Relationship between the Cost of Capital and Environmental, Social, and Governance Scores: Evidence from Latin America

, , ,

, , ,

Abstract

:1. Introduction

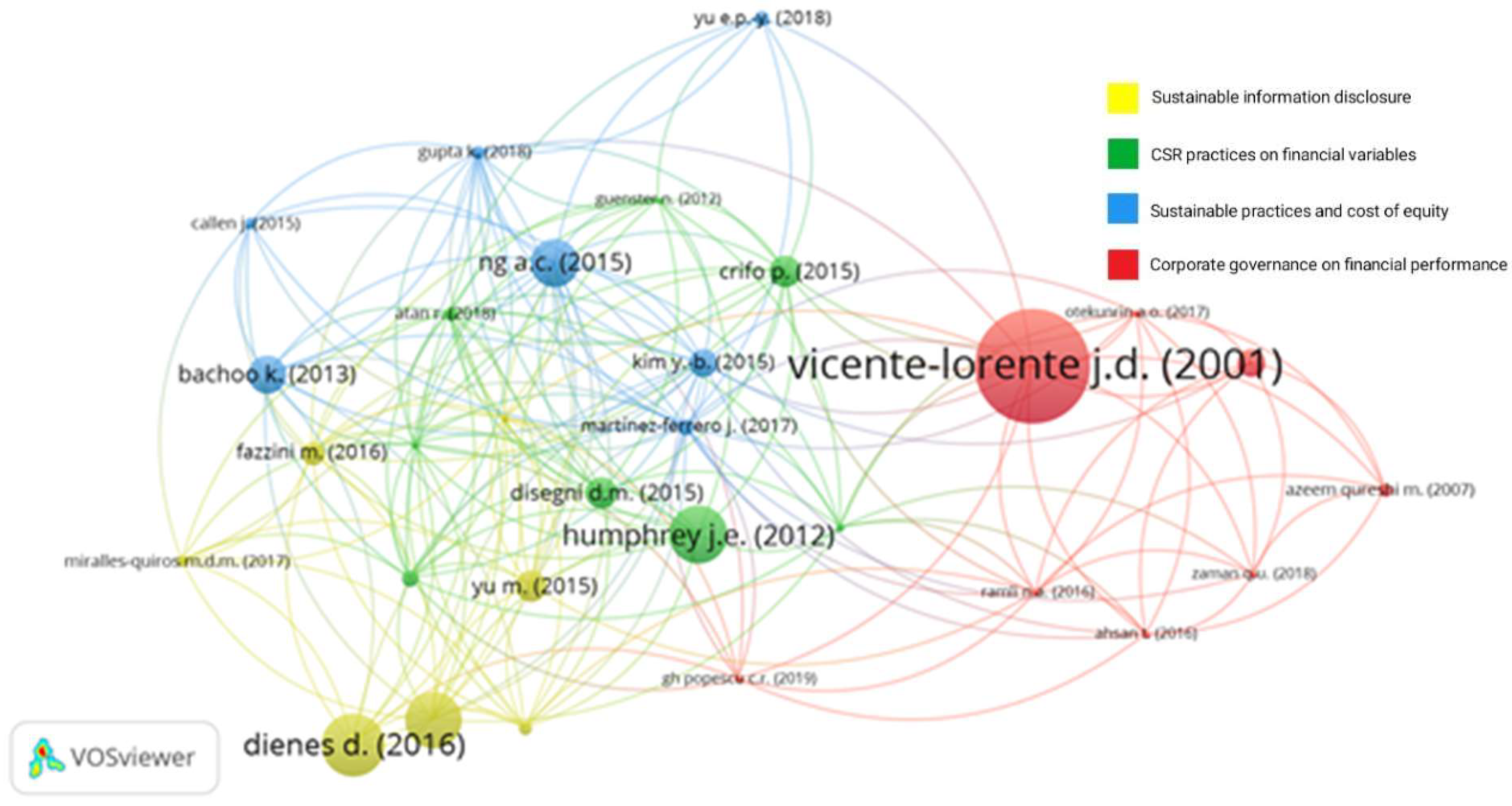

2. Literature Review

2.1. Cluster 1: CSR Practices on Financial Variables

2.2. Cluster 2: Sustainable Information Disclosure

2.3. Cluster 3: Sustainable Practices and Cost of Equity

2.4. Cluster 4: Corporate Governance on Financial Performance

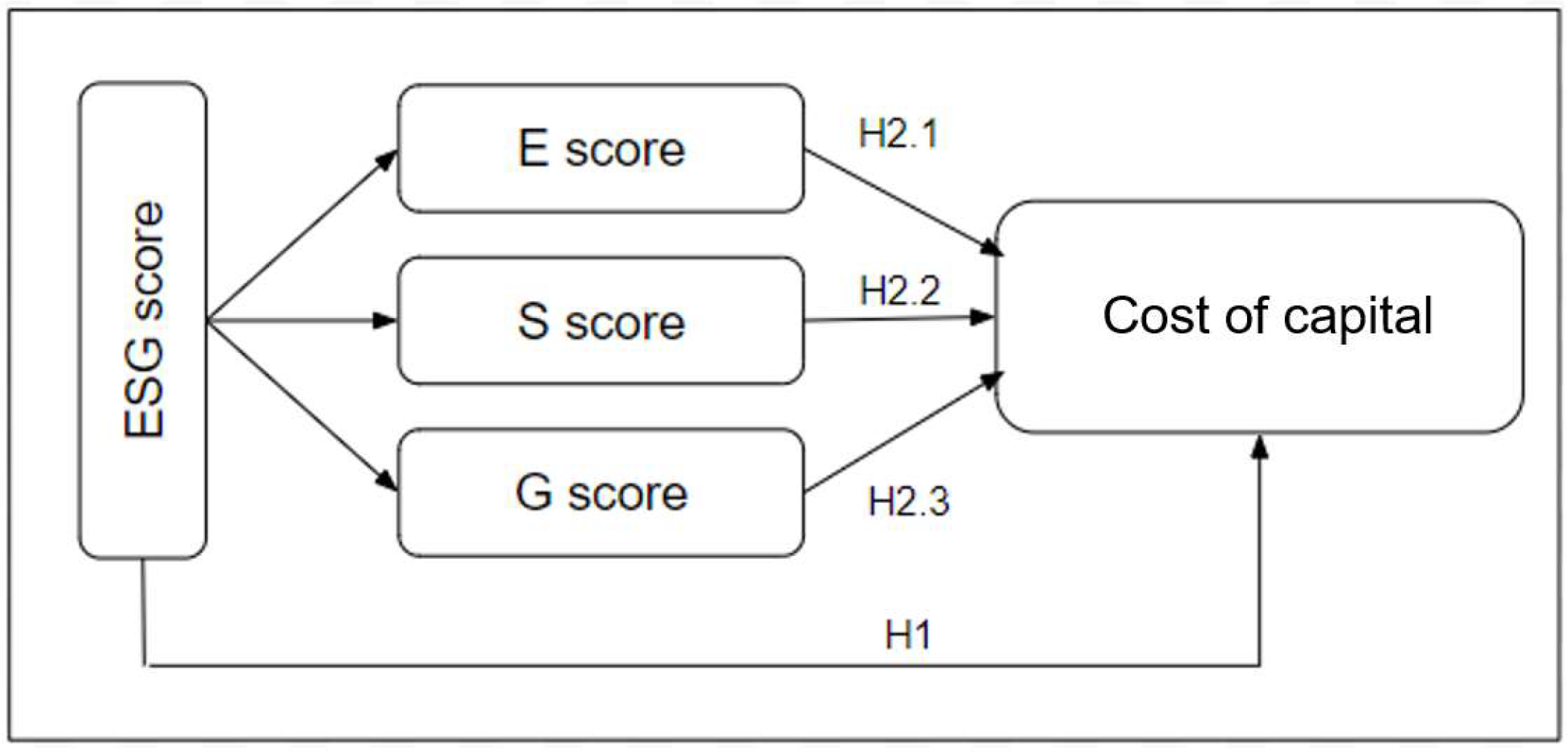

2.5. Hypothesis Development

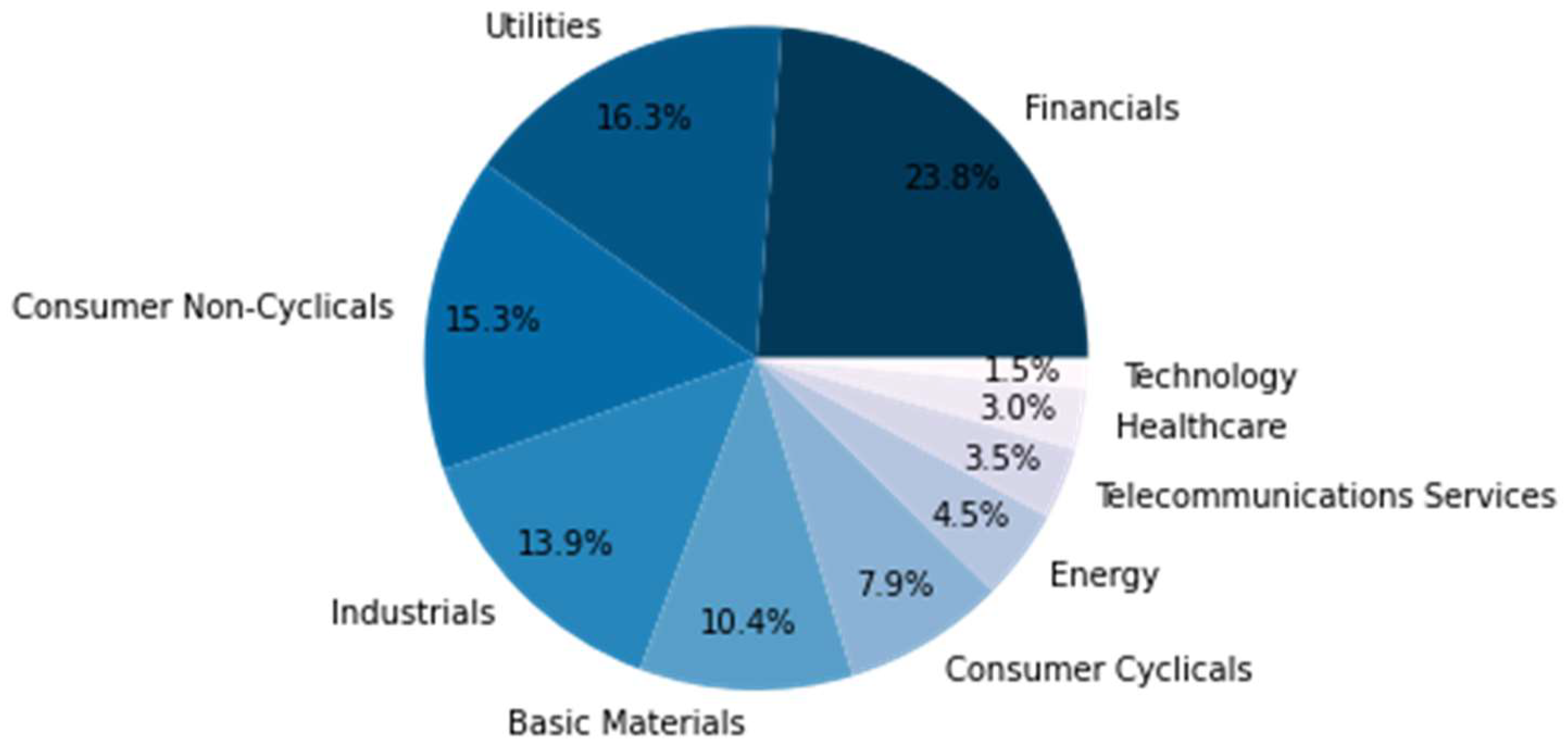

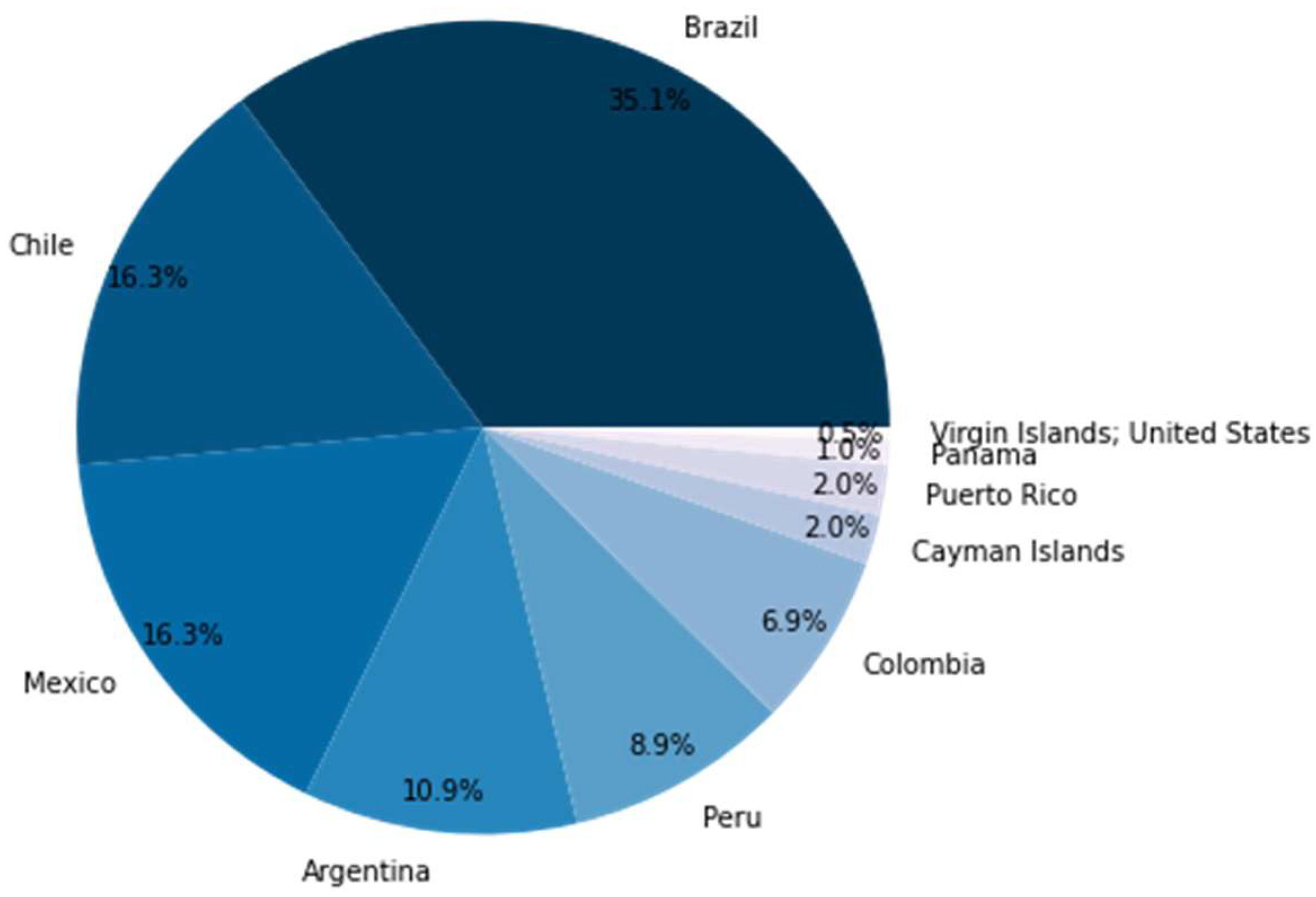

