An Assessment Tool to Integrate Sustainability Principles into the Global Supply Chain

, , ,

, , ,

Abstract

:1. Introduction

1.1. Sustainability Principles

1.2. Sustainability, Global Supply Chain, and the Circular Economy

2. Literature Review

2.1. Sustainability Principles and Circular Economy

2.1.1. Research Question 1a: Are Sustainability Principles Integrated in the Current Circular Economy Paradigm?

2.1.2. Research Question 1b: How Could Sustainability Principles be Integrated into the Current Circular Economy Paradigm?

2.2. Sustainability Principles and Corporate Sustainability Assessment along the Supply Chain

Research Question 2 How are Sustainability Principles being Nowadays Integrated into the Assessment of corporate Performance along Supply Chains?

- The multidimensionality of the sustainability concept makes the search for suitable CSP assessment very difficult [96]. In this context, two main issues must be addressed. On the one hand, although social issues in the supply chain have grown in importance in the last years [78], there is no consensus on the adequate indicators or methods for social assessment [86]. On the other hand, very few proposals, approaches, and frameworks (for example, [98] or [61]) explicitly address a balance among the different sustainability dimensions. To avoid the possible offsetting of negative scores with good scores some authors, such as Escrig-Olmedo et al. [16], and Rivera et al. [100], evaluate the performance in organizations by means of the Fuzzy Inference System methodology.

- The inter-generational perspective is not considered in the majority of the proposed frameworks, since they do not take into account the interactions of different metrics, outputs, and parameters over time (future) and the long-term effects of today’s decisions. However, it is observed that a growing number of different assessment methodologies, such as LCA, are adopting different methods like “hotspots analysis” to prioritize potential actions around the most significant economic, environmental and social sustainability impacts of a company [87,88]. In this context, UNEP’s Hotspots Analysis Overarching Methodological Framework should be considered in the CSP assessment process.

- In general terms, there is a lack of integration of stakeholders’ interests in decisions on LCSA models. In order to face these challenges, some proposals, like those of Halog and Manik [86] or Souza et al. [94] integrate the stakeholders’ preferences through multiple-criteria decision methods. The use of these methodologies, combined with fuzzy logic methods, allows the complete integration of stakeholders’ interests [57].

- Some frameworks are adopting a LCT approach (for instance [35,86,94]); however, more investigation is needed for advancing into the supply chain management. To overcome this challenge, different tools for monitoring impacts on sustainability like LCA (for example, [85,88]) or footprints methodologies (for instance, [101]) have been developed. In an international context, two of the most accepted methodologies are the Organizational Environmental Footprint from the European Commission, which measures the environmental impacts, and the UNEP/SETAC methodology, which measures social impacts [88,89].

