1. Introduction

The COVID-19 health crisis has had a significant impact on the business environment, especially on small and medium-sized economic entities. According to the report by the Vodafone Group, 57% of small and medium-sized businesses lost orders or contracts due to the pandemic, and 35% of small businesses (SMEs) reported that the pandemic had a significant impact on demand and revenue [

1]. The effects of the health crisis are manifested mainly by the loss of customers and the reduction of orders, which leads the economic entities to: (i) improve the cost management for their efficient monitoring; (ii) improve the quality of services and products; (iii) maintain qualified and performing employees; (iv) adapt to customer needs [

2].

In the financial accounting services sector, the impact of the health crisis is manifested in the inability of employees to work in traditional offices [

3]. At the same time, economic entities have faced staffing crises due to scheduled childcare leave and being forced to resort to staff “rotations” to comply with the regulations of government emergency management bodies [

4]. Entities’ difficulties may be exacerbated by the absence of experts to provide the management information needed for rapid decision making by management, to report on operational activity, or to monitor, for example, working capital and cash flows in a timely manner or daily and/or monthly reports sent to the leadership or to the state institutions [

5]. Regardless of the reasons underlying the crisis, from an accounting point of view, the Romanian economic entities are obliged, according to the legislation in force, OMFP 1802/2014 (for companies whose securities are not traded on a regulated financial market) and OMFP no. 2844/2016 (for companies whose securities are admitted to trading on a regulated market), respectively, to keep up-to-date accounting records and to ensure an internal control of the economic entity that allows it to collect accurate, exhaustive, and timely information. All these day-to-day activities in the financial-accounting departments that support the continuity of data collection and processing put increasing pressure on economic entities which, in a crisis situation, need to focus on preparing the necessary decision-making reports [

6].

In this context, the digital transformation of economic entities and the use of Industry 4.0. specific tools outline a new vision for the business environment, where customer demand, resources, and data are shared, owned, used, and organized to make a product or service cheaper, more efficient, and more sustainable [

7,

8]. The digitalization of companies is associated with disruptive technologies (artificial intelligence, automation of processes by robotics, blockchain, intelligent data analysis, and cybersecurity) that contribute to reshaping the functioning of companies both inside and outside the environment (business partners, workforce, state institutions, etc.) [

9,

10,

11,

12]. At the same time, the global Internet network, enhanced by specific digital transformation technologies such as cloud computing, artificial intelligence, Big Data, Internet of Things (IoT), Internet of Everything (IoE), and augmented reality, contributes to streamlining employee work by using telecommunications and provides real-time connectivity to company-specific processes and information used to assist managerial decisions [

13]. Increasing the pace of digitization in the financial accounting department, by integrating ICT tools, is one of the viable solutions to solve problems related to the inability of employees to carry out their work but also to streamline existing processes. In such a context, the digitization of economic processes was one of the main ways in which the entities managed to cope with the pressure of the COVID-19 health crisis. Digitization has many forms of manifestation, from the use of social networks for entities in the HORECA sector, so that they can deliver products to the customer, to the migration to work from home in the service industry [

14].

The current crisis caused by the COVID-19 pandemic has a significant impact on the degree to which Romania has materialized its efforts to go through the necessary steps for the transition to a digital economy. According to the DESI Country Profile report published in 2021, Romania is advanced in terms of coverage through very high-capacity networks and ranks 14th in the EU in terms of readiness to use 5G networks. However, the same report indicates a shortage of indicators referring to the digital skills of the active population and at the same time indicates a low performance in terms of the degree of digitalization of economic entities and public services [

15]. In the wake of the pandemic crisis, the EC and other agencies have encouraged and financially helped EU member states to adopt digitalization as a measure to protect the population against the spread of the virus and at the same time to adapt to the 21st century technology. At the same time, digitization involves the transformation of information from analog to digital, which makes work faster, easier, and more efficient [

16]. The immediate consequences for economic entities that conventionally adopt access to high-performance tools and technologies are increased efficiency and improved productivity of digitized processes. Digitization is more than a conventional change. It must go beyond the classic patterns of organizational culture. The shift towards digitalization means both a change in the mentality of the human factor, as digitalization is equally about technology and people, and a process that includes a well-organized implementation plan [

17].

The aim of this research is to highlight the impact of the digitalization of accounting on the business environment, the work style, and the role of professional accountants: the paradigm shift. This study is based on theoretical research as well as empirical research based on a questionnaire applied in economic entities, and respondents are both decision makers and professional accountants. Examining the approached topic, the paradigm shift in the accounting profession because of the digitization of accounting, we manage to synthesize the main ideas from the literature and perform research based on a questionnaire in which we validate the stated hypotheses. This study stands out both because of the innovative character of the approached subject, the digitalization of accounting, which represents a concept in full expansion, and because of its practical utility. This is proven by the analyses performed and the conclusions drawn in the context of an economic environment that is constantly looking for solutions. All operations can be moved to a controlled and accessible digital environment that can be accessed from any location.

This article is structured as follows: a review section of the literature, which presents the main concepts specific to the topic of the study, a section on the research methodology used to gather relevant information and data, a section in which the main results are presented from the analysis of the questionnaire, and a section in which the main conclusions of the research are formulated and the directions for future research are proposed.

2. Literature Review

In the 1990s, with the advent of technology, economic entities began to invest more and more in digitalization, which was limited to websites, various pieces of equipment, and programs. Digitization has now reached new heights. A generally accepted definition is difficult to establish because digitization is an abstract term with many variables. According to Ritter and Pedersen, 2020, digitization involves the integration of technology in all sectors of a business and results in fundamental changes in the way it operates and in the value it offers to the end customer, which results in the fact that the digitization process represents, for each business, something completely different, depending on the specifics of the activity, the information needs, and the available resources [

18]. Unlike the banking system, where digitization involves both the transposition of data into the virtual environment and the availability to the customer, in the field of accounting, digitization can mean, for example, the use of integrated business management software applications, available on both mobile devices (phone, tablet) as well as on fixed (desktop) devices.