3. Data and Variables

Data Sources

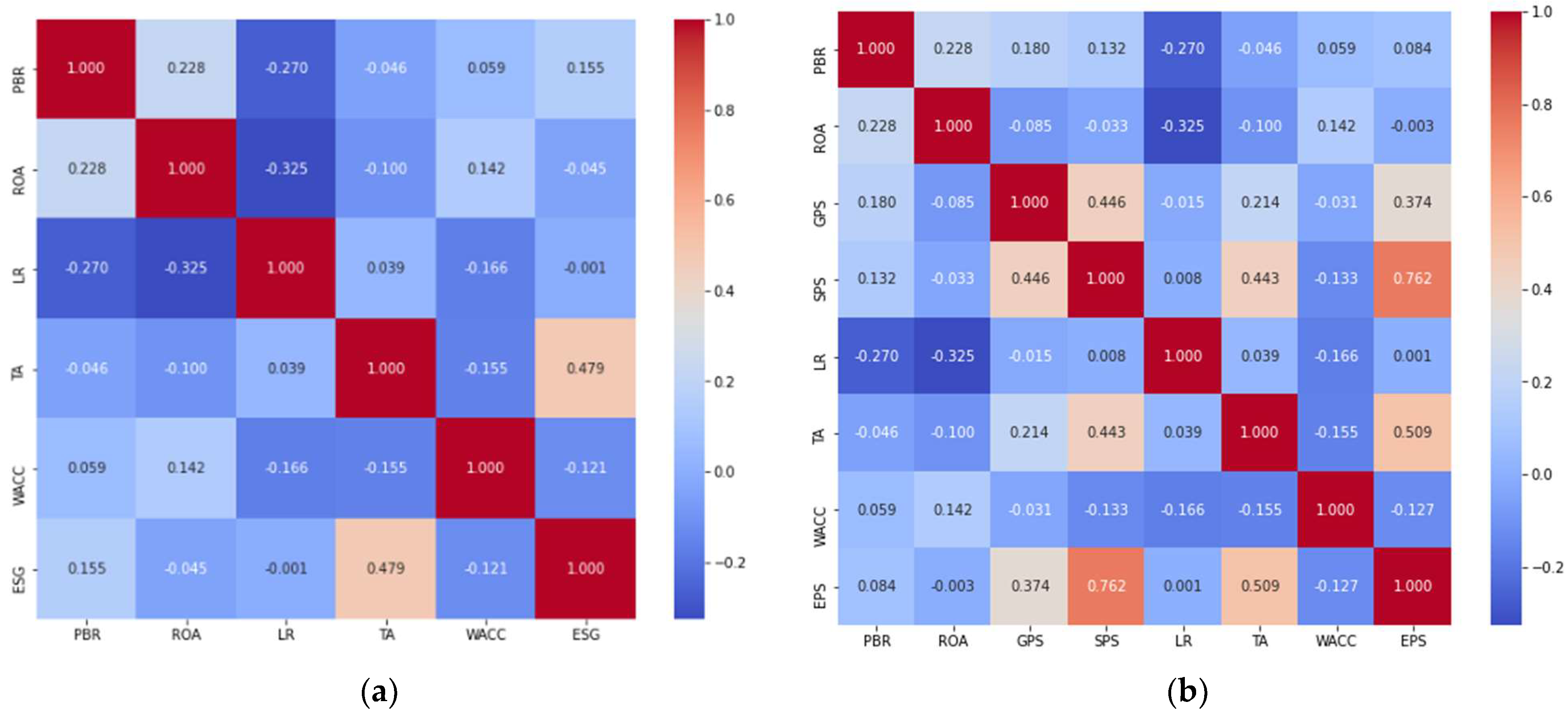

4. Empirical Results

4.1. Descriptive Statistics

4.2. Construction of the Model

4.3. Model Results

4.3.1. ESG Overall Performance and Cost of Capital

4.3.2. ESG Pillar Scores and Cost of Capital

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development; United Nations: New York, NY, USA, 2015; Volume 16301. [Google Scholar]

- Principles for Responsable Investment What is the PRI? About the PRI. 2022. Available online: https://www.unpri.org/about-us/about-the-pri (accessed on 16 March 2022).

