Syed Usman Qadri

Syed Usman Qadri Zhiqiang Ma1*

Zhiqiang Ma1*- 1School of Management, Jiangsu University, Zhenjiang, China

- 2Department of Management Science, TIMES Institute, Multan, Pakistan

- 3Department of Public Administration, Wuhan University, Wuhan, China

- 4Department of Management Science, Business School, University of International Business and Economics, Beijing, China

- 5School of Information and Computing Sciences, Zhejiang University, Hangzhou, China

The COVID-19 epidemic has damaged developing as well as developed economies and reduced the profitability of several companies. Technological advancement plays a vital role in the company's performance in this current situation. All activities carry on virtually. In this study, the financial performance of enterprises in the South Asian banking industry will be compared before and after the COVID-19 epidemic. Furthermore, the full influence of the pandemic will take place in the long run. This study also explains the technological effect on improving performance, especially during the period of the COVID-19 pandemic. It has an impact on people's social lives as well as the economic world. This study examined a sample of 34 banks from the South Asian region from 2016 to 2021. A Wilcox rank test was used to determine whether there was a significant difference before and after the epidemic era. The overall conclusion of this study is that the COVID-19 pandemic had a significant influence on the bank's financial performance, particularly in terms of profitability. But technological advancement has a positive effect on organizational performance, ultimately increasing the financial performance of South Asian banks. And there is a big difference between pre-pandemic and post-pandemic organizational performance. The findings of this study have significant policy implications since it is clear that cooperation among governments, banks, regulatory agencies, and central banks is necessary to address the financial and economic effects of the COVID-19 pandemic.

1. Introduction

The global pandemic COVID-19, a coronavirus pandemic, has had a disproportionate impact on the world's social, economic, political, and religious systems (1). On December 31, 2019, Dr. Tedros Adhanom Ghebreyesus, Director of the World Health Organization, declared the coronavirus a public health emergency (2). The whole corporate world confronts various obstacles in the business climate in 2020, including the collapse of oil prices and the release of a new version of COVID-19 (3, 4). This destructive and upgraded form of COVID-19 not only has an impact on the health and prosperity of the people living in society, but it also causes instability in the global economy (5, 6). After the declaration of WHO COVID-19 as a worldwide pandemic, the whole globe was declared a global lockdown (7). As a result, both corporate and non-profit organizations have been horrified by the international pandemic issue of COVID-19 (3). This widespread shutdown harmed all macroeconomic metrics (e.g., oil prices, unemployment rates, commodity prices, inflation rates, etc.). Ultimately, many organizations' financial performance suffers, and the majority of employees are dismissed or work from home (2). IMF data shows that global GDP will fall by 3.2 percent in 2020. Furthermore, GDP in advanced markets falls by 4.6 percent, GDP in emerging markets falls by 2.1 percent, and GDP in developing markets falls by 2.0 percent. The author estimates that the firms' second quarter revenues in 2020 will decline by 80 percent, 60 percent, and 50 percent, respectively (8). As a result, the development of this pandemic has necessitated tight and prompt measures and policies from local governments as well as local authorities to restrict viral transmission (9). The rapid reaction of the government and local authorities to the spread of this virus led to behavioral and psychological changes in the general public, as well as a reduction in the social gap between them (9). International authorities have also taken rigorous measures such as banning air travel, halting international tourism, restricting ridership, reducing inter-country travel, and so on (9). The spread of the global pandemic affects the east, west, north, and south counties, and the country faces on economic recession (10, 11). Finally, in 2020, the world economy will confront a major threat in the form of the new COVID-19 pandemic. Furthermore, in this pandemic situation, social work has become increasingly difficult to perform due to lockdown (12, 13). Government restrictions are reducing in-person services in the services sector. The service sector includes banks, telecommunications, financial institutions, postal services, insurance companies, and software development firms (14).

Numerous sectors operate in the global economy, but two (manufacturing and services) are regarded as the most important because they contribute significantly to global GDP. According to the IMF's (15), the services sector contributed 63.6 percent of the world's GDP (16). There is a lot of literature available on the manufacturing sector that is affected by the global pandemic. Therefore, I have selected the services sector to learn about the effect of COVID-19. Erden and Aslan (17) concluded that banks are included in the services sector that has been impacted by the pandemic (18). The term “bank” appears for the first time in history in Italy. There is no common definition of a bank in the international literature. A general definition will be made after a few definitions are given here. A bank is defined as an enterprise that accepts deposits from individuals and invests in various sectors in order to pay the individual a margin (19). The financial performance of the banking sector has had ups and downs during COVID-19 (20). The global financial crisis is a major danger to the banking sector in South Asia, as it reduces banking performance (21). A number of other events that occurred in the past will have an impact on the financial performance of the baking sector. The Crimean War of 1854, which took place between Russia and the Ottomans, affected the banking sector. As a result, the Ottoman bank's performance decreased due to that war. The global financial crisis of 2008 also had a great impact on the banking industry in South Asian banks. Ultimately, it will affect the financial performance of the banking sector. Another event in the downfall of tourism in Sri Lanka is that it accounts for 12 percent of the country's GDP (22). It will also affect the banking sector of Sri Lanka As a result, the financial performance of Sri Lanka's banking sector has deteriorated. The financial crisis of 2008 significantly contributed to the lower efficiency of Bangladesh's banking sector. Burki and Niazi (23) discovered that the banking industry's financial performance declined from 1991 to 2000. The author of the study stated that local banks, as well as international banks and Islamic banks, saw a reduction in performance during and post the pandemic period. As a result, financial performance is seen as a tool for analyzing how firms can successfully execute (24).

All of the preceding discussion was about signaling theory because a bad signal is sent to the market in the form of war, a crisis, or pandemic (25). It will decrease the performance of the different companies. The researcher, (26) argues that the market generates both positive and negative signals for business users. As a result, these signals are regarded by business users as information and educate them about the company's present financial health. Positive and negative signals can have an impact on investment decisions and market circumstances. The COVID-19 sends out negative signals to the market and has an impact on every industry of business. People tend to avoid investing after such a terrible epidemic indicator and prefer to cut their losses by withdrawing investments (27). These types of bad signals will also result in a lower level of economic activity and a reduction in economic growth. The existing literature explores several methods to assess a company's financial performance, such as profitability, liquidity, solvency, and activity (24, 28, 29). A lot of methods are available for financial performance, which include the CAMEL Model, VAIC Model, TOPSIS Model, MCDM Model, DEA Model, and the Financial Ratios Analysis Method (30–36).

