth and institutions over a time period. Changes in knowledge and institutions across time are reflected in changes in total factor productivity (TFP) [71]. That way, it is important to collect information from SMEs in the agri-food sector, in order to estimate the value of the changes in the amounts and compositions of manufactured, human, and natural resources.

Manioudis and Meramveliotakis [72] offered three methodological and analytical concepts that should be at the heart of every study aimed at achieving sustainable development:

- -

- First, any thorough examination of the concept of development should distinguish between two levels of study. The goal of these examinations is to understand the historical phases of socio-economic systems. Under such a theoretical framework, the concept of development serves as a “transhistorical category” that is relevant to all types of socioeconomic systems.

- -

- The second principle relates to the importance of past development studies, because “history matters” in determining development trajectories.

- -

- The third premise is attributed to the examination of sustainable development, including the fundamentally multidisciplinary character of development studies. A more thorough comprehension of the various elements that impact, alter, and accelerate human development, such as economic, political, institutional, and cultural aspects, necessitates a theory that focuses on these different elements.

The agri-food industry is a complex production system comprising specific commercial activities, i.e., processes of matter, energy, and information transformation. To assess the production outcomes and sustainable development of these production processes, approaching the measurement of the activity inputs and outputs is required, taking into account the diversity of the production types in this sector.

The capacity to successfully encourage agri-food SMEs producers to achieve sustainable development and higher production requires obtaining information at the micro level. At the same time, the latter will support improved outcomes at the macro level, meaning that each synergistic impact will affect how the agri-food sector develops as a whole. The collaboration and exchange of information across government organisations, companies, agencies, and other stakeholders in the agri-food sector encourage manufacturers, the government, and the responsible ministry to be better informed and address issues as they arise (Figure 6).

The fundamental aspects of the concept, i.e., the operation of the Integrated Framework for Sustainable Development in agri-food SMEs, are as follows:

- -

- A central government institution, e.g., the Ministry of Agriculture and/or the Ministry of Industry, constitutes the “roof” institutions that monitor the operation of the Integrated Framework.

- -

- Scientific research institutes, which are entrusted with organising the processes of gathering data, analysing them, examination, and presentation, as well as the continuous improvement in the integrated framework’s operation. Processed data, or information, are sent to the central government institution, e.g., the Ministry of Agriculture and/or the Ministry of Industry, where they are used to gain insight into the operations of SMEs and develop appropriate agri-food policy initiatives.

- -

- Agri-food SMEs should maintain records, i.e., engage in data collection.

Limitations and Suggestions for Future Research

The integrated framework provides a broad range of data, including details on the structure, type of production, quantity produced, its value, the inputs used, price, employment of the labour force, and both internal and external product realisations.

To ascertain the advantages of the presented methodological solutions, that is, to verify their validity, it is essential to test the integrated framework at the micro and macro levels. Taking into consideration their size, type, and territorial dispersion, the integrated framework should be evaluated at the micro and macro levels on representative samples of agri-food SMEs, which are characterised by extremely varied outputs. Following this, a special database of the gathered data must be created, serving as the foundation for the additional processing and analysis of the sustainable development of agri-food SMEs.

To achieve adequate data quality, future research needs to investigate the following significant potential barriers:

- -

- Insufficiently coordinated institutional mechanisms for gathering quantitative and qualitative data.

- -

- A key issue in terms of ensuring the quality of these data is inadequate logistical and technical assistance, combined with poor monitoring.

- -

- An incomplete or delayed data set.

- -

- A low level of data utilization by agri-food producers.

- -

- An inadequate approach when analysing the collected data.

The integrated framework aims to support the sustainable development of agri-food SMEs and the entire agri-food sector in a systematic and comprehensive way through an analysis of the outcomes of agri-food SMEs.

It also indicates that every participant involved in this sector will be associated in building a comprehensive database. A solid foundation for decision making may be offered by integrating data from multiple sources with data generated by the outcomes inside agri-food SMEs. Manufacturers can improve their future operations and timely coordinate production activities through the process of integrating internal and external data sources.

This paper’s limitation relates to the significant amount of data that the system of records define, as well as the possibility that they will be observed from the viewpoint of a number of institutions, whose recommendations and actualization might limit the sustainable development of agri-food SMEs. Therefore, future research should also be focused on the information flows between defined stakeholders in the agri-food sector.