As of 2020, digitalization has entered all fields of activity as a necessity, as a mandatory decision adopted by the management of economic entities, due to the repercussions of the health crisis. The social distancing measure, taken to combat the COVID-19 pandemic, had an immediate impact on business flows. The impossibility of carrying out activities through physical interaction, face to face, and the impossibility of signing documents, required the rapid reorganization and digitization [

19] of all management and decision-making processes, accounting occupying, in this approach, a central place. The study of the research carried out so far shows that the representatives of the academic environment state that the digitization of the processes in the financial-accounting department aims to [

20]:

Automate accounting processes to increase day-to-day efficiency. Digitization allows you to perform routine tasks at a steady pace (up to five times faster than performing them manually). Thus, the automation of processes leads to a reduction in the time allocated to routine operations, increasing the availability and productivity of employees to perform a larger volume of work. Automation allows for the prevention of human error because it captures information with a high degree of accuracy, both from digital documents and on paper. The computer system then automatically processes these documents and verifies the information based on multiple correlations.

Track and access real-time accounting. Adopting cloud-specific technology allows access to accounting data and locations outside the office. By moving the data to the cloud, it will be possible to follow and streamline in real time the processes in the financial accounting department, with beneficial effects on communication with all actors involved (employees, customers, state, etc.). Through this mechanism, an employee can access the data he needs on his own, without the involvement of colleagues in the department and/or in the economic entity [

21].

Move accounting transactions to geographically positioned employees and customers outside the traditional office [

22]. Cloud accounting allows for openness to remote work for employees and customers, which is a major advantage for the pandemic situation. The COVID-19 pandemic highlighted the ability of economic entities to organize and find alternatives to the lockdown set up by the authorities as a measure to prevent the spread of the virus. Implementing a cloud accounting system provides access to work tools for employees who must work “remotely”. Moreover, the financial accounting processes can be carried out without interruption and in the conditions of isolation imposed on employees.

Cloud accounting platforms use accounting software hosted on remote servers, which is a challenge for professional accountants and entrepreneurs. In the literature, cloud accounting is also found under other names: online accounting, web-based accounting, and real-time accounting [

23]. All these names are synonymous and designate a tool designed to assist professional accountants in their work, both in the classic workplace (office) and in any other places where there is an internet connection [

24]. This way of doing business has many positive effects on economic entities, such as: business efficiency, faster speed and accuracy of data processing, and more efficient use of hardware and software resources [

25]. Cloud Accounting is a modern concept that consists of processing accounting data through Cloud Computing [

26,

27,

28]. This tool is based on a package of services, applications, access to information, and data storage, which the user uses without knowing the physical location and configuration of the system that provides these services.

By opting for Cloud Computing and virtualizing accounting processes—collecting and electronically recording documents—a new accounting model was obtained. Cloud computing involves storing and managing a huge amount of data, pooling, sharing, and allocating resources dynamically and flexibly, and facilitating the efficient exchange and sharing of data [

29,

30]. In this way, some current operations of the supply, production, and inventory processes are performed automatically. In the study written by the team coordinated by Ionescu et al., 2014, they indicate that in stock accounting benefits can be obtained such as [

31]: automatic reporting of stocks, by allocating electronic documents for each transaction; automatic preparation of the list of supplies needed, which after approval, is automatically sent to each supplier; reduction of the time and staff allocated to costing operations by automatic calculation. At the same time, one study [

31] indicates that in terms of fixed assets accounting, in addition to reducing the volume of work, there are also advantages such as: keeping a complete list of each fixed asset, updated in real time; permanent access to all data on fixed assets, from all operational divisions of the economic entity; automatic updating of software with the latest changes in legislation and tax treatment of fixed assets; centralized control over the depreciation policy and the release of various reports on depreciation and amortization of fixed assets; the ability to automatically modify data with purchases, sales, transfers, improvements, or revaluation of fixed assets.

In the literature, the following aspects have been identified that determine the improvement of the professional accountant–entrepreneur relationship [

32,

33,

34,

35]: (i) through built-in technologies, cloud accounting applications offer entrepreneurs the opportunity to scan daily accounting documents issued or received, making them available, in real time, to the professional accountant, who, through the consulting services offered, can optimize and develop the business; (ii) securing access to data on one’s own business is a permanent concern for the entrepreneur, as any lack of confidence in the security of the data in custody can lead to business failure. Cloud computing platforms are constantly improving system security, removing fears about the security and confidentiality of data that is stored on a system in a location other than one’s own office. The confidentiality of financial accounting data is guaranteed to both the contractor and the professional accountant; (iii) streamlining the financial accounting activity by eliminating duplicate information, preventing errors, and increasing data accuracy due to electronic data processing and automation mechanisms of various repetitive tasks generates positive effects in terms of time use and costs associated with accounting activities; (iv) end-user satisfaction with the use of cloud computing tools is due to the positive influence on information quality, the interplay between information technology and managerial decision, with a major impact on meeting their own information needs [

36,

37].

Cloud Accounting also has several disadvantages that we find listed in the literature, as follows: the need for an Internet connection, lack of a specific regulatory framework, ensuring information security that requires three levels of security (network security, server security, and application security), and data privacy issues [

38]. Authors Yau-Yeung et al., 2020 consider that the adoption of internal measures involving the development and structuring of staff implementation and training policies is critical for cloud accounting [

39]. Economic entities can increase their operational efficiency by using the cloud, implementing systemic risk assessments, and creating effective policies and risk response plans that stem from the use of this technology [

40]. Storing data in the cloud can have disadvantages that lie in the risks perceived by users, namely: increased dependence on third parties, loss of data sovereignty, data confidentiality and security, and physical location of data centers of the cloud storage provider [

41,

42]. It turns out that, in addition to innovation and adaptability, new technologies incorporate both benefits and risks that influence the business environment. The main risks identified by the authors who studied this issue [

25,

43,

44], which influence the degree of trust and the reliability of accounting in both classical and digital format, are the losses that may occur in terms of confidentiality, privacy, integrity, and availability of information, key attributes of the accounting system.

What is certain is that through the virtual environment and disruptive technologies, the economy of the 21st century is characterized as a global and real-time economy, aligned with the demands of today’s market. Cloud accounting brings benefits because behind the technology is always a professional who checks and advises entrepreneurs—this expert is relieved by technology of repetitive, time-consuming tasks and now has resources to enhance their “humanity”—customer relations, consulting, and problem solving [

45,

46]. By using cloud accounting applications and modern technologies, the professional accountant is repositioned from a data logger to a business analyst/consultant/strategist. In the current period, the classic way of organizing and keeping accounts is changing. This process is based on the automation of repetitive activities performed by the professional accountant through software that acquires new functionalities (RPA, Machine Learning, OCR).

