1. Introduction

The problem of the deterioration of the ecological environment hinders the sustainable development of the economy and society. The regulatory authorities regard environmental information disclosure (EID) as a governance method to compel firms to fulfill their environmental responsibilities and exhibit environmentally friendly behavior [

1,

2]. The listed firms in high-polluting industries are considered the biggest perpetrators of natural environmental pollution and are subject to rigorous scrutiny and high expectations in terms of EID behavior [

3,

4]. However, many firms comply symbolically with low-quality reports, or even opportunistically use EID to overstate their actual environmental performance [

5,

6]. Thus, it is imperative to find ways to prompt high-polluting firms to conduct substantive environmental protection behavior and engage in high-quality EID.

Governments have actively implemented a wide spectrum of formal environmental regulations and policies to urge firms to disclose their environmental information. Command-oriented regulation highlights the regulatory pressure from the government sector, including political embeddedness [

7,

8,

9] and legal regulation [

10,

11]. Meanwhile, market-based regulations emphasize the effect of economic incentive means, such as environmental tax [

12], emission charges [

13,

14,

15], and environmental subsidies [

16]. However, few studies have explored how informal regulations such as social media influence corporate EID behavior. In particular, recent studies have been appealing for a greater focus on the role of social media in corporate environmental governance [

17], rather than passively responding to external pressure or fitting the existing requirements.

Despite the academic attention directed towards the relationship between social media and corporate voluntary information, the empirical findings remain limited and controversial. Some scholars find that social media plays an active supervisory role in constraining corporate violation disclosure and enhancing the quality of information disclosure [

18,

19,

20]. Lei et al. [

19] demonstrate that Twitter-adopting firms are more active in releasing more transparent voluntary nonfinancial information. Lyon and Montgomery [

21] suggest that social media increases the information supply to a variety of stakeholders and enables external stakeholders to detect and penalize enterprises for corporate greenwashing behavior. Other scholars reveal opposite evidence, contending social media has a negative effect on voluntary information disclosure [

22]. Intense social media attention exposes corporate management to tremendous pressure and highlights expectations, thus compelling firms to engage in low-quality symbolic disclosure to depict an environmentally friendly image and maintain legitimacy [

23,

24]. Therefore, the relationship between social media and corporate voluntary information disclosure is highly important and controversial. Additionally, the existing literature lacks studies that focus on the impact of social media on corporate EID. Thus, this paper investigates how firm–investor social media interactions may affect the EID behavior of high-polluting enterprises.

China offers a unique and interesting setting to investigate this issue. First, the lack of definite disclosure standards and weak enforcement information disclosure regulations leaves Chinese firms with a high level of discretion to determine what to disclose in environmental reports and how [

6,

18]. The quality and credibility of corporate EID in China have been subject to severe criticism [

5,

6]. A new force is required to supervise corporate EID behavior beyond formal regulations. Second, retail investors are the main participants in the Chinese capital market. According to the statistics of the China Securities Depository and Clearing Corporation (CSDC), small investors account for almost 99.77% of the market participants in China. Thus, they play a vital role in supervising corporate behavior. Third, on 1 January 2010, the Shenzhen Stock Exchange released the first interactive platform in China, called “Hudongyi”, (Available online:

http://irm.cninfo.com.cn (accessed on 1 March 2022)) to facilitate a two-way interaction between listed companies and investors. Shortly after, the Shanghai Stock Exchange (SSE) introduced a similar online platform, named “easy interaction” (Available online:

http://sns.sseinfo.com (accessed on 1 March 2022)). These two novel official social media platforms offer an ideal opportunity for small investors to participate in corporate decisions through asking questions and requesting replies from corporate management.

Based on a sample of heavy-polluting Chinese firms listed in the Shenzhen and Shanghai Stock Exchanges from 2010 to 2019, we first explore how social media interaction impacts the EID quality of high-polluting enterprises. The results show that social media interaction indeed promotes the EID quality of high-polluting enterprises, which supports the monitoring role of social media. This finding is robust to a variety of alternative estimation approaches and alternate measures of core variables. In addition, we examine the mechanism through which social media influences EID from the three perspectives of information function, regulatory intervention, and market pressure. The empirical results show that the positive relationship between social media and EID is more significant for enterprises with high analyst coverage and for state-owned enterprises (SOEs). However, the positive relationship is weaker for firms whose CEOs hold chairman positions (i.e., CEO duality). In a supplementary analysis, we also analyze the heterogeneous effects of social media on EID types and the topic of social media interaction. We find that social media interaction promotes hard EID to a larger extent than soft information disclosure, and the effect of environment-related posts is more pronounced than non-environment-related posts.