There has been a significant disruption in the global business world as many firms have been forced to close due to the current COVID-19 epidemic. Based on the above COVID-19 and financial performance, it is required to undertake research to assess the financial performance of the South Asian banking system both before and after the pandemic. But the advancement and development of technology can have a positive impact on employees' performance as well as improve the overall performance of the South Asian banking industry (37). Technological advancement is the combination of creating new knowledge and generating new ideas that will impact the overall performance of companies (38). Internal business progress drives technological advancement, and internal business progress is dependent on the organizational workforce (39). The studies of Alam and Murad (40); Song et al. (41), Sapta et al. (42) explore that there is a close relationship between technological advancement and employee performance. So, advancements in technology, particularly in ICT (information and communication technology), can result in an increase in productivity or enhanced performance (43). Hence, the objective of this research is to forecast financial performance and the effects of COVID-19 on the financial performance of South Asian banks and also to see if there are any variations in financial performance between the pre and post COVID-19 pandemics. Further, how does technological advancement increase the overall performance of the South Asian banks? The contributions of our research are as follows: Theoretically, it multiplies the effects of COVID-19 on the financial performance of South Asian banks across industries. Most of the previous studies carried out have mainly focused on the effects of the COVID pandemic on the manufacturing sector at the macro-level of the economy. Few researchers focused on the effect of the pandemic on South Asian markets or on Pakistan, Sri Lanka, and Bangladesh's financial markets. Practically, it will assist policymakers in developing policies to deal with COVID-19 pandemics or emergency situations. The final part examines the financial impacts of major pandemics and other uncontrollable events on the economy. The reaction of the markets to COVID-19 has already been studied in detail by Liu et al. (44), Narayan et al. (45), and Wang et al. (46).

2. Related literature and hypothesis development

2.1. Financial performance and ratios analysis

Financial performance analysis is regarded as the most significant analysis since it assists users (investors, shareholders, stakeholders, managers, owners, and so on) in determining whether or not the organization is functioning successfully (47). Ratio Analysis, on the other hand, is a crucial technique for analyzing a company's financial performance (48). It is also beneficial to understand the company's strengths, weaknesses, opportunities, and threats. Based on the information presented above, it is determined that ratio analysis is carried out through the financial statements of the firms in order to learn about the financial performance of the companies. The existing literature (24, 28, 29) divided the ratios into the following main heads, which included profitability, liquidity, solvency, and activity.

2.1.1. Profitability measures

2.1.1.1. Return on assets

There are several ratios that are used to assess a company's earnings and profitability. Balasundaram (49) suggests that ROA is the best way to measure a company's profitability based on these measures. This ratio is used to determine if a company's assets are being used to generate profits as well as how much profit is earned on the basis of the company's assets (50, 51). A higher ratio indicates that the firm is operating well, and vice versa. We use the following formula to compute the ROA: net income/total assets.

H1 There is significant difference in return on assets pre and post pandemic of south Asian banks.

2.1.1.2. Earning per share

This ratio is also used to assess the company's profitability. The study of Darya (52) that the EPS demonstrates a company's performance; if the earnings per share are high, the shareholder wealth is maximized, and the company's rate of return is likewise high (53). This ratio is also beneficial to investors, as they must examine it before investing in any stock. Divide net income by the number of shares in circulation to get earnings per share.

H2 There is significant difference in earning per share pre and post pandemic of south Asian banks.

2.1.2. Performance measures

2.1.2.1. Return on equity

Different ratios are used to assess corporate performance. ROE is the most important ratio for assessing a company's success. The ultimate goal of an investor is to maximize their wealth and grow the margin on their stock in that firm, which can be measured using ROE (54). The higher the ROE, the greater the shareholder wealth. Divide the company's net income by its total equity to arrive at this ratio.

H3 There is significant difference in return on equity pre and post pandemic of south Asian banks.

2.1.2.2. Total assets turnover ratio

Another metric used to assess a company's performance is the Total Assets Turnover Ratio. According to Ellis (55), asset turnover or utilization measures which assets are capable of generating and what the organization really generates from that asset. The research by Jose et al. (56) and Seema et al. (57) demonstrates that asset utilization has a major impact on a firm's financial success. This ratio is calculated by dividing total sales or revenue by total assets.

H4 There is significant difference in total assets turnover pre and post pandemic south Asian banks.

2.1.3. Leverage measure

2.1.3.1. Debt to equity ratio

Solvency ratios are another name for leverage ratios. These ratios indicate a company's capacity to satisfy its short-term and long-term obligations through stock or debt (58). A company that has a larger proportion of debt than equity is more likely to fail (59). In the event of insolvency, the corporation has the capacity to pay its debts promptly by liquidating its assets (59). This ratio is calculated by total liabilities, or debt, divided by total equity.

H5 There is significant difference in debt-to-equity pre and post pandemic of south Asian banks.

2.1.3.2. Debt to total assets ratio

This ratio, DTAR, is also known as a leverage ratio since it indicates how many assets a firm has to service its debts (5). In other words, it indicates how much debt is covered by the company's total assets. DTAR is used to calculate the amount of leverage, or how much debt is used to acquire assets. This ratio is calculated by dividing total debt by total assets.

H6 There is significant difference in debt to assets pre and post pandemic south Asian banks.

3. Materials and methods

3.1. Study design

This is quantitative research that compares the effects of the pandemic on organizational performance in the banking industry before and after the epidemic. The model is based on earlier research conducted by Daryanto and Rizki (58). The data is collected from the official websites of South Asian banks.

