The impact of digital transformation on corporate sustainability- new evidence from Chinese listed companies

Chenxi Zhang1

Chenxi Zhang1  Pengyu Chen

Pengyu Chen- 1School of Business, Gachon University, Seongnam, South Korea

- 2Department of Economics, College of Business and Economics, Dankook University, Yongin-si, South Korea

- 3School of Economics, Jiangsu University of Technology, Changzhou, China

As Industry 4.0 is seen as the core industrial stage for achieving sustainable development, more and more scholars are exploring the practical effects of Industry 4.0. This paper evaluates the impact of digital transformation on business sustainability, explores whether digital transformation breaks down perceptions, and examines the mechanisms by which it works. First, we measured the digital transformation of each firm using textual analysis. and found that the coefficient of digital transformation is 0.006 on corporate sustainability at the 1% significant level. Secondly, we found that digital transformation eases knowledge flow barriers and makes knowledge more accessible to firms. Firms with higher digital transformation attract more skilled people, which can create talent barriers. Digital transformation can exacerbate firms’ industry monopolies, while increasing the proportion of boardroom women and the inclusion of older members sends positive signals to outsiders. Finally, we find that low costs, high labor productivity, high innovation and low cost of sales are important channels for digital transformation. In addition, digital transformation increases the management costs of firms.

1 Introduction

The concept of Industry 4.0 was firstly introduced in 2011 (Ustundag and Cevikcan, 2017). Industry 4.0 is considered as a new industrial scenario that combines various high technologies through internet of things (IoT) technologies, culminating in an integrated platform that can serve both businesses and consumers, in order to achieve sustainable development (Frank et al., 2019). This new industrial scenario is disrupting traditional corporate business models as well as industry structures (Dregger et al., 2016). However, the transformation process of companies turning into the Industry 4.0 Connected Smart Enterprise from the industrial stage can not succeed easily, and digital transformation is considered a intergrade (Dalenogare et al., 2018). As a new industrial reform, digital transformation is seen as an important stage in achieving corporate sustainability (Kamble et al., 2018; Feroz et al., 2021). According to the Global Environmental Performance Report published by Yale University in 2020 (Chen, 2022), China ranked 120th in terms of environmental performance in the world (out of 180 countries) with a score of 37.3. As one main emitter of pollution, China attaches great importance to the environmental management ability of Chinese enterprises. Therefore, it would be highly valuable to further explore the relationship between digital transformation and corporate sustainability.

The existing literature on digital transformation and sustainability mainly focuses on the literature analysis methods (Feroz et al., 2021), macro-level sustainability (Bieser and Hilty, 2018), industry-level sustainability (Hrustek, 2020) but rarely pays attention to the firm-level sustainability. For example, taking Chinese listed manufacturing firms in 2010–2020 as the objects, Guo and Xu (2021) found that digital transformation is positively related to process-based business performance and non-linearly related to profit-oriented financial performance. Wen et al. (2022) found that digitalization could help companies to innovate and achieve sustainable growth based on data from Chinese listed manufacturing companies. This paper fills a gap in the existing literature by exploring the relationship between digital transformation and corporate sustainability through quantitative analysis. Furthermore, the application of digital technologies such as big data, robotics, the IoT, blockchain, and smart technologies can lead to disruptive changes in competitive momentum, industry structures, innovation approaches, and board structures (Porter and Heppelmann, 2014; Appio et al., 2021). For example, Guo et al. (2022) explored that digital transformation can alleviate industry monopolies based on market competitiveness and firm scale. A missing part in estimating how digitalization can disrupt perceptions is studying innovation approaches and board structures. Digital transformation may affect different stages of the innovation process in a complex and causally ambiguous way (Barrett et al., 2015), providing greater scalability for corporate innovation (Iansiti and Lakhani, 2020). In addition, digital transformation could lead to disruptive changes in the board (Wolfe, 2020), making promotion and vetting mechanisms more transparent and more inclusive to different ages (Noor et al., 2016). Existing literature rarely examines the impact of digital transformation on innovation stages and board structures, so it is of meaning to explore how digital transformation changes innovation approaches and board structures.