This study contributes to the existing literature in the following three ways. First, this study enriches research on the determinants of corporate EID in the Chinese context. Most prior studies shed considerable light on formal institutions, such as command-oriented regulations [

10,

11,

25] or market-based regulations [

12,

13,

14], but ignore the influence of informal regulations, such as social media interaction. This study introduces social media as a supplement for formal regulation in supervising EID activities through facilitating the expression of individual investors’ voices and empowering individual investors to participate in the supervision of corporate EID behavior. Thus, we identify a new method of corporate environmental governance and respond to the call for a more in-depth investigation of cross-disciplinary research on social media and corporate environmental governance [

26,

27].

Second, this paper extends the literature on the consequences of social media interaction on corporate EID decision making. In contrast to prior research that predominantly focuses on how social media is used by listed firms to disseminate their environmental protection efforts from the information perspective [

28,

29,

30], this paper sheds light on how social media interaction exerts pressure on firms to enhance EID quality from the governance perspective. This research adds empirical evidence that social media is a double-edged sword [

17], as it not only benefits firms through accelerating the transfer of desired information to a wider audience, but also mobilizes the enthusiasm of external constituents towards participating in the supervision of corporate behavior.

Third, this paper contributes to the social media literature by elaborating the mechanism through which social media influences EID decisions. While previous research has provided evidence on the positive impact of social media on corporate non-financial disclosure, it is still not very clear how social media influences corporate EID decisions [

18,

19,

20]. We conduct a mechanism-based analysis to verify the three mechanisms of information function, market pressure, and government intervention, which strengthens our understanding of how social media influences corporate EID decisions.

3. Research Design

3.1. Sample Selection and Data Sources

The initial sample included Chinese A-share high-polluting enterprises from 2010 to 2019. This study chose 2010 as the starting year of the sample because the Shenzhen Stock Exchange developed the first online interactive platform, called “Hudongyi”, in 2010. Before that, no official E-interactive platform existed for the direct exchange between investors and listed firms. We identified 16 high-polluting industries (thermal power, steel, cement, electrolytic aluminum, coal, metallurgical, chemical, petrochemical, building materials, papermaking, brewing, pharmaceutical, fermentation, textile, leather, and mining) based on the “Guidelines on environmental information disclosure of the listed companies” issued by the Ministry of Environmental Protection of the People’s Republic of China in 2010.