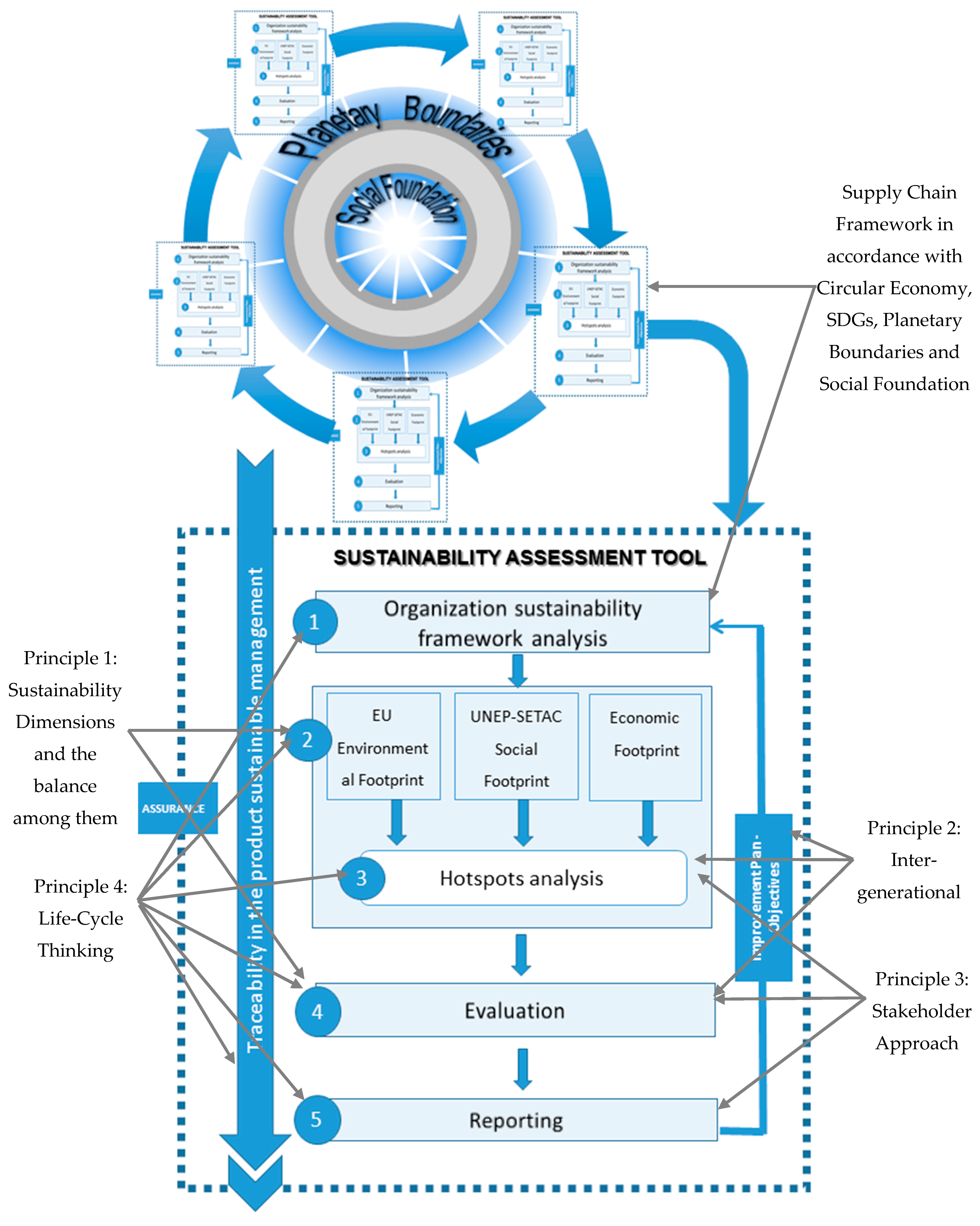

3. A Corporate Sustainability Assessment Framework Proposal

4. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Griggs, D.; Stafford-Smith, M.; Gaffney, O.; Rockström, J.; Öhman, M.C.; Shyamsundar, P.; Steffen, W.; Glaser, G.; Kanie, N.; Noble, I. Policy: Sustainable development goals for people and planet. Nature 2013, 495, 305–307. [Google Scholar] [CrossRef] [PubMed]

- Glavič, P.; Lukman, R. Review of sustainability terms and their definitions. J. Clean. Prod. 2007, 15, 1875–1885. [Google Scholar] [CrossRef]

- Lozano, R. Envisioning sustainability three-dimensionally. J. Clean. Prod. 2008, 16, 1838–1846. [Google Scholar] [CrossRef]

- Alayón, C.; Säfsten, K.; Johansson, G. Conceptual sustainable production principles in practice: Do they reflect what companies do? J. Clean. Prod. 2017, 141, 693–701. [Google Scholar] [CrossRef]

- De Castro Hilsdorf, W.; de Mattos, C.A.; de Campos Maciel, L.O. Principles of sustainability and practices in the heavy-duty vehicle industry: A study of multiple cases. J. Clean. Prod. 2017, 141, 1231–1239. [Google Scholar] [CrossRef]

- Silvius, A.G.; Kampinga, M.; Paniagua, S.; Mooi, H. Considering sustainability in project management decision making; An investigation using Q-methodology. Int. J. Proj. Manag. 2017, 35, 1133–1150. [Google Scholar] [CrossRef]

- Flint, R.W. Practice of Sustainable Community Development: A Participatory Framework for Change; Springer: New York, NY, USA, 2013. [Google Scholar]

- Lindsey, T.C. Sustainable principles: Common values for achieving sustainability. J. Clean. Prod. 2011, 19, 561–565. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of 21st Century Business; Capstone Publishing Ltd.: Oxford, UK, 1997. [Google Scholar]

- Freeman, E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- International Organization for Standardization (ISO). International Organization for Standardization, ISO 26000:2010—Guidance on Social Responsibility; ISO: Genève, Switzerland, 2010. [Google Scholar]

- World Commission on Environment and Development (WCED). World Commission on Environment and Development. Our Common Future. 1987. Available online: www.un-documents.net/our-common-future.pdf (accessed on 19 December 2017).

