Economic Forest Sustainability: Comparison between Lithuania and Sweden

Abstract

:

1. Introduction

2. Concepts and Methods

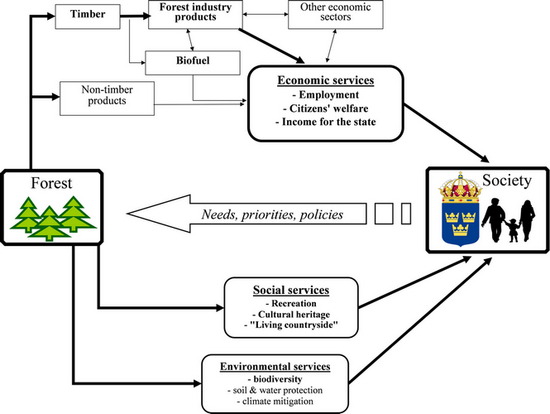

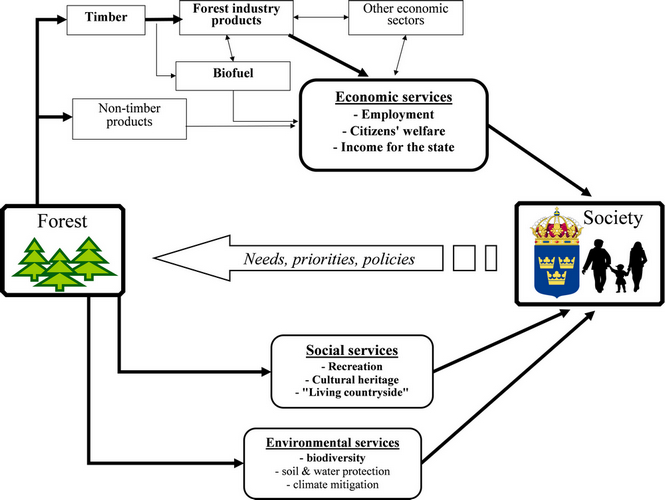

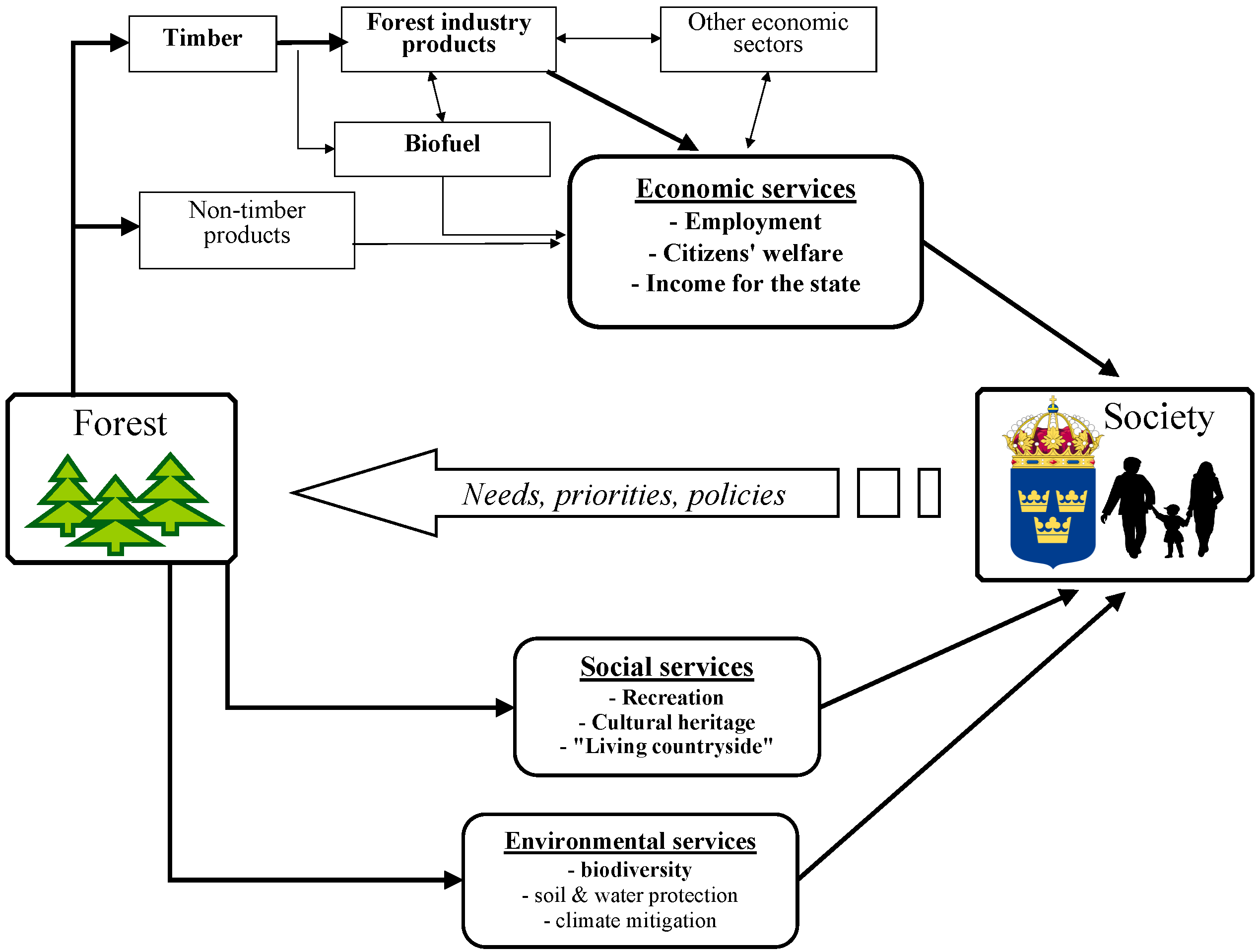

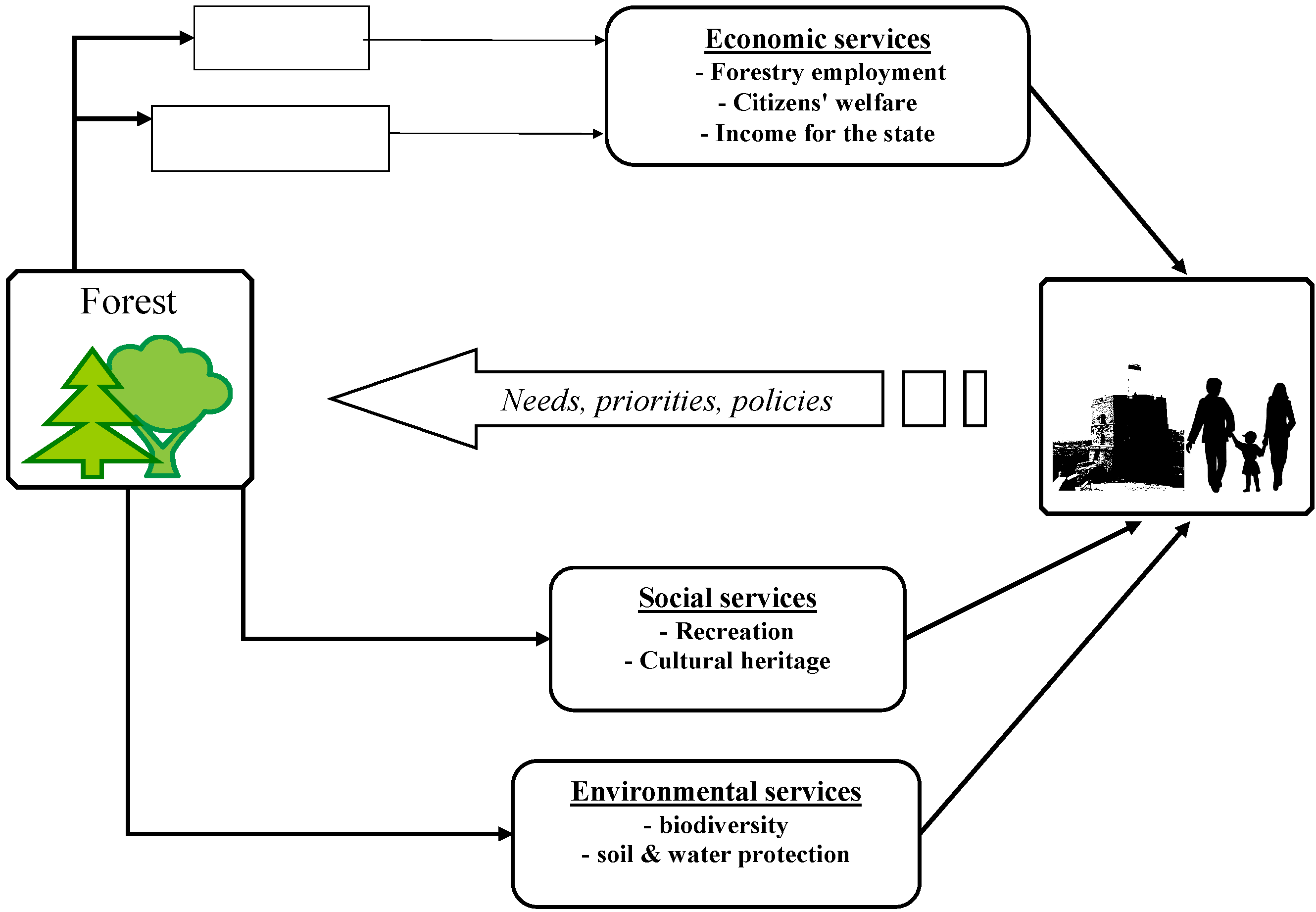

2.1. Conceptualizing Economic Forest Sustainability

2.2. Analysis at Macro Level

2.3. Analysis at the Micro Level

3. Results

3.1. Macro Level: Economic Sustainability for Society

3.1.1. Sweden: A Forest Sector Perspective

3.1.2. Lithuania: A Forestry Perspective

3.1.3. Comparison of Macro Indicators

{kind=link}

{kind=link}

{kind=link}

| Lithuania (LT) | Sweden (SE) | % Difference | |

|---|---|---|---|

| Average annual harvest/increment ratio, % (2003–2012) | 50 | 76 | |

| Employment in forestry, people (2012) | 10,900 | 15,700 | |

| Employment in forestry, people/million ha forest (2012) | 5450 | 680 | 701 |

| Employment in the forest sector (excluding furniture) (2012) | 35,300 | 74,700 | |