In this context, David and Cernușca, 2020 research the perception of professional accountants about the future of the accounting profession in the digital age and how they are prepared to deal with this process. The conclusions of the research conducted during 2019 were that the vast majority of professional accountants interviewed are open and aware of the effort they have to make in order to adapt to the challenges posed by the deepening digitalization of accounting. In this regard, the direction that professional accountants need to follow is becoming more and more clear, namely cloud-oriented work, IT skills development, and customer advice [

47]. Another study [

48], in the same area of concern, states that “the accounting profession is currently receptive to technology” and that the current situation requires the profession to keep up with technological evolution. The study appeals to the rule of absolute majority (64.3%) to validate the hypothesis that “accessing documents in different formats for use is a special problem in the missions of professional accountants”. The authors conclude that in the current stage of development of the digital economy in Romania, access for the purpose of using accounting documents in different formats is a special problem in the missions of professional accountants, from the perspective of lack and/or impossibility of obtaining accounting data and lack/restriction of access to data managed by old or new accounting information systems. There is also the problem of the low level of consistency and confidence in the accounting data.

The author Botea, 2018 considers that 97% of accounting is made up of activities that can be digitized [

49]. The role of the accounting profession in the digital age is also studied by Ciubotariu, 2020, who lists the benefits of digitization in the field of accounting (dematerialization of documents, timid attempt to introduce technical advances in ICT in accounting programs, changing the role of the accountant from a simple data operator to a business consultant) and its disadvantages (the need for a fast and stable internet connection, the protection of information against cyber-attacks, the loss of control over the data that is stored in the cloud) [

38]. Based on the findings of the analyzed authors, it can be stated that the role of the professional accountant is changing, and that this transformation must be supported by both the professional body and the university environment by developing skills in data analysis, data security, and advanced use of information technology.

According to the author Ciupală, 2020, the economic evolution and the health crisis of 2020 drove economic agents to adopt business decisions aligned with the realities in continuous transformation [

50]. Businesses require quality, relevant information that accountants need to provide in real time, which helps to increase business efficiency. In such cases, the classic way of exercising the accounting profession, which involves the transmission of documents in order to record them and close the management period (month), is no longer sufficient. The young generation of entrepreneurs (millennials) who are familiar with what is new in the field of ICT and mobile devices and are constantly adapting to the requirements of the business environment, want a different relationship with professional accountants. Millennial expectations include [

51]: adapting professional accountants to the current period and using cloud accounting applications that allow real-time transaction data to be recorded and obtaining advice from professional accountants (e.g., government or European grants, analysis of financial statements to identify deviations and correct them).

The constant adaptation of the accounting system to changes in technology and the way of carrying out the specific activities of accounting in the age of technology are mentioned more and more often in the literature [

52]. Another group of authors [

53] conclude that the role of the professional accountant in the digital age is changing from a man of numbers to a visionary person (with professional reasoning) who thinks analytically and has the ability to interpret the data in the computer systems he works with and detect possible mistakes as a result of programming errors. The ability of the professional accountant to access and process the data stored in a cloud accounting system according to its users is even more important because the information is either sent to decision makers within the entities for business management or the state. The professional accountant manages the relationship of the entrepreneur, through his business, with the state institutions [

54].

In Romania, accounting is connected to taxation. The main users of the information produced by accounting are state institutions. The calculation, reporting, and settlement of taxes and fees due is based on financial accounting data as they result from the application of accounting regulations, restated in accordance with tax law. Digitization at the level of state institutions with a role in collecting taxes and fees, namely the National Agency of Fiscal Administration, the digital transformation of the relationship between the private sector and the tax administration, is part of the process of extending the use of IT technologies to all actors in Romania. As of November 2021, the national system regarding the electronic invoice RO e-Factura is operational in Romania. The administration, operation, and implementation of this system, as well as the electronic invoice at the national level, are regulated by OUG 120/2021. The implementation of this system is done gradually, having in the first phase an optional character, both for the B2G (Business to Government) relationship and for the B2B (Business to Business) relationship [

55]. Therefore, the framework for the use of the Cloud accounting system is created not only as a facility for economic entities, as an element of technological progress, but also in relation to the state, which recognizes and accepts, practically, electronic invoicing (to the detriment of traditional).

Accounting professionals therefore use tools in the field of artificial intelligence due to the power of these technologies to analyze a large set of data and automate repetitive processes. By using these technologies, professional accountants can provide three categories of services [

56]: (i) processing information and providing useful data in the decision-making process, with better and cheaper data; (ii) data analysis and generating new perspectives on the business resulting from data analysis; (iii) consulting, due to the “release of time” that can be used to perform value-added tasks, such as: decision making, problem solving, counseling, strategy development, relationship building, and leadership.

Gușe and Mangiuc, 2022 believe that digitalization will contribute to a reorganization of social contact between people and the business environment, with significant differences between accounting professionals educated in the analog age and those born in the digital age. These differences can be reduced by continuing education and the use of cloud technologies, artificial intelligence, and machine learning [

57]. The digitalization, as well as the transformations imposed by it on the business environment and implicitly on the organizational results, will contribute to the evolution and maintenance of the companies’ reputation and their positioning as actors that contribute to social and environmental sustainability [

58]. At the same time, a positive relationship between digitization and green performance contributes to streamlining technological processes, increasing the speed of information transmission and developing ways of processing it, increasing product quality, etc. [

56,

59,

60]. In the context of these approaches, there is a complex dimension of the phenomenon of digital transformation that both companies and staff go through, and the authors Ionaşcu et al., 2022 consider the digital transformation of companies to be the phenomenon of change that companies support and propagate in the environment in which they operate by adopting, with different intensity, digital technologies [

61].

In contemporary society, the elements specific to the field of information technology are strongly correlated with each other. It can be concluded from the study of scientific literature and articles published in journals dedicated to the fields of accounting and auditing that all aspects of social and economic life are subject to the influence generated by the concept of emerging information technologies. Such a concept includes technologies such as: artificial intelligence, the Internet of Things, software robots, cybersecurity (which currently has a strong echo due to the social conditions generated by the COVID-19 pandemic and favorable technical conditions), accessibility of technology, and very good speed of communications on the Internet. For the topic of analysis, artificial intelligence and software robots play a key role due to the facilities offered by accounting data processing algorithms. Artificial intelligence [

56,

62] is a generic concept that refers to systems that copy human intelligence to perform various activities in work processes and that can be continuously improved based on the information they gather in each work stage. The central concept of artificial intelligence systems is to copy and then surpass the way people perceive and interact with the world.