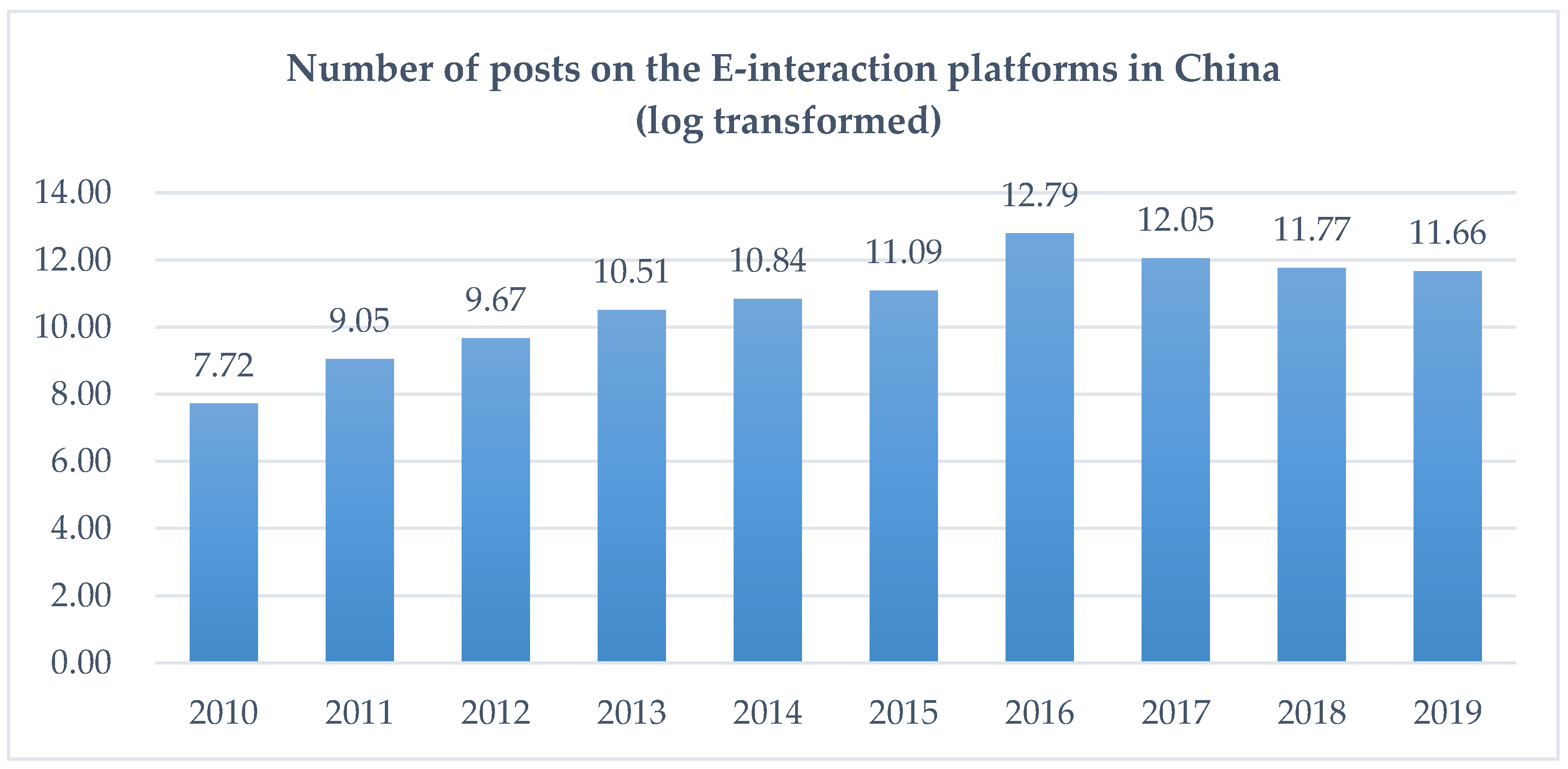

We used the unique and detailed original posting data on the E-interaction platforms initiated by the Shanghai and Shenzhen Stock Exchange. This context offered a unique opportunity to test our theoretical hypotheses. First, in contrast to other online platforms, such as Twitter, Microblog, and Stock Message Boards, which lack the supervision of official regulation, the E-Interaction platform is built under the supervision of the stock exchange, and its operating environment is more reliable. Firms are required by the stock exchange to check the questions in the E-Interaction platform on time and reply within two days. In this sense, corporate management’s identification of the internet stakeholders’ opinions expressed on this platform is expected, and the latter has a stronger influence on corporate decisions than other social media platforms. Second, this platform establishes a Q and A section, and all the Q and A records are open to all visitors, including usernames, user IDs, and the dates and contents of posts, as well as the firms’ replies. This setup provided the access to the data for our study. As shown in

Figure 1, the volume of postings on the E-interaction platforms increased gradually in China from 2010 to 2019.

The data sources of our study are listed as follows: (1) Data on social media interaction were collected from the official E-interactive platforms initiated by the Shanghai and Shenzhen Stock Exchange. We used the Python program to automatically crawl all the detailed original postings data for each firm via the two E-interactive platforms from 2010 to 2019. (2) The information on corporate EID was manually extracted using the content analysis of corporate annual reports or corporate social responsibility reports. (3) Data on corporate ownership, analyst coverage, and basic financial indicators were collected from the China Stock Market and Accounting Research (CSMAR) database, which has been widely used in prior research [

4,

5,

20].

After merging the above datasets, the following steps were taken for the sample selection process: (1) we excluded firms with abnormal financial conditions, such as those defined as ST and *ST companies. (2) We removed observations with at least one missing control variable. Finally, a total of 13,936 firm-year effective observations from 2211 enterprises were obtained.