Based on data from listed Chinese manufacturing companies in 2010–2019, a double-effects fixed model is used to explore whether digital transformation contributes to the sustainable development. Second, as an unknown corporate strategy, digital transformation varies across different types of firms, and we classify firms into several types in terms of innovation and corporate governance, such as the speed of knowledge flow, technical staff, competitiveness, the proportion of female directors and the average age of board members. Thirdly, considering that digital transformation is disrupting traditional business models, the potential pathways through which digital transformation affects the sustainability were explored in terms of changes in production and distribution patterns, innovation capabilities and firm labor productivity, respectively. Through this study, the following questions are to be answered: 1) Does digital transformation contribute to corporate sustainability? 2) If so, which types of companies are more sensitive to digital transformation? 3) And through which pathways does digital transformation affect corporate sustainability?

The main contributions of this study are as follows: 1) Unlike existing studies that separately discuss the impact of digital transformation on firm performance, innovation or organizational structure. This paper comprehensively measures corporate sustainability from the perspectives of environmental management, environmental control, human resources disclosure, product and consumer disclosure and community involvement. It fills the gap in existing research on the impact of digital transformation on corporate environmental governance. 2) It was found that the attitudes of different types of enterprises towards digital transformation strategies are inconsistent. Namely, digital transformation can alleviate knowledge and skill barriers between firms and mitigate the gap between monopolistic and non-monopolistic firms. In addition, digital transformation is more friendly to women and older directors in the board. This provides strong evidence for the adoption of digital transformation by firms under Industry 4.0 and reduces concerns about the uncertainty of digital transformation in developing countries such as China. 3) As mentioned earlier, digital transformation is disrupting traditional business models. Due to the availability and validity of data, it is difficult to keep track of changes in the production and sales patterns. Therefore, both models were measured in terms of cost of production and cost of sales, based on the fact that changes in production and sales models are ultimately reflected in costs (Hobbs, 2020). Moreover, the potential pathways of the impact of digital transformation on corporate sustainability were explored, offering new perspectives in order for business managers to achieve both corporate environmental and economic performance under the Industry 4.0 process.

The rest of the paper is organized as follows. Section 2 provides the theoretical analysis, Section 3 provides the research methodology and data, while Section 4 provides the results and discussion. Section 5 presents the conclusions and policy implications.

2 Theoretical analysis

2.1 Sustainability and digital transformation measurement

The concept of sustainable development originates from the sustainable forest management (Grober, 2007), which aims to manage forests for the purpose of sustainable yield. Over the years, the concept of sustainable development has evolved to focus more on ecological, economic, political, and cultural objectives (James, 2014). The existing literature focuses on measuring sustainable development at the macro level, such as at the national level (Vachon and Mao, 2008), the provincial level (Yang and Ding, 2018), and the municipal level (Lam and Yap., 2019). Studies on corporate sustainability mainly use ESG ratings as a proxy variable (Jia and Li, 2020) or divide corporate sustainability activities into sub-themes (Gray et al., 1995; Katmon et al., 2019). For example, Branco and Rodrigues (2008) categorized corporate sustainability activities into 23 items and divided them into several categories such as environmental, human resources, products, customers, and community involvement. Considering that ESG ratings in China are new and imperfectly developed, this paper refers to the sustainability evaluation system proposed by Zaid et al. (2020), combined with corporate disclosure in China, categorizes it into categories including environmental management, environmental regulation, environmental governance, human resources, consumer and community involvement.