| Employment in the forest sector, people/million ha forest (2012) | 17,650 | 2554 | 591 |

| Average nominal price of conifer sawn timber, Euro/m3 (2010–2012) | 46.8 | 57.1 | |

| Average nominal price of conifer pulpwood, Euro/m3 (2010–2012) | 30.1 | 35.3 | |

| Total annual value of timber harvests, million Euros (2012 in LT, 2011 in SE) | 292 | 3364 | |

| Total annual value of industrial forest production, million Euros (2012 in LT, 2010 in SE) 1 | 966 | 23,219 | |

| Value of industrial forest production 1/value of timber harvests | 3.3 | 6.9 | |

| Total value of forest sector production 1/forest area, Euro/ha (2012 in LT, 2010 in SE) | 629 | 1032 | −64 |

| Total forest industrial production 1/harvested timber, euro/m3 (2010) | 121 | 319 | −164 |

3.2. Micro Level: Forest Owner Perspective

| Lithuania (LT) | Sweden (SE) | |

|---|---|---|

| FM paradigm | The FM ideal: to obtain even, maximized timber flow of sawlog dimensions | Key aims: to support industries with pulpwood and timber; to secure preconditions for profitable forestry |

| Forestry strongly regulated; similar regimes in state and private forests | Large FM freedom, environmental consideration mainly through voluntary commitments | |

| Landscape-level FM model | - Lithuanian FM is based on forestland zoning into functional forest groups, defining | - Regulation is minimal at the landscape level; some restrictions apply at property level, including the percentage of the area that can be clear-felled |

| permissible FM regimes for each group - Annual allowable cuts based on age class control | ||

| Stand-level FM model | Prevailing model is even-aged FM with final clear or selective felling, often forming mixed semi natural stands: | Prevailing model: even-aged management of conifer monocultures, prevalently spruce: |

| - Natural regeneration as common as artificial (~50%) | - Artificial forest regeneration prevails (70%), with spruce as the dominant species (85%) (S. Sweden) | |