6. Conclusions

This article’s study focused on the theoretical, conceptual, and methodological aspects of constructing an integrated framework for fostering sustainable development in agri-food SMEs at the micro and macro levels. In doing so, two main fields of research were distinguished: the micro level, which refers to record creation and information development inside agri-food SMEs, and the macro level, which should enable information collection, processing, and summarizing based on various types of production.

The foundation for the efficient operation and ongoing development of the Integrated Framework for Sustainable Development in agri-food SMEs is the creation of a database for the needs of analyses at all levels, primarily the analysis of the business of agri-food SMEs and their sustainable development, followed by the analysis of the development of this sector as a whole, and the effects of specific agri-food policy measures.

Due to the responsibility of making decisions within their production operations, SMEs in the agri-food sector require daily data on the amount of resources spent for each production cycle on the one hand, and their realised business outcomes on the other. Monitoring production processes, such as the specific operations and costs associated with these production processes, can help with the control or management of SMEs and in achieving their sustainable development. Future decisions made in the field are crucial for the planning and control of production operations and should therefore be treated with care.

Making the right judgements is a constant, iterative process, during which, one is required to recognise possible issues and approach the development and analysis of prospective solutions, especially when they relate to specific interventions for certain types of production. Producers can obtain insight into their production potential and a better understanding of the indications that show the success or failure of their previously realised production activities by implementing higher levels of organisation in these production activities. With this strategy, their manufacturing processes are better controlled and there are better chances to produce agri-food products of a higher quality and obtain a larger market share.

Different stakeholders in the agri-food sector will benefit through an array of advantages stemming from the creation of the Integrated Framework for Sustainable Development in agri-food SMEs, including:

- -

- Primarily, producers will achieve better decision making and, consequently, more efficient operations, through a variety of production and financial data on their business operations obtained in the form of various reports (derived success indicators, a number of other analytical reports on assets, liabilities, costs, and results, etc.);

- -

- Reliable data will be made available for providing appropriate economic advice;

- -

- The ministry of industry and agriculture and other state institutions will have an accurate database for implementing suitable kinds of incentives and developing/sustaining measures of the agri-food policy as a whole;

- -

- The professional associations of manufacturers in the agri-food sector (chambers and clusters, etc.) will have a strong information foundation for recommending measures and carrying out operations aimed at improving the economic position of the SMEs involved in the process;

- -

- The integrated framework will allow for advancements in the research and staff development, etc., of scientific and educational institutes and organisations.

The agri-food sector, overall, needs both production and economic data on its company operations to define acceptable measures and build future policies. The ability to access the aforementioned categorized data is a crucial resource for those in charge of formulating policies and achieving the objectives of agri-food SMEs.

An integrated framework for sustainable development in agri-food SMEs with a variety of production types has the potential to boost activity and procedural efficiency and timeliness, as well as achieve information correctness and consistency. This framework includes specifically defined dynamics for the collection, handling, analysis, and flow of quantitative and qualitative information.

Author Contributions

Conceptualization, A.F. and A.T.; methodology, A.F. and A.T.; resources, A.F. and A.T.; writing—original draft preparation, A.F. and A.T.; writing—review and editing, A.F. and A.T.; visualization, A.F. and A.T. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

FADN database.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Sachs, J.; Schmidt-Traub, G.; Kroll, C.; Fuller, G. Sustainable Development Report: The Sustainable Development Goals and COVID-19; Sustainable Development Solutions Network. 2020. Available online: https://www.sdgindex.org/reports/sustainable-development-report-2020/ (accessed on 20 December 2022).

- Dabkiene, V. Scope of farms sustainability tools based on FADN data. Econ. Eng. Agric. Rural Dev. 2016, 16, 121–128. [Google Scholar]

- Leyva, D.; De la Torre, M.; Coronado, Y. Sustainability of the Agricultural Systems of Indigenous People in Hidalgo, Mexico. Sustainability 2021, 13, 8075. [Google Scholar] [CrossRef]

- Capitello, R.; Sirieix, L. What does ‘sustainable wine’ mean? An investigation of French and Italian wine consumers. In Social Sustainability in the Global Wine Industry; Forbes, S., De Silva, T.A., Gilinsky, A., Jr., Eds.; Palgrave Pivot: Cham, Switzerland, 2020; pp. 137–154. [Google Scholar]