- Ridsdale, D.R.; Noble, B.F. Assessing sustainable remediation frameworks using sustainability principles. J. Environ. Manag. 2016, 184, 36–44. [Google Scholar] [CrossRef] [PubMed]

- Neumayer, E. Weak Versus Strong Sustainability: Exploring the Limits of Two Opposing Paradigms; Edward Elgar Publishing: Cheltenham, UK, 2003. [Google Scholar]

- Turner, R.K. Sustainable Environmental Economics and Management: Principles and Practice; Belhaven Press: London, UK, 1993. [Google Scholar]

- Escrig-Olmedo, E.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á.; Rivera-Lirio, J.M. Lights & Shadows on Sustainability Rating Scoring. Rev. Manag. Sci. 2014, 8, 559–574. [Google Scholar]

- Ferrero-Ferrero, I.; Fernández-Izquierdo, M.Á.; Muñoz-Torres, M.J. The Effect of Environmental, Social and Governance Consistency on Economic Results. Sustainability 2016, 8, 1005. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á.; Rivera-Lirio, J.M. Measuring corporate environmental performance: A methodology for sustainable development. Bus. Strategy Environ. 2017, 26, 142–162. [Google Scholar] [CrossRef]

- Boyle, C.; Coates, G.T.K. Sustainability principles and practice for engineers. IEEE Technol. Soc. Mag. 2005, 24, 32–39. [Google Scholar] [CrossRef]

- Amaeshi, K.M.; Osuji, O.K.; Nnodim, P. Corporate social responsibility in supply chains of global brands: A boundaryless responsibility? Clarifications, exceptions and implications. J. Bus. Ethics 2008, 81, 223–234. [Google Scholar] [CrossRef] [Green Version]

- Andersen, M.; Skjoett-Larsen, T. Corporate social responsibility in global supply chains. Supply Chain Manag. 2009, 14, 75–86. [Google Scholar] [CrossRef]

- Guide, V.D.R., Jr.; Van Wassenhove, L.N. The evolution of closed-loop supply chain research. Oper. Res. 2009, 57, 10–18. [Google Scholar] [CrossRef]

- Srivastava, S.K. Green supply-chain management: A state-of-the-art literature review. Int. J. Manag. Rev. 2007, 9, 53–80. [Google Scholar] [CrossRef]

- Seuring, S.; Müller, M. From a literature review to a conceptual framework for sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- O’Rourke, D. The science of sustainable supply chains. Science 2014, 344, 1124–1127. [Google Scholar] [CrossRef] [PubMed]

- Hazen, B.T.; Mollenkopf, D.A.; Wang, Y. Remanufacturing for the circular economy: An examination of consumer switching behavior. Bus. Strategy Environ. 2017, 26, 451–464. [Google Scholar] [CrossRef]

- Liu, S.; Chang, Y.T. Manufacturers’ Closed-Loop Orientation for Green Supply Chain Management. Sustainability 2017, 9, 222. [Google Scholar] [CrossRef]

- Masi, D.; Day, S.; Godsell, J. Supply Chain Configurations in the Circular Economy: A Systematic Literature Review. Sustainability 2017, 9, 1602. [Google Scholar] [CrossRef]

- Witjes, S.; Lozano, R. Towards a more Circular Economy: Proposing a framework linking sustainable public procurement and sustainable business models. Resour. Conserv. Recycl. 2016, 112, 37–44. [Google Scholar] [CrossRef]

- Murray, A.; Skene, K.; Haynes, K. The circular economy: An interdisciplinary exploration of the concept and application in a global context. J. Bus. Ethics 2017, 140, 369–380. [Google Scholar] [CrossRef]

- Ellen MacArthur Foundation. Towards a Circular Economy: Business Rationale for an Accelerated Transition. 2015. Available online: https://www.ellenmacarthurfoundation.org (accessed on 22 November 2017).

- European Commission. Towards a Circular Economy: A Zero Waste Programme for Europe, COM (2014) 398 Final, Brussels, 2014. Available online: http://ec.europa.eu/environment/circular-economy/pdf/circular-economy-communication.pdf (accessed on 16 February 2018).

- Su, B.; Heshmati, A.; Geng, Y.; Yu, X. A review of the circular economy in China: Moving from rhetoric to implementation. J. Clean. Prod. 2013, 42, 215–227. [Google Scholar] [CrossRef]

- Tajbakhsh, A.; Hassini, E. Performance measurement of sustainable supply chains: A review and research questions. Int. J. Prod. Perform. Manag. 2015, 64, 744–783. [Google Scholar] [CrossRef]

- Hoogmartens, R.; Van Passel, S.; Van Acker, K.; Dubois, M. Bridging the gap between LCA, LCC and CBA as sustainability assessment tools. Environ. Impact Asses. 2014, 48, 27–33. [Google Scholar] [CrossRef]

- Webster, J.; Watson, R.T. Analyzing the past to prepare for the future: Writing a literature review. MIS Q. 2002, 26, 13–23. [Google Scholar]

- Geissdoerfer, M.; Savaget, P.; Bocken, N.M.; Hultink, E.J. The Circular Economy–A new sustainability paradigm? J. Clean. Prod. 2017, 143, 757–768. [Google Scholar] [CrossRef]