Digital transformation is a complex process and one variable is difficult to proxy for it (Matt et al., 2015). Some scholars have analyzed only single technology, for example, robotics, the Internet of Things (IoT), blockchain, and big data (Ballestar et al., 2021; Chin et al., 2021). For example, Chin et al. (2021) explored the impact of blockchain on innovation. Other scholars decomposed digitalization into multiple technologies (Ballestar et al., 2021) or used the proportion of R&D investment and innovation output as a proxy variable for digital transformation (Jafari-Sadeghi et al., 2021). This paper uses textual analysis to measure digital transformation for firms disclose more information in the form of text.

2.2 Digital transformation and corporate sustainability

Digital transformation is seen as a key way to achieve sustainable development (Andriushchenko et al., 2020). Digital technology achieves sustainable development by reducing costs, improving management efficiency and improving labor productivity. Existing research on digital transformation has focused on employment, labor (Ballestar et al., 2021), productivity (Guo et al., 2022), and innovation (Abdalla and Nakagawa, 2021), while has rarely explored corporate sustainability. In a recent study, Jiao and Sun (2021) used urban data and found that the digital economy can improve economic development and employment to achieve sustainable urban development. Zuo et al. (2021) found that digital transformation had a significant increase in the sustainable efficiency of technology investment in the banking sector. It is worth noting that all these studies focus on the macro level, so it is meaningful to explore the impact of digital transformation on sustainability at the firm level to fill the gaps in existing literature.

2.3 Digital transformation disrupts perceptions

Digital transformation is disrupting perceptions (Rasiwala and Kohli, 2021). Digital transformation may disrupt existing organisational rules and structures (Philip and Gavrilova Aguilar., 2022), changing traditional competitive patterns and business models (Nadkarni and Prügl, 2021; Vaska et al., 2021; Chen and Hao, 2022). Some studies have found that digital transformation can strengthen the market position of monopolies (Soto Setzke et al., 2021) and weaken the differences brought about by firm scale (Hu, 2022). This paper focuses more on innovation structures and changes in the organizational structure of firms, such as knowledge flows, technical staff, and board structures. Based on organizational capability theory, strategic organizational activities require external environmental resources and the ability to deal with the external environment. Digital transformation can accelerate the flow of information, knowledge (Hao and Zhang, 2021). On one hand, senior digital technologies can convert data into digital resources in symbolic formats for communication; on the other hand, digital technologies can reduce the cost of storing knowledge (Gomber et al., 2018; Chen, 2022). Technical staff are one of the key factors influencing innovation in firms, which is rarely considered in existing researches on digital transformation. The digital construction of a company brings more than just efficiency, it also requires a high level of technical skills among employees (Trenerry et al., 2021). Does this give rise to a talent monopoly in companies? It is worth thinking about.

Board diversity is one of the most important factors influencing corporate sustainability (Zaid et al., 2020), and in the same way, digital transformation is changing the organisational structure and board diversity of firms (Gfrerer et al., 2021). On one hand, emerging technologies promote a culture of gender equality, and digital technologies can increase ‘information centralisation’ and public access to information (Antonio and Tuffley, 2014). On the other hand, digital technologies can exacerbate gender dichotomies (Dragiewicz et al., 2018) and widen perceptions between men and women, such as health issues and risk awareness (Kohlrausch and Weber, 2021). Age diversity is also an important part of board diversity. Some studies suggest that younger directors are more sensitive to emerging technologies and can respond positively to changes in the external environment (Hsu et al., 2019). However, it is worth noting that digital transformation entails unpredictable risks (Verhoef et al., 2021), which can be mitigated by older directors’ relatively rich managerial experience and resource relationships net (Chen, 2011). Gender and age equality are essential links, and it is worth thinking about how digital transformation, as an important means of achieving sustainable development, can affect gender and age equality. Although available data does not allow us to capture the age and gender of a company’s employees, changes in board structure can influence overall corporate decision-making results and send different signals to the society (Certo, 2003; Mallin and Michelon, 2011). By looking at the impact of digital transformation on board gender and age members, this paper explores whether it promotes gender and age equalisation, which is relevant for achieving gender equality and addressing aging issues.