- Barrett, C.B.; Constas, M.A. Toward a theory of resilience for international development applications. Proc. Natl. Acad. Sci. USA 2014, 111, 14625–14630. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Chavas, J.P. Adverse shocks in agriculture: The assessment and management of downside risk. J. Agric. Econ. 2019, 70, 731–748. [Google Scholar] [CrossRef]

- Kamali, F.P.; Borges, J.A.R.; Meuwissen, M.P.M.; de Boer, I.J.M.; Oude Lansink, A.G.J.M. Sustainability Assessment of Agricultural Systems: The Validity of Expert Opinion and Robustness of a Multi-Criteria Analysis. Agric. Syst. 2006, 157, 118–128. [Google Scholar] [CrossRef]

- Bigliardi, B.; Galanakis, C.M. Innovation management and sustainability in the food industry: Concepts and models. In The Interaction of Food Industry and Environment; Galanakis, C., Ed.; Academic Press: Cambridge, MA, USA, 2020; pp. 315–340. [Google Scholar]

- Aibar-Guzman, B.; García-Sanchez, I.M.; Aibar-Guzman, C.; Hussain, N. Sustainable product innovation in agri-food industry: Do ownership structure and capital structure matter? J. Innov. Knowl. 2022, 7, 100160. [Google Scholar] [CrossRef]

- Ilg, P. How to foster green product innovation in an inert sector. J. Innov. Knowl. 2019, 4, 129–138. [Google Scholar] [CrossRef]

- Hilmersson, F.P.; Hilmersson, M. Networking to accelerate the pace of SME innovations. J. Innov Knowl. 2021, 6, 43–49. [Google Scholar] [CrossRef]

- Fan, X.; Wang, Y.; Lu, X. Digital transformation drives sustainable innovation capability improvement in manufacturing enterprises: Based on FsQCA and NCA Approaches. Sustainability 2023, 15, 542. [Google Scholar] [CrossRef]

- Venturelli, A.; Caputo, A.; Pizzi, S.; Valenza, G. A dynamic framework for sustainable open innovation in the food industry. Br. Food J. 2020, 124, 1895–1911. [Google Scholar] [CrossRef]

- Bogers, M.; Chesbrough, H.; Strand, R. Sustainable open innovation to address a grand challenge: Lessons from Carlsberg and the green fiber bottle. Br. Food J. 2020, 122, 1505–1517. [Google Scholar] [CrossRef]

- Ehgartner, U. The discursive framework of sustainability in UK food policy: The marginalised environmental dimension. J. Environ. Policy Plan. 2020, 22, 473–485. [Google Scholar] [CrossRef]

- Ribeiro-Navarrete, S.; Botella-Carrubi, D.; Palacios-Marqués, D.; Orero-Blat, M. The effect of digitalization on business performance: An applied study of KIBS. J. Bus. Res. 2021, 126, 319–326. [Google Scholar] [CrossRef]

- Heredia, J.; Castillo-Vergara, M.; Geldes, C.; Gamarra, F.M.C.; Flores, A.; Heredia, W. How do digital capabilities affect firm performance? The mediating role of technological capabilities in the “new normal”. J. Innov. Knowl. 2022, 7, 100171. [Google Scholar] [CrossRef]

- Zhai, H.; Yang, M.; Chan, K.C. Does digital transformation enhance a firm’s performance? Evidence from China. Technol. Soc. 2022, 68, 101841. [Google Scholar] [CrossRef]

- Dey, P.K.; Malesios, C.; De, D.; Chowdhury, S.; Abdelaziz, F.B. Could lean practices and process innovation enhance supply chain sustainability of small and medium-sized enterprises? Bus. Strategy Environ. 2019, 28, 582–598. [Google Scholar] [CrossRef]

- Quartey, S.H.; Oguntoye, O. Promoting corporate sustainability in small and medium-sized enterprises: Key determinants of intermediary performance in Africa. Bus. Strategy Environ. 2020, 29, 1160–1172. [Google Scholar] [CrossRef]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business models for sustainability: A co-evolutionary analysis of sustainable entrepreneurship, innovation, and transformation. Organ. Environ. 2016, 29, 264–289. [Google Scholar] [CrossRef]

- Martins, A.; Branco, M.C.; Melo, P.N.; Machado, C. Sustainability in small and medium-sized enterprises: A systematic literature review and future research agenda. Sustainability 2022, 14, 6493. [Google Scholar] [CrossRef]