- Niero, M.; Hauschild, M.Z. Closing the Loop for Packaging: Finding a Framework to Operationalize Circular Economy Strategies. Procedia CIRP 2017, 61, 685–690. [Google Scholar] [CrossRef]

- Sauvé, S.; Bernard, S.; Sloan, P. Environmental sciences, sustainable development and circular economy: Alternative concepts for trans-disciplinary research. Environ. Dev. 2016, 17, 48–56. [Google Scholar] [CrossRef]

- Loiseau, E.; Saikku, L.; Antikainen, R.; Droste, N.; Hansjürgens, B.; Pitkänen, K.; Leskinen, P.; Kuikman, P.; Thomsen, M. Green economy and related concepts: An overview. J. Clean. Prod. 2016, 139, 361–371. [Google Scholar] [CrossRef]

- Korhonen, J.; Honkasalo, A.; Seppälä, J. Circular economy: The concept and its limitations. Ecol. Econ. 2018, 143, 37–46. [Google Scholar] [CrossRef]

- Zeng, H.; Chen, X.; Xiao, X.; Zhou, Z. Institutional pressures, sustainable supply chain management, and circular economy capability: Empirical evidence from Chinese eco-industrial park firms. J. Clean. Prod. 2017, 155, 54–65. [Google Scholar] [CrossRef]

- Steffen, W.; Richardson, K.; Rockström, J.; Cornell, S.E.; Fetzer, I.; Bennett, E.M.; Biggs, R.; Carpenter, S.R.; de Vries, W.; de Wit, C.A.; et al. Planetary boundaries: Guiding human development on a changing planet. Science 2015, 347, 1259855. [Google Scholar] [CrossRef] [PubMed]

- McDonough, W.; Braungart, M. Towards a sustaining architecture for the 21st century: The promise of cradle-to-cradle design. Ind. Environ. 2003, 26, 13–16. [Google Scholar]

- Raworth, K. Doughnut Economics: Seven Ways to Think Like a 21st-Century Economist; Chelsea Green Publishing: Chelsea, VT, USA, 2017. [Google Scholar]

- Melissa, L.; Raworth, K.; Rockström, J. Between Social and Planetary Boundaries: Navigating Pathways in the Safe and Just Space for Humanity. ISSC and UNESCO World Social Science Report 2013, Changing Global Environments 2013. Available online: http://www.worldsocialscience.org/documents/wss-report-2013-part-1.pdf#page=21 (accessed on 6 February 2018).

- Fischer, A.; Pascucci, S. Institutional incentives in circular economy transition: The case of material use in the Dutch textile industry. J. Clean. Prod. 2017, 155, 17–32. [Google Scholar] [CrossRef]

- Wood, D.J. Corporate social performance revisited. Acad. Manag. Rev. 1991, 16, 691–718. [Google Scholar]

- Wood, D.J. Measuring corporate social performance: A review. Int. J. Manag. Rev. 2010, 12, 50–84. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. An overview of sustainability assessment methodologies. Ecol. Indic. 2009, 9, 189–212. [Google Scholar] [CrossRef]

- Roca, L.C.; Searcy, C. An analysis of indicators disclosed in corporate sustainability reporting. J. Clean. Prod. 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Morioka, S.N.; de Carvalho, M.M. A systematic literature review towards a conceptual framework for integrating sustainability performance into business. J. Clean. Prod. 2016, 136, 134–146. [Google Scholar] [CrossRef]

- Searcy, C. Corporate sustainability performance measurement systems: A review and research agenda. J. Bus. Ethics 2012, 107, 239–253. [Google Scholar] [CrossRef]

- Searcy, C. Measuring enterprise sustainability. Bus. Strategy Environ. 2016, 25, 120–133. [Google Scholar] [CrossRef]

- Pope, J.; Annandale, D.; Morrison-Saunders, A. Conceptualising sustainability assessment. Environ. Impact Assess. 2004, 24, 595–616. [Google Scholar] [CrossRef]

- Muñoz-Torres, M.J.; Fernandez-Izquierdo, M.A.; Rivera-Lirio, J.M.; Ferrero-Ferrero, I.; Escrig-Olmedo, E.; Marullo, M.C.; Gisbert-Navarro, J.V. D5.1 List of Issues to Be Considered under Life Cycle Thinking; Public Report, SMART H2020 Project; 2017; Available online: http://www.smart.uio.no/research/life-cycle-thinking---issues-to-be-considered.pdf (accessed on 14 February 2018).