- Yesuf, A.J.; Aassouli, D. Exploring synergies and performance evaluation between Islamic funds and socially responsible investment (SRIs) in light of the Sustainable Development Goals (SDGs). Heliyon 2020, 6, e04562. [Google Scholar] [CrossRef] [PubMed]

- Cesarone, F.; Luis Martino, M.; Carleo, A. Does ESG Impact Really Enhance Portfolio Profitability? Sustainability 2022, 14, 2050. [Google Scholar] [CrossRef]

- Jonsdottir, G.E.; Sigurjonsson, T.O.; Alavi, A.R.; Mitchell, J. Applying Responsible Ownership to Advance SDGs and the ESG Framework, Resulting in the Issuance of Green Bonds. Sustainability 2021, 13, 7331. [Google Scholar] [CrossRef]

- Camilo Mejía-Escobar, J.; David González-Ruiz, J.; Franco-Sepúlveda, G.; Becchetti, L.; Ciciretti, R. Current State and Development of Green Bonds Market in the Latin America and the Caribbean. Sustainability 2021, 13, 10872. [Google Scholar] [CrossRef]

- Dhaliwal, D.; Li, O.Z.; Tsang, A.; Yang, Y.G. Corporate social responsibility disclosure and the cost of equity capital: The roles of stakeholder orientation and financial transparency. J. Account. Public Policy 2014, 33, 328–355. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Building a Good Reputation. Eur. Manag. J. 2004, 22, 704–713. [Google Scholar] [CrossRef]

- Duque-Grisales, E.; Aguilera-Caracuel, J. Environmental, Social and Governance (ESG) Scores and Financial Performance of Multilatinas: Moderating Effects of Geographic International Diversification and Financial Slack. J. Bus. Ethics 2019, 168, 315–334. [Google Scholar] [CrossRef]

- Petrakis, P.; Carayannis, E.; Kostis, P.; Aldowaish, A.; Kokuryo, J.; Almazyad, O.; Goi, H.C. Environmental, Social, and Governance Integration into the Business Model: Literature Review and Research Agenda. Sustainability 2022, 14, 2959. [Google Scholar] [CrossRef]