- Barth, H.; Ulvenblad, P.O.; Ulvenblad, P. Towards a conceptual framework of sustainable business model innovation in the agri-food sector: A systematic literature review. Sustainability 2017, 9, 1620. [Google Scholar] [CrossRef] [Green Version]

- Schmidt, F.C.; Zanini, R.R.; Korzenowski, A.L.; Schmidt Junior, R.; Xavier do Nascimento, K.B. Evaluation of sustainability practices in small and medium-sized manufacturing enterprises in Southern Brazil. Sustainability 2018, 10, 2460. [Google Scholar] [CrossRef] [Green Version]

- Pattanasak, P.; Anantana, T.; Paphawasit, B.; Wudhikarn, R. Critical factors and performance measurement of business incubators: A systematic literature review. Sustainability 2022, 14, 4610. [Google Scholar] [CrossRef]

- Mani, V.; Jabbour, C.J.C.; Mani, K.T.N. Supply chain social sustainability in small and medium manufacturing enterprises and firms‘s, performance: Emprimical evidence from an emerging Asian economy. Int. J. Produc. Econ. 2020, 227, 107656. [Google Scholar] [CrossRef]

- Bartolacci, F.; Caputo, A.; Soverchia, M. Sustainability and financial performance of small and medium sized enterprises: A bibliometric and systematic literature review. Bus. Strategy Environ. 2019, 29, 1297–1309. [Google Scholar] [CrossRef]

- Jaramillo, J.A.; Sossa, J.W.Z.; Mendoza, G.L.O. Barriers to sustainability for small and medium enterprises in the framework of sustainable development—Literature review. Bus. Strategy Environ. 2019, 28, 512–524. [Google Scholar]

- Vasileiou, K.; Morris, J. The Sustainability of the Supply Chain for Fresh Potatoes in Britain. Supply Chain Manag. 2006, 11, 317–327. [Google Scholar] [CrossRef]

- Slijper, T.; Mey, Y.; Poortvliet, M.; Meuwissen, M. Quantifying the resilience of Euroopean farms using FADN. Eur. Rev. Agric. Econ. 2022, 49, 121–150. [Google Scholar] [CrossRef]

- Darnhofer, I. Resilience and why it matters for farm management. Eur Rev. Agric. Econ. 2014, 41, 461–484. [Google Scholar] [CrossRef]

- Dantsis, T.; Douma, C.; Giourga, C.; Loumou, A.; Polychronaki, E.A. A methodological approach to assess and compare the sustainability level of agricultural plant production systems. Ecol. Indic. 2010, 10, 256–263. [Google Scholar] [CrossRef]

- Van Passel, S.; Meul, M. Multilevel and multi-user sustainability assessment of farming systems. Environ. Impact Assess. Rev. 2012, 32, 170–180. [Google Scholar] [CrossRef]

- Sauvenier, X.; Valckx, J.; Van Cauwenbergh, N.; Wauters, E.; Bachev, H.; Biala, K.; Hermy, M. Framework for Assessing Sustainability Levels in Belgian Agricultural Systems—SAFE; Part 1: Sustainable Production and Consumption Patterns. Final Report—SPSD II CP 28; Belgian Science Policy: Brussels, Belgium, 2005. [Google Scholar]

- Daskalopoulou, I.; Petrou, A. Utilising a farm typology to identify potential adopters of alternative farming activities in Greek agriculture. J. Rural Studies 2002, 18, 95–103. [Google Scholar] [CrossRef]

- Zakrzewska, A.; Nowak, A. Diversification of agricultural output intensity across the European Union in light of the assumptions of sustainable Development. Agriculture 2022, 12, 1370. [Google Scholar] [CrossRef]

- Li, M.; Long, H.; Tang, L.; Tu, S.; Zhang, Y.; Qu, Y. Analysis of the spatial variations of determinants of agricultural production efficiency in China. Comput. Electron. Agric. 2021, 180, 105890. [Google Scholar]

- Jung, J.; Gómez-Bengoechea, G. A Literature Review on Firm Digitalization: Drivers and Impacts; Estudios Sobre la Economía Española; Fedea: Madrid, Spain, 2022. [Google Scholar]

- Castro, N.R.; Chousa, J.P. An integrated framework for the financial analysis of sustainability. Bus. Strategy Environ. 2006, 15, 322–333. [Google Scholar] [CrossRef]