- Escrig-Olmedo, E.; Rivera-Lirio, J.M.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á. Integrating multiple ESG investors’ preferences into sustainable investment: A fuzzy multicriteria methodological approach. J. Clean. Prod. 2017, 162, 1334–1345. [Google Scholar] [CrossRef]

- Busch, T.; Bauer, R.; Orlitzky, M. Sustainable Development and Financial Markets Old Paths and New Avenues. Bus. Soc. 2016, 55, 303–329. [Google Scholar] [CrossRef]

- Chatterji, A.K.; Durand, R.; Levine, D.I.; Touboul, S. Do ratings of firms converge? Implications for managers, investors and strategy researchers. Strateg. Manag. J. 2016, 37, 1597–1614. [Google Scholar] [CrossRef]

- Antolin-Lopez, R.; Delgado-Ceballos, J.; Montiel, I. Deconstructing corporate sustainability: A comparison of different stakeholder metrics. J. Clean. Prod. 2016, 136, 5–17. [Google Scholar] [CrossRef]

- Chardine-Baumann, E.; Botta-Genoulaz, V. A framework for sustainable performance assessment of supply chain management practices. Comput. Ind. Eng. 2014, 76, 138–147. [Google Scholar] [CrossRef]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- European Commission Joint Research Centre (EC JRC). Organization Environmental Footprint (OEF). 2012. Available online: http://www.eur-lex.europa.eu/legal-content (accessed on 2 November 2017).

- UNEP/SETAC Life Cycle Initiative. Towards a Life Cycle Sustainability Assessment. Making Informed Choices on Products. 2011. Available online: https://www.uncclearn.org/sites/default/files/unep_lifecycleinit_dec_final_1.pdf (accessed on 2 November 2017).

- The Organisation for Economic Co-operation and Development (OECD). Guidelines for Multinational Enterprises; OECD Publishing, 2011; Available online: http://dx.doi.org/10.1787/9789264115415-en (accessed on 2 November 2017).

- United Nations Global Compact. The Ten Principles of the UN Global Compact. Available online: https://www.unglobalcompact.org/what-is-gc/mission/principles (accessed on 2 November 2017).

- Principles for Responsible Investment (UN’s PRI). 2006. Available online: https://www.unpri.org/ (accessed on 2 November 2017).

- Accountability. AA1000 Accountability Principles Standard (AA1000APS). 2008. Available online: https://www.accountability.org/standards/ (accessed on 2 November 2017).

- Carbon Disclosure Project (CDP). Available online: https://www.cdp.net/ (accessed on 2 November 2017).

- European Commission (EC). Regulation (EC) No 1221/2009 of the European Parliament and of the Council of 25 November 2009 on the Voluntary Participation by Organisations in a Community Eco-Management and Audit Scheme (EMAS). Available online: http://ec.europa.eu/environment/emas/emas_publications/policy_en.htm (accessed on 2 November 2017).

- ISO. International Organization for Standardization, ISO 1400X. Available online: www.iso.org (accessed on 2 November 2017).

- OHSAS 1. 8001. Available online: https://www.bsigroup.com/en-GB/ohsas-18001-occupational-health-and-safety/ (accessed on 2 November 2017).

- Social Accountability International (SAI). Social Accountability 8000 International Standard. SA8000. 2014. Available online: http://sa-intl.org/_data/n_0001/resources/live/SA8000%20Standard%202014.pdf (accessed on 2 November 2017).

- Global Reporting Initiative (GRI). G4 Guidelines Part 1: Reporting Principles and Standard Disclosures. 2013. Available online: https://www.globalreporting.org/resourcelibrary/GRIG4-Part1-Reporting-Principles-and-Standard-Disclosures.pdf (accessed on 2 November 2017).

- Integrated Reporting (IR). International Integrated Reporting Framework. 2013. Available online: http://integratedreporting.org/resource/international-ir-framework/ (accessed on 2 November 2017).

- Maestrini, V.; Luzzini, D.; Maccarrone, P.; Caniato, F. Supply chain performance measurement systems: A systematic review and research agenda. Int. J. Prod. Econ. 2017, 183, 299–315. [Google Scholar] [CrossRef]

- Fritz, M.M.; Schöggl, J.P.; Baumgartner, R.J. Selected sustainability aspects for supply chain data exchange: Towards a supply chain-wide sustainability assessment. J. Clean. Prod. 2017, 141, 587–607. [Google Scholar] [CrossRef]

- Yawar, S.A.; Seuring, S. Management of social issues in supply chains: A literature review exploring social issues, actions and performance outcomes. J. Bus. Ethics 2017, 141, 621–643. [Google Scholar] [CrossRef]

- Beske-Janssen, P.; Johnson, M.P.; Schaltegger, S. 20 years of performance measurement in sustainable supply chain management–what has been achieved? Supply Chain Manag. 2015, 20, 664–680. [Google Scholar] [CrossRef]