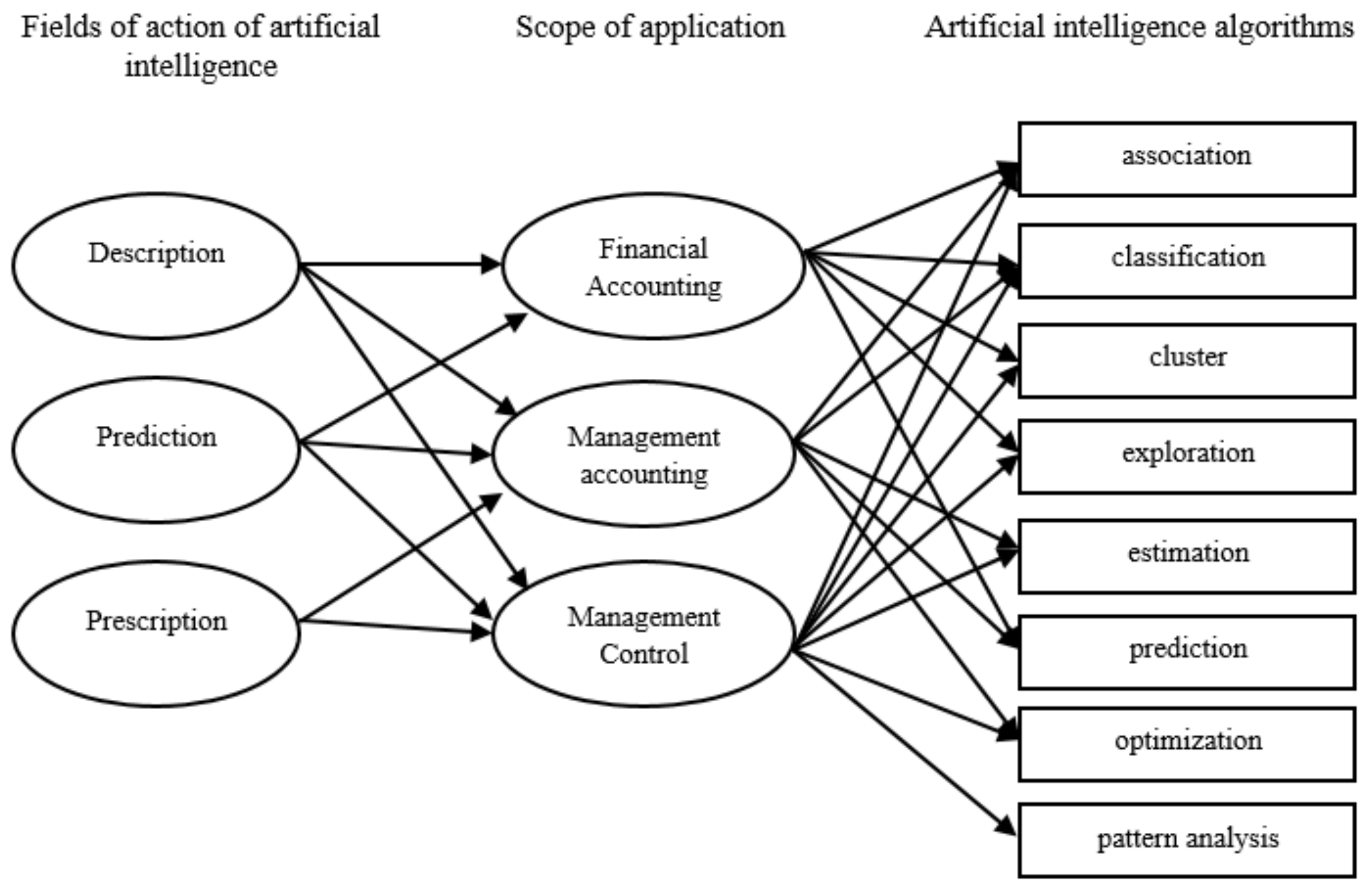

Artificial intelligence [

63,

64] has three areas of action: description, prediction, and prescription. The three fields of action can be described as follows: the description represents the knowledge/understanding of the researched data (what happened), the purpose of the prediction is the use of historical information to decipher the future (what will happen), and the purpose of the prescription is to get the best results (what needs to happen). In relation to these three fields of action of artificial intelligence,

Figure 1 is elaborated, in which the specific elements of artificial intelligence and the financial-accounting system within the economic operators are superimposed.

Analyzing

Figure 1 it can be seen that both financial and management accounting, but especially managerial control, fully benefit from the possibility of applying artificial intelligence algorithms that aim at a better understanding and use of data in the information-accounting system. The link between accounting and managerial control is much better exploited by such technologies due to the fact that the information provided by the first component can be analyzed in detail by algorithms provided by artificial intelligence, resulting in information essential to consolidate/support managerial decision.