- Figurek, A.; Vukoje, V. The importance of network accounting data for the creation of agricultural policy, Faculty of Economics Subotica. Anali Ekonomskog fakulteta u Subotici 2011, 25, 187–195. [Google Scholar]

- Rodionovna, A.N.; Aleksandrovich, N.A. Information technologies in the study of factors of competitiveness of grain production. Econ. Agric. Russ. 2022, 5, 72–77. [Google Scholar]

- Tilley, S. Systems Analysis and Design; Cengage Learning: Boston, MA, USA, 2019. [Google Scholar]

- Chen, K.C.G. What is the systems approach? Interfaces 1975, 6, 32–37. [Google Scholar] [CrossRef] [Green Version]

- Lugonja, D.; Jurišić, M.; Plaščak, I.; Zbukvić, I.; Glavica-Tominić, D.; Krušelj, I.; Radočaj, D. Smart agriculture development and its contribution to the sustainable digital transformation of the agri-food sector. Tehnicki Glasnik 2022, 16, 264–267. [Google Scholar] [CrossRef]

- Warke, V.; Kumar, S.; Bongale, A.; Kotecha, K. Sustainable development of smart manufacturing driven by the digital twin framework: A statistical analysis. Sustainability 2021, 13, 10139. [Google Scholar] [CrossRef]

- Chaudhuri, R.; Chatterjee, S.; Vrontis, D.; Chaudhuri, S. Innovation in SMEs, AI dynamism, and sustainability: The current situation and way forward. Sustainability 2022, 14, 12760. [Google Scholar] [CrossRef]

- Thrassou, A.; Chaudhuri, R.; Vrontis, D. Does “CHALTA HAI” culture negatively impact sustainability of business firms in India? An empirical investigation. J. Asia Bus. Stud. 2021, 15, 666–685. [Google Scholar]

- Bebbington, J.; Unerman, J. Advancing research into accounting and the UN sustainable development goals. Account., Auditing. Account J. 2020, 33, 1657–1670. [Google Scholar] [CrossRef]

- McGahan, A.M.; Bogers, M.L.A.M.; Chesbrough, H.; Holgersson, M. Tackling societal challenges with open innovation. Calif. Manag. Rev. 2021, 63, 49–61. [Google Scholar] [CrossRef]

- Kieti, J.; Waema, T.M.; Ndemo, E.B.; Omwansa, T.K.; Baumüller, H. Sources of value creation in aggregator platforms for digital services in agriculture-insights from likely users in Kenya. Digi. Bus. 2021, 1, 100007. [Google Scholar] [CrossRef]

- Hanafizadeh, P.; Khosravi, B.; Tabatabaeian, S.H. Rethinking dominant theories used in information systems field in the digital platform era. Digi. Policy. Regul. Gov. 2020, 22, 363–384. [Google Scholar] [CrossRef]

- Knippenberg, E.; Jensen, N.; Constas, M. Quantifying household resilience with high frequency data: Temporal dynamics and methodological options. World Dev. 2019, 121, 1–15. [Google Scholar] [CrossRef]

- Barry, P.; Ellinger, P.N. Financial Management in Agriculture, 7th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2012. [Google Scholar]

- Figurek, A. Synergy of information systems in agriculture. Ekonomika APK Int. Sci. Prod. J. 2015, 2, 83–89. [Google Scholar]

- Bossel, H. Indicators for Sustainable Development: Theory, Method, Applications; A Report to the Balaton Group; International Institute for Sustainable Development: Winnipeg, Canada, 1999. [Google Scholar]

- Jarek, K.; Mazurek, G. Marketing and artificial intelligence. Central Eur. Bus. Rev. 2019, 8, 46–55. [Google Scholar] [CrossRef]

- Vrchota, J.; Pech, M.; Rolínek, L.; Bednář, J. Sustainability Outcomes of Green Processes in Relation to Industry 4.0 in Manufacturing: Systematic Review. Sustainability 2020, 12, 5968. [Google Scholar] [CrossRef]

- Müller, J.M.; Kiel, D.; Voigt, K.-I. What Drives the Implementation of Industry 4.0? The Role of Opportunities and Challenges in the Context of Sustainability. Sustainability 2018, 10, 247. [Google Scholar] [CrossRef] [Green Version]