- Genovese, A.; Acquaye, A.A.; Figueroa, A.; Koh, S.L. Sustainable supply chain management and the transition towards a circular economy: Evidence and some applications. Omega-Int. J. Manag. S 2017, 66, 344–357. [Google Scholar] [CrossRef]

- Onat, N.C.; Kucukvar, M.; Halog, A.; Cloutier, S. Systems Thinking for Life Cycle Sustainability Assessment: A Review of Recent Developments, Applications, and Future Perspectives. Sustainability 2017, 9, 706. [Google Scholar] [CrossRef]

- Neugebauer, S.; Forin, S.; Finkbeiner, M. From life cycle costing to economic life cycle assessment—introducing an economic impact pathway. Sustainability 2016, 8, 428. [Google Scholar] [CrossRef]

- Wu, R.; Yang, D.; Chen, J. Social life cycle assessment revisited. Sustainability 2014, 6, 4200–4226. [Google Scholar] [CrossRef]

- Chhipi-Shrestha, G.K.; Hewage, K.; Sadiq, R. ‘Socializing’sustainability: A critical review on current development status of social life cycle impact assessment method. Clean Technol. Environ. Policy 2015, 17, 579–596. [Google Scholar] [CrossRef]

- Arcese, G.; Lucchetti, M.C.; Massa, I. Modeling Social Life Cycle Assessment framework for the Italian wine sector. J. Clean. Prod. 2017, 140, 1027–1036. [Google Scholar] [CrossRef]

- Halog, A.; Manik, Y. Advancing integrated systems modelling framework for life cycle sustainability assessment. Sustainability 2011, 3, 469–499. [Google Scholar] [CrossRef]

- Martínez-Blanco, J.; Lehmann, A.; Chang, Y.J.; Finkbeiner, M. Social organizational LCA (SOLCA)—A new approach for implementing social LCA. Int. J. Life Cycle Assess. 2015, 20, 1586–1599. [Google Scholar] [CrossRef]

- Tsalis, T.; Avramidou, A.; Nikolaou, I.E. A social LCA framework to assess the corporate social profile of companies: Insights from a case study. J. Clean. Prod. 2017, 164, 1665–1676. [Google Scholar] [CrossRef]

- Van Kempen, E.A.; Spiliotopoulou, E.; Stojanovski, G.; de Leeuw, S. Using life cycle sustainability assessment to trade off sourcing strategies for humanitarian relief items. Int. J. Life Cycle Assess. 2017, 22, 1718–1730. [Google Scholar] [CrossRef]

- Wang, S.W.; Hsu, C.W.; Hu, A.H. An analytic framework for social life cycle impact assessment—Part 1: Methodology. Int. J. Life Cycle Assess. 2016, 21, 1514–1528. [Google Scholar] [CrossRef]

- Rodríguez-Olalla, A.; Avilés-Palacios, C. Integrating Sustainability in Organisations: An Activity-Based Sustainability Model. Sustainability 2017, 9, 1072. [Google Scholar] [CrossRef]

- Govindan, K.; Khodaverdi, R.; Jafarian, A. A fuzzy multi criteria approach for measuring sustainability performance of a supplier based on triple bottom line approach. J. Clean. Prod. 2013, 47, 345–354. [Google Scholar] [CrossRef]

- Govindan, K.; Darbari, J.D.; Agarwal, V.; Jha, P.C. Fuzzy multi-objective approach for optimal selection of suppliers and transportation decisions in an eco-efficient closed loop supply chain network. J. Clean. Prod. 2017, 165, 1598–1619. [Google Scholar] [CrossRef]

- Souza, R.G.; Rosenhead, J.; Salhofer, S.P.; Valle, R.A.B.; Lins, M.P.E. Definition of sustainability impact categories based on stakeholder perspectives. J. Clean. Prod. 2015, 105, 41–51. [Google Scholar] [CrossRef]

- Varsei, M.; Soosay, C.; Fahimnia, B.; Sarkis, J. Framing sustainability performance of supply chains with multidimensional indicators. Supply Chain Manag. 2014, 19, 242–257. [Google Scholar] [CrossRef]

- Ahi, P.; Searcy, C. Assessing sustainability in the supply chain: A triple bottom line approach. Appl. Math. Model. 2015, 39, 2882–2896. [Google Scholar] [CrossRef]

- Bai, C.; Sarkis, J. Determining and applying sustainable supplier key performance indicators. Supply Chain Manag. 2014, 19, 275–291. [Google Scholar] [CrossRef]

- Beske, P.; Seuring, S. Putting sustainability into supply chain management. Supply Chain Manag. 2014, 19, 322–331. [Google Scholar] [CrossRef]