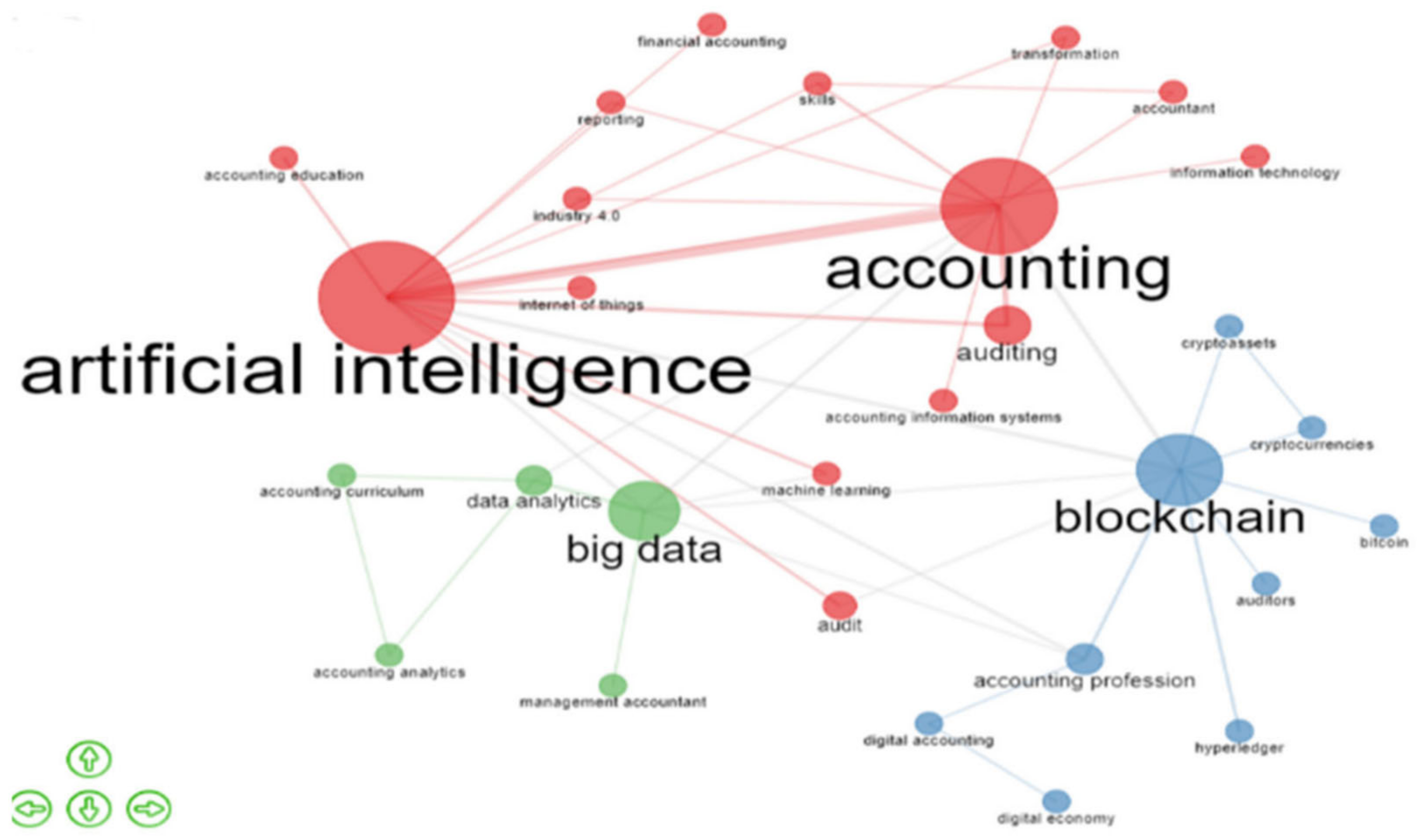

The topicality of the research topic can be appreciated by the interest shown in the scientific, academic, and research environment for the concepts of Cloud Accounting, Artificial Intelligence, Robotic Process Automation, and their connection with the field of accounting. An online search found scientific articles indexed in international databases (Web of Science, Science Direct, Scopus) and in the Google Scholar semantic search engine. Only articles with the following search title, abstract, or keywords were analyzed: “Accountant OR accounting & profession OR accounting & industry * (Topic) and artificial & intelligence OR RPA OR big & data OR emerging & technologist * OR digital * (Topic)”

The text mining analysis performed with the support of the bibliometrix package within the statistical modeling application R highlights the following diagram of the links between the components that make up emerging technologies (artificial intelligence, software robots, Internet of Things, cybersecurity, etc.).

Figure 2 highlights the keywords that frequently appear in articles that match the database query phrase. All the elements that we intuited to be related to the cloud accounting field are found in the previous image: big data, machine learning, internet of things, artificial intelligence, etc.

An in-depth analysis focusing on the emerging information technologies can be seen in

Figure 3, which shows the relationships between information technologies (artificial intelligence, big data, blockchain) and the accounting services industry.

3. Materials and Methods

The issue of this scientific approach is represented by the acceleration of the process of digitization of accounting in the context, on the one hand, of the restrictions of communication between the actors of the economic and social environment, in the traditional, classical, face-to-face environment, and, on the other hand, the orientation towards the virtual environment of activities to a decisive extent for the decision to adopt digitization. In this context, the research sought answers to the following research question: Does the digitalization of accounting, from technology to human resources, lead to a paradigm shift in the mission/role of the professional accountant?

To answer the research question, the following objectives were formulated:

Objective 1: Identify the determinants in the decision-making process regarding the digitization of accounting and establish a hierarchy according to the importance given by the respondents.

Objective 2: To study the existence of dependency/independence between the typology of respondents and to appreciate the advantages of digitizing accounting.

Objective 3: Study the role and challenges for the professional accountant in a digitized environment from the perspective of paradigm shift.

In the next stage of the research approach, the research hypotheses were defined, the verification of which is proposed to achieve the mentioned objectives and answer the research questions.

Hypothesis 1. Digitization of accounting is necessary to ensure business continuity in the event of a pandemic crisis, and it is the result of decisions taken at the level of economic entities and the state, under the influence of determinants.

Hypothesis 2. Between the experience in the field of the respondents and the appreciation of the advantages of the digitalization of accounting, the economic entity has a dependent relationship with the professional accountant and the state.

Hypothesis 3. In a digital environment, the role of the professional accountant evolves towards creative missions of added value for the entrepreneur and his business.

In order to achieve these hypotheses, statistical-mathematical analysis methods adapted to the study were applied. The research is a cross-sectional descriptive study that was conducted between January and February 2021. The questionnaire applied to decision makers in some economic entities and, at the same time, professional accountants. The questionnaire was developed based on the previous literature. Research hypotheses were used to test the link between the variables analyzed. The minimum sample size, determined by SPSS software, was 289 samples. Given this, the values for significance level, power, and effect size were set to 5%, 90%, and 0.5, respectively. All respondents were from Romania, more precisely the southeastern area, the questionnaire being addressed to persons practicing the accounting profession, either as employees of economic entities (economist/accountant; economic/financial accounting director) or independent accounting experts. The elaboration and transmission of the questionnaire was done through the platform

www.isondaje.ro (accessed on 4 March 2022), the generated link being distributed through social networks with the support of some accounting firms. The respondents were their clients.

The questionnaire had the following structure:

Part I, general questions, their role being to provide a more accurate picture of the personal profile of the respondents in the sample (experience gained in the field, gender, legal form of organization of the economic entity, field of activity, membership of national and international professional organizations);

Part II, questions on the extent to which IT technologies are integrated into financial accounting and the perception of them as a solution to pandemic health crisis situations;

Part III, questions on the role of the professional accountant in the context of the digitalization of accounting and, in this context, the change of accounting paradigm.