| - Thinning systems of rather low intensity, targeting maximum sawlog production at the end of rotation | - Rather intensive thinnings to “purify” species composition, improve stand structure and serve as a source of intermediate revenues | |

| - MARAs fixed for species and forest groups | - MARAs differentiated by site productivity, 60–90 years for pine and 45–90 years for spruce | |

| - Environmental requirements include minimum quantities of deadwood and biodiversity trees |

| Group I | Group II | Group III | Group IV | Total | |

|---|---|---|---|---|---|

| Forest reserves | Protected forests | Protective forests | Commercial forests | ||

| Silvicultural activity | Not allowed | Yes | Yes | Yes | |

| Clear felling | Not allowed | Not allowed | Up to 5 ha | Up to 8 ha | |

| MARA pine, years | - | 171 | 111 | 101 | |

| MARA spruce, years | 121 | 81 | 71 | ||

| Area distribution of private forests, % | - | 9 | 20 | 71 | 100 |

| Silvicultural measure | Scots pine | Norway spruce | ||

|---|---|---|---|---|

| Stand age | Cash flow, Euro/ha | Stand age | Cash flow, Euro/ha | |

| Forest regeneration | 0 | −652 | 0 | −941 |

| Pre-commercial thinnings | 5 | −87 | 5 | −87 |

| 15 | −72 | 15 | −72 | |

| 25 | −24 | |||

| Commercial thinnings | 25 | 211 | 45 | 685 |

| 45 | 487 | |||

| 65 | 601 | |||

| Final felling, following ARAs | ||||

| - Sweden | 65 | 6,283 | 60 | 7,848 |

| - Lithuania, Group IV | 101 | 9,557 | 71 | 9,493 |

| - Lithuania, Group III | 111 | 10,178 | 81 | 10,807 |

| - Lithuania, Group II | 171 | 11,178 | 121 | 13,419 |

| Tree species | Southern Sweden | LT Group IV | LT Group III | LT Group II | ||||

|---|---|---|---|---|---|---|---|---|

| NPV, €/ha | % a | NPV, €/ha | % | NPV, €/ha | % | NPV, €/ha | % | |

| Scots pine | 5891 | 100 | 3147 | 53 | 2447 | 42 | 629 | 11 |

| Norway spruce | 6633 | 100 | 5887 | 89 | 4768 | 72 | 1727 | 26 |

4. Discussion

4.1. Key Findings: Lithuania versus Sweden

4.2. Implications for Policy

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Duncker, P.S.; Barreiro, S.M.; Hengeveld, G.M.; Lind, T.; Mason, W.L.; Ambrozy, S.; Spiecker, H. classification of forest management approaches: A new conceptual framework and its applicability to European forestry. Ecol. Soc. 2012, 17, 51. [Google Scholar]

- Brukas, V.; Weber, N. Forest management after the economic transition-at the crossroads between German and Scandinavian traditions. For. Policy Econ. 2009, 11, 586–592. [Google Scholar] [CrossRef]

- Brukas, V.; Sallnäs, O. Forest management plan as a policy instrument: Carrot, stick or sermon? Land Use Policy 2012, 29, 605–613. [Google Scholar] [CrossRef]

- Brukas, V.; Felton, A.; Lindbladh, M.; Sallnäs, O. Linking forest management, policy and biodiversity indicators—A comparison of Lithuania and Southern Sweden. For. Ecol. Manag. 2013, 291, 181–189. [Google Scholar] [CrossRef]

- Enander, K.G. Skogsbruk på Samhälles Villkor; Department of Forest Ecology and Management: Umeå, Sweden, 2007. [Google Scholar]

- Brukas, V.; Helles, F.; Tarp, P.; Thorsen, B.J. Discount rate and harvest policy: Implications for the Baltic forestry. For. Policy Econ. 2001, 2, 143–156. [Google Scholar] [CrossRef]

- Lithuanian Statistical Yearbook of Forestry; Ministry of Environment of the Republic of Lithuania (MERL): Kaunas, Lithuania, 2013.

- Swedish Statistical Yearbook of Forestry; Swedish Forest Agency, NRS Tryckeri AB: Huskvarna, Sweden, 2013.