- Atan, R.; Alam, M.M.; Said, J.; Zamri, M. The impacts of environmental, social, and governance factors on firm performance: Panel study of Malaysian companies. Manag. Environ. Qual. Int. J. 2018, 29, 182–194. [Google Scholar] [CrossRef]

- Ng, A.C.; Rezaee, Z. Business sustainability performance and cost of equity capital. J. Corp. Financ. 2015, 34, 128–149. [Google Scholar] [CrossRef]

- Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. Account. Rev. 2011, 86, 59–100. Available online: https://www.jstor.org/stable/29780225 (accessed on 17 February 2022). [CrossRef]

- Shad, M.K.; Lai, F.W.; Shamim, A.; McShane, M. The efficacy of sustainability reporting towards cost of debt and equity reduction. Environ. Sci. Pollut. Res. 2020, 27, 22511–22522. [Google Scholar] [CrossRef] [PubMed]

- Bernstsson, W. The Impact of ESG Score on Firm’s Cost of Capital and Riskiness; University of Gothenburg: Gothenburg, Sweden, 2019. [Google Scholar]

- Middha, D.; Shailesh Doshi, Y. Relationship between Esg and Financial Performance of Publicly Listed Firms on the s&p 500; Simon Fraser University: Burnaby, BC, Canada, 2019. [Google Scholar]

- Husted, B.W.; Sousa-Filho, J.M. de Board structure and environmental, social, and governance disclosure in Latin America. J. Bus. Res. 2019, 102, 220–227. [Google Scholar] [CrossRef]

- Moreno-Gómez, J.; Calleja-Blanco, J. The relationship between women’s presence in corporate positions and firm performance: The case of Colombia. Int. J. Gend. Entrep. 2018, 10, 83–100. [Google Scholar] [CrossRef]

- Lafuente, E.; Vaillant, Y. Balance rather than critical mass or tokenism: Gender diversity, leadership and performance in financial firms. Int. J. Manpow. 2019, 40, 894–916. [Google Scholar] [CrossRef]

- Waltman, L. A review of the literature on citation impact indicators. J. Informetr. 2016, 10, 365–391. [Google Scholar] [CrossRef] [Green Version]

- Marquez-Cardenas, V.; Gonzalez-Ruiz, J.D.; Duque-Grisales, E. Board gender diversity and firm performance: Evidence from Latin America. J. Sustain. Financ. Investig. 2022, 24, 2017256. [Google Scholar] [CrossRef]

- David González-Ruiz, J.; Camilo Mejia-Escobar, J.; Franco-Sepúlveda, G.; González-Ruiz, C.; Mejia-Escobar, J.D. Towards an Understanding of Project Finance in the Mining Sector in the Sustainability Context: A Scientometric Analysis. Sustainability 2021, 13, 10317. [Google Scholar] [CrossRef]

- Chen, D.; Jia, F.; Guo, J. A systematic review of current status and trends of mega-infrastructure projects. Ain Shams Eng. J. 2022, 13, 11. [Google Scholar] [CrossRef]

- Tamala, J.K.; Maramag, E.I.; Simeon, K.A.; Ignacio, J.J. A bibliometric analysis of sustainable oil and gas production research using VOSviewer. Clean. Eng. Technol. 2022, 7, 100437. [Google Scholar] [CrossRef]

- van Eck, N.J.; Waltman, L. VOSviewer Manual; Universiteit Leiden: Leiden, The Netherlands, 2020. [Google Scholar]

- Crifo, P.; Forget, V.D.; Teyssier, S. The price of environmental, social and governance practice disclosure: An experiment with professional private equity investors. J. Corp. Financ. 2015, 30, 168–194. [Google Scholar] [CrossRef]

- Yoon, B.; Lee, J.; Byun, R. Does ESG Performance Enhance Firm Value? Evidence from Korea. Sustainability 2018, 10, 3635. [Google Scholar] [CrossRef] [Green Version]

- Guenster, N. Performance Implications of SR Investing: Past versus Future. In Socially Responsible Finance and Investing: Financial Institutions, Corporations, Investors, and Activists; Wiley: Hoboken, NJ, USA, 2012; pp. 443–454. [Google Scholar] [CrossRef]