The typology of the respondents was determined according to the following variables:

Regarding the respondents, they were analyzed according to: the position held in the economic entities, the seniority in the respective position/function, and biological age.

Regarding the entities, the subject of the research, we were interested in: the size of the entities according to the classification in the Romanian legislation, as well as the main field of activity.

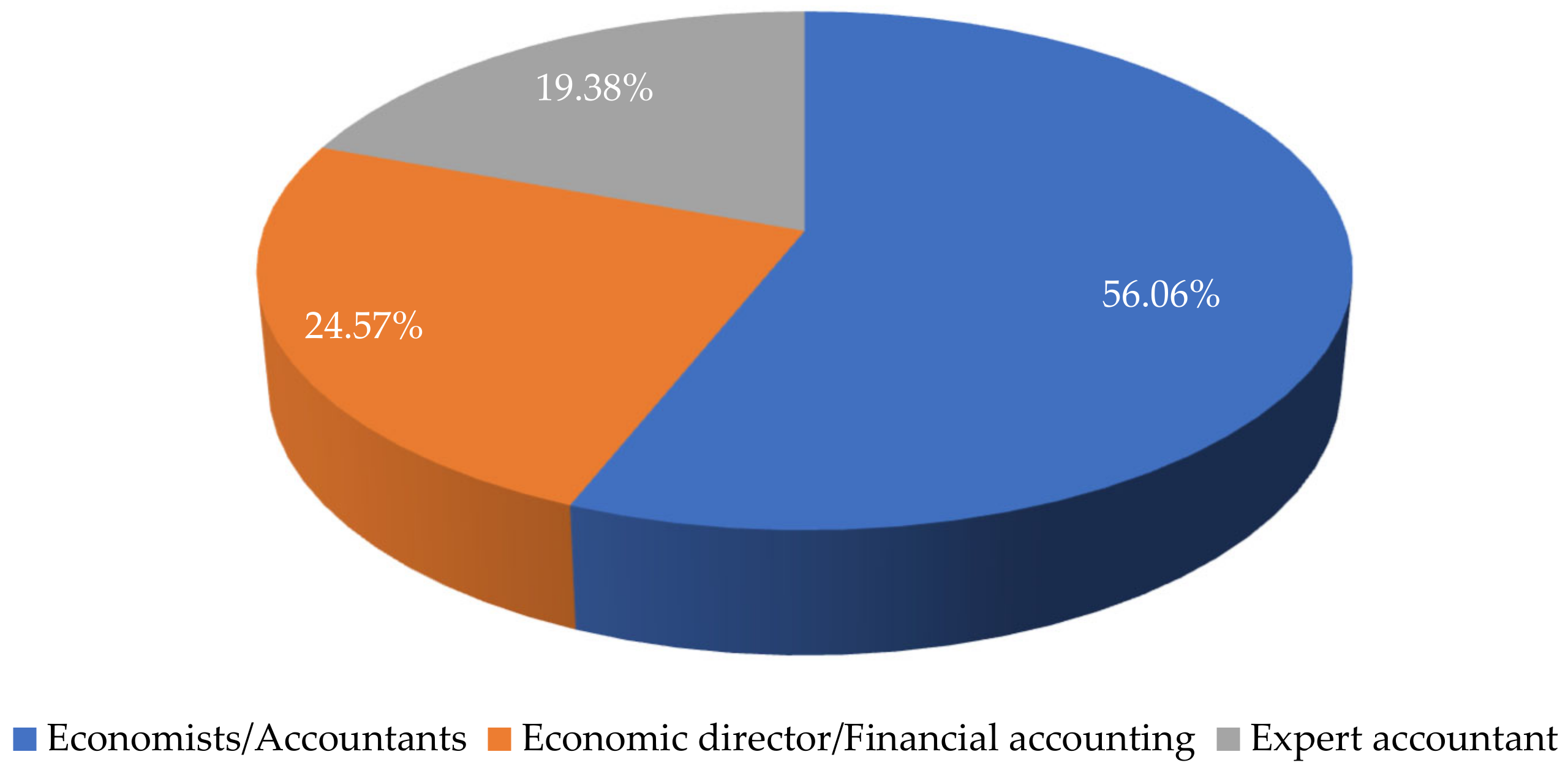

In terms of positions/functions, the distribution of the sample was 56.06% economists/accountants (162 people), 24.56% economic/financial accounting directors (71 people), and 19.38% accounting experts (56 people). The graphical representation is shown below in

Figure 4.

The respondents carried out the activity and made decisions for 179 micro-entities (61.94%), 63 small entities (21.80%), and 47 medium and large entities (16.26%) distributed on fields of activity highlighted in

Table 1.

Table 1 shows that the largest share was held by entities that carry out professional activities, intermediation, and technical and logistical support, which is 47.05% of all entities, respectively. For the other fields of activity, the distribution was relatively the same. The collected data were processed using the IBM SPSS v26 program, and the following statistical tests were performed: Reliability test, Chi-squared, and K related samples. The usefulness of each test is given by the possibilities of processing the data and interpreting the characteristic results, as follows:

Reliability test—is used to determine the consistency of the data by applying the Cronbach’s alpha coefficient test method. The reliability test is valid if the calculated Cronbach’s alpha coefficient is greater than 0.7.

Chi-squared—is used to determine the probability that the variables investigated are independent. This test checks if two variables are associated and if the association is significant. A significance threshold of 0.05 indicates that there is a 5% chance that the collected data will appear randomly.

K related samples (Friedman Test)—is used to analyze non-parametric data, ordinal data in this case, if there are more than two dependent samples. This test is used to test the difference in rank in the case of a variable measured repeatedly, more than twice, on the same group of subjects.

4. Results

The reliability test is used to calculate and determine the consistency of the data in the questionnaire. The reliability of the data is determined in the SPSS analysis application by applying the Cronbach’s alpha coefficient test method.

Table 2 shows the results of the reliability test within the SPSS application. According to the literature [

65], the reliability test is performed for a value of the Alpha Cronbach coefficient that exceeds the threshold of 0.7.

In the study, the result of the Cronbach’s Alpha coefficient indicates a value higher than 0.7, demonstrating the consistency of the processed data.

The starting point in formulating the

Hypothesis 1 is represented by the fact that the studies carried out (since the 1990s) revealed that the digitalization of the activity is an act of management decision, as it involves investments for the integration of new technologies, their size depending on the specifics of the activity, the information needs, and the necessary resources [

18]. Based on the theoretical documentation, we identified and defined seven determining factors, from our point of view, for the decision to digitize business and therefore accounting.