- Schöggl, J.P.; Fritz, M.M.; Baumgartner, R.J. Toward supply chain-wide sustainability assessment: A conceptual framework and an aggregation method to assess supply chain performance. J. Clean. Prod. 2016, 131, 822–835. [Google Scholar] [CrossRef]

- Rivera, J.M.; Munoz, M.J.; Moneva, J.M. Revisiting the Relationship between Corporate Stakeholder Commitment and Social and Financial Performance. Sustain. Dev. 2017, 25, 482–494. [Google Scholar] [CrossRef]

- Čuček, L.; Klemeš, J.J.; Kravanja, Z. A review of footprint analysis tools for monitoring impacts on sustainability. J. Clean. Prod. 2012, 34, 9–20. [Google Scholar] [CrossRef]

- Iansiti, M.; Levien, R. Strategy as ecology. Harv. Bus. Rev. 2004, 82, 68–81. [Google Scholar] [PubMed]

{kind=link}

| Tools and Initiatives | Sustainability Dimensions 1 | Balance | Inter-Generational Perspective | Stakeholder Approach | Life Cycle Thinking |

|---|---|---|---|---|---|

| promoted by financial market | |||||

| Sustainability agencies and indices | EC | X | ≠ | ✓ | X |

| EN | |||||

| SO | |||||

| promoted by international institutions | |||||

| Organization Environmental Footprint [63] | EN | X | ✓ | ✓ | ✓ |

| UNEP/SETAC Life Cycle Initiative [64] | SO | X | ✓ | ✓ | ✓ |

| OECD Guidelines for Multinational Enterprise [65] | EC | - | ✓ | X | ✓ |

| EN | |||||

| SO | |||||

| UN Global Compact [66] | EC | - | ✓ | X | X |

| EN | |||||

| SO | |||||

| The UN’s Principles for Responsible Investment [67] | EC | ✓ | ✓ | ✓ | X |

| EN | |||||

| SO | |||||

| promoted by multi-stakeholder international institutions | |||||

| AA1000 Assurance Standard (Accountability) [68] | EC | X | X | ✓ | X |

| EN | |||||

| SO | |||||

| CDP (the former CARBON DISCLOSURE PROJECT) [69] | EN | X | ✓ | ✓ | X |

| EMAS certification [70] | EN | X | ✓ | ✓ | ≠ Indirect aspects and product life cycle issues. |

| ISO 1400X [71] | EN | X | ✓ | ✓ | ✓ |

| OHSAS 18001 [72] | SO | - | ✓ | ✓ | X |

| SA8000 [73] | SO | - | ✓ | ✓ | X |

| ISO 26000 [11] | EC | X | ✓ | ✓ | ✓ |

| EN | |||||

| SO | |||||

| GRI Report Guidelines G4 Sustainability Reporting Guidelines [74] | EC | - | ≠ | ✓ | ≠ For some indicators direct + indirect impacts must be accounted |

| EN | |||||

| SO | |||||

| International Integrated Reporting Framework [75] | EC | - | ✓ | ✓ | X |

| EN | |||||

| SO | |||||

| Method | Author and Year | Objective | Sustainability Dimensions 1 | Balance | Inter-Generational Perspective | Stakeholder Approach | Life Cycle Thinking | |

|---|---|---|---|---|---|---|---|---|

| LCA | S-LCA | Arcese et al. [85] | To identify the socioeconomic impact subcategories and the consequent inventory indicators definition related to the five stakeholders’ categories involved in the life cycle. | SO | X | X | ✓ | ✓ |

| LCA, LCC, and S-LCA, MCDM, DEA | Halog and Manik [86] | To develop an integrated methodology by capitalizing the complementary strengths of different methods used by industrial ecologists and biophysical economists | EC | ✓ | X | ✓ | ✓ | |

| EN | ||||||||

| SO | ||||||||

| Social organizational LCA (SOLCA) | Martínez-Blanco et al. [87] | To propose a new approach, namely SOLCA and to present its first outline. Main reference: methodological documents are SLCA (UNEP/SETAC 2009) and OLCA (ISO 2014; UNEP 2015). | SO | ✓ | ✓ | ✓ | ✓ | |

| S-LCA | Tsalis et al. [88] | To provide a methodological framework for SLCA inspired by the UNEP/ SETAC guideline, which addresses and evaluates the social profile of companies using information from sustainability reports. | EC | X | X | ✓ | ✓ | |

| EN | ||||||||

| SO | ||||||||

| LCA | van Kempen et al. [89] | To contribute to the development of the field by conducting a life cycle sustainability analysis (LCSA) of sourcing scenarios for a core relief item in a humanitarian supply chain considering the ReCiPe method and UNEP/ SETAC guideline | EC | X | ✓ | ✓ | ✓ | |