- Carlowitz, H.C.V. Sylvicultura Oeconomica oder Hauswirthliche Nachricht und Naturgemäße Anweisung zur Wilden Baum-Zucht; UBA: Leipzig, Braun, Germany, 2000. [Google Scholar]

- Hytönen, M. History, evolution and significance of the multiple-use concept. In Multiple-Use Forestry in the Nordic Countries; Hytönen, M., Ed.; METLA, Finnish Forest Research Institute, Helsinki Research Centre: Helsinki, Finland, 1995; pp. 43–65. [Google Scholar]

- United Nations. Report of the World Commission on Environment and Development; General Assembly Resolution 42/187; Oxford University Press: Oxford, UK, 11 December 1987. [Google Scholar]

- Langhelle, O. Sustainable development: exploring the ethics of “our common future”. Int. Polic. Sci. Rev. 1999, 20, 129–149. [Google Scholar] [CrossRef]

- Daly, H.E. Toward some operational principles of sustainable development. Ecol. Econ. 1990, 2, 1–6. [Google Scholar] [CrossRef]

- Verburg, R.M.; Wiegel, V. On the compatibility of sustainability and economic growth. Environ. Ethics 1997, 19, 247–265. [Google Scholar] [CrossRef]

- Giddings, B.; Hopwood, B.; O’Brien, G. Environment, economy and society: Fitting them together into sustainable development. Sustain. Dev. 2002, 10, 187–196. [Google Scholar] [CrossRef]

- Sneddon, C.; Howarth, R.B.; Norgaard, R.B. Sustainable development in a post-Brundtland world. Ecol. Econ. 2006, 57, 253–268. [Google Scholar] [CrossRef]

- Peters, D.M.; Schraml, U. Does background matter? Disciplinary perspectives on sustainable forest management. Biodivers. Conserv. 2014, 23, 3373–3389. [Google Scholar] [CrossRef]

- Anand, S.; Sen, A. Human development and economic sustainability. World Dev. 2000, 28, 2029–2049. [Google Scholar] [CrossRef]

- Improved Pan-European Indicators for Sustainable Forest Management. In Presented at Ministerial Conference for the Protection of Forests in Europe (MCPFE), Expert Level Meeting, Vienna, Austria, 7–8 October 2002.

- Grainger, A. Forest sustainability indicator systems as procedural policy tools in global environmental governance. Global Environ. Chang. 2012, 22, 147–160. [Google Scholar] [CrossRef]

- Brukas, V. New world, old ideas—A narrative of the Lithuanian forestry transition. J. Environ. Pol. Plann. 2015. [Google Scholar] [CrossRef]

- Ingemarson, F.; Lindhagen, A.; Eriksson, L. A typology of small-scale private forest owners in Sweden. Scand. J. Forest Res. 2006, 21, 249–259. [Google Scholar] [CrossRef]

- Stanislovaitis, A.; Kavaliauskas, M.; Brukas, V.; Mozgeris, G. Forest owner is more than her goal: A qualitative forest owner typology. Scand. J. For. Res. 2015, in press. [Google Scholar]

- Kuliešis, A. Forest Yield Models and Tables in Lithuania; LMS: Kaunas, Lithuania, 1993; (In Lithuanian, with English abstract). [Google Scholar]

- Kenstavičius, J.J. Normativniie Materialii dlia Taksacii lesov Litovskoi SSR i Kaliningradskoi Oblasti PSFSR (Norms for Forest Inventory in Lithuanian SSR and Kaliningrad Region of the RSFSR); Tipografija Preiskurantizdata: Moscow, Russia, 1987. (In Russian) [Google Scholar]

- Directorate General of State Forests (at the Ministry of Enviroment Republic of Lithuania). Available onlie: www.gmu.lt (accessed on 10 November 2014).

- Klemperer, W.D. Forest Resource Economics and Finance; McGraw-Hill Inc.: New York, NY, USA, 1996. [Google Scholar]

- Roos, A. The Economics of Forest Ownership; Report No 42; The Swedish University of Agricultural Sciences: Uppsala, Sweden, 1996. [Google Scholar]

- Södra. Available onlie: http://www.sodra.com/en/ (accessed 3 May 2013).

- Hysing, E.; Olsson, J. Contextualising the Advocacy Coalition Framework: Theorising Change in Swedish Forest Policy. Environ. Polit. 2008, 17, 730–748. [Google Scholar] [CrossRef]

- Lidskog, R.; Sjödin, D. Why do forest owners fail to heed warnings? Conflicting risk evaluations made by the Swedish Forest Agency and forest owners. Scand. J. For. Res. 2014, 29, 275–282. [Google Scholar]

- Boström, M. How State-Dependent is a Non-State-Driven Rule-Making Project? The case of forest certification in Sweden. J. Environ. Policy Plann. 2003, 5, 165–180. [Google Scholar] [CrossRef]

- Brukas, V.; Linkevičius, E.; Činga, G. Policy drivers behind forest utilisation in Lithuania in 1986–2007. Balt. For. 2009, 15, 86–96. [Google Scholar]

- Morkevičius, A. Lithuanian Timber Sector Continues to Increase the Processing Capacity and Exports. Portal of the Lithuanian Forest Owner Association: LMSA, Vilnius, Lithuania, 2012. Available online: www.forest.lt/ (accessed on 15 September 2014).

- Brukas, V.; Kuliešis, A.; Sallnäs, O.; Linkevičius, E. Resource availability, planning rigidity and Realpolitik in Lithuanian forest utilization. Nat. Res. Forum 2011, 35, 77–88. [Google Scholar] [CrossRef]

- Thorsen, B.J. Spatial Integration in the Nordic timber market: Long-run equilibria and short-run dynamics. Scand. J. For. Res. 1998, 13, 488–498. [Google Scholar] [CrossRef]

- LD (Landsbygdsdepartementet), Skogsvårdsförordning (Forestry Act); Ministry of Rural Affairs: Stockholm, Sweden, 1993.

- LRS (Lietuvos Respublikos Seimas). Forest Act of the Lithuanian Republic; Valstybės žinios LRS: Vilnius, Lithuania, 2011. [Google Scholar]

- Mizaraitė, D. Forest Ownership Objectives and Private Forestry Problems: Gender Aspects; Research Report; Lithuanian Forest Research Institute: Girionys, Lithuania, 2005. [Google Scholar]

- Felton, A.; Lindbladh, M.; Brunet, J.; Fritz, O. Replacing coniferous monocultures with mixed-species production stands: An assessment of the potential benefits for forest biodiversity in Northern Europe. Forest Ecol. Manag. 2010, 260, 939–947. [Google Scholar] [CrossRef]

- Naturvårdsverket. Miljömålen. Årlig Uppföljning av Sveriges Miljökvalitetsmål och Etappmål 2014 (Environmental Objectives. Annual Follow up of the Swedish Environmental Objectives and Partial Objectives 2014); Swedish Environmental Protection Agency: Stockholm, Sweden, 2014. [Google Scholar]

- Pilot Study on National Forest Programme in Sweden—An External Analysis; Swedish Forest Agency (SFA): Jönköping, Sweden, 2013.

- Ministry of Rural Affairs. Hur ska dialogprocessen genomföras? (How will the process of dialogue be implemented?). Available online: www.regeringen.se/content/1/c6/24/21/29/25fa4d5b.pdf (accessed on 12 November 2014).

- Glück, P.; Humphreys, D. National Forest Programmes in a European context: Findings from COST Action E19. For. Policy Econ. 2002, 4, 253–258. [Google Scholar] [CrossRef]

- Nilsson, S. Experiences of policy reforms of the forest sector in transition and other countries. For. Policy Econ. 2005, 7, 831–847. [Google Scholar] [CrossRef]

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Brukas, V.; Mizaras, S.; Mizaraitė, D. Economic Forest Sustainability: Comparison between Lithuania and Sweden. Forests 2015, 6, 47-64. https://doi.org/10.3390/f6010047

Brukas V, Mizaras S, Mizaraitė D. Economic Forest Sustainability: Comparison between Lithuania and Sweden. Forests. 2015; 6(1):47-64. https://doi.org/10.3390/f6010047

Chicago/Turabian StyleBrukas, Vilis, Stasys Mizaras, and Diana Mizaraitė. 2015. "Economic Forest Sustainability: Comparison between Lithuania and Sweden" Forests 6, no. 1: 47-64. https://doi.org/10.3390/f6010047