To test this hypothesis, the Friedman test was used, which showed us a hierarchy of the analyzed parameters, with seven determining factors, depending on the importance given by respondents (importance was measured from 1 (least important) to 7 (most important)). The results obtained allowed us to draw the following conclusion: the human component (mean rank 4.89) is decisive in the digitization process, but it must benefit from the necessary technical and technological support (mean rank 4.55), so that the digitization is achieved by optimal configuration according to the functional structure of the entity (mean rank 4.24), according to

Table 3 and

Table 4.

It is recognized that digitization, through the tools used, determines a continuous process of modeling the business environment in all sectors, with significant consequences on the structure and business processes but also on the culture of organizations [

66], confirmed by the study. The change in mentality and way of doing business is expected especially by the young generation of entrepreneurs, willing to bring IT technologies from private life into economic activity, because the current business environment is extremely dynamic and subject to restrictions (including those generated by the health crisis). For an economic entity operating in this environment, it acquires increasing importance because of access to information, speed of transmission, speed of decision making, mobility, and flexibility. Therefore,

Table 5 below presents the presentation of the correlation between the age of the respondents, their position/function, and their experience in the position/function occupied.

In the age category 25–35 years, the total number of respondents is 212, i.e., 73.35% of the total, 78.30% of them having an experience between 3 and 20 years. We can conclude that our study has helped to confirm the fact that digitalization responds mainly to the needs of young entrepreneurs who are largely familiar with the information and communication technologies involved in the digitalization of economic activity, including accounting.

Regarding the

Hypothesis 2, David and Cernușca, 2020, indicated the recognition by professional accountants of the need to adapt to the challenges of the digitalization of accounting, the efforts being dependent on the extent to which professional accountants are aware and appreciate the benefits of integrating information technology in their business [

47]. From this point of view, it was a challenge to analyze the extent to which the experience of professional accountants influences or does not influence their perception of the digitalization of accounting. The analysis of the existence of some dependency/independence relations between the typology of the respondents and the impact of the digitalization of accounting on the economic entities was carried out considering the following two aspects of their activity:

The interaction with the external environment of the entity, the aspect subject to analysis being the process of drawing up/transmitting the financial/fiscal reports to the state and other third parties.

The decision-making process, as an element of the internal environment of the entity, the aspect subject to analysis being assisting the managerial decision based on the data provided by the financial/accounting information system.

Given the fact that in Romania entrepreneurs face the obligation of financial and fiscal reporting to the state and that calculations of taxes and fees based on legislation are difficult to apply (on the one hand due to the complexity of regulations and on the other due to the very frequent changes that the Romanian state makes), it was interesting to investigate the perception of the decision makers/professional accountants regarding the impact of digitalization on the process of preparation and transmission of financial/fiscal reports to the state and other third parties. Respondents were asked to assess the importance of this impact by giving one of the following ratings: not important, of medium importance, or very important, the result being that 242 people out of a total of 289 appreciated this impact to be very important, i.e., 83.73%.

In the first case, by applying the Chi-square test, we formulated the null hypothesis: there is no connection between the respondents’ experience and the importance given to the impact of digitalization on the process of preparing/transmitting financial/fiscal reports to the state and other third parties. The result obtained is presented in

Table 6.

The null hypothesis is confirmed, which means that regardless of the experience in the field of activity, the role of IT technologies adopted in the entity by the digitization decision is recognized as very important. This is vital in the conditions of a pandemic crisis when the only way to communicate is through the virtual environment.

In the second case, by applying the Chi-square test, we formulated the null hypothesis: there is no connection between the respondents’ experience and the importance given to the impact of digitalization on the process of assisting managerial decisions based on data provided by the financial/accounting information system. The result obtained is presented in

Table 7.

The null hypothesis is also confirmed regarding this second aspect X2 (9, N = 289) = (25.418, p < 0.005)

Facilitating all processes both inside and outside the company through digitization is ensured by the fact that it allows operations to be carried out so that stakeholders have real-time access to information relevant to substantiating decisions. When asked about this advantage of digitization, the respondents answered according to the situation in

Table 8.

Applying the Chi-square test, this time the null hypothesis between the respondents’ experience and the real-time access to information facilitated by digitization was not confirmed. The two variables were independent, see

Table 9.

The necessary financial resources, i.e., the costs associated with the adoption of digitization in economic entities, are not listed as a determining factor for the digitization decision on the first positions resulting from the application of the Friedman test (

Table 4). However, respondents, regardless of their experience, greatly appreciated the opportunity to allocate funds for the digitization of financial accounting activity in the context of alignment with the new work culture induced by the health crisis. The correlation analysis performed in

Table 10 and the calculation of the Chi-square test in

Table 11 revealed that the two variables are independent.

The conclusions that can be drawn up to this point in the research are set out below. Validation of Hypothesis 1: Digitization of accounting is a necessity to ensure business continuity in the conditions of the COVID-19 pandemic crisis, and it is the result of decisions taken at the level of economic entities and the state, under the influence of determinants.

In our opinion, the positioning of the organizational culture takes first place as a determining factor in the decision to digitize. The dependence of the implementation of digitization on telecommunications infrastructure and government electronic services and an optimal configuration according to the functional structure of the entity are elements that validate the hypothesis. The digitization of the economy in general and of accounting in particular are dependent on both the human factor and the available technological resources.

We analyzed the perception of respondents, decision makers, and accounting professionals alike regarding the importance of users’ access to data and financial accounting information in the context of the activity in the virtual environment. This included the components of permanent interaction, storage capacity, and the processing of a large volume of data in secure conditions. We obtained these results by applying the Friedman test with the following hierarchy of possibilities/opportunities to continue the activity offered by IT technologies in the context of a pandemic health crisis,

Table 12.