| EN | ||||||||

| SO | ||||||||

| S-LCA | Wang et al. [90] | To develop a new framework of social life cycle impact assessment (SLCIA) method based on UNEP/SETAC. | SO | X | ✓ | ✓ | ✓ | |

| Activity-Based Sustainability (ABS) integration model | Rodríguez-Olalla and Avilés-Palacios [91] | To define an ABS integration model that complements other models from an inside-out perspective. | EC | X | ✓ | ✓ | ✓ | |

| EN | ||||||||

| SO | ||||||||

| Multi-criteria methods (MCDM) | Composite index | Chardine-Baumann and Botta-Genoulaz [61] | To provide a framework for sustainable performance assessment in terms of the impacts of its SCM practices | EC | ✓ | X | X | ✓ |

| EN | ||||||||

| SO | ||||||||

| Fuzzy MCDM | Govindan et al. [92] | To identify an effective model based on the TBL approach for supplier selection operations in supply chains | EC | X | X | X | X | |

| EN | ||||||||

| SO | ||||||||

| Analytic Hierarchy Process Fuzzy multi-objective model (FMOM) | Govindan et al. [93] | To present a FMOM aimed at configuring CLSC network design for product recovery, which integrates supplier selection, flow allocation, and transportation decisions. | EC | X | X | ✓ | X | |

| EN | ||||||||

| SO | ||||||||

| Multi-criteria methods | Souza et al. [94] | To define a methodological approach for the selection of LCSA impact categories based on consultation of real stakeholders. | EC | X | ✓ | ✓ | ✓ | |

| EN | ||||||||

| SO | ||||||||

| Combination of MCDM (e.g., AHP) | Varsei et al. [95] | To provide a framework which can assist focal companies in the development of sustainable supply chains. | EC | X | X | ✓ | X | |

| EN | ||||||||

| SO | ||||||||

| Probabilistic models | Ahi and Searcy [96] | To provide a probabilistic models for assessing sustainability in the supply chain | EC | X | ✓ | ✓ | ✓ | |

| EN | ||||||||

| SO | ||||||||

| DEA | Bai and Sarkis [97] | To introduce a methodology to identify sustainable supply chain Key Performace Indicator (KPI) that can be used for sustainability performance evaluation for suppliers. | EC | X | X | X | X | |

| EN | ||||||||

| SO | ||||||||

| Supply chain framework | Beske and Seuring [86] | To identify key categories of SSCM and related practices that are required to fulfill the demands of sustainability and, therefore, contributing to sustainability performance. | EC | X | ✓ | ✓ | ✓ | |

| EN | ||||||||

| SO | ||||||||

| Hoogmart-ens et al. [35] | To present a framework that clarifies the connections and coherence between these existing assessment tools | EC | X | X | X | ✓ | ||

| EN | ||||||||

| SO | ||||||||

| Schöggl et al. [99] | To provide a conceptual framework for supply chain sustainability assessment. | EC | ✓ | X | ✓ | X | ||

| EN | ||||||||

| SO | ||||||||

| Tajbakhsh, and Hassini, [34] | To analyze the reviewed literature and propose some research questions and indicators for performance measurement. | EC | X | ✓ | ✓ | X | ||

| EN | ||||||||

| SO | ||||||||

| Yawar and Seuring [78] | To explore the intersection between social issues, CSR actions and performance outcomes, offering a conceptual framework to the management of social issues in supply chain. | EC | X | X | ✓ | X | ||

| SO | ||||||||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á.; Rivera-Lirio, J.M.; Ferrero-Ferrero, I.; Escrig-Olmedo, E.; Gisbert-Navarro, J.V.; Marullo, M.C. An Assessment Tool to Integrate Sustainability Principles into the Global Supply Chain. Sustainability 2018, 10, 535. https://doi.org/10.3390/su10020535

Muñoz-Torres MJ, Fernández-Izquierdo MÁ, Rivera-Lirio JM, Ferrero-Ferrero I, Escrig-Olmedo E, Gisbert-Navarro JV, Marullo MC. An Assessment Tool to Integrate Sustainability Principles into the Global Supply Chain. Sustainability. 2018; 10(2):535. https://doi.org/10.3390/su10020535

Chicago/Turabian StyleMuñoz-Torres, María Jesús, María Ángeles Fernández-Izquierdo, Juana M. Rivera-Lirio, Idoya Ferrero-Ferrero, Elena Escrig-Olmedo, José Vicente Gisbert-Navarro, and María Chiara Marullo. 2018. "An Assessment Tool to Integrate Sustainability Principles into the Global Supply Chain" Sustainability 10, no. 2: 535. https://doi.org/10.3390/su10020535