3.2. Variables and Models

3.2.1. Corporate EID

The content analysis method is a mainstream method to measure enterprise EID quality in existing studies. Following prior research [

1,

2,

3], this study assessed the quality of EID through adopting the 10-item list of the environmental information disclosure evaluation system. The ten items include both hard and soft information disclosures. The scoring index consists of the following 10 items: (1) corporate investment in environmental protection and green technology; (2) government subsidies and grants related to environmental protection; (3) pollution emission and reduction; (4) ISO environmental system certification; (5) actions taken to improve the natural environment; (6) the influences of environmental protection policies; (7) loans for environmental protection; (8) litigation, penalties, and awards associated with the environment; (9) goals and visions concerning corporate environmental protection; and (10) other issues of expenditure and income related to the environment. From the above scoring index, items (1), (2), (3), (6), (7), (8), and (10) represent quantitative and monetary information, and are classified as hard information disclosures, whereas (4), (5) and (9) represent qualitative non-monetary information and are classified as soft information disclosures.

For each item, we assigned 0 points in the case of non-disclosure, 1 point for quantitative disclosure, 2 points for non-monetary information disclosure, and 3 points for qualitative monetary information disclosure [

47]. Each enterprise obtains an aggregate score by adding the score of each item using the following formula:

where

is the total score of the EID quality for the firm i in the year of t, and

is the score of the item j for the firm i in the year of t. The variable j covers data between a score of 1 and 10 in the scoring index. A larger value suggests a higher quality of the corporate environmental disclosure.

3.2.2. Social Media Interaction

Following prior studies [

39,

40,

41], we used the number of questions posted on the E-interaction platforms to indicate the level of social media interaction. We first created a continuous variable, INTERACT, calculated via the natural logarithm of one plus the total number of effective questions (i.e., questions with management replies) posted by the individual investors on the E-interactive platforms for each firm. For the robustness test, we also used the natural logarithm of one plus the total number of words of each question for each firm as a proxy for social media interaction. A larger value indicates a stronger firm–investor interaction on social media platforms.

3.3. Model Building

To test H1 and examine the relationship between social media interaction and EID quality, this study employs the ordinary least squares (OLS) regression, and the regression model is designed as follows:

Among the above models, is the dependent variable, representing the quality of the corporate environmental disclosure of firm i in year t + 1. is the number of questions posted on the E-interactive platforms of firm i in year t. is the random error. A positive and statistically significant in model (1) would support H1.

To eliminate potential confounding effects, we included a series of control variables that may influence the impact of social media activism on EID. Referring to the prior literature ([

6]), we controlled the firm size (SIZE), which is calculated as the natural logarithm of the total assets of the firm. To control the profitability of polluting firms, we included the ROA, which was measured via the net income divided by the total assets of the firm. The leverage of the firm (LEV) was measured using the total debt over the total assets. We also considered several corporate governance factors. We controlled the size of the board of directors (BOARD), the proportion of independent directors on the board (INDEP), the shareholding ratio of the largest shareholder (TOP1), and the institutional ownership (INS). Moreover, we controlled the regional market development level (MARKET) by using the provincial marketization index developed by Fan et al. [

53].

Table 1 presents the definitions of the variables used in this study.

7. Discussion

7.1. Practical Implications

Our research has several important practical implications. First, the government and policymakers should fully recognize the importance of social media supervision in promoting the green transformation of listed firms in this new era of information and take measures to guide enterprises in strengthening the participation of online interactions with investors on social media platforms. According to our results, social media interaction is an effective external supervision force with a practical significance for prompting the high-quality disclosures of heavy-polluting enterprises. Our research demonstrates that stimulating the efficiency of external governance by giving full play to the supervisory role of social media is the key to enhancing the EID quality of highly polluting enterprises. Thus, the government should implement measures, including the formulation of related regulations, to seek firms’ assurance on the reliability of online participation and integrate the online interaction quality into listed companies’ information-disclosure-performance evaluations.

Second, high-polluting firms, especially those owned by the state and receiving intensive analyst coverage, should be fully aware of the challenges brought about by the new media environment and adopt proactive information disclosure strategies. According to the analysis above, social media empowers individual investors to voice their concerns to management directly and to tap into the wisdom of the crowd, which triggers market pressure and regulatory pressure for enterprises and influences corporate EID decisions. Therefore, as the main perpetrators of ecological deterioration, high-polluting firms should respond actively to social media pressure and adopt substantial environmental actions to express their commitment and effort to fulfill sustainable development instead of complying symbolically through unverified information disclosure. Specifically, when targeted by intense social media activism, high-quality EID and increased hard information disclosure are encouraged for firms to cope with external institutional environmental pressure.