3 Data and model setting

3.1 Data

This paper uses Chinese A-share listed manufacturing companies from 2009 to 2019 as a sample, using corporate financial data from the China Securities Market and Accounting Research Database (CSMAR) and the WinGo Text Analytics Database (wingodata.com). The sample study year of this paper starts from 2009, as key data are disclosed from 2009 onwards. Considering that ST&ST* firms are often in a state of poor operating income, these extreme values can affect the regression results. Therefore, we present these enterprises. In addition, to make up for some missing data, we supplemented them with the wind database and manually reviewed annual reports. We ended up with 16,159 firm-year observations.

3.1.1 Dependent variables

We refer to existing studies on corporate sustainability, some of which use ESG indexes to measure corporate sustainability (Drempetic et al., 2020; Jia and Li, 2020), while others construct sustainability evaluation systems through disclosure information of companies (Madaleno and Vieira, 2020; Zaid et al., 2020). As the ESG index of Chinese listed manufacturing companies is seriously missing, this paper adopts the approach of Zaid et al. (2020) and constructs a new corporate sustainability evaluation system by combining the information disclosed by Chinese listed companies (Appendix Table A1). In this study, we use a dichotomous approach to score corporate sustainability. Then, according to Zaid et al. (2020), the sustainability index for each firm is calculated as follows:

Where

3.1.2 Independent variables

As it is difficult to measure the digital transformation of enterprises through quantitative analysis, this paper uses textual analysis to measure the digital transformation (Guo et al., 2022; Zhai et al., 2022). Unlike Zhai et al. (2022), who examined only five keywords related to digital transformation (digitalization, artificial intelligence, big data, Internet of Things, cloud computing). This paper constructs nine keywords to describe the digital transformation, namely, big data, informatization, intelligence, robotics, Internet of Things, blockchain, automation, digitalization, cloud computing. We count the number of occurrences of these nine keywords and then, the logarithm of the number of keywords +1 to measure the digital transformation (Zhai et al., 2022).

3.1.3 Mediation variables

We analyze the mechanism of the corporate sustainability in terms of three aspects: costs, labor productivity, and innovation. In this paper, the ratio of production cost to total assets (CoA) is used to measure the change of firm selling expense (Khalifaturofi’ah, 2018). We measure labor productivity in terms of a firm’s value added per unit of labor (VAL) (Tang, 2017). This data is taken from the CSMAR database on the topic of enterprise EVA (economic value added), which is equal to operating profit - income tax expense + [interest expense (non-financial institutions) + asset impairment losses + R&D expenses] * (1 - corporate income tax rate) + increase in deferred income tax liabilities - increase in deferred income tax assets. And use the logarithm of the R&D investment (RD) to measure a firm innovation (Santacreu and Zhu, 2018).

3.1.4 Control variables

With reference to previous empirical studies on firms (Liu et al., 2020), the following control variables are introduced in this paper. These variables include ratio of net fixed assets to total assets (Fix), return on assets (ROA), logarithm of total employees (Size), logarithm of firm age (Age) and ratio of total liabilities to total assets (Lev).

3.2 Model setting

To test the impact of digital transformation on the corporate sustainability, the baseline model is constructed as follows:

Where

4 Empirical results and analysis

4.1 Frequency distribution and descriptive statistics

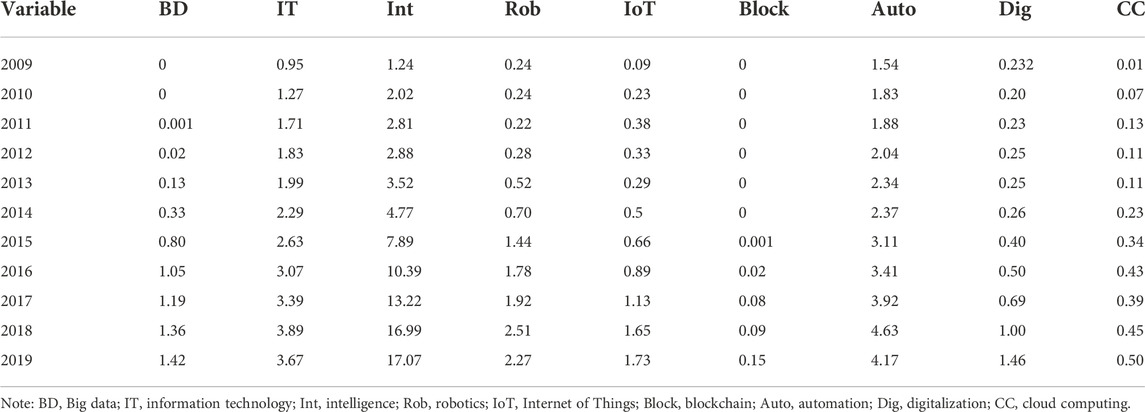

Table 1 is the distribution of the mean values by keyword over the years. It can show that the digital conversion is gradually deepening, and it is worth noting that the frequency of each keyword has increased substantially since 2012. One possible explanation is that since 2012 the Chinese government has issued a smart city pilot policy, referring to the use of various information technologies to improve resource use efficiency (Fan et al., 2021).

TABLE 1. The distribution of the mean values by keyword.

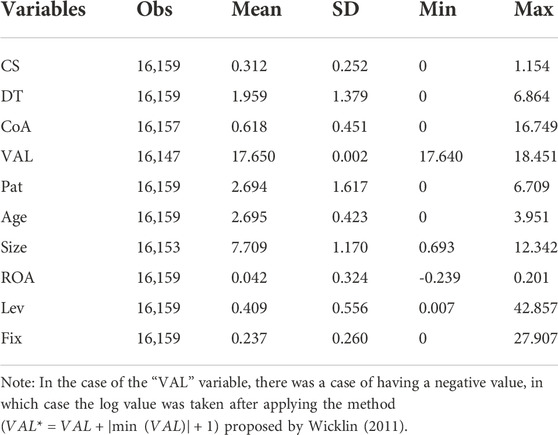

Table 2 provides descriptive statistical analyses for all variables, which present the mean, standard deviation, and minimum and maximum values for the variables. In the sample data, the mean, minimum and maximum values for corporate sustainability are 0.312, 0, and 1.154, indicating a large variation between corporate sustainability. The mean, minimum and maximum values for digital conversion are 1.959, 0, and 6.864, indicating that most firms are at a low digital stage. The mean, minimum and maximum values for the other variables show that there is a large variation between firms. In addition, we used the variance inflation factor (VIF) to test multicollinearity between the variables. The test results show that the VIF values for all variables are less than 10, with an average VIF value of 1.22, indicating that the impact of multicollinearity is negligible on the interpretation of the regression results.

TABLE 2. Descriptive statistics.