- Humphrey, J.E.; Lee, D.D.; Shen, Y. Does it cost to be sustainable? J. Corp. Financ. 2012, 18, 626–639. [Google Scholar] [CrossRef]

- DiSegni, D.M.; Huly, M.; Akron, S. Corporate social responsibility, environmental leadership and financial performance. Soc. Responsib. J. 2015, 11, 131–148. [Google Scholar] [CrossRef] [Green Version]

- Cajias, M.; Fuerst, F.; Bienert, S. Can investing in corporate social responsibility lower a company’s cost of capital? Stud. Econ. Financ. 2014, 31, 202–222. [Google Scholar] [CrossRef]

- Dienes, D.; Sassen, R.; Fischer, J. What are the drivers of sustainability reporting? A systematic review. Sustain. Account. Manag. Policy J. 2016, 7, 154–189. [Google Scholar] [CrossRef]

- Albers, C.; Günther, T. Disclose or not disclose: Determinants of social reporting for STOXX Europe 600 firms. Zeitschrift für Plan. Unternehm. 2010, 21, 323–347. [Google Scholar] [CrossRef] [Green Version]

- Fazzini, M.; Dal Maso, L. The value relevance of “assured” environmental disclosure: The Italian experience. Sustain. Account. Manag. Policy J. 2016, 7, 225–245. [Google Scholar] [CrossRef]

- Yu, M.; Zhao, R. Sustainability and firm valuation: An international investigation. Int. J. Account. Inf. Manag. 2015, 23, 289–307. [Google Scholar] [CrossRef]

- Miralles-Quiros, M.D.M.; Miralles-Quiros, J.L.; Arraiano, I.G. Sustainable Development, Sustainability Leadership and Firm Valuation: Differences across Europe. Bus. Strateg. Environ. 2017, 26, 1014–1028. [Google Scholar] [CrossRef]

- Martínez Ferrero, J. Effect of sustainable practices on capital costs and corporate reputation. Rev. Contab. Account. Rev. 2014, 17, 153–162. [Google Scholar] [CrossRef] [Green Version]

- Gupta, K. Environmental Sustainability and Implied Cost of Equity: International Evidence. J. Bus. Ethics 2018, 147, 343–365. [Google Scholar] [CrossRef]

- Bachoo, K.; Tan, R.; Wilson, M. Firm Value and the Quality of Sustainability Reporting in Australia. Aust. Account. Rev. 2013, 23, 67–87. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; García-Sánchez, I.M. Sustainability assurance and cost of capital: Does assurance impact on credibility of corporate social responsibility information? Bus. Ethics A Eur. Rev. 2017, 26, 223–239. [Google Scholar] [CrossRef]

- Hussain, H.I.; Grabara, J.; Razimi, M.S.A.; Sharif, S.P. Sustainability of Leverage Levels in Response to Shocks in Equity Prices: Islamic Finance as a Socially Responsible Investment. Sustainability 2019, 11, 3260. [Google Scholar] [CrossRef] [Green Version]

- Gh Popescu, C.R. Corporate social responsibility, corporate governance and business performance: Limits and challenges imposed by the implementation of directive 2013/34/EU in Romania. Sustainability 2019, 11, 5146. [Google Scholar] [CrossRef] [Green Version]

- Olubukola, O.A. Adoption of International Financial Reporting Standard, Capital Structure and Profitability of Listed Firms in Nigeria. 2017. Available online: https://ibima.org/accepted-paper/adoption-of-international-financial-reporting-standard-capital-structure-and-profitability-of-listed-firms-in-nigeria-2/ (accessed on 17 February 2022).

- Refinitiv Environmental, Social and Governance (ESG) Scores. 2022. Available online: https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/esg-scores-methodology.pdf (accessed on 17 December 2021).

- Fama, E.F.; French, K.R.; Lakonishok, J.; Penman, S.; Sinquefield, R.; Stulz, R. Size and Book-to-Market Factors in Earnings and Returns. J. Financ. 1995, 50, 131–155. [Google Scholar] [CrossRef]

- Vena, L.; Sciascia, S.; Cortesi, A. Integrated reporting and cost of capital: The moderating role of cultural dimensions. J. Int. Financ. Manag. Account. 2020, 31, 191–214. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R.; Constan-Tinides, G.; Ferson, W.; George, E.; Harvey, C.; Lakonishok, J.; Sinquefield, R.; Stulz, R.; Zmijeweski, M. The Cross-Section of Expected Stock Returns. J. Financ. 1992, 47, 427–465. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Common risk factors in the returns on stocks and bonds. J. Financ. Econ. 1993, 33, 3–56. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Introductory Econometrics: A Modern Approach, 5th ed.; Cengage-Learning: South-Western, UK, 2013. [Google Scholar]