Third, analysts—as important information intermediaries—should play a more active role in supervising enterprises’ EID behavior. Analyst coverage can largely alleviate the problem of information asymmetry inside and outside the enterprise and exert pressure on the top executives to restrict window dressing regarding EID behaviors. Our empirical results demonstrate that analyst coverage will aggravate firms’ vulnerability to social media pressure and strengthen firms’ motivation to adapt EID as a way of cultivating legitimacy. Thus, analysts should place more emphasis on the environmental aspects of listed enterprises when they release stock reports or make stock recommendations, especially for those enterprises with poor environmental performance or low EID quality.

7.2. Limitations and Future Research Directions

There are some limitations that can be further explored in future research. First, while we take the E-interaction platforms initiated by the stock exchanges as the research scenario, many other new media platforms, such as Guba, Weibo, and WeChat, persistently provide good channels for market participants to exchange information. Despite being useful representatives, E-interaction platforms are unable to fully cover the interactions between firms and their investors. Greater attention should be focused on the influence of these social media platforms. Second, we did not distinguish between the positive or negative emotions of each question on the E-interaction platforms. Instead, we only assumed that the questions posted on the platforms were equally important, which would put pressure on the corporation and would in turn influence corporate EID behavior, regardless of whether their emotions were positive or negative. Future research should further explore the detailed textual features of social media posts, such as emotions and readability. Third, we contextualized this research in China, a developing country where the weak enforcement of information disclosure regulations and the imperfect government regulation system blunt the effectiveness of formal regulations. However, whether the findings are applicable to other developed countries remains to be explored. Future studies should examine our conclusions in developed countries where the formal regulations are strict.

8. Conclusions

In this study, we investigated whether and how firm–investor social media interaction influences the EID quality of high-polluting firms in an attempt to clarify the supervisory role of social media interactions. Using panel data on Chinese high-polluting listed firms, we drew the following conclusions:

First, the empirical results show that firm–investor social media interactions can significantly promote the EID quality of high-polluting firms, confirming the supervisory role of social media in promoting substantial information disclosure. The extant literature mainly focused on offline, formal institutions such as command-control regulation [

7,

8,

9,

10,

11] and market-incentive regulations [

12,

13,

14,

15,

16]. To our knowledge, this study is one of the very few to investigate the impact of social media interaction on corporate EID. This study demonstrates that social media interaction can relieve information asymmetry between firms and external stakeholders and trigger both market and regulatory pressure for the firms; therefore, it compels firms to implement high quality environmental disclosures. Our results are consistent with those of Fan et al. [

18] and Lei et al. [

20], verifying that social media supplements formal regulation in empowering environmental activism and responds to the call for a more in-depth investigation of how changes in information technology, such as the application of social media, affect corporate disclosure practices [

14,

32,

36].

Second, this study further reveals that the positive impact of social media interaction on EID is moderated by financial analyst coverage, state-owned property rights, and CEO duality. The results show that the promoting effect of social media interaction on EID is more pronounced for enterprises with a high level of financial analyst coverage and for state-owned enterprises but is weaker for enterprises whose CEOs hold a chairman position. The above results demonstrate that analysts serve as key information intermediaries in the capital market through which social media pressure is transformed into corporate EID decisions [

66], and that the impact of social media on corporate EID behavior depends heavily on firms’ property rights and CEO’s discretion power. These findings strengthen our understanding of the underlying mechanism through which social media affects the EID of high-polluting firms.

Third, the heterogeneity analysis shows that social media interaction promotes hard information disclosure to a larger extent than soft information disclosure. This result further confirms the effectiveness of social media in putting pressure on high-polluting enterprises to implement substantial environmental actions and is in accordance with the view in previous studies that enterprises tend to disclose more detailed environmental information and take substantive measures under greater legitimacy pressure [

47,

67,

68]. Moreover, we also consider the topic of social media interaction, and we found that not only environment-related posts, but also non-environment-related posts, can promote the EID of high-polluting enterprises; however, the impact of environment-related posts is more pronounced. This finding echoes the notion in the prior literature [

19,

40,

63] that the attention brought by social media puts pressure on the management and prompts them to behave in a more conservative and honest manner.

{kind=link}