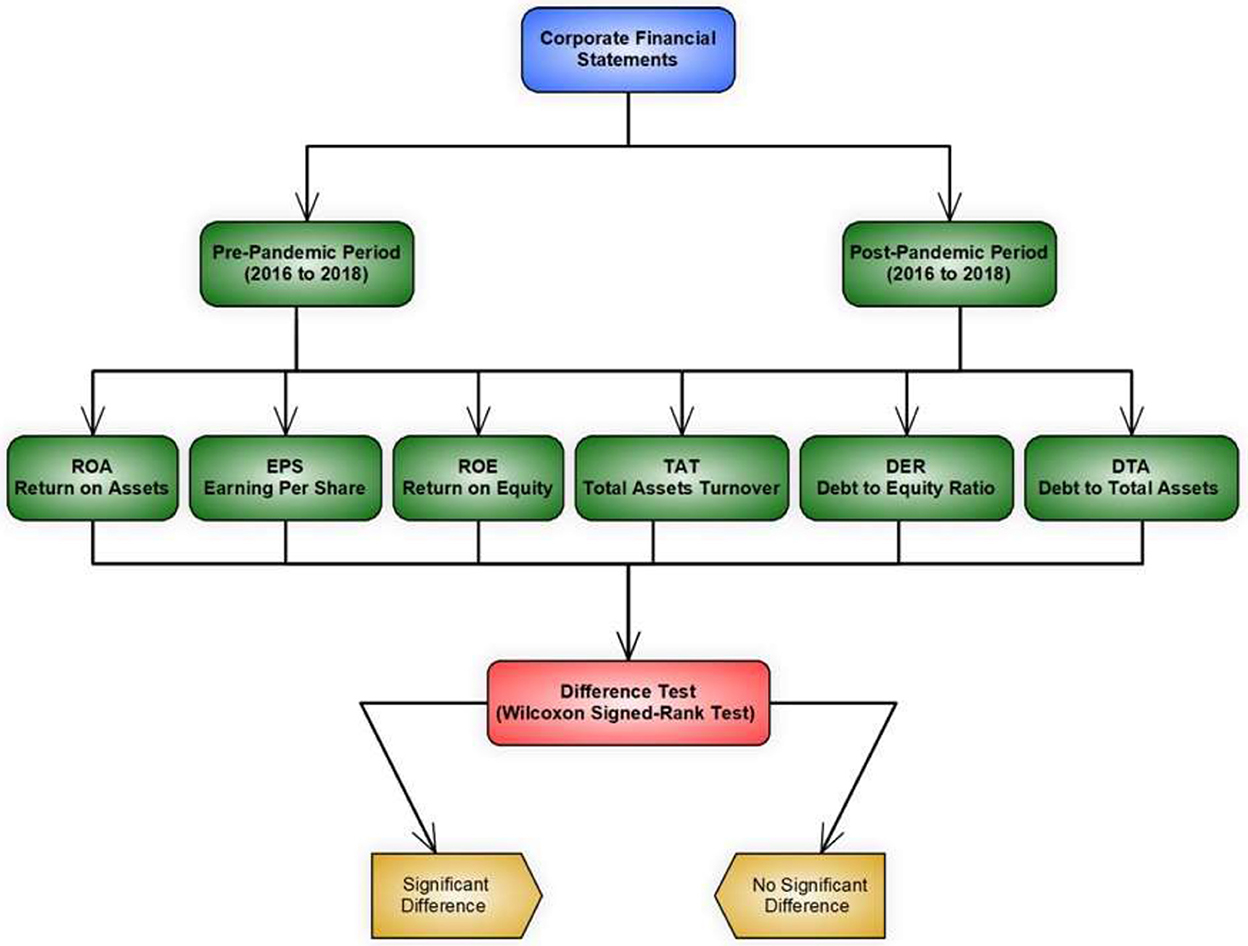

3.2. Study model

Figure 1 represent the model which we have been followed for this study. We have collected the data from official websites of the banks of South Asia. By using the collected data, we find out the ROS, EPS, ROE, TAT, DER and DAT. And also check that there is any difference between the pre and post pandemic period.

Figure 1. Study model.

3.3. Data collection and sources of this study

All of the data used in this study came from secondary sources, including the official websites of South Asian banks. To meet the study's goal, data is gathered for 6 years, with the year chosen depending on the most recent year. All 6 years were separated into two parts: the first 3 years, from 2016 to 2018, were considered pre-pandemic, and the remaining 3 years, from 2019 to 2021, were considered post-pandemic. This study examined a sample of 34 banks from the South Asian region from 2016 to 2021. Only banks with the most recent financial statements from 2021 are included in the data sample; banks without financial statements during that time period are excluded. Then, examine the financial performance of the pre-pandemic and post-pandemic periods. The scope of the study is broad because it includes the banking system of Pakistan, Sri Lanka, and Bangladesh banking systems. With the help of parent articles (58), we determine the population size N for the requirement of an article. Because without knowing the actual population of any study, we can't estimate the data size. In the given reference article, we considered the time period 2016–2020. In this article, we considered period from 2016 to 2021, increasing the time duration due to the improvement of results.

4. Results and findings

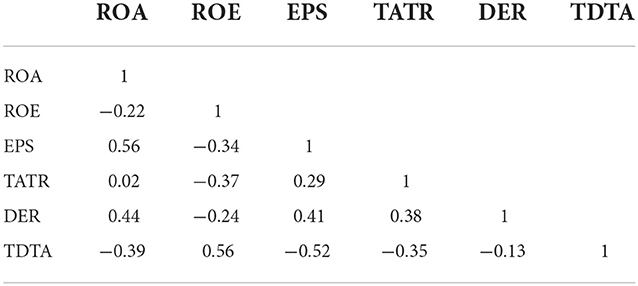

4.1. Correlation matrix

Table 1 shows the correlation between all the studied variables. The result of −1 indicates a perfectly negative linear correlation between two variables, while the result of 0 indicates no linear correlation between two variables, and 1 indicates a perfectly positive linear correlation between two variables. The overall result of the correlation matrix shows that all the variables have a strong positive relationship with each other.

Table 1. Correlation matrix of all variables.

4.2. Financial statistic

The ROA, which gauges the total profitability of the banking industry, has been declining since 2016 and will continue to do so until 2019. Figure 2 also illustrates that the ROA of banks was at its lowest during the post-pandemic period. Figure 2 also reveals that the ROA was 73 prior to the pandemic, but it has fallen while COVID is at its highest in 2019. The EPSPS share ratio is beneficial from the investor's point of view. The EPS in the post-pandemic era is much higher than in the pre-pandemic period. The EPS has now been raised to 6.96 in 2021 because of the banks' profit margin increase in 2021. ROE shows the owner's contribution to the company. The ROE has been improving over the period from 2016 to 2021. In the pandemic period, businesses face losses, and the owner's equity is more equity in their business for survival. The total asset turnover ratio is used to evaluate an organization's performance. The bank's TATR declines significantly from 2016 to 2021, as seen in Figure 2. It was 6.96 before the epidemic, but it has dropped to 6.36 since then. The DER ratio is used to assess a company's leverage; the greater the ratio, the more leveraged and riskier the corporation. The overall results show that the South Asian banks have low leverage. Another ratio used to assess the company's leverage is total debt to total assets. In the epidemic phase, it declines continuously.

Figure 2. Graphical representation of financial ratios.

Figure 2 represents the overall average of different ratios in the pre- and post-pandemic periods. On the X axis, all the ratios are presented, while on the Y axis, the results of the different ratios are presented. And the graphical representation shows that the results are better in the pre-pandemic period than in the post-pandemic period.

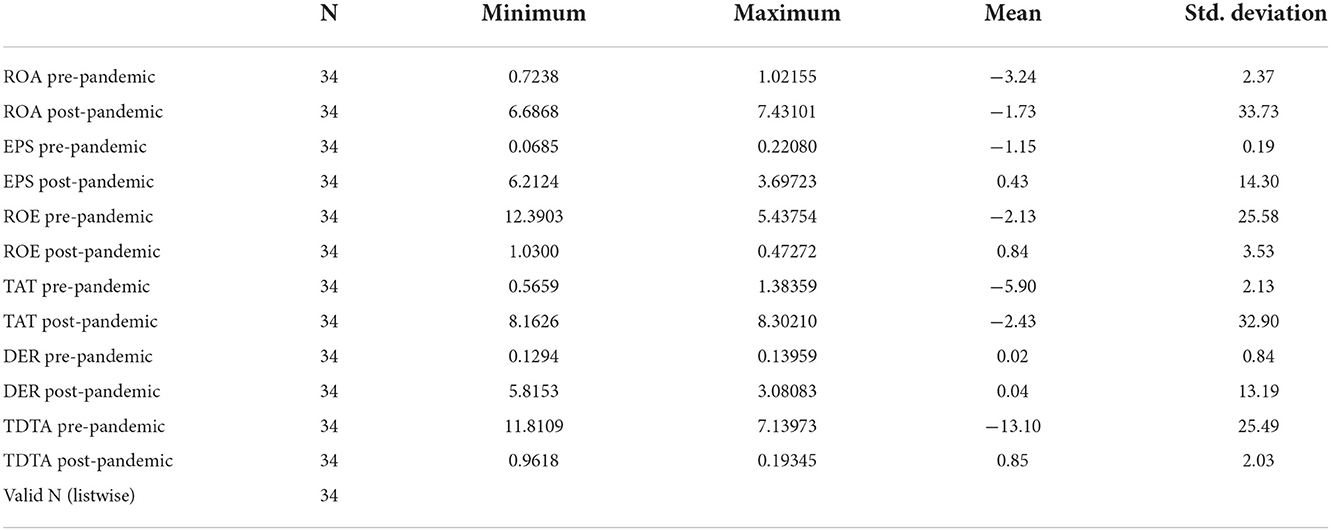

4.3. Descriptive statistic

Table 2 displays descriptive statistics for the gathered data, including (minimum value, maximum value, mean, and standard deviation) for all variables of banks listed on the Pakistan Stock Exchange from 2016 to 2021. According to Table 2, the mean value of ROA in the pre-pandemic period was −3.24 and in the post-pandemic period was −1.73. This clearly demonstrates that ROA decreases during the epidemic but increases somewhat in 2021. In the post-pandemic phase, the residual ROE, EPS, TAT, DER, and TDTA all grow. This is because, after the epidemic period is over, the firms' net income rises, which influences all ratios. Based on the findings, we may conclude that the COVID-19 pandemic condition is hazardous for the banking sector of Pakistan.

Table 2. Data descriptive statistics results for all variable pre and post pandemic period.

4.4. Wilcoxon signed-rank test

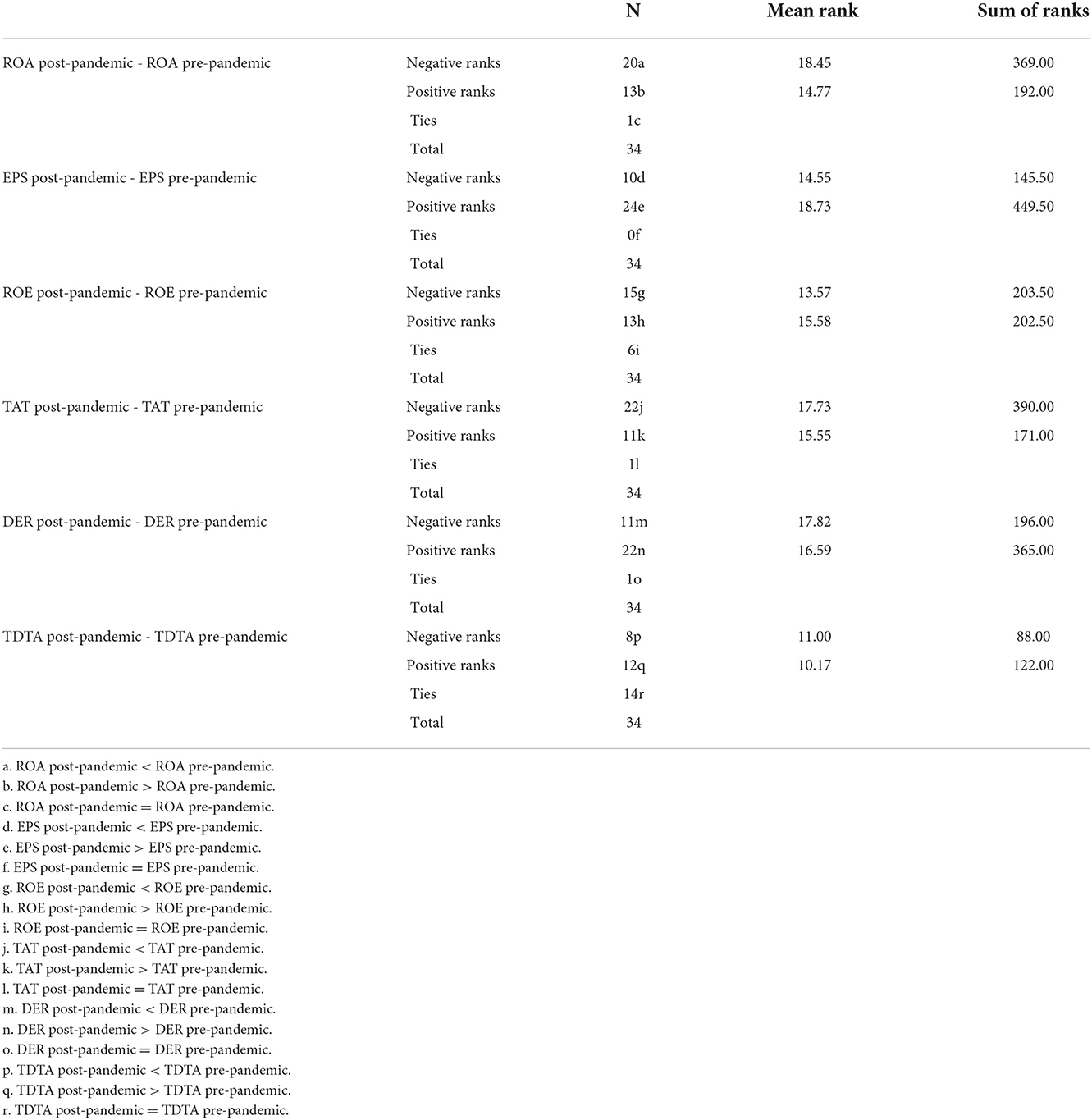

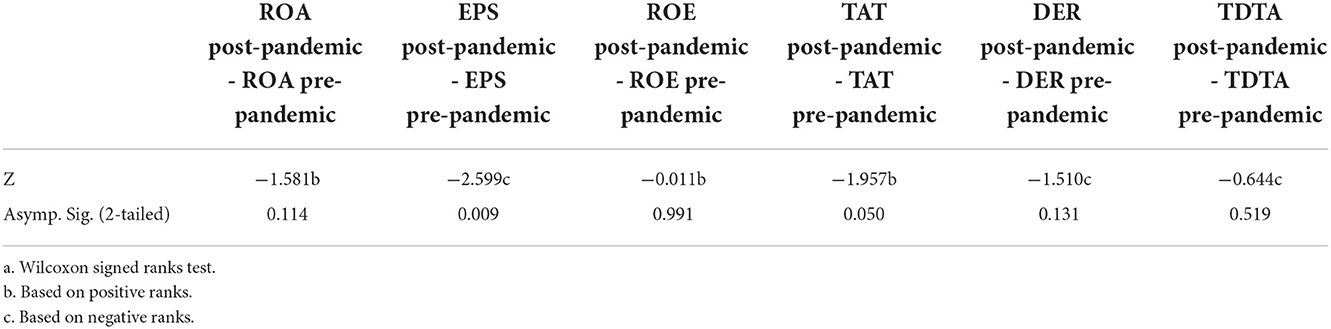

The Wilcoxon Signed Ranks Test in Table 3 reveals for the first ROA, the banks have a negative rank of 20 and a positive rank of 13, indicating that the ROA is lower and the Z score is −1.58 shown in Table 4. It indicates that the ROA differs between the before and after pandemic periods. As a result, we may deduce that ROA is falling year after year. As a result, we accept the first hypothesis, which states that there is a difference in return on assets before and after the pandemic, but this difference is not important because it has a.114 meaningful value. In the instance of EPS, it has 10 negative rankings and 24 positives rankings, with a Z score of −2.599 shown in Table 4, indicating that there is a difference in EPS between the pre and post pandemic periods. While the difference is noteworthy since it has a value of 0.001, which is smaller than the value of 0.005. The second hypothesis is likewise accepted on the basis of the first. The next metric is the ROE, which indicates that the banking sector's ROE is higher than it was before the epidemic. As a result, we can infer that the ROE has increased year after year. However, the rank test reveals that it has 15 negative rankings and 13 positive rankings, indicating that the ROE differs between the pre and post pandemic periods. As a result, the third hypothesis, that there is a significant difference in the return on equity before and after the pandemic, is accepted. The performance of banks is judged by the TAT ratio, which has a lower negative rank than a higher positive rank. The Z score for that ratio is −1.957 shown in Table 4, but it is not significant because it is more than 0.005. As a result, the notion that TAT differs between pre and post-pandemic is accepted. Similarly, the DER and TDTA are used to assess bank liquidity. Both have a greater positive rank than a negative rank, and the Z values are −1.510 and −0.644, respectively shown in Table 4, with no significant difference. As a result, the remaining two hypotheses are likewise accepted.

Table 3. Wilcoxon signed-rank test results.

Table 4. Test statistics.

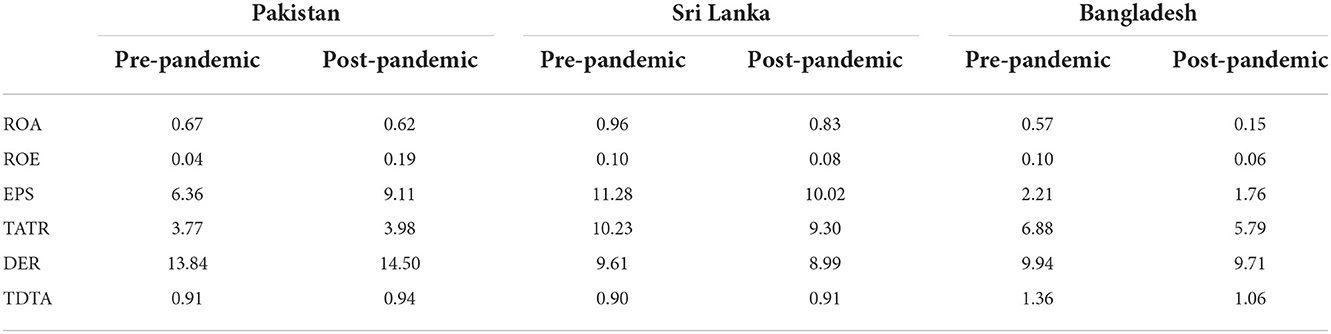

Table 5 presents the descriptive statistics of the banks listed on the South Asian markets untill December 2021. The average returns of all banks in south Asian markets were negative during the pandemic period. However, because the COVID-19 epidemic in Pakistan is less severe than in other nations, the average return increases year after year. The data also suggests that the average return in Sri Lanka is lower since the country is more influenced by COVID-19. As a result, the country's financial performance suffers more during a pandemic. This result is consistent with Goodell (60) study that the financial sector is vulnerable during a pandemic and economic recession because of the possible occurrence of excessive bad loans and massive deposit withdrawals in a short time. The overall results show that all the south Asian Bankss' performance was positively influenced by the lockdown. Finally, our empirical findings back up (60) study, which focuses on the harmful consequences of COVID-19 on the banking industry. Because of the high risk of increasing bad debts and abnormally large withdrawals that may cause corporate crises or even bankruptcy, financial firms' stocks are among the most seriously affected securities on stock markets during a pandemic.

Table 5. Year wise comparison of financial ratios.

4.5. Endogeneity

The results of Table 6 endogeneity show that the model has endogeneity because the probability of Durbin and Wu-Hausman F (1,312) is 0.7054, which is insignificant and accepts the null hypothesis that variables are exogenous. There is no evidence of endogeneity in the model.

Table 6. The result of endogeneity.

Table 7 shows the average return in terms of net profit of the south Asian banking industry. It's clearly shows that the results of the net profitability are decrease during the 2019 and 2021. But the net profitability of the banks is sufficient in 2016 to 2018. And the main reasons of decreasing the profitability during 2019 to 2021 is the COVID-19 pandemic affects. Because of the businesses are close down during pandemic. But banking fall in the services sector so, they don't stop their operations completely. They working during the period of pandemic through different modes like internet banking or through internet apps.

Table 7. Year wise average return.

5. Discussion

The goal of this study was to assess the financial performance of the banking industry before and after the epidemic. The COVID-19 has a great impact on each business, especially the south Asian banking sector. During the pandemic period, Pakistan's government is also fighting against COVID-19 through social distancing and lockdown (61). The National Bank of Pakistan continues its operations through advanced technology (internet). Mostly, banks have shifted to a mobile app, and a user can make any transaction (withdraw, transfer) by using this app. Same as that in Bangladesh, where the government declared a general holiday for 2 months from March 26 to May 30 (62). The banks had continued their work on a small scale during the pandemic situation (63). They are also using the latest technology and providing e-services to their customers. Then there is no need to attack the branches physically. This will also maintain the social distance because no one will come to the branches. Sri Lanka, another famous tourist destination in the South Asian region, is also affected by this pandemic. The economy of said country is also dependent on the services sector, and the economy is declining badly. The country removes travel restrictions in 2021, which is a positive sign of recovery of 0.1% in said year (64). In Sri Lanka, the banks are also continuing their banking operations during COVID-19 for many reasons. One of the most important reasons for continuous operation in Sri Lanka is that the banks are responsible for payment and settlement systems. Therefore, the central bank of Sri Lanka (CBSL) authorizes the banks to regulate and supervise the payment, clearing, and settlement systems. Hence, banking operations continue during the period of COVID-19 in the south Asian banking sector. These banks perform their operations through the OTS (online transaction system), and some banks have shifted to mobile apps through which a customer can get the same services as banks. In the period, those banks have decreased their margins because they are not using the internet or advancing in technology. Therefore, in 2021, banks will improve their financial performance. In South Asia, the banking sector works for the government in the collection of taxes and the disbursement of cash for government expenditures. And almost all of the businesses working around the globe also depend on the banking sector. If the banks are closed during COVID-19, then the most critical situations will happen, and every business will face them. The banks play a vital role in emerging economies; if they close their operations during the pandemic period, the economies will face the following problems: lack of short-term and long-term capital financing; increased unemployment; a falling economic growth rate; increased interest rates; and much more (65).

The COVID-19 has negative impact on the financial performance of the banking industry in South Asia. As a result, the ROA of banks' assets has decreased throughout the epidemic era. As a consequence, the first hypothesis is accepted that there is significant difference in return on assets pre and post pandemic of south. The return on assets more decrease during the period of COVID-19. This finding supports the recent research of (63, 65), who discovered that the ROA decreased during the COVID-19 period. The second theory is concerning EPS, which is accepted and confirmed by Aprilia and Oetomo (66). Based on the rank test, the third hypothesis demonstrated that there is a difference in ROE between the pre and post pandemic periods, and the result is consistent with the previous study by Esomar and Christianty (67), in which the author stated that there were significant differences in ROE before and during the COVID-19 pandemic. The alternative explanation is also acceptable, since statistical data demonstrates a difference in performance between the pre and post pandemic periods. Daryanto and Rizki (58) prior investigation yielded similar results.

Finally, the banking sector plays a very important role in the economic development and growth of a country (68). But the overall performance of the banking sector is affected by many factors. COVID-19 is considered an important factor that affects the financial performance of the banking sector in South Asia. In this situation, the banking sector improves its performance through many indicators, which include IT adoption, technological advancement, and improved customer experience. A study by Dadoukis et al. (69) confirms that high IT-adopters improve their performance as compared to low IT-adopters in the period of the pandemic. All the businesses are closed during this time, but the banks are using the latest technology to run the business smoothly. Customers can perform transactions from their homes without standing in line at the banks. During the period of the pandemic, most banks will waive their transaction charges (free bank transfers through apps). The advancement in technology is measured through different things like mobile apps, social factors, free e-transactions, etc. This study is in line with previous research (70), which states that technology advancement is very influential in employee performance, ultimately increasing the performance of South Asian banks. The results of this study will also aid policymakers in developing policies to handle such crucial situations.

6. Conclusion

The purpose of this study is to analyse the financial performance of the South Asian banking sector before and after the COVID-19 pandemic. Using overall performance measures, liquidity, solvency, profitability, and activity ratios, it is found that the company had better performance before the pandemic. But the same was disturbed during the period of the COVID-19 pandemic, resulting in a decline. Another finding that we made was that the performance before and after the pandemic had significant differences, mainly in liquidity ratios, solvency ratios, and profitability ratios. Finally, we can conclude that banks can maintain their position in the business world because they do not stop working even in the pandemic period. They offer their service through technological advancement, and in the period 2021, they improve their performance as compared to the other pandemic periods. The said study is helpful for business owners, shareholders, and governments to understand the effect of COVID-19 on financial performance, especially in the banking sector, which has greatly contributed to the development of the country. We exclusively compared the organizational performance of the South Asian banking sector before and after the COVID-19 period. We gathered data from the most recent years, from 2016 to 2021, to assess organizational effectiveness. There are numerous other factors that influence stock markets during pandemics; however, this study did not take these into account and instead focused solely on the COVID-19 pandemic. Meanwhile, this study only examined the banking sector; further research might be conducted to examine other manufacturing sectors in order to provide more generalized conclusions. Furthermore, the study can be used to assess the organization's performance in relation to other variables, such as management strategies and decisions taken during the pandemic.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

ZM, SUQ, and ML contributed to conception and design of the study. SQ organized the database. SUQ and MR performed the statistical analysis. CY, ML, and SUQ wrote the first draft of the manuscript. ZM, SUQ, SQ, and MR wrote sections of the manuscript. HX contributed to correlation matrix and interpret results. All authors contributed to the article and approved the submitted version.

Funding

This study was funded by Key Program of National Social Science Fund of China (21AZD067).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher's note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

1. Verma P, Dumka A, Bhardwaj A, Ashok A, Kestwal MC, Kumar P. A statistical analysis of impact of COVID19 on the global economy and stock index returns. SN Comput Sci. (2021) 2:1–13. doi: 10.1007/s42979-020-00410-w

2. Pappas N. COVID19: holiday intentions during a pandemic. Tour Manag. (2021) 84:104287. doi: 10.1016/j.tourman.2021.104287

3. Assous HF, Al-Najjar D. Consequences of COVID-19 on banking sector index: artificial neural network model. Int J Fin Stud. (2021) 9:67. doi: 10.3390/ijfs9040067

4. Zafar S, Aziz F. The banking sector of Pakistan: the case of its growth and impact on revenue generation 2007 to 2012. IOSR J Econ Finance. (2013) 1:46–50. doi: 10.9790/5933-0154650

5. Al Faruk AR. Comparative Analysis of sharia stock performance before and during COVID-19 pandemic in Indonesia. Perbanas J Islam Econ Bus. (2022) 2:65–74. doi: 10.56174/pjieb.v2i1.44

6. Xiazi X, Shabir M. COVID-19 pandemic impact on bank performance. Front Psychol. (2021). doi: 10.3389/fpsyg.2022.1014009

7. AlAli MS. The effect of WHO COVID-19 announcement on Asian stock markets returns: an event study analysis. J Econ Bus. (2020) 3:1051–4. doi: 10.31014/aior.1992.03.03.261

8. Kozak S. The impact of COVID-19 on bank equity and performance: the case of Central Eastern South European countries. Sustainability. (2021) 13:11036. doi: 10.3390/su131911036

9. Arellana J, Márquez L, Cantillo V. COVID-19 outbreak in Colombia: An analysis of its impacts on transport systems. J Adv Transport. (2020) 2020:1–16. doi: 10.1155/2020/8867316

10. Ghouse G, Bhatti MI, Shahid MH. Impact of COVID-19, political, and financial events on the performance of commercial banking sector. J Risk Finan Manag. (2022) 15:186. doi: 10.3390/jrfm15040186

11. Moh'd AL-Tamimi KA. The effects of COVID-19 pandemic on the economies of the Gulf Cooperation Council States due to low oil prices. Int J Fin Res. (2021) 12:279–85. doi: 10.5430/ijfr.v12n1p279

12. Qadri SU, Li M, Ma Z, Qadri S, Ye C, Usman M. Unpaid leave on COVID-19: the impact of psychological breach contract on emotional exhaustion: the mediating role of job distrust and insecurity. Front Psychol. (2022) 13:953454. doi: 10.3389/fpsyg.2022.953454

13. Anh DLT, Gan C. The impact of the COVID-19 lockdown on stock market performance: evidence from Vietnam. J Econ Stud. (2020) 48:836–51. doi: 10.1108/JES-06-2020-0312

14. Hung NT. Dynamic spill over effects between oil prices and stock markets: new evidence from pre and during COVID-19 outbreak. Aims Energy. (2020) 8:819–34. doi: 10.3934/energy.2020.5.819

15. Fund IM,. World Economic Outlook Database October 2012. World Economic Outlook Database (2012). Available online at: https://www.imf.org/en/Publications/WEO/weo-database/2012/October

16. Irfan S, Kee D. Critical success factors of TQM and its impact on increased service quality: a case from service sector of Pakistan. Middle-East J Sci Res. (2013) 15:61–74. doi: 10.5829/idosi.mejsr.2013.15.1.828

17. Erden B, Aslan OF. The impact of the COVID-19 pandemic outbreak on the sustainable development of the turkish banking sector. Front Environ Sci. (2022) 2020. doi: 10.3389/fenvs.2022.989070

18. Schor M, Protopopova A. Effect of COVID-19 on pet food bank servicing: quantifying numbers of clients serviced in the vancouver downtown Eastside, British Columbia, Canada. Front Vet Sci. (2021) 8:730390. doi: 10.3389/fvets.2021.730390

19. Khgan J. How Do Commercial Banks Work Why Do They Matter? Investopedia (2021). Available online at: https://www.investopedia.com/terms/c/commercialbank.asp

20. Arabaci H, Yücel D. Impact of COVID-19 pandemic on Turkish banking sector. Soc Sci Res J. (2020) 9:196–208.

21. Phulpoto LA, Shah AB, Shaikh FM. Global financial crises and its impact on banking sector in Pakistan. Asian Econom Soc Society. (2012) 2:142–52.

22. Chandel RS, Kanga S, Singh SK. Impact of COVID-19 on tourism sector: a case study of Rajasthan, India. AIMS Geosci. (2021) 7:224–43. doi: 10.3934/geosci.2021014

23. Burki AA, Niazi G. Impact of financial reforms on efficiency of state-owned, private and foreign banks in Pakistan. Appl Econ. (2010) 42:3147–60. doi: 10.1080/00036840802112315

24. Savitri N, Hidayati S. Financial performance analysis of companies in the primary consumer goods sector before and during COVID-19. Int J Bus Eco Strategy. (2022) 4:49–56. doi: 10.36096/ijbes.v4i1.307

25. Connelly BL, Certo ST, Ireland RD, Reutzel CR. Signaling theory: A review and assessment. J Manag. (2010) 37:39–67. doi: 10.1177/0149206310388419

27. Rababah A. Al-Haddad L, Sial MS, Chunmei Z, Cherian J. Analyzing the effects of COVID-19 pandemic on the financial performance of Chinese listed companies. J Public Affair. (2020) 20:e2440. doi: 10.1002/pa.2440

30. Sidharta I, Affandi A. The empirical study on intellectual capital approach toward financial performance on rural banking sectors in Indonesia. Int J Econ Finan Issues. (2016) 6:1247–53.

31. Mondal A, Ghosh SK. Intellectual capital and financial performance of Indian banks. J Intell Capital. (2012) 515–30. doi: 10.1108/14691931211276115

32. Bulgurcu BK. Application of TOPSIS technique for financial performance evaluation of technology firms in Istanbul stock exchange market. Procedia-Soc Behav Sci. (2012) 62:1033–40. doi: 10.1016/j.sbspro.2012.09.176

33. Farrokh M, Heydari H, Janani H. Two comparative MCDM approaches for evaluating the financial performance of Iranian basic metals companies. Iranian J Manag Stud. (2016) 9:359–82. Available online at: https://ijms.ut.ac.ir/article_56415_183c81e5cf9293cfc4a674abbe554354.pdf

34. Fenyves V, Tarnóczi T, Zsidó K. Financial performance evaluation of agricultural enterprises with DEA method. Procedia Econ Fin. (2015) 32:423–31. doi: 10.1016/S2212-5671(15)01413-6

35. Gökalp F. Comparing the financial performance of banks in Turkey by using Promethee method. Ege Stratejik Araştirmalar Dergisi. (2015) 6:63–82. doi: 10.18354/esam.90895

36. Saeed H, Shahid A, Tirmizi SMA. An empirical investigation of banking sector performance of Pakistan and Sri Lanka by using CAMELS ratio of framework. J Sustain Finan Invest. (2020) 10:247–68. doi: 10.1080/20430795.2019.1673140

37. Ganlin P, Qamruzzaman MD, Mehta AM, Naqvi FN, Karim S. Innovative finance, technological adaptation and smes sustainability: The mediating role of government support during covid-19 pandemic. Sustainability (Switzerland). (2021) 13:1–27. doi: 10.3390/su13169218

38. Martínez-Caro E, Cepeda-Carrión G, Cegarra-Navarro JG, Garcia-Perez A. The effect of information technology assimilation on firm performance in B2B scenarios. Ind Manag Data Syst. (2020) 120:2269–96. doi: 10.1108/IMDS-10-2019-0554

39. Pavitt K. Key characteristics of the large innovating firm. Bri J Manag. (1991) 2:41–50 doi: 10.1111/j.1467-8551.1991.tb00014.x

40. Alam MM, Murad MW. The impacts of economic growth, trade openness and technological progress on renewable energy use in organization for economic co-operation and development countries. Renewable Energy. (2020) 145:382–90. doi: 10.1016/j.renene.2019.06.054

41. Song Q, Wang Y, Chen Y, Benitez J, Hu J. Impact of the usage of social media in the workplace on team and employee performance. Inform Manag. (2019) 56:103160. doi: 10.1016/j.im.2019.04.003

42. Sapta IKS, Muafi M, Setini NM. The role of technology, organizational culture, and job satisfaction in improving employee performance during the covid-19 pandemic. J Asian Finan Econom Bus. (2021) 8:495–505. doi: 10.13106/jafeb.2021.vol8.no1.495

43. Wang Z, Lu J, Li M, Yang S, Wang Y, Cheng X. Edge computing and blockchain in enterprise performance and venture capital management. Comput Intell Neurosci. (2022) 2022:2914936. doi: 10.1155/2022/2914936

44. Liu L, Wang E-Z, Lee C-C. Impact of the COVID-19 pandemic on the crude oil and stock markets in the US: A time-varying analysis. Energ Res Lett. (2020) 1:1–5. doi: 10.46557/001c.13154

45. Narayan PK, Devpura N, Wang H. Japanese currency and stock market-What happened during the COVID-19 pandemic? Econom Anal Policy. (2020) 68:191–8. doi: 10.1016/j.eap.2020.09.014

46. Wang Z, Li M, Lu J, Cheng X. Business Innovation based on artificial intelligence and Blockchain technology. Inf Process Manag. (2022) 59:102759. doi: 10.1016/j.ipm.2021.102759

47. Alviana T, Megawati M. Comparative analysis of company financial performance before and during the COVID-19 pandemic on LQ45 index. Finan Manag Stud. (2021) 1:60–73.

48. Ross SA, Westerfield RW, Jordan BD. Pengantar Keuangan Perusahaan. Jakarta: Salemba Empat (2009).

49. Balasundaram N. A comparative study of financial performance of banking sector in Bangladesh-an application of CAMELS rating system. Ann Univ Bucharest Econ Admin Series. (2008).

51. Basheer ZM, Althahabi AM, Ali MH, Wafqan HM, Al Mahdi RA, Oudah Al- Muttar MY, et al. Determinants of financial performance: A case from oil and gas companies listed in the iraq stock exchange. Cuadernos de Economia. (2022) 45:33–44. doi: 10.32826/cude.v1i128.704

54. Almajali AY, Alamro SA, Al-Soub YZ. Factors affecting the financial performance of Jordanian insurance companies listed at amman stock exchange. J Manag Res. (2012) 4:266. doi: 10.5296/jmr.v4i2.1482

55. Ellis R. Asset Utilization: A Metric for Focusing Reliability Efforts. 7th ed. Marriott Houston, TX: Westside Houston (1998).

56. Jose HA, Gao H, Zheng X, Alidaee B, Wang H. A study of the relative efficiency of chinese ports: A financial ratio-based data envelopment analysis approach. J Expert Syst. (2010) 27:349–62. doi: 10.1111/j.1468-0394.2010.00552.x

57. Seema GPK, Surendra SY. Impact of MoU on financial performance of public sector enterprises in India. J Adv Manag Res. (2011) 8:263–84. doi: 10.1108/09727981111175984

58. Daryanto WM, Rizki MI. Financial performance analysis of construction company before and during COVID-19 pandemic in Indonesia. Int J Bus Econ Law. (2021) 24:99–108.

59. Amalia S, Fadjriah EN, Nugraha MN. The influence of the financial ratio to the prevention of bankruptcy in cigarette manufacturing companies sub sector. Solid State Technol. (2020) 63:4173–82.

61. Qadri S, Chen S, Qadri SU. How does COVID-19 affect demographic, administrative, and social economic domain? empirical evidence from an emerging economy. Int J Mental Health Pro. (2022). doi: 10.32604/ijmhp.2022.021689

62. Ahamed F. Macroeconomic Impact of COVID-19: a case study on Bangladesh. IOSR J Econ Fin. (2021) 12:2021. doi: 10.9790/5933-1201042429

63. Yasmin S, Alam MK, Ali FB, Banik R, Salma N. Psychological impact of COVID-19 among people from the banking sector in Bangladesh: a cross-sectional study. Int J Ment Health Addict. (2022) 20:1485–99. doi: 10.1007/s11469-020-00456-0

64. Khan MA, Naqvi HA, Hakeem MM, Din GMU, Iqbal N. Economic and financial impact of the COVID-19 pandemic in South Asia. Environ Sci Pollut Res Int. (2022) 29:15703–12. doi: 10.1007/s11356-021-16894-9

65. Xie H, Chang HL, Hafeez M, Saliba C. COVID-19 post-implications for sustainable banking sector performance: evidence from emerging Asian economies. Econom Res. (2022) 35:4801–16. doi: 10.1080/1331677X.2021.2018619

66. Aprilia NS, Oetomo HW. Comparison of financial performance before and after the acquisition of manufacturing companies. Jurnal Ilmu Dan Riset Manajemen. (2015) 4:1–19.

67. Esomar MJF, Christianty R. The impact of the Covid-19 pandemic on the financial performance of sector companies services at IDX. J Bus Manag Concept. (2021) 7:227–33.

68. Alam MS, Rabbani MR, Tausif MR, Abey J. Banks' performance and economic growth in India: A panel cointegration analysis. Economies. (2021) 9:1–13. doi: 10.3390/economies9010038

69. Dadoukis A, Fiaschetti M, Fusi G. IT adoption and bank performance during the Covid-19 pandemic. Econom Lett. (2021) 204:109904. doi: 10.1016/J.ECONLET.2021.109904

Keywords: financial performance, pre-COVID-19, post-COVID-19, COVID-19 pandemic, South Asian banking sector, banking performance

Citation: Qadri SU, Ma Z, Raza M, Li M, Qadri S, Ye C and Xie H (2023) COVID-19 and financial performance: Pre and post effect of COVID-19 on organization performance; A study based on South Asian economy. Front. Public Health 10:1055406. doi: 10.3389/fpubh.2022.1055406

Received: 27 September 2022; Accepted: 30 November 2022;

Published: 10 January 2023.

Edited by:

Giray Gozgor, Istanbul Medeniyet University, TurkeyCopyright © 2023 Qadri, Ma, Raza, Li, Qadri, Ye and Xie. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Zhiqiang Ma, mzq@ujs.edu.cn; Mingxing Li, mingxingli6@jus.edu.cn; Syed Usman Qadri, usmangillani79@yahoo.com; Mohsin Raza, write2mraza@gmail.com

†ORCID: Mohsin Raza orcid.org/0000-0002-7645-8830