- Greene, W. Econometric Analysis, 8th ed.; Pearson: London, UK, 2018. [Google Scholar]

- Stock, J.; Watson, M. Introduction to Econometrics, 4th ed.; Pearson: London, UK, 2019. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Denotation | Measurement | Literature Sources |

|---|---|---|---|

| Firm size | TA | Natural logarithm of total assets | [46] |

| Profitability | ROA | Return on assets | [15] |

| Financial leverage | LR | Total debt divided by total assets | [48] |

| Firm’s growth opportunities | PBR | Natural logarithm of the market-to-book ratio | [48,49] |

| Variable | Mean | Std. Dev. | Min | 25% | 50% | 75% | Max | CV |

|---|---|---|---|---|---|---|---|---|

| WACC | 0.089 | 0.050 | 0.021 | 0.057 | 0.073 | 0.106 | 0.338 | 0.562 |

| ESG | 48.937 | 19.342 | 6.700 | 33.552 | 52.069 | 64.626 | 89.523 | 0.395 |

| EPS | 48.781 | 23.542 | 4.915 | 27.998 | 50.580 | 67.997 | 97.246 | 0.483 |

| GPS | 50.383 | 21.700 | 6.279 | 32.383 | 52.424 | 67.464 | 92.233 | 0.430 |

| SPS | 47.843 | 23.991 | 3.002 | 27.164 | 51.569 | 66.553 | 95.014 | 0.500 |

| PBR | 0.507 | 0.859 | −2.743 | 0.003 | 0.483 | 1.006 | 3.481 | 1.694 |

| ROA | 0.044 | 0.085 | −0.696 | 0.014 | 0.038 | 0.077 | 0.466 | 1.932 |

| LR | 1.223 | 3.673 | 0.000 | 0.191 | 0.487 | 0.984 | 46.240 | 3.003 |

| TA | 8.409 | 1.554 | 3.128 | 7.463 | 8.380 | 9.514 | 12.980 | 0.185 |

| Statistic | p-Value | |

|---|---|---|

| Breusch–Pagan Lagrangian test | 18.1855 *** (LM Statistic) | 0.0027 |

| Hausman test | 54.5311 *** (Chi-squared) | 0.0000 |

| Variable | (1) | (2) |

|---|---|---|

| Constant | 0.0065 (0.0614) | 0.0129 (0.0615) |

| PBR | −0.0321 *** (0.0056) | −0.0323 *** (0.0055) |

| ROA | 0.0328 (0.0252) | 0.0315 (0.0250) |

| LR | −0.0017 ** (0.0008) | −0.0017 * (0.0009) |

| TA | 0.0149 * (0.0080) | 0.0146 * (0.0080) |

| ESG | −0.0006 ** (0.0003) | |

| GPS | −0.0003 ** (0.0001) | |

| SPS | −0.0000 (0.0002) | |

| EPS | −0.0003 (0.0002) | |

| Year 2018 | 0.0143 *** (0.0023) | 0.0142 *** (0.0023) |

| Year 2019 | −0.0075 *** (0.0021) | −0.0076 *** (0.0021) |

| R-squared | 0.4013 | 0.4044 |

| F-statistic (robust) | 20.849 *** | 16.797 *** |

| Number of observations | 606 | 606 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ramirez, A.G.; Monsalve, J.; González-Ruiz, J.D.; Almonacid, P.; Peña, A. Relationship between the Cost of Capital and Environmental, Social, and Governance Scores: Evidence from Latin America. Sustainability 2022, 14, 5012. https://doi.org/10.3390/su14095012

Ramirez AG, Monsalve J, González-Ruiz JD, Almonacid P, Peña A. Relationship between the Cost of Capital and Environmental, Social, and Governance Scores: Evidence from Latin America. Sustainability. 2022; 14(9):5012. https://doi.org/10.3390/su14095012

Chicago/Turabian StyleRamirez, Ana Gabriela, Julián Monsalve, Juan David González-Ruiz, Paula Almonacid, and Alejandro Peña. 2022. "Relationship between the Cost of Capital and Environmental, Social, and Governance Scores: Evidence from Latin America" Sustainability 14, no. 9: 5012. https://doi.org/10.3390/su14095012