- Haseeb, M.; Hussain, H.I.; Ślusarczyk, B.; Jermsittiparsert, K. Industry 4.0: A Solution towards Technology Challenges of Sustainable Business Performance. Soc. Sci. 2019, 8, 154. [Google Scholar] [CrossRef] [Green Version]

- Sharma, J.K.; Dubey, P.K. A need of farm records and accounting in agriculture sector. Int. J. Innov. Stud. Sociol. Humanit. 2019, 4, 155–158. [Google Scholar]

- Thrassou, A.; Chebbi, H.; Uzunboylu, N. Postmodern approaches to business management and innovative notions for contextual adaptation—A review. EuroMed J. Bus. 2021, 16, 261–273. [Google Scholar] [CrossRef]

- Thrassou, A.; Vrontis, D.; Efthymiou, L.; Uzunboylu, N. An Overview of Business Advancement through Technology: The Changing Landscape of Work and Employment. In Business Advancement through Technology Volume II; Thrassou, A., Vrontis, D., Efthymiou, L., Weber, Y., Shams, S.M.R., Tsoukatos, E., Eds.; Palgrave Studies in Cross-Disciplinary Business Research; Association with EuroMed Academy of Business; Palgrave Macmillan: Cham, Switzerland, 2022. [Google Scholar] [CrossRef]

- Vrontis, D.; Thrassou, A.; Weber, Y.; Shams, R.; Tsoukatos, E.; Efthymiou, L. Business Under Crisis Volume I: Avenues for Innovation, Entrepreneurship and Sustainability; Book Series: Palgrave Studies in Cross-Disciplinary Business Research, in Association with EuroMed Academy of Business; Palgrave Macmillan: Cham, Switzerland; Springer: Berlin/Heidelberg, Germany, 2022. [Google Scholar] [CrossRef]

- Chomac-Pierzecka, E.; Sobczak, A.; Urbanczyk, E. RES Market Development and Public Awareness of the Economic and Environmental Dimension of the Energy Transformation in Poland and Lithuania. Energies 2022, 15, 5461. [Google Scholar] [CrossRef]

- Fageberg, J. Mobilizing innovation for sustainability transitions: A comment on transformative innovation policy. Res. Policy 2018, 47, 1568–1576. [Google Scholar] [CrossRef]

- Freeman, C. The National System of Innovation’ in historical perspective. Camb. J. Econ. 1995, 19, 5–24. [Google Scholar]

- Lundvall, B.A.; Johnson, B.; Andersen, E.S.; Dalum, B. National systems of production, innovation and competence building. Res. Policy 2002, 31, 213–231. [Google Scholar] [CrossRef]

- Edquist, C. Systems of Innovation: Technologies, Institutions and Organizations, 1st ed.; Routledge: Abingdon, UK, 1997. [Google Scholar] [CrossRef]

- Meramveliotakis, G.; Manioudis, M. History, Knowledge, and Sustainable Economic Development: The Contribution of John Stuart Mill’s Grand Stage Theory. Sustainability 2021, 13, 1468. [Google Scholar] [CrossRef]

- Manioudis, M.; Meramveliotakis, G. New Institutional Economics and Economic Development: A Smithian Critique. In Bringing Microeconomics and Macroeconomics and the Effects on Economic Development and Growth; Kostis, P., Ed.; IGI Global: Hershey, PA, USA, 2020; pp. 27–40. [Google Scholar]

- Dasgupta, P. The idea of sustainable development. Sustain. Sci. 2007, 2, 5–11. [Google Scholar] [CrossRef]

- Manioudis, M.; Meramveliotakis, G. Broad strokes towards a grand theory in the analysis of sustainable development: A return to the classical political economy. New Political Econ. 2022, 27, 866–878. [Google Scholar] [CrossRef]

Figure 1.

Integrated framework for sustainable development. Developed by the authors.

Figure 2.

An event log for agri-food SMEs with different types of production. Developed by the authors.

Figure 2.

An event log for agri-food SMEs with different types of production. Developed by the authors.

Figure 3.

Determination of input costs with the example of crop production. Developed by the authors.

Figure 3.

Determination of input costs with the example of crop production. Developed by the authors.

Figure 4.

Cost centres. Developed by the authors.

Figure 5.

Revenues and expenses in the agri-food sector. Developed by the authors.

Figure 6.

Micro and macro level in agri-food sector. Developed by the authors.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |