Pitfalls of the EU’s Carbon Border Adjustment Mechanism

1

Korea Maritime Institute, Pusan 4911, Korea

2

Graduate School of Arts and Science, New York University, New York, NY 10016, USA

3

Department of International Trade, Sunchon National University, Sunchon 57922, Korea

4

Korea Maritime Institute, Busan 4911, Korea

5

Department of International Trade, Inha University, Incheon 22212, Korea

*

Author to whom correspondence should be addressed.

Energies 2021, 14(21), 7303; https://doi.org/10.3390/en14217303

Submission received: 15 October 2021

/

Revised: 26 October 2021

/

Accepted: 27 October 2021

/

Published: 4 November 2021

(This article belongs to the Special Issue Energy Policy for a Sustainable Economic Growth)

Abstract

:The European Union (EU), which has led international discussions on global warming, officially announced its plan for the Carbon Border Adjustment Mechanism (CBAM) in July 2021. Many existing studies have indicated the CBAM will curtail greenhouse gases, and will subsequently be positive in terms of reducing global warming. However, serious legal issues and trade disputes are expected in terms of the compatibility of the CBAM with the trade rules of the General Agreement on Tariffs and Trade (GATT). Contrary to the EU’s explanation, the international community has a strong view of CBAM as a new trade barrier under the guise of preventing global warming. Above all, this is because it is an arbitrary measure by the EU and not the one that has been internationally agreed upon. Therefore, this paper tries to identify the pitfalls and estimate the global cost of CBAM, arguing that the mechanism is not in line with international trade rules, and that many countries will not sit back and suffer from it. The world economy will inevitably face a vicious cycle of trade retaliation. The CBAM will drive up trade costs and cause another trade distortion. While the goal of preventing climate change is good, the CBAM scheme is too costly for the world economy.

1. Introduction

Although international consensus in acknowledging and making efforts to prevent global warming has been established, it is difficult to reach an international agreement on practical measures to reduce greenhouse gases, because such an agreement could have an immense impact on international trade and national interests. The European Union (EU), which has led discussions on global warming, confirmed the implementation of the Carbon Border Adjustment Mechanism (CBAM) in July 2021, and subsequently publicized the carbon border tax for the international community. While countries certainly concur on the necessity for a sustainable development mechanism to reduce greenhouse gases, some have revolted against the CBAM. To circumvent such resistance, the EU says the CBAM is not a tariff, and that part of the carbon border tax will be allocated to supporting the development of energy technology. Despite this suggestion, it can surely be understood that the CBAM is means of imposing unilateral trade barriers on imports [1,2,3,4].

This paper researches and explains the effects from the CBAM implementation in a comprehensive and thorough manner. Many previous studies, including [5,6,7,8,9] and others, have failed to consider the side effects that the implementation of the CBAM will bring. As many studies have indicated, the effects of the CBAM will clearly curtail greenhouse gases, and will subsequently be positive in terms of reducing global warming. However, serious trade disputes and legal issues have been raised in terms of its compatibility with the current the General Agreement on Tariffs and Trade (GATT) and World Trade Organization (WTO) rules. The implementation of the CBAM could evoke trade conflicts and retaliation due to its imposition of new unilateral tariffs, which is incompatible with the GATT/WTO system [10,11,12,13,14,15].

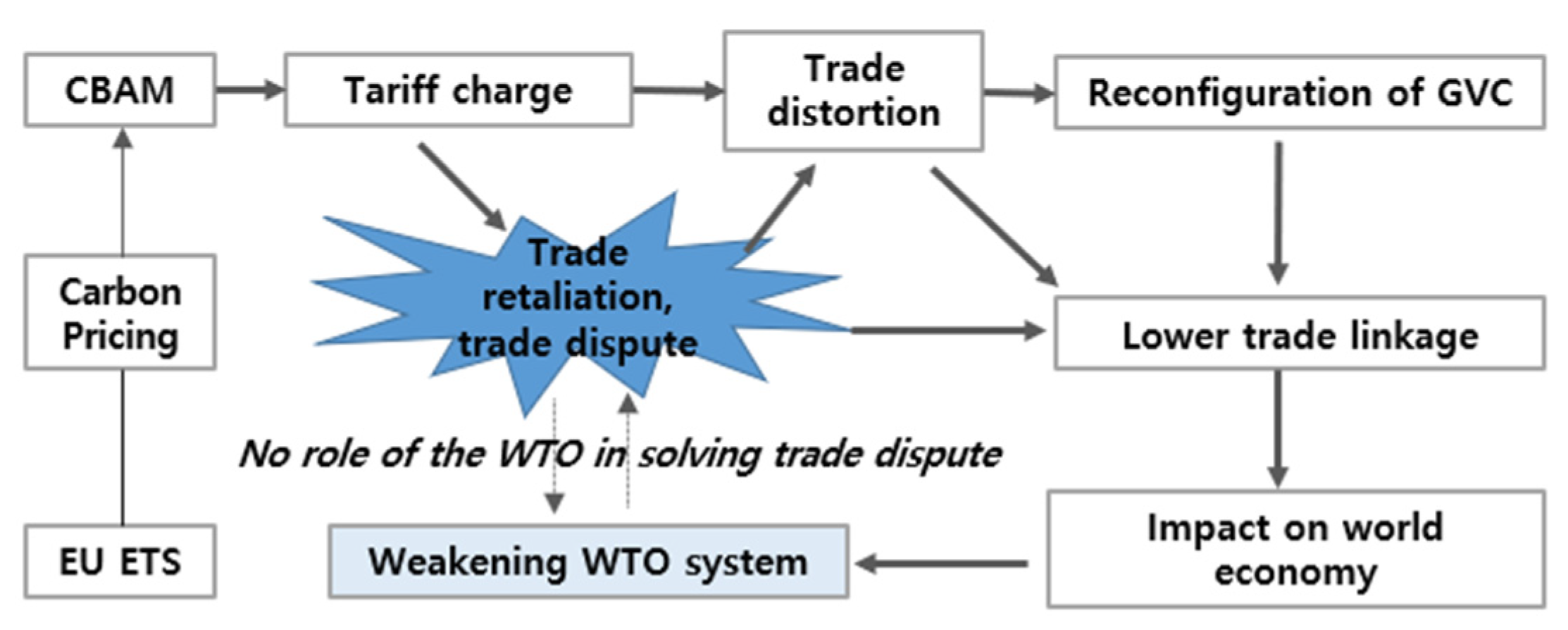

Since the CBAM may not be compatible with GATT/WTO trade rules, international controversy is likely. This paper will (1) discuss the legal issues caused by unilateral CBAM implementation, and (2) estimate the global economic loss generated by subsequent trade retaliation. Furthermore, due to the Appellate Body crisis, the WTO dispute settlement system will work properly, which may ultimately impact the global trade environment to an extent worse than the double whammy losses from the U.S.–China conflict and the COVID-19 pandemic. Trade retaliation causes global supply chains to be reconfigured and reduces trade flows. As a consequence, the status of the WTO will inevitably be weakened owing to its limited role in dealing with trade disputes, as demonstrated in Figure 1. These factors are merely mentioned or described in previous studies, yet not much research has been done using a systematic approach. This paper seeks to focus on these issues from the perspective of GATT/WTO trade rules and by using an empirical simulation model.

Section 2 will review the previous literature on global warming, the CBAM, and other related issues. Section 3 will discuss how the CBAM will unavoidably be at the center of an international trade controversy in terms of the GATT and WTO. For the CBAM to function properly, it must be compatible with international trade rules. If this mechanism is promoted by the Biden administration in the U.S. (which rejoined the Paris Climate Accord in early 2021) under circumstances where many of its components are not in accordance with GATT/WTO rules, the potential risk of a series of trade conflicts is high.

Noting that the WTO Appellate Body stopped functioning at the end of 2019, the multilateral trade system that is supposed to preserve free and rules-based global trade may be at a crossroads if the CBAM conflict, which could severely impact global trade, is not resolved. In Section 4, this paper, for the first time, systematically estimates the impacts both of enforcing the CBAM and of possible trade retaliation by using a dynamic computational general equilibrium (CGE) model. Finally, Section 5 provides the conclusion, suggesting that enforcement of the unilateral carbon tax under CBAM could render the WTO even more helpless than it is now.

2. Literature Review

2.1. “Fit for 55” and the CBAM

Since the United Nations Conference on Environment and Development (the Earth Summit) held in Rio de Janeiro in 1992, the topic of climate change has become a global issue, and the world has been discussing ways to prevent climate disaster. Consequently, several specific measures were adopted: the UN Framework Convention on Climate Change (UNFCCC) in 1992, the Kyoto Protocol in 1997, and the Paris Agreement in 2015. More specifically, UN members must submit improved commitments of “2030 Nationally Determined Contributions (NDCs)” following the “2050 strategy of climate-neutrality”.

Since the beginning of the negotiations during the UNFCCC, EU members have been actively participating in discussions on preventing climate change. The view of EU policymakers and politicians is that climate change could serve as an opportunity to strengthen the EU’s global position and legitimacy [16,17,18].

The EU agreed on the European Green Deal in December 2019. It aims to build up Europe as the first climate-neutral continent by 2050, and its vision lies in protection of biodiversity, construction of a circular economy, and eradication of pollution, among other things. The deal aims to bolster the EU’s role in international discussions on the issues of climate and the environment. Taken overall, the European Green Deal strengthens the comprehensiveness and governance structure of climate policies, yet lacks consideration of global fairness and equity, as does the 2050 Climate Neutrality Target. Fit for 55, first introduced on 14 July 2021, is an upgraded version of the European Green Deal that adds implementation measures while maintaining the original structure. The legislation promises to reduce carbon emissions by 50~55% and claims to apply the CBAM to other countries [19].

Following [20], who put forward optimal policies to prevent trade distortion caused by cross-border externalities, Refs. [21,22,23] developed theories on environmental issues. In particular, Keen and Kotsogiann is showed that an accurate environmental trade adjustment is very complex, and an optimal set of environmental tariffs is a way of balancing foreign production and consumption behavior, which differs by region and items.

Since the CBAM proposal, many studies have been using dynamic CGE models, including [7,8,24,25,26,27,28], among others. Furthermore, many researchers are currently analyzing the country- and industry-wide impacts of the CBAM. For example, Bellora [7] evaluated the CBAM as means of reducing carbon emissions. Aichele and Feibermayr systematically analyzed the issue of carbon leakage, where businesses transfer production to other countries that have lax carbon emission constraints. Previous studies on the carbon border tax have generally found that imposing import tariffs on export items from countries with loose carbon emission regulations will change the production structure, and will be effective in reducing global carbon emissions and reducing carbon leakage [26,29,30,31].

2.2. Limitations of the CBAM

Considerable research has been published on the limitations of the CBAM. Studies have suggested that there are many requirements for CBAM to be effective. For example, Refs. [32,33] pointed out that export subsidies on sectors with high carbon emissions must be abolished to realize the effects of the carbon border tax. Also, other problems regarding the CBAM have been raised. When the data on carbon emissions becomes merged with international trade law, optimistic reduction effects could be realized [33,34]. Furthermore, regulations on export subsidies and Emission Trading System (ETS) free allowance allocations must be included to fully realize the effect of the carbon border tax [33,35]. At the WTO Committee on Trade and Environment (CTE) meeting in March 2021, the lack of transparency in the CBAM and how it could potentially distort trade were pointed out [3]. Refs. [2,4] viewed the CBAM as being akin to new trade barriers.

In the process of promoting a carbon-free economy, Lowe [36] also pointed out that the CBAM may further increase the gap between developed countries and developing countries. Eicke [37] claimed that the risks to trade-related policies are growing for underdeveloped economies, since they have relatively less accessibility to low-carbon financing and technology, delaying the energy transition, which could decrease the stability and competitiveness of those economies. Refs. [33,38] raised the issue of the cost of applying the CBAM. Smaller economies and those with greater dependence on trade with the EU, such as African countries and those with borders adjacent to the EU, could face a greater shock [38]. For these reasons, a collective climate measure may be preferred over the unilateral CBAM [34]. There are concerns about how the implementation of the CBAM may intensify global protectionist sentiments due to the countermeasures of individual countries to the mechanism [39]. Many researchers and practitioners, such as [10,12,13], worry about retaliation against the EU.

Moreover, there are concerns about negative effects from implementing the carbon border tax. This could lead to trade reduction and welfare loss in emerging markets and developing countries, where major industries with carbon emissions are clustered [31,40]. Eicke [38] expressed the view that risks faced by trading countries when the CBAM is implemented will increase in several cases, i.e., when a particular trading country has greater dependence on trade with the EU; when current carbon emissions are high, or a carbon lock-in situation exists; when a country lacks a systemic capacity to quantify the volume of carbon emissions needed by EU monitoring, reporting, and verification (MRV).

3. Analysis of WTO-Compatibility with the CBAM

3.1. Overview

Much of the previous literature expressed concerns over measures preventing climate change, including the CBAM, and their compatibility with WTO agreements. Among them, some of the most notable recent studies include those by [2,14,16,41,42,43,44,45]. Controversy over the CBAM has intensified. Specifically, developing countries (including China) have argued that the CBAM conflicts with the WTO free trade principles and is unfair from numerous perspectives. Subsequently, the EU announced it would seek measures to accommodate the positions of developing countries and harmonize the CBAM with WTO principles before its implementation. However, it will be difficult to reach international accord on the CBAM. If this issue of WTO compatibility is not resolved, the EU will not be able to circumvent an international trade conflict [2,46,47,48,49].

The EU has been making efforts to bring the CBAM within the WTO system [50] While the EU’s climate policies have been developing for more than three decades, it has been trying to establish regulations and systems compatible with WTO rules, as well as trying to change already established WTO agreements. This is called parallel adaptation, and the EU has been pursuing a systematic approach based on trade rules—in other words, “a GATT/WTO environmentally-friendly approach” [44]. Yet, due to its imposition of new tariffs, the CBAM faces obstacles in meeting the WTO rules and satisfying other WTO members. In this regard, European Parliament [51] reported that “[it] supports the introduction of a CBAM, provided that it is compatible with WTO rules and EU free trade agreements (FTAs) by not being discriminatory or constituting a disguised restriction on international trade.”

It would seem difficult for the EU to resolve the WTO-compatibility issue with the CBAM, which has existed since its inception. UNCTAD [41] asserted: “With the exception of a carbon tax on domestically consumed products, all other carbon adjustment mechanisms discussed by the European Commission do not stand the test of GATT-compatibility. They all violate basic GATT provisions and cannot be justified by the public policy exception of GATT Article XX.” More specifically, Englisch [42] maintain that it would not be possible to impose any border tax based on carbon content without violating the most-favored-nation (MFN) principle, while Bacchus [2] also noted that if countries do not immediately settle the disputes with their trading partners, trade conflict will intensify.

3.2. GATT/WTO Articles Subject to Potential Violation

This section analyzes the EU CBAM mechanisms that have the potential contravene WTO principles. The articles relevant to the CBAM include GATT Article I: General Most-Favoured-Nation Treatment; Article XI: General Elimination of Quantitative Restrictions; Article XVI: Subsidies; and Article XXI: Security Exceptions. Some of the articles that could be subject to GATT/WTO incompatibility are listed in Table 1.

Many pages would be needed to discuss the possible violations under all the articles in Table 1; therefore, this section only briefly discusses the compatibility issue under GATT Article I (MFN) and Article II (BAT). MFN treatment is one of the cornerstones of the GATT/WTO; it obliges a member country to refrain from any discriminatory practices in trade, and to grant equal benefits from a particular product to all like products from member countries. However, due to the technology gap between exporters, the CBAM tariffs will inevitably be assessed differently based on the extent of each countries’ environmental regulations, their technology levels, the availability of an ETS, and other matters. Therefore, even if the carbon border tax is imposed under a consistent standard, discrimination will still exist in reality [44]. In other words, the CBAM could violate the MFN principle as it relates to other countries’ exports of like products (mentioned in GATT Article I, paragraph 1) [41,42].

Moreover, the GATT does not specify or regulate any guidelines about carbon content. If the EU discriminates against imports of like products based on exporter carbon content, this will clearly violate the MFN principle. More specifically, if the EU self-judges the extent and the quality of the climate change measures of other WTO member countries, and subsequently selects import items based on how many emissions certificates the members have purchased, this will result in discrimination among WTO members [2].

GATT Article II, paragraph 2, states: “Nothing in this Article shall prevent any contracting party from imposing at any time on the importation of any product,” and subparagraph (a) includes “a charge equivalent to an internal tax imposed consistently with the provisions of paragraph 2 of Article III in respect of the like domestic product or in respect of an article from which the imported product has been manufactured or produced in whole or in part.” Furthermore, included in Article II are subparagraphs (b) and (c), reading “…any anti-dumping or countervailing duty applied consistently with the provisions of Article VI…”; and “…fees or other charges commensurate with the cost of services rendered…”, respectively. Thus, GATT Article II paragraph 2, subparagraph (a) allows the so-called border adjustments tax (BAT). However, that does not mean there is no problem with the CBAM, because subparagraph (a) in paragraph 2 of Article II is to be interpreted to mean only those taxes imposed for adjusting imports of final goods that are “physically incorporated inputs” may be adjusted [52].

For the BAT, there are other problems similar to the violation of the MFN principle. It is very likely that the new carbon certificates will be costly, and as the EU continues to expand its climate policies, additional measures will be introduced, which will eventually increase the price of carbon certificates. The EU has continued to maintain its position that the CBAM is a requirement for internal regulation. Considering this, if the price of carbon certificates rises and exceeds the ceilings of commitments on binding tariffs, the burdens for exporting countries will increase, although it is acknowledged that the CBAM is not a BAT. That will impose extra trade barriers on non-EU countries, even though that it is not a violation of law [2]. A similar point was raised by Horn [4], who wrote: “the possibility for protectionism is in our view and, we believe, the opinion more generally, the main drawback of BATs.”

In summary, the CBAM has the potential bring about many legal issues that could be incompatible with various articles of the GATT/WTO. Therefore, many countries will claim there are international trade conflicts with the EU’s imposition of tariffs, and this will lead to retaliation [11,12], which will ultimately deteriorate the global trade environment. Section 4 will estimate how such situations will impact trade.

4. The Impact of the CBAM: Analysis from the Perspective of Trade Retaliation

From 2033 on, non-EU exporters into the EU must purchase a carbon certificate based on the carbon content of their products during production, and must submit the certificate to the authorities of the importing EU country. If payment for the carbon emission is made via certified emission reduction (CER), the applicable amount of tax is to be reduced. However, members of the European Free Trade Association (EFTA), such as Switzerland, Iceland, Liechtenstein, and Norway, are exempt from such duties because they implement an emission trading system linked to the EU’s ETS. There are 56 applicable sectors, including cement, electric power, fertilizer, steel, and aluminum. (Table 2) Many issues, such as understanding how the EU assesses the carbon content, the price of carbon certificates, adjustment of an ETS free assignment, duration of the transition, and expansion of the range of applicable items by 2025, are under consideration.

4.1. Model and Data Used for Analysis

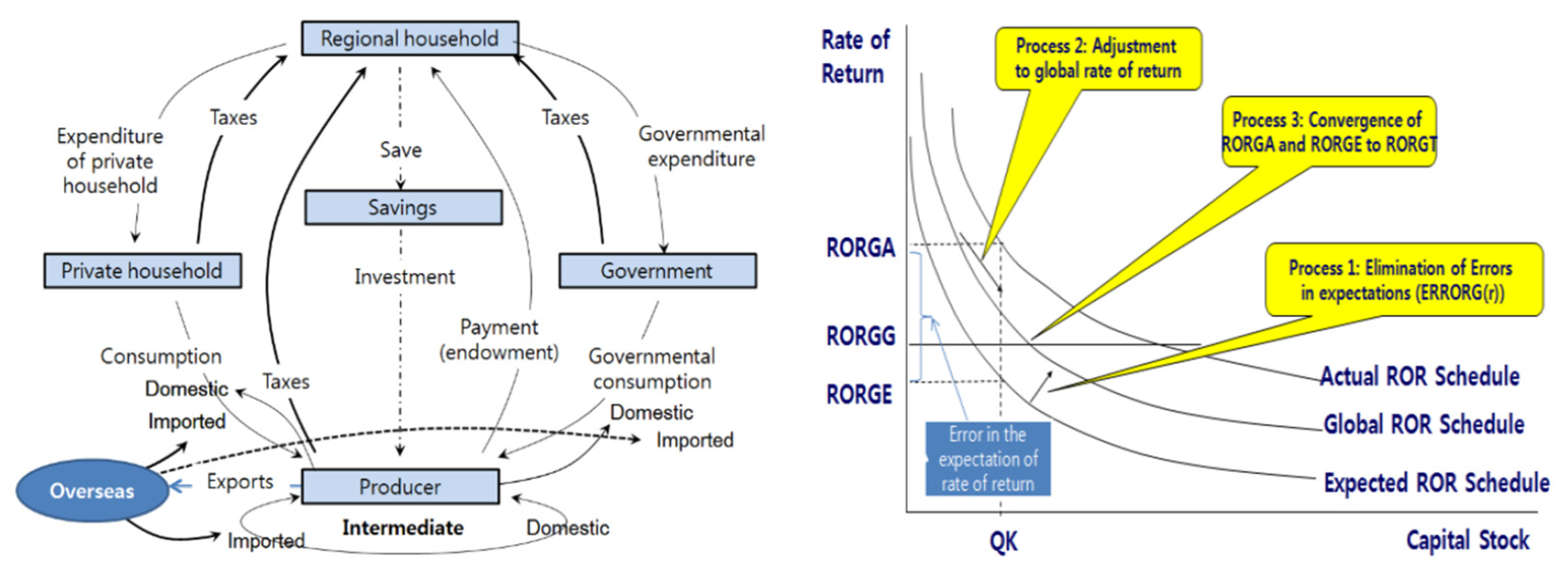

To analyze the impact of the EU’s imposition of the CBAM, this paper uses the recursive dynamic GTAP (GTAP-Dyn) model, which is discussed in detail in [53]. The GTAP-Dyn model is one of the models modified by the authors of [54]. It allows dynamic analyses to be made by adding the investment theory for international capital mobility and ownership. The investment theory, which lies at the center of the GTAP-Dyn model, uses a disequilibrium approach based on the assumption of imperfect mobility of capital. Theoretically, savings are invested in a region with the highest rate of return (ROR). If capital mobility is perfect, the ROR of all regions must be the same; however, in reality, RORs are regionally not equal. In the GTAP-Dyn model, the regional equalization of ROR is assumed to only occur in the long term, and regional differences arise in the short term. However, as seen in the model on the right side of Figure 2, due to the mechanism gradually equalizing expected ROR and actual ROR, the regionally differing RORs level out over time.

To estimate the impact of the EU’s imposition of CBAM tariffs, we should classify the parallel energy-intensive sectors: coal, oil, gas, steel (including aluminum), petrochemicals, and electric power. There are 10 individually disaggregated sectors: coal, oil, gas, paper, aluminum, steel, oil products (oil_pcts), cement, chemicals, and electricity. For the classification of countries, the paper focuses on those which will be heavily impacted by the CBAM measures and those which are the largest emitters of CO2. The top 20 countries with the most exports of the 56 listed CBAM items into the EU include China, Russia, Turkey, India, USA and South Korea (Table 3) [58].

In building the model, the specifications of countries with insignificant volumes of exports to the EU have not been disaggregated because that could reduce the accuracy of the simulation in the model due to the size of the necessary data. Thus, the countries have been disaggregated into 18 countries (Table 4) where tariff equivalents can be identified.

4.2. Scenarios

Because a detailed plan for applying the carbon border tax has not yet been suggested, this paper sets up potential scenarios based on the expected circumstances (Table 5). In addition to carbon price forecast, time period, and technological change, scenarios are set to reflect the trade retaliation hypothesized in this paper. It is assumed that the impact of CBAM on global industry and trade adjustment will exist over the next 15 years. Realistically, the effect may persist for a longer period of time, but it was set in consideration of the limitations of the analytical model. The carbon price was set at the current level as of August 2021 and considering future price changes. The EU has announced that some of the CBAM tariff revenue will be used to improve the technical efficiency of the energy industry. CBAM revenue was calculated using a separate GTAP model and technology improvement of 1.5% for 5 years was estimated based on the revenue. Scenario 1 in Table 5 assumes the CBAM application is the most lax, and thus, all ETS countries and those under review of implementation are exempt from the duty of the carbon border tax. Scenario 2 assumes all countries except four in the EFTA with the EU-related system and the EU itself impose the carbon border tax. This scenario conveys the CBAM plan as it is currently known. Intense resistance is expected from major countries, such as China, the United States, and Russia, against the EU’s CBAM system, especially those that are subject to high tariffs. This may lead to trade retaliation via counter-tariffs to the extent that they can be imposed, as predicted by the authors of [10,11]. Accordingly, Scenario 3 assumes retaliation measures are adopted against the EU. Lastly, Scenario 4 reviews circumstances where all economies, rising above bilateral retaliation, decide to adopt the carbon border tax. The scenarios that comprehensively consider the target countries of the carbon border tax, the reflection of carbon pricing, and the increase in efficiency of carbon-related technology can be summarized as follows.

4.2.1. Target Countries

The target countries of the EU’s carbon border tax, the cost of carbon, and changes in carbon-related technology using the carbon tax earned by the EU have been reflected in the scenarios of this study. World Bank [59] classified major countries in the world based on whether an ETS would be implemented (implementation, reviewing implementation, no implementation) as of April 2021. Table 6 summarizes major contents of ETS implementations in Europe and individual countries.

4.2.2. Carbon Pricing

It is plausible that the EU will, through the CBAM, impose tariffs based on the CO2 emission quantity embedded in imports. Such tariffs can be estimated by using the export quantity of CO2 and the transaction costs of CO2 per ton between countries. That is, ad valorem based on the CO2 emission quantities of countries should be calculated. In this regard, UNCTAD [40] assessed tariff equivalents based on carbon emissions of exporters to the EU, as summarized in Table 7. This paper relies on the UNCTAD assessment.

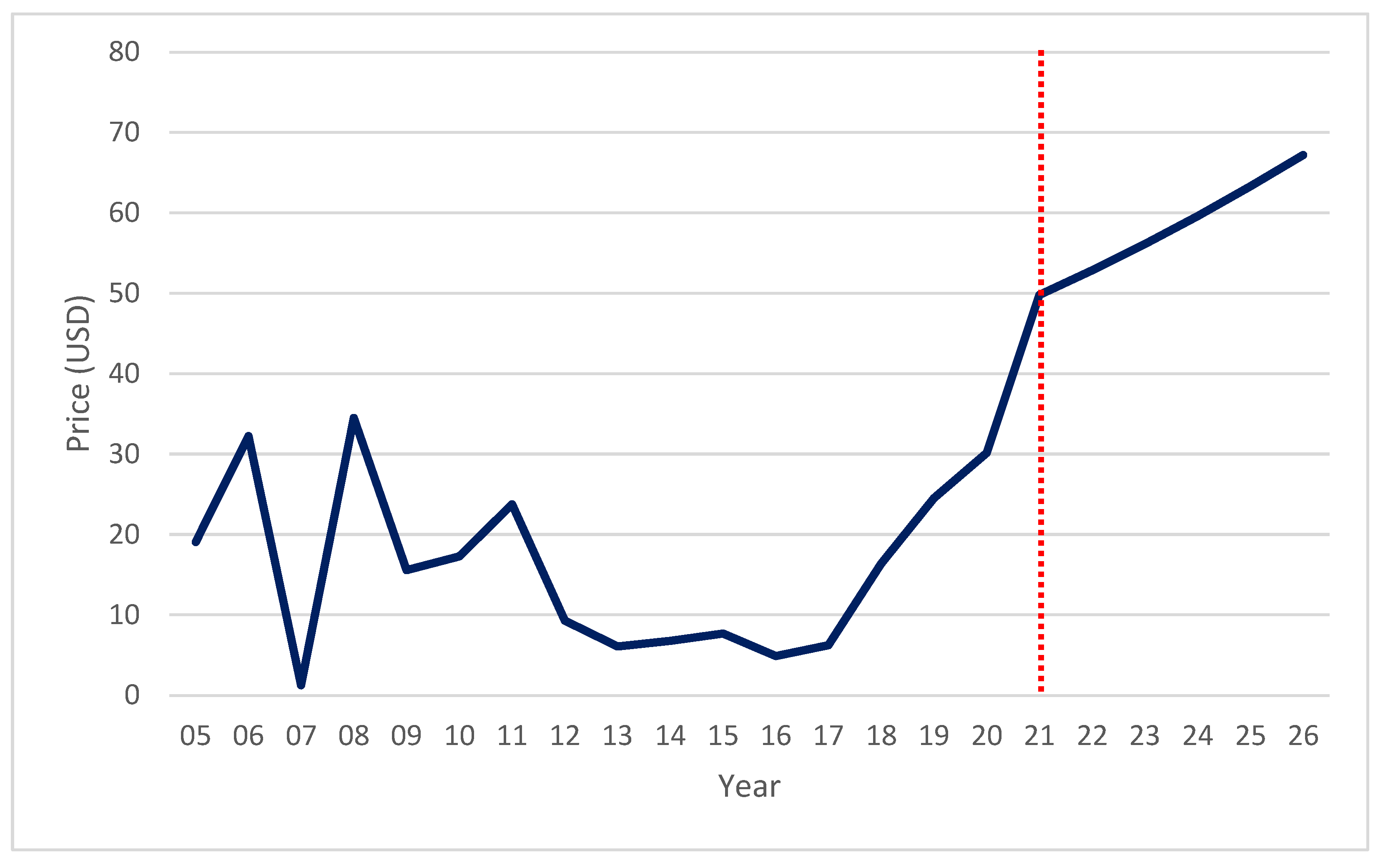

The cost of carbon used for tariff equivalents in the analysis [40] was 44 USD per metric ton (Mt) of CO2. However, this may not accurately reflect constantly increasing carbon prices. According to World Bank [59], the EU’s carbon price for August 2021 was 49.77 USD/Mt (Figure 3). Yet, considering the trend of carbon pricing, in the year 2026, in which the CBAM will be fully implemented, the price will be 67.2 USD, and by 2033, it is expected to go beyond 100 USD/Mt (assuming the annual average rate of increase to be approximately 6.2%).

This paper revises the tariff equivalents from [40] by reflecting the estimates of the EU’s future carbon prices. The recursive dynamic model has the advantage of allowing researchers to set different carbon pricing levels for specific years; thus, this paper sets scenarios with constantly increasing prices from 67.2 USD in 2031 to 90.7 USD in 2031, and 122.5 USD in 2036. In particular, Scenario 4, which is the worst case assuming that all countries impose reciprocal carbon border taxes, applies equal tariff rates to all countries.

4.2.3. Increases in the Efficiency of Carbon-Related Technology

The EU has stated that it will invest the tax revenue earned from the carbon tax to enhance carbon technology. This means the development of low-carbon, high-efficiency energy sectors, and it is expected that this will reduce the demand for EU imports in energy sectors. To reflect this in the model, we set up a scenario where the weight the carbon tax has in the EU’s financial income affects the development of technology in the energy industry.

4.3. Simulation Results and Interpretation

This section presents the simulation results using the GTAP-Dyn simulation model under the four scenarios following the CBAM in the context of total change in the trade of the world’s energy products and the changes by country. The model produces estimates for many variables, such as production, but this section focuses on trade. Simulation results for other variables can be provided upon request.

4.3.1. Impacts on the Trade of Energy Products

As expected, the analysis shows that global trade in energy sectors will be reduced as a result of the EU’s carbon tax. Looking at the changes in the amount of trade based on each scenario (Table 8), exports and imports of most items would be reduced, and the fluctuations in trade volumes will be impacted very differently depending on the sector. Under scenarios assuming the EU’s unilateral imposition of tariffs (Scenario 1 and Scenario 2), the change in exports and imports would be in the order of 3.0%, showing a relatively small reduction in trade. However, under the scenario imposing retaliatory tariffs against EU trade partners (Scenario 3), the reduction in volume would be larger—4.5~4.6%. Furthermore, under the scenario where all countries adopt a carbon border tax (Scenario 4), global trade volume is expected to decrease by 14%. The sectors that suffer from the largest trade reduction in Scenario 4 would be paper (−15.6%), steel (−14.2%), and oil_pcts (−13.7%).

4.3.2. Changes in Trade by Country

Global trade in energy sectors is expected to decrease following the EU’s imposition of the carbon tax (Table 9). Imports and exports for most countries are reduced, and the fluctuations in trade would be quite different depending on the country and the industry. Based on Scenario 4, the rates of reduction in exports are expected to be most notable in countries adjacent to the EU: the United Kingdom (−26.4%), Belarus (−26.1%), Turkey (−23.4%), as institutionally predicted by the authors of [2,4]. Next to these would be China (−20.9%), South Korea (−20.8%), and other East Asian steel exporters. For the EU, the volumes of exports in energy sectors may all go up, except in Scenario 4. In Scenarios 1 and 2, exports are expected to increase, going beyond 15%. The EU would gain from the CBAM. In Scenario 3, where mutual imposition of tariffs is assumed, the export growth rate would go down to 3.5%, and in Scenario 4, the EU would see a reduction of 0.4%. The imports from energy sectors are also expected to drop, and each country would experience different rates of reduction. The EU would experience the biggest reduction in imports due to the tariffs, followed by Russia, Canada, and Ukraine.

The difference between Scenario 2 and Scenarios 3 and 4 is that the imposition of the carbon border tax expands to other countries or to the world. Under mutual imposition of tariffs, or if a third country’s adoption of tariffs decreases the rate of reduction more than the EU’s unilateral tariff, retaliation works and subsequent retaliations would be made, as the authors of [14,15] logically explored. As a representative case, one of the EU’s biggest carbon exporters, Russia, is expected to have a huge reduction (−23.5%) under Scenario 2; while in Scenario 3, where countries around the globe impose a carbon tax, the degree of reduction would be smaller (−20.3%). Likewise, other major exporters, such as China, Ukraine, South Korea, the United States, Argentina, and Japan, exceed the differences under S3 and S2 in the rate of reduction of exports by 3%. Countries (especially developing countries) are more likely to retaliate against the EU than simply accept the unilateral imposition, i.e., they would be subject to heavy damage [36] and would seek retaliation against the EU.

4.3.3. Change in Trade of Steel and Aluminum

Among the sectors subject to CBAM tariffs, the products that the EU imports the most are steel and aluminum; thus, these items can be considered a representative index for the change in trade. When looking at the simulation results (Table 10) for these two energy sectors more closely, the EU would increase its exports substantially (43% under Scenarios 1 and 2, 20% under Scenarios 3 and 4), while the exports and imports of other countries would be severely affected under all scenarios. Steel would be impacted more than aluminum in the global context (the average of world aluminum trade would decrease by 1.8~12.6%, and that of steel by 3.8~14.2%). Scenario 4 shows a significantly higher rate of reduction, where the rates for aluminum and steel would be 12.6% and −14.2%, respectively.

As indicated by rates of change for trade in the energy sectors mentioned above, most countries would experience lower rates of reduction under Scenario 3 than under Scenario 2. Most countries, including Canada, China, Korea, the United States, and Japan, would have smaller export reductions under Scenario 3 (mutual imposition of tariffs with the EU) than under Scenarios 1 and 2 (EU’s unilateral imposition of tariffs), and Japan may even increase its trade (for reference, China: −11.4 → −1.9%; USA: −8.8 → −0.3%; Japan: −7.5 → 1.7%). This happens due to changes in international competitiveness due to the imposition of tariffs. The simulation results support trade retaliation against the EU’s CBAM, which will eventually lead to the trade environment assumed in Scenario 4.

5. Discussion and Conclusions

With the announcement of the CBAM by the EU, awareness among companies of carbon reduction has been strengthened, and the global carbon credit market is revitalizing itself. The size of the global carbon credit market reached 229 billion euros in 2020, more than five times that of three years ago. Some positive effects from the announcement of the CBAM are found in that the price of carbon credits in major countries has risen significantly, and China, the world’s No. 1 carbon emitter, integrated the carbon credit trading market nationwide this year.

Major exporters of energy products will find it advantageous to adopt retaliatory tariffs (Scenario 3, 4) rather than accept the EU’s unilateral tariffs (Scenario 1, 2). Such reciprocal retaliatory tariffs will offset the effect of the CBAM, thereby reinforcing the price competitiveness of their energy products. Chapter 4 suggests that this will increase the exports of energy product by non-EU countries. Of the four scenarios, Scenario 3 is most likely to become a reality. If countries with high carbon emissions, such as Russia, China, and India, engage in trade retaliation, the CBAM will become disadvantageous for the EU. As such, it is questionable whether CBAM can be implemented as the EU intends.

Although the EU has undertaken various legal reviews to assert that the CBAM is compatible with GATT/WTO rules [48], current CBAM initiatives cannot avoid normative violations [41]. No country will oppose a response to climate change, but for CBAM to be implemented successfully, technical, legal, and, above all, political issues must be overcome [47]. Refs. [36,38] argued, it clearly raises the bar (i.e., trade barriers) for developing countries, and the affected countries will engage in trade retaliation [14].

This paper analyzed the ways in which the CBAM does not conform to GATT/WTO trade rules, as explained in Section 3, and for the first time, quantitatively estimated the impact of CBAM under several scenarios from the perspective of trade retaliation. Based on the findings of the empirical simulations in Section 4, it is possible to confirm large losses for non-EU countries and developing countries, and serious impacts on the steel and aluminum sectors.

Despite the 12th WTO Trade Ministers’ Meeting (MC12) scheduled for November 2021, the future of the WTO is still uncertain due to various factors, such as the passive U.S. stance and the US–China trade conflict. Due to the suspension of the Appellate Body, the WTO has lost its capacity to resolve trade disputes. If the WTO plays no role in mitigating global trade retaliation, its status will suffer further. In some respects, the Biden administration can accommodate the CBAM, in that the U.S. has returned to the Paris Agreement that former president Donald Trump withdrew from, and pledged to promote eco-friendly policies. Moreover, the U.S., which is decoupling from China, can adopt the CBAM and introduce a U.S.-style carbon border tax, which could be used to contain China. In that case, the multilateral trade system of the WTO will effectively collapse, although the MC12 trade ministers have emphasized the importance of the WTO.

The current CBAM, which poses a real risk of deteriorating the global trade environment, requires a new legal review, as well as an economic review, at the global level, but not from the EU’s point of view. The implementation period should be delayed, and an international information cooperation system should be discussed first, along with a technical analysis. Today, production is dispersed across multiple countries owing to the global value chain (GVC). When the carbon history of a specific product can be accurately estimated, and if related information can be shared internationally, a carbon border tax can be calculated rationally. Additionally, ways to use tax revenue to reduce the backlash against the CBAM require international agreement. Clearly, this is a new tax imposed on third countries, and if all the revenue, not part of it for international publicity, is used to support environmental technology in developing countries, international acceptance of the CBAM will improve, and criticism against it as a protectionist measure may diminish.

Since the trade retaliation suggested in this paper is highly likely to become a reality, the EU should postpone the implementation of CBAM and closely consult with the international community. In particular, special and differentiated consideration should be made for developing countries, where substantial impact due to CBAM is inevitable. A WTO-level response is also needed. Member States should discuss CBAM tariffs that are inconsistent with WTO rules. If the global trade environment deteriorates due to trade retaliation, the WTO may be in real trouble. Taken together, the justification for preventing climate change is good, but the CBAM scheme is too costly.

Author Contributions

Conceptualization, I.C., K.H. and B.L.; methodology, K.H. and J.-I.C.; software, B.L. and I.C.; validation, J.-I.C. and B.L.; formal analysis, B.L. and J.Y.; investigation, K.H. and J.Y.; resources, I.C. and J.-I.C.; data curation, B.L. and I.C.; writing—original draft preparation, I.C. and K.H.; writing—review and editing, I.C. and K.H.; supervision, I.C.; project administration, I.C.; funding acquisition, I.C. and J.-I.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research was supported by Academic-research Cooperation Program in Korea Maritime Institute (KMI).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Chase, P.; Pinkert, R. The EU’s Triangular Dilemma on Climate and Trade. German Marshall Fund, Policy Brief. 2021. Available online: https://www.gmfus.org/sites/default/files/2021-09/Chase%20%26%20Pinkert%20-%20CBAM%20-%20brief_0.pdf (accessed on 4 October 2021).

- Bacchus, J. Legal Issues with the European Carbon Border Adjustment Mechanism; CATO Briefing Paper, No.125; CATO Institute: Washington, WA, USA, 2021; pp. 3–6. [Google Scholar]

- International Institute for Sustainable Development (IISD). An EU Carbon Border Adjustment Mechanism: Can It Make Global Trade Greener While Respecting WTO Rules? Commentary, 17 May 2021. Available online: https://sdg.iisd.org/commentary/guest-articles/an-eu-carbon-border-adjustment-mechanism-can-it-make-global-trade-greener-while-respecting-wto-rules/(accessed on 4 October 2021).

- Horn, H.; Mavroidis, P.C. To B(TA) or not to B(TA)? On the Legality and Desirability of Border Tax Adjustments from a Trade Perspective. World Econ. 2011, 34, 1911–1937. [Google Scholar] [CrossRef] [Green Version]

- IMF. World Economic Outlook Annex 3.1. In The Impact of Environmental Policy on Clean Innovation; Working Paper No. 2021/213; IMF: Washington, DC, USA, 2021. [Google Scholar]

- Clerc, L.; Bontemps-Chanel, A.; Diot, S.; Overton, G.; De Soares Albergaria, S.; Vernet, L.; Louardi, M. A First Assessment of Financial Risks Stemming from Climate Change: The Main Results of the 2020 Climate Pilot Exercise. Bangue de France, No.122-2021, Analysis et Synthèsis. 2021. Available online: https://c2e2.unepdtu.org/kms_object/a-first-assessment-of-financial-risks-stemming-from-climate-change-results-of-the-2020-climate-pilot-exercise/ (accessed on 1 October 2021).

- Bellora, C.; Fontagné, L. EU in Search of a WTO—Compatible Carbon Border Adjustment Mechanism. 2021. Available online: http://www.lionel-fontagne.eu/uploads/9/8/3/3/98330770/cblf_cba_2021.pdf (accessed on 4 October 2021).

- Balistreri, E.J.; Kaffine, D.T.; Yonezawa, H. Optimal Environmental Border Adjustments under the General Agreement on Tariffs and Trade; CARD Working Papers; Center for Agricultural and Rural Development, Iowa State University: Ames, IA, USA, 2019; p. 25. Available online: https://lib.dr.iastate.edu/card_workingpapers/603 (accessed on 4 October 2021).

- Kahn, M.E.; Mohaddes, K.; Ng, R.N.C.; Pesaran, M.H.; Raissi, M.; Yang, J.C. Long-Term Macroeconomic Effects of Climate Change: A Cross-Country Analysis; Working Paper 26167; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Gläser, A.; Caspar, O.; Li, L.; Kardish, C.; Holovko, I.; Makarov, I. Less Confrontation, More Cooperation. German Watch Policy Brief 21-3-2e. 2021. Available online: https://germanwatch.org/en/20355 (accessed on 1 October 2021).

- Appunn, K. Emission Reduction Panacea or Recipe for Trade War? The EU’s Carbon Border Tax Debate. Clean Energy Wire Editorial, 23 July 2021. Available online: https://www.cleanenergywire.org/factsheets/emission-reduction-panacea-or-recipe-trade-war-eus-carbon-border-tax-debate(accessed on 2 October 2021).

- Dias, A.; Bret, B.L.; Prost, O.; Rard, R. Carbon Border Adjustment Mechanism (CBAM)—EU Proposal 2021. GIDE LOYRETTE NOUEL CARBON 2021. Available online: https://www.gide.com/en/actualites/carbon-border-adjustment-mechanism-cbam-eu-proposal (accessed on 1 October 2021).

- Christoffersen, P.S. The Carbon Border Adjustment Mechanism. Teneo Editorial, 9 June 2021. Available online: https://www.teneo.com/the-carbon-border-adjustment-mechanism/(accessed on 24 September 2021).

- Sapir, A. The European Union’s Carbon Border Mechanism and the WTO. Bruegel, 19 July 2021. Available online: https://www.bruegel.org/2021/07/the-european-unions-carbon-border-mechanism-and-the-wto/(accessed on 1 October 2021).

- De Vos, B. The Carbon Border Adjustment Mechanism: Ensuring Fairness. EURACTIV Editorial, 29 October 2020. Available online: https://www.euractiv.com/section/energy-environment/opinion/the-carbon-border-adjustment-mechanism-ensuring-fairness/(accessed on 4 October 2021).

- Kulovesi, K.; van Asselt, H. Three Decades of Learning-by-Doing: The Evolving Climate Change Mitigation Policy of the European Union. In Climate and Energy Policies in the EU, China and Korea—Transition, Policy Cooperation and Linkage; Edward Elgar Forthcoming: Cheltenham, UK, 2021; Available online: https://ssrn.com/abstract=3859498 (accessed on 4 October 2021).

- Sebastian, O.; Kelly, C.R. EU Leadership in International Climate Policy: Achievements and Challenges. Int. Spect. 2008, 43, 35–50. [Google Scholar] [CrossRef]

- Jordan, A.; van Asselt, H.; Berkhout, F.; Huitema, D.; Rayner, T. Understanding the Paradoxes of Multilevel Governing: Climate Change Policy in the European Union. Global Environ. Polit. 2012, 12, 43–66. [Google Scholar] [CrossRef] [Green Version]

- KIET. Major contents of EU’s CBAM and Implications. i-KIET Industry and Economic Issue. 2021, 119, 1–11. Available online: https://www.kiet.re.kr/kiet_web/?sub_num=9&state=view&idx=58168 (accessed on 5 September 2021).

- Markusen, J.R. International externalizes and optimal tax structures. J. Int. Econ. 1975, 5, 15–29. [Google Scholar] [CrossRef]

- Hoel, M. Should a carbon tax be differentiated across sectors. J. Public Econ. 1996, 59, 17–32. [Google Scholar] [CrossRef]

- Jakob, M.; Marschinski, R.; Hübler, M. Between a Rock and a Hard Place: A Trade-Theory Analysis of Leakage Under Production- and Consumption-Based Policies. Environ. Resour. Econ. 2013, 56, 47–72. [Google Scholar] [CrossRef]

- Keen, M.; Kotsogiannis, C. Coordinating climate and trade policies: Pareto efficiency and the role of border tax adjustments. J. Int. Econ. 2014, 94, 119–128. [Google Scholar] [CrossRef] [Green Version]

- Aichele, R.; Felbermayr, G. Kyoto and the carbon footprint of nations. J. Environ. Econ. Manag. 2012, 63, 336–354. [Google Scholar] [CrossRef] [Green Version]

- Aichele, R.; Felbermayr, G. Kyoto and Carbon Leakage: An Empirical Analysis of the Carbon Content of Bilateral Trade. Rev. Econ. Stat. 2015, 97, 104–115. [Google Scholar] [CrossRef] [Green Version]

- Shapiro, J.S. The environmental bias of trade policy. Q. J. Econ. 2020, 136, 831–886. [Google Scholar] [CrossRef]

- Nevalainen, A. EU’s Carbon Border Adjustment Mechanism—Its Purpose and Effects on Carbon Leakage. Bachelor’s Thesis, Aalto University School of Business, Helsinki, Finland, 2021. [Google Scholar]

- Zhong, J.; Pei, J. Beggar Thy Neighbor? On the Competitiveness and Welfare Impacts of the EU’s Proposed Carbon Border Adjustment Mechanism. 2021, pp. 19–23. Available online: https://ssrn.com/abstract=3891356 (accessed on 4 October 2021).

- Fischer, C.; Fox, A. Comparing policies to combat emissions leakage: Border carbon adjustments versus rebates. J. Environ. Econ. Manag. 2012, 64, 199–216. [Google Scholar] [CrossRef]

- Branger, F.; Quirion, P. Would border carbon adjustments prevent carbon leakage and heavy industry competitiveness losses? Insights from a meta-analysis of recent economic studies. Ecol. Econ. 2014, 99, 29–39. [Google Scholar] [CrossRef] [Green Version]

- Larch, M.; Wanner, J. Carbon tariffs: An analysis of the trade, welfare, and emission effects. J. Int. Econ. 2017, 109, 195–213. [Google Scholar] [CrossRef] [Green Version]

- Elliott, J.; Foster, I.; Kortum, S.; Munson, T.; Cervantes, F.P.; Weisbach, D. Trade and carbon taxes. Am. Econ. Rev. 2010, 100, 465–469. [Google Scholar] [CrossRef] [Green Version]

- Elliott, J.; Foster, I.; Kortum, S.; Jush, G.K.; Munson, T.; Weisbach, D. Unilateral Carbon Taxes, Border Tax Adjustments and Carbon Leakage. Theor. Inq. Law 2013, 14, 207–244. [Google Scholar] [CrossRef] [Green Version]

- Mehling, M.A.; van Asselt, H.; Das, K.; Droege, S.; Verkuijl, C. Designing border carbon adjustments for enhanced climate action. Am. J. Int. Law 2019, 113, 433–481. [Google Scholar] [CrossRef] [Green Version]

- Palacková, E. Saving face and facing climate change: Are border adjustments a viable option to stop carbon leakage? Eur. View 2019, 18, 149–155. [Google Scholar] [CrossRef]

- Lowe, S. The EU’s Carbon Border Adjustment Mechanism: How to Make It Work for Developing Countries. Centre for European Reform. 2021. Available online: https://www.cer.eu/publications/archive/policy-brief/2021/eus-carbon-border-adjustment-mechanism-how-make-it-work (accessed on 11 September 2021).

- Eicke, L.; Goldthau, A. Are we at risk of an uneven low-carbon transition? Assessing evidence from a mixed-method elite study. Environ. Sci. Policy 2021, 124, 370–379. [Google Scholar] [CrossRef]

- Eicke, L.; Weko, S.; Apergi, M.; Marian, A. Pulling up the carbon ladder? Decarbonization, dependence, and third-country risks from the European carbon border adjustment mechanism. Energy Res. Soc. Sci. 2021, 80, 102240. [Google Scholar] [CrossRef]

- Wall Street Journal, Here Come the Climate Protectionists. 11 July 2021. Available online: https://www.wsj.com/articles/here-come-the-climate-protectionists-11626042142 (accessed on 4 August 2021).

- UNCTAD. A European Union Carbon Border Adjustment Mechanism: Implications for Developing Countries. 2021. Available online: https://unctad.org/webflyer/european-union-carbon-border-adjustment-mechanism-implications-developing-countries (accessed on 27 September 2021).

- Quick, R. Carbon Border Adjustment: A Dissenting View on Its Alleged GATT-Compatibility. Nomos eLibrary. 2021. Available online: https://www.nomos-elibrary.de/10.5771/1435-439X-2020-4-549.pdf?download_full_pdf=1 (accessed on 5 August 2021).

- Englisch, J.; Falco, T. EU Carbon Border Adjustments for Imported Products and WTO Law. 2021, pp. 14–75. Available online: https://ssrn.com/abstract=3863038 (accessed on 4 October 2021).

- Krenek, A. How to Implement a WTO-Compatible Full Border Carbon Adjustment as an Important Part of the European Green Deal. Österreichische Gesellschaft für Europapolitik, ÖGfE Policy Brief. 2020. Available online: https://www.oegfe.at/policy-briefs/wto-compatible-bca-green-deal/?lang=en (accessed on 22 July 2021).

- Han, J.H. Competition and Coexistence of International Trade Norms and Environmental Norms: Focusing on the EU Carbon Border Adjustment Mechanism. Rev. Int. Area Stud. 2021, 30, 156–162. [Google Scholar]

- Kim, H. Carbon Border Adjustment and Its WTO Compatibility Issues: GATT Articles II, III & XX. Int. Trade Law 2021, 151, 3–54. [Google Scholar]

- Falcao, T. Ensuring and EU Carbon Tax Complies with WTO Rules. Tax Notes Int. 2021, 101, 43–47. [Google Scholar]

- Lehne, J. The EU Can’t ‘Go it Alone’ on Border Carbon Adjustments. E3G Commentary, 8 October 2020. Available online: https://www.e3g.org/news/the-eu-can-t-go-it-alone-on-border-carbon-adjustments/(accessed on 4 October 2021).

- Pauwelyn, J.; Kleimann, D. Trade-Related Aspects of a Carbon Border Adjustment Mechanism; A Legal Assessment; European Parliament, Directorate-General for External Policies: Brussel, Belgium, 2020. [Google Scholar]

- Van Asselt, H. The Prospects of Trade and Climate Disputes before the WTO. In Climate Change Litigation: Global Perspectives; Brill Publishing: Leiden, The Netherlands, 2020. [Google Scholar]

- KOTRA. Progress of EU CBAM and Prospect. Global Market Report 21-010, 2021, 7. Available online: https://news.kotra.or.kr/user/reports/kotranews/20/usrReportsView.do?reportsIdx=12965 (accessed on 1 September 2021).

- European Parliament. REPORT towards a WTO-Compatible EU Carbon Border Adjustment Mechanism. 2021. Available online: https://www.europarl.europa.eu/doceo/document/A-9-2021-0019_EN.html (accessed on 4 October 2021).

- Kang, S. Carbon Border Tax Adjustment from WTO Point of View; Working Paper No. 2010/08; Society of International Economic Law (SIEL): London, UK, 2010; pp. 5–11. [Google Scholar]

- Hertel, T.W.; Walmsley, T. China’s Accession to the WTO: Timing Is Everything; GTAP Working Papers 403; Center for Global Trade Analysis, Department of Agricultural Economics, Purdue University: West Lafayette, IN, USA, 2000. [Google Scholar]

- Hertel, T.; Tsigas, M. Structure of the GTAP model. In Global Trade Analysis: Modeling and Applications; The Press Syndicate of the University of Cambridge: New York, NY, USA, 1997. [Google Scholar]

- Ianchovichina, E.; Walmsley, T.L. Dynamic Modeling and Applications for Global Economic Analysis; Cambridge University Press: New York, NY, USA, 2012. [Google Scholar]

- Cheong, I.; Cho, J. The impact of Korea’s FTA network on seaborne logistics. Marit. Policy Manag. 2013, 40, 146–160. [Google Scholar] [CrossRef]

- Cho, J.; Hong, E.K.; Yoo, J.; Cheong, I. The Impact of Global Protectionism on Port Logistics Demand. Sustainability 2020, 12, 1444. [Google Scholar] [CrossRef] [Green Version]

- UNCTAD. UNCTAD Comtrade Database. Available online: https://comtrade.un.org/data/ (accessed on 29 September 2021).

- World Bank. Carbon Pricing Dashboard. 2021. Available online: https://carbonpricingdashboard.worldbank.org/map_data (accessed on 29 September 2021).

Figure 1.

Channels of impacts of the CBAM.

Figure 2.

Structure of the GTAP model, and adjustment of expected ROR and actual ROR. Source: [54,55], recited from [56,57].

Figure 3.

Trend of the EU’s carbon pricing. Note: Estimates from 2022. Source: Author’s calculation based on [59].

Figure 3.

Trend of the EU’s carbon pricing. Note: Estimates from 2022. Source: Author’s calculation based on [59].

{kind=link}

{kind=link}

{kind=link}

Table 1.

Possible incompatibilities between the CBAM and GATT/WTO articles.

| GATT/WTO Article | Key Issues | Possible Incompatibility | Note |

|---|---|---|---|

| GATT Article I: General Most-Favoured-Nation (MFN) Treatment | Article I is the most fundamental GATT principle banning discriminatory treatment between members. Thus, there should not be any discrimination in tariffs, fines, import/export regulations, procedures, and more, for all members. | The EU will assess the border adjustment tax in different ways considering CO2 content, environmental regulations, and technology of exporters on a particular item. Therefore, this is clearly incompatible with the MFN treatment principle. | There is no way to resolve the incompatibility issue with Article I as of now (Englisch and Falcao, 2021). |

| GATT Article II: Schedules of Concessions; Clause (a) Border Adjustment Tax (BAT) | “A penalty, commensurate to an inland tax, on all or partial goods which contribute to manufacturing or production of imports or domestic goods” is included in Article II Clause (a). Whether the CBAM does apply to the BAT or not is a critical issue. | Although the EU maintains the CBAM is not a BAT, non-EU countries with higher tariff burdens tend to view it as a BAT. | If the CBAM tariffs exceed the EU’s binding tariffs, the situation could get worse. |

| GATT Article III: National Treatment on Internal Taxation and Regulation | In principle, an inland tax or other penalties that are normally not imposed on domestic goods must not be imposed on foreign goods (the GATT’s second principle). | The carbon adjustment tax is imposed only based on carbon content. This can violate the national treatment principle. | There is a limitation on the EU when assessing the carbon content of all imports. Also, other technical issues can arise. |

| GATT Article XX: General Exceptions | The CBAM-related aspects in Article XX are clauses (b) and (g) as well as the chapeau clause. Clause (b): A measure on health and life protection of humans and animals/plants. Clause (g): A measure on preservation of limited natural resources. Chapeau: The environmental preventive measures must not be used as a “willful” or “unfair discriminatory tool” between countries in similar conditions. | Clauses (b) and (g) can be compatible. However, the CBAM must be applied in the same manner as a domestic carbon tax. There must not be any willful or unfair discriminatory tool, as declared in the chapeau. It depends on the regulations mentioned in the chapeau clause. | If the CBAM is permitted as a general exception, other countries’ imposition of carbon taxes must also be allowed. That is, there is the possibility that protectionism will prevail. |

| GATT Article XI: General Elimination of Quantitative Restrictions (QR) | This is one of the GATT’s top three principles. The article bans quantity restrictions and import licensing; only tariffs, taxes, and penalties are allowed. | Based on this article, the way the CBAM enforces foreign producer participation in the EU ETS can be interpreted as a form of QR. Thus, this is incompatible with the WTO agreement. | In this case, the costs of the CBAM can be increased due to the QR. |

| GATT Article XXI: Security Exceptions | When members seek to protect critical national security interests, they can take exceptionally necessary measures under this article (specifically, during wartime or other internationally urgent circumstances). | Whether the Intergovernmental Panel on Climate Change (IPCC) announcement can be construed as being for security purposes or not will be a critical point. | Similar measures adopted by their countries will also have to be approved as a national security exception. |

| WTO Agreement Clause 3 of Article IX and Clause 4 of Article XVI | If it is difficult for a member country to implement a WTO agreement due to an “exceptional circumstance” the country can ask for a waiver of duties, but all member countries must agree to grant the waiver. | If the CBAM is considered a critical situation, it can be deemed an “exceptional circumstance”, and thus, the EU can request a waiver. | Since the WTO requires unanimity, the likelihood of receiving a waiver is remote. |

Source: Authors’ summary based on the Articles of the GATT.

Table 2.

Summary of the EU’s Carbon Border Adjustment Mechanism.

| Classification | Major Summary |

|---|---|

| Purpose |

|

| Time of introduction |

|

| Target countries |

|

| Types of items |

|

| Measures |

|

Source: CBAM plan by the EU.

Table 3.

Top 20 countries exporting major steel and mineral products into the EU. (Unit: billions USD).

Table 3.

Top 20 countries exporting major steel and mineral products into the EU. (Unit: billions USD).

| Country | Aluminum | Cement | Electricity | Fertilizer | Iron and Steel | Total |

|---|---|---|---|---|---|---|

| China | 4.2 | 0.0 | 0.0 | 0.1 | 15.1 | 19.4 |

| Russian Federation | 2.8 | 0.0 | 0.7 | 1.7 | 5.9 | 11.1 |

| Turkey | 1.8 | 0.1 | 0.1 | 0.1 | 7.4 | 9.5 |

| India | 0.5 | 0.0 | 0.0 | 0.0 | 4.1 | 4.6 |

| USA | 1.0 | 0.0 | 0.0 | 0.1 | 3.4 | 4.6 |

| Rep. of Korea | 0.3 | 0.0 | 0.0 | 0.0 | 4.0 | 4.3 |

| Ukraine | 0.0 | 0.0 | 0.4 | 0.1 | 3.8 | 4.3 |

| Serbia | 0.3 | 0.0 | 0.5 | 0.1 | 1.0 | 2.0 |

| Brazil | 0.0 | 0.0 | 0.0 | 0.0 | 1.8 | 1.9 |

| United Arab Emirates | 1.5 | 0.0 | 0.0 | 0.0 | 0.3 | 1.8 |

| South Africa | 0.5 | 0.0 | 0.0 | 0.0 | 1.1 | 1.5 |

| Japan | 0.1 | 0.0 | 0.0 | 0.0 | 1.3 | 1.4 |

| Belarus | 0.0 | 0.0 | 0.0 | 0.5 | 0.7 | 1.3 |

| Egypt | 0.4 | 0.0 | 0.0 | 0.5 | 0.2 | 1.2 |

| Vietnam | 0.1 | 0.0 | 0.0 | 0.0 | 1.1 | 1.2 |

| Mozambique | 1.1 | 0.0 | 0.0 | 0.0 | 0.0 | 1.1 |

| Bosnia Herzegovina | 0.3 | 0.0 | 0.3 | 0.0 | 0.5 | 1.0 |

| Canada | 0.3 | 0.0 | 0.0 | 0.2 | 0.3 | 0.8 |

| Malaysia | 0.2 | 0.0 | 0.0 | 0.0 | 0.6 | 0.8 |

Note: Aluminum (76, HS code), Cement (2523), Electricity (2716), Fertilizer (31), Iron and Steel (72, 73). Source: Authors’ calculation based on the UN Comtrade Database [58].

Table 4.

Disaggregation of countries and sectors.

| Countries and Sectors | Disaggregated Countries and Sectors | |

|---|---|---|

| Countries (18) | Belarus, Brazil, Canada, China, Egypt, India, Japan, Rep. of Korea, Malaysia, Russia, South Africa, Turkey, United Arab Emirates, Ukraine, U.S., U.K., Mozambique, Rest of the World (ROW) | |

| Sectors (GTAP code, 35) | Energy-intensive Sectors (10) | Coal, Oil, Gas, Paper, Aluminum, Steel, Oil_pcts, Cement, Chemicals, Electricity |

| Others (25) | Afs, Cmn, Cns, Edu, Eeq, Ele, Fmp, Fsh, Ins, Lum, Mvh, Oap, Obs, Ofd, Ofi, Ome, Omf, Otp, Ros, Tex, Trd, Whs, Wtp, Wtr, Oth_ind_ser | |

Source: Authors’ clarification based on the GTAP Data v.10.

Table 5.

Summaries of the simulation scenarios.

| Scenario | Target Countries | Time Period | Carbon Price | Energy Efficiency |

|---|---|---|---|---|

| 1 | EU → the world (except those that have implemented an ETS or anticipate implementation) | Analysis of change in trends over 15 years (‘21~’36) | 67.2 USD/t~122.5 USD | Increasing by 1.5% for 5 years in technology efficiency of the EU |

| 2 | EU → the world | |||

| 3 | EU → the world; the world → EU | |||

| 4 | The world → the world |

Note: EU includes countries in the EFTA, such as Switzerland; the world excludes the EU.

Table 6.

The status of ETS implementation.

| Status | Country | Title of Initiative | Year of Execution | GHG Emission (MtCO2e) |

|---|---|---|---|---|

| Implementation (10) | China | China’s national ETS | 2021 | 3996.90 |

| EU, EFTA | EU ETS | 2005 | 1725.77 | |

| South Korea | Korea ETS | 2015 | 513.42 | |

| Germany | Germany ETS | 2021 | 398.62 | |

| Mexico | Mexico pilot ETS | 2020 | 328.72 | |

| United Kingdom | U.K. ETS | 2021 | 192.43 | |

| Kazakhstan | Kazakhstan ETS | 2013 | 156.52 | |

| Canada | Canada federal OBPS | 2019 | 73.52 | |

| New Zealand | New Zealand ETS | 2008 | 45.25 | |

| Switzerland | Switzerland ETS | 2008 | 6.04 | |

| Review of implementation (11) | Chile, Colombia, Indonesia, Japan, Montenegro, Serbia, Thailand, Turkey, Ukraine, Vietnam, Pakistan | |||

| No implementation | ROW | |||

Note: The jurisdiction targets the ETS of the country (national) or the economic bloc (regional); an ETS in regions within countries (subnational) is assumed to be non-implementation. Source: Adapted from [59].

Table 7.

EU carbon tariff equivalents by importer (44 USD/Mt). (Unit: [%]).

| Country | Paper | Aluminum | Steel | Oil_Pcts | Cement | Chemicals | Electricity | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Belarus | 1.7 | (0) | 0.7 | (1.9) | 2.9 | (0) | 1.4 | (1.4) | 30.3 | (2.8) | 4.4 | (3.4) | 11.3 | (0) |

| Brazil | 0.8 | (0) | 4.4 | (1) | 3.3 | (1) | 0.9 | (1.9) | 7 | (0) | 0.8 | (4) | (0) | |

| Canada | 1.3 | (0.2) | 1.3 | (1.4) | 2.2 | (0.3) | 1.3 | (1.4) | 4.1 | (0.1) | 2.2 | (1.1) | (0) | |

| China | 1.7 | (0.1) | 2.4 | (5.3) | 3.7 | (0.5) | 2.3 | (0) | 10.3 | (4.6) | 3 | (4.6) | (0) | |

| Egypt | 2.3 | (0) | 2.4 | (0) | 5.9 | (0) | 0.7 | (0) | 10.6 | (0) | 5.4 | (0) | (0) | |

| India | 4 | (0) | 5.6 | (1.8) | 12.6 | (0) | 0.9 | (1.4) | 22.1 | (0.3) | 4.6 | (3.4) | (0) | |

| Japan | 1 | (0.1) | 0.4 | (2.7) | 1 | (0.1) | 0.8 | (0.9) | 5 | (2.7) | 1.4 | (3.8) | (0) | |

| Rep. of Korea | 1 | (0) | 0.6 | (0) | 1.5 | (0) | 0.8 | (0) | 4.8 | (0.1) | 1.2 | (0.3) | (0) | |

| Malaysia | 1.4 | (0.1) | 2.6 | (2.4) | 3.3 | (0.3) | 4.6 | (1.1) | 6.4 | (5) | 2.6 | (3) | (0) | |

| Russia | 5.1 | (0.1) | 3 | (2.5) | 5.3 | (0.3) | 1.3 | (1.8) | 10.5 | (0.2) | 7 | (3.2) | 20.8 | (0) |

| South Africa | 1.7 | (0) | 6.4 | (0.1) | 6.2 | (0) | 10.4 | (0) | 11.7 | (0) | 4.2 | (0.4) | (0) | |

| Turkey | 1.1 | (0) | 1.2 | (0) | 2.9 | (0) | 1.2 | (0) | 12.3 | (0) | 2 | (0) | 16.6 | (0) |

| United Arab Emirates | 3.1 | (0.1) | 0.8 | (4.5) | 1.9 | (0.3) | 0.7 | (1.4) | 7.6 | (0.4) | 3.7 | (3.2) | (0) | |

| Ukraine | 1.6 | (0) | 5.3 | (0.9) | 9.2 | (0) | 3.1 | (0) | 18.7 | (0) | 10.8 | (1.3) | 15.6 | (0) |

| U.S. | 0.7 | (0.1) | 1.2 | (2.3) | 1.5 | (0.5) | 1.3 | (1.4) | 3.2 | (2.1) | 1.2 | (2) | (0) | |

| U.K. | 0.2 | (0) | 0.1 | (0) | 0.3 | (0) | 0.6 | (0) | 0.6 | (0) | 0.1 | (0) | 7.8 | (0) |

| Mozambique | 0.3 | (0) | 4.6 | (0) | 11.3 | (0) | 1 | (0) | 1.8 | (0) | 0.8 | (0) | (0) | |

| ROW | 0.3 | (0) | 4.6 | (0.2) | 11.3 | (0.1) | 1 | (0.7) | 1.8 | (0.1) | 0.8 | (0.9) | (0) | |

Source: UNCTAD [40] and GTAP Data v.10.

Table 8.

Impacts on trade in the energy sectors. (Unit: [%]).

| Energy Products | Scenario 1 | Scenario 2 | Scenario 3 | Scenario 4 | ||||

|---|---|---|---|---|---|---|---|---|

| Export | Import | Export | Import | Export | Import | Export | Import | |

| Paper | −2.7 | −2.6 | −2.8 | −2.6 | −4.0 | −3.8 | −15.6 | −15.5 |

| Aluminum | −1.8 | −1.7 | −1.8 | −1.7 | −3.0 | −3.0 | −12.6 | −12.6 |

| Steel | −3.8 | −3.6 | −3.9 | −3.7 | −6.5 | −6.3 | −14.2 | −14.1 |

| Oil_pcts | −4.9 | −4.8 | −5.0 | −4.8 | −5.3 | −5.1 | −13.7 | −13.6 |

| Cement | −2.7 | −2.5 | −3.1 | −3.0 | −5.1 | −4.9 | −11.2 | −11.1 |

| Chemicals | −1.4 | −1.4 | −1.5 | −1.5 | −3.3 | −3.3 | −12.8 | −12.8 |

| Electricity | −2.1 | −2.1 | −2.2 | −2.2 | −4.9 | −4.9 | −17.6 | −17.6 |

| Average | −2.8 | −2.7 | −2.9 | −2.8 | −4.6 | −4.5 | −14.0 | −13.9 |

Table 9.

Impacts on trade in energy products. (Unit: [%]).

| Countrie (Order of Carbon Exports) | S1 | S2 | S3 | S4 | Difference | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Export | Import | Export | Import | Export | Import | Export | Import | S3 minus S2 | S4 minus S2 | |

| Russia | −23.7 | −2.2 | −23.5 | −2.1 | −20.3 | −12.4 | −17.3 | −15.3 | 3.2 | 6.2 |

| China | −9.9 | 0.9 | −12.2 | 0.6 | −8.5 | −0.7 | −20.9 | −14.2 | 3.7 | −8.7 |

| Turkey | −12.2 | 0.1 | −20.2 | −0.5 | −17.2 | −6.2 | −23.4 | −10.9 | 3 | −3.2 |

| U.K. | −13.5 | 0.9 | −18.0 | 0.9 | −16.4 | −4.0 | −26.4 | −11.4 | 1.6 | −8.4 |

| Ukraine | −11.0 | −2.5 | −21.5 | −6.1 | −16.6 | −10.7 | −22.4 | −14.3 | 4.9 | −0.9 |

| Rep. of Korea | −7.6 | −1.7 | −8.2 | −1.8 | −4.6 | −1.0 | −20.8 | −13.9 | 3.6 | −12.6 |

| India | −14.6 | −0.4 | −14.5 | −0.4 | −12.0 | −3.4 | −20.5 | −12.1 | 2.5 | −6 |

| Brazil | −9.9 | −0.6 | −9.7 | −0.5 | −7.1 | −2.2 | −19.4 | −12.7 | 2.6 | −9.7 |

| U.S. | −10.5 | 0.1 | −10.3 | 0.2 | −7.1 | −0.8 | −20.3 | −13.5 | 3.2 | −10 |

| South Africa | −11.0 | −1.8 | −10.9 | −1.8 | −9.7 | −5.1 | −16.4 | −13.7 | 1.2 | −5.5 |

| Argentina | −7.3 | −1.4 | −7.1 | −1.4 | −3.0 | −2.4 | −16.2 | −11.9 | 4.1 | −9.1 |

| Mozambique | −8.9 | −7.9 | −8.6 | −7.8 | −5.6 | −7.9 | −18.5 | −8.8 | 3 | −9.9 |

| Egypt | −16.0 | −2.0 | −15.7 | −2.0 | −13.6 | −4.1 | −22.7 | −9.8 | 2.1 | −7 |

| Belarus | −25.9 | −4.3 | −25.7 | −4.0 | −18.9 | −4.3 | −26.1 | −12.7 | 6.8 | −0.4 |

| Canada | −6.4 | −2.3 | −7.4 | −2.4 | −5.3 | −2.2 | −19.1 | −15.0 | 2.1 | −11.7 |

| Malaysia | −8.9 | −1.2 | −8.7 | −1.1 | −4.8 | −0.8 | −20.1 | −10.5 | 3.9 | −11.4 |

| Japan | −7.8 | −0.2 | −8.4 | −0.3 | −4.7 | 0.0 | −19.7 | −14.3 | 3.7 | −11.3 |

| EU27 | 15.7 | −6.6 | 16.5 | −7.0 | 3.5 | −10.1 | −0.4 | −16.9 | −13 | −16.9 |

| ROW | −10.7 | −1.4 | −10.5 | −1.3 | −7.9 | −1.7 | −19.9 | −11.9 | 2.6 | −9.4 |

Table 10.

Impacts on exports of steel and aluminum (Unit: [%]).

| Countries (Order of Carbon Exports) | S1 | S2 | S3 | S4 | ||||

|---|---|---|---|---|---|---|---|---|

| Aluminum | Steel | Aluminum | Steel | Aluminum | Steel | Aluminum | Steel | |

| Russia | −16.1 | −18.9 | −15.4 | −18.8 | −14.0 | −12.6 | −12.3 | −18.1 |

| China | −13.6 | −9.6 | −16.2 | −11.4 | −10.2 | −1.9 | −21.3 | −20.0 |

| Turkey | −16.4 | −12.3 | −19.7 | −14.9 | −17.0 | −8.3 | −28.7 | −22.0 |

| U.K. | −9.5 | −18.7 | −9.3 | −19.0 | −0.1 | −15.2 | −25.4 | −30.1 |

| Ukraine | −15.7 | −14.3 | −14.7 | −24.7 | −11.3 | −18.7 | −24.8 | −21.6 |

| Rep. of Korea | −9.0 | −8.7 | −8.8 | −9.3 | −3.5 | −1.7 | −29.7 | −22.4 |

| India | −8.9 | −22.0 | −8.7 | −21.9 | −14.7 | −13.1 | −19.4 | −22.0 |

| Brazil | −10.1 | −12.7 | −9.8 | −12.5 | −4.3 | −6.6 | −14.3 | −20.4 |

| U.S. | −14.1 | −8.9 | −13.7 | −8.8 | −7.8 | −0.3 | −21.9 | −17.6 |

| South Africa | −12.2 | −12.6 | −12.0 | −12.5 | −9.8 | −7.2 | −12.3 | −16.2 |

| Argentina | −6.7 | −3.6 | −6.4 | −3.6 | −2.8 | 6.5 | −17.3 | −13.3 |

| Mozambique | −57.2 | 0.5 | −56.2 | 0.4 | −58.5 | 14.4 | −23.6 | −16.7 |

| Egypt | −19.8 | −21.4 | −18.8 | −20.9 | −19.0 | −12.0 | −25.8 | −23.4 |

| Belarus | −13.7 | −29.5 | −12.9 | −28.7 | −8.8 | −25.3 | −37.9 | −33.4 |

| Canada | −11.9 | −6.9 | −11.5 | −6.9 | −8.6 | −2.7 | −28.3 | −19.2 |

| Malaysia | −11.4 | −8.9 | −11.0 | −8.9 | −4.8 | 2.3 | −25.4 | −20.1 |

| Japan | −11.0 | −7.5 | −10.7 | −7.5 | −4.3 | 1.7 | −24.4 | −18.5 |

| EU27 | 43.8 | 13.1 | 43.6 | 14.7 | 20.3 | −7.8 | 20.5 | −2.3 |

| ROW | −14.6 | −17.9 | −14.3 | −17.8 | −10.7 | −11.5 | −19.6 | −20.9 |

| Average | −1.8 | −3.8 | −1.8 | −3.9 | −3.0 | −6.5 | −12.6 | −14.2 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Lim, B.; Hong, K.; Yoon, J.; Chang, J.-I.; Cheong, I. Pitfalls of the EU’s Carbon Border Adjustment Mechanism. Energies 2021, 14, 7303. https://doi.org/10.3390/en14217303

AMA Style

Lim B, Hong K, Yoon J, Chang J-I, Cheong I. Pitfalls of the EU’s Carbon Border Adjustment Mechanism. Energies. 2021; 14(21):7303. https://doi.org/10.3390/en14217303

Chicago/Turabian StyleLim, Byeongho, Kyoungseo Hong, Jooyoung Yoon, Jeong-In Chang, and Inkyo Cheong. 2021. "Pitfalls of the EU’s Carbon Border Adjustment Mechanism" Energies 14, no. 21: 7303. https://doi.org/10.3390/en14217303

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.