Invalidation of Hypothesis 2: Between the experience in the field of the respondents and the appreciation of the advantages of the digitalization of accounting for the economic entity in the relationship with the professional accountant and the state, there were dependency relations. Whether it was about assessing (1) the impact of digitization on the process of preparing/transmitting financial/fiscal reports to the state and other third parties, (2) the impact of digitization on the process of assisting management decisions based on data provided by the financial/accounting information system, (3) the extent to which digitization facilitates real-time access to information, or (4) the appropriateness of allocating funds for the digitization of financial accounting activity in the context of alignment with the new work culture induced by the health crisis, the results of the Chi-square test revealed, in all cases, independence between variables. Therefore, the integration of information technology in financial accounting activity is a facilitator of communication between economic actors (professional accountant–entrepreneur–state) and, practically, the implementation of accounting digitalization is a real act of assuming managerial responsibility by the entrepreneur. In addition, the professional accountant intervenes both in the management of the business and in the management of the entrepreneur’s relationship with the state institutions, relative to his business. This is why our scientific approach continues: in order to achieve the third objective and verify the Hypothesis 3.

The digital transformation of companies—the reorganization of the relationship between the professional accountant and the business environment under the impact of digitalization—prompts a repositioning of the professional in terms of his training needs and the mission and roles of a digital society [

57,

58,

61].

The preceding paragraphs show that digitization is a broad concept which spans from ensuring more stable and more connected Internet connectivity to the implementation of software for automation and access to cloud services. The use of hosted applications in a cloud-like infrastructure helps reduce costs and increase business efficiency while providing a climate of protection for employees and entrepreneurs. One of the consequences of the dynamic evolution of the digitalization of accounting is the change of attitude of professional accountants regarding the provision of value-added consulting services for clients, the profession becoming an integral part of corporate governance.

This migration of the role of professional accountant from service provider—data recorder to business partner—data valorizer, is also confirmed in the case of our study. The role of data analyst and business evaluator was mentioned by 122 respondents, 42.22%, while 81 of them mentioned the role of advisor and business strategist, representing 28.02% of the total (

Table 13).

Applying the Chi-square test,

Table 14, to verify the null hypothesis between the respondents’ position/function and the assessment of the role of the professional accountant in a digitized environment, there is no dependence. The result is that the hypothesis is invalid X

2 (9, N = 289) = (15.410,

p > 0.005), the conclusion being that regardless of the position held (Economist/Accountant, Economic/Financial Accounting Director, Chartered Accountant), the respondents recognize the paradigm shift of the role of the professional accountant.

Next, an analysis of the dependency/independence relationship between the experience in the position/position held by the respondents and the role they assign with priority to the professional accountant in a digital environment is considered relevant for the study. Through the descriptive statistical analysis of the two variables, we obtained the result presented in

Table 15 in which it can be seen that the highest values obtained for the two roles associated with the professional accountant, Business Advisor and Strategist, and Data Analyst and Business Evaluator, were registered on the experience categories 3–10 years and 10–20 years.

The Chi-square test performed in

Table 16 confirms the dependence between the analyzed parameters, the null hypothesis, the respondents’ experience, and the role of the professional accountant in a digitized environment. There is no dependence, so it is invalidated.

Regardless of the role those professional accountants play in their relationship with entrepreneurs, the demands of a digital environment require them to have or acquire specific IT skills, which is why we analyzed the agreement/disagreement of respondents on the need to include training professionalization of IT issues. We also achieved a hierarchy of areas of competence in

Table 17.

In our opinion, the answers to this question and the hierarchy obtained highlight the primary problem that arose in the conditions of the pandemic, that of the restriction of physical interaction between business actors, entrepreneurs, employees, professional accountants, and state agencies/institutions. This is why the facility offered by digitalization, that of permanent interaction provided by the virtual environment, was mentioned in the first place by the respondents. Detailed frequency by assessment categories is shown in

Table 18.

Hypothesis 3: In a digital environment, the role of the professional accountant is evolving towards creative missions of added value for the entrepreneur and his business is validated.

6. Conclusions

The conclusions drawn from the study, respectively “Digitization of accounting leads to a paradigm shift on the mission/role of professional accountant” can be formulated as follows: (i) Digitization of activity in general and financial accounting in particular is a facilitator of communication between economic actors from entrepreneurs and professional accountants to the state and other third parties. Positive impact: Ensuring business continuity during pandemic crisis and accessing information in real time, virtual space, as opposed to physical space, virtually eliminating the time gap between when information is generated and when it can be accessed by the beneficiary.; (ii) The determinants of the decision to digitize the business, implicitly of the financial accounting activity are both related to the internal environment of the economic entity, organizational culture and the need for optimal configuration according to the functional structure of the entity, and the external environment, respectively telecommunications infrastructure and services, government electronics. Positive impact: Generating data and information adapted to the information needs of users for business management as well as for interaction with all actors in the business environment, from customers and suppliers to state bodies and institutions.; (iii) The migration of the role of the professional accountant from the registrar of figures, calculation of taxes and fees to the capitalizer of data and useful information in the decision-making process as well as in the interaction with the state. Positive impact: The development of partnerships with professional accountants designed to contribute to increasing the performance of economic entities, with a favorable influence on the entire economy.

The digital adaptation allows the accounting departments to respond and adapt to crisis situations, in this case the pandemic crisis whose “new normality” has limited the physical contact between people, respectively the physical circulation of documents. In these circumstances, the entities whose financial-accounting departments were digitized best and quickly managed to adapt, even if this digitization was limited to automated processing and remote access of data.

The evolution of the accounting professional from the accounting period based on stand-alone software programs and physical documents to the digital age in which accounting programs move to the cloud is accompanied by the paradigm shift on the role of the professional accountant for the entrepreneur, both in terms of business management and communication management with state institutions. According to the authors, the accounting profession, as part of the financial accounting management carried out within economic entities, is integrated into the digital economy through elements such as: Artificial Intelligence, Blockchain, and Robotic Process Automation, which are part of the category of emerging information technologies with an exponential development due to favorable technical and social conditions. The research carried out is useful for entrepreneurs, professional accountants and other actors in the business environment who will use in a permanent and complete way the facilities offered by information technologies in their entire activity.

The limit of the study can be considered the limited geographical representation in Romania, more precisely the southeastern part of the country. At the same time, it should be noted that the study was based on qualitative questions, the answers being under the impact of the particularities of behavior, mentality, and culture of the professional accountants’ respondents. The period in which the study was conducted was also under the impact of the pandemic crisis of COVID-19, a period marked by a widespread digitization at all levels of economic and social life, which may be a disruptive factor of respondents’ perception of the phenomenon of digitization.

Future research perspectives aim to expand the study to other countries in South-Eastern Europe, with results that may highlight cultural differences, behaviors and/or mentality, as well as legislation on the evolution of accounting digitization and the improvement of professional accounting.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}