4.2 Analysis of regression results

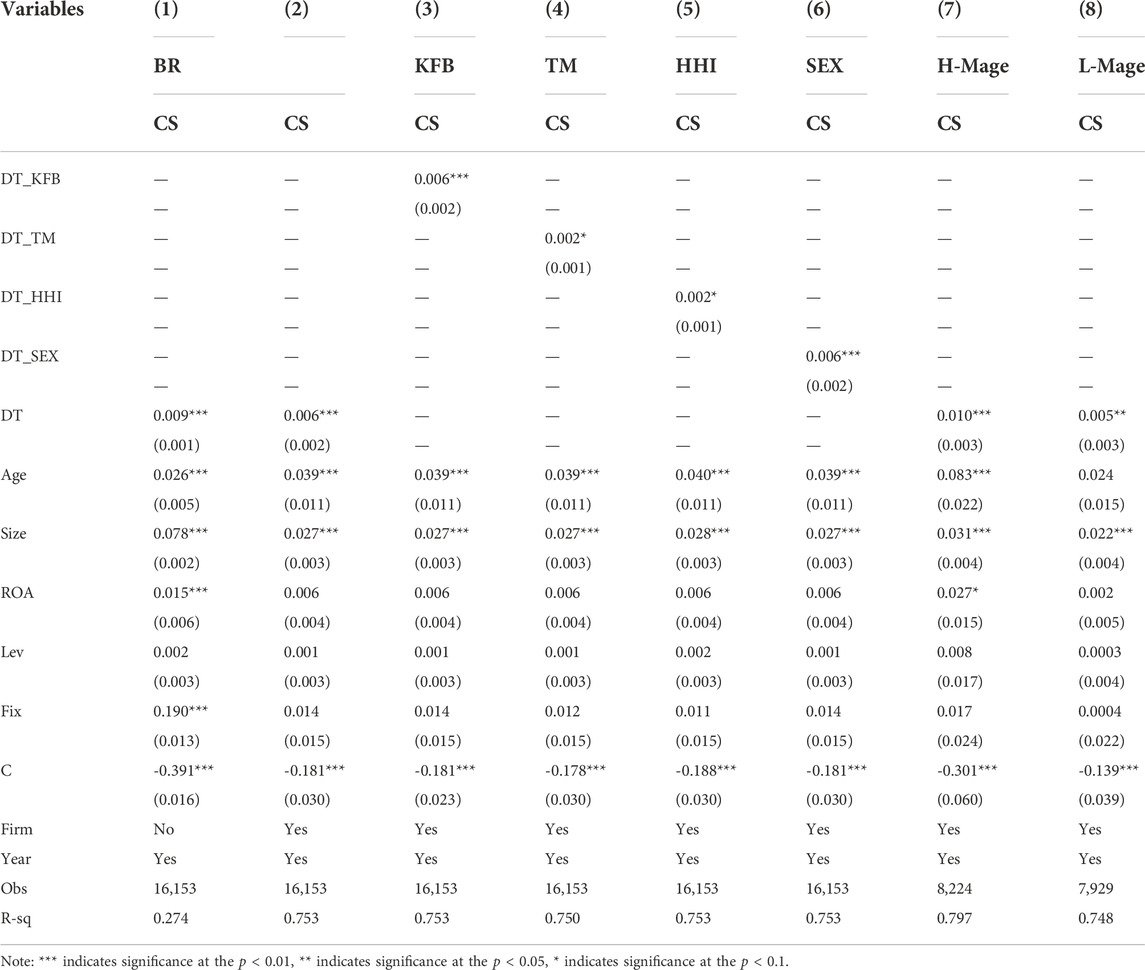

Table 3, column 1) and 2) provide the regression results between digital transformation and corporate sustainability without controlling individual effects and with controlling individual effects, respectively. Digital transformation has effects on firms, which may reinforce advantages or moderate unbalances based on their firm characteristics. We set up several dummy variables to test whether digital transformation mitigates knowledge flow barriers, technician outflow, industry monopolies, boardroom female disadvantage, and boardroom advanced age. Column 3) is a dummy variable for knowledge flow barriers, namely, KFB = 1 if the number of patent citations is greater than the median, otherwise, KFB = 0. The greater the number of patent citations, the lower the barriers to knowledge flow between firms. Column 4) is a dummy variable for technician flow. TM = 1 means that technicians are flowing in, TM = 0 means that technicians are flowing out. Column 5) is a dummy variable for industry competitiveness. We calculated the industry-level Herfindahl-Hirschman index (HHI) by operating income. HHI = 1, if this is greater than the median, which indicates that the firm is in a monopoly position. Structural changes in the board can affect strategic decisions throughout the firm (Sidhu et al., 2021). Column 6) is a dummy variable for the proportion of boardroom women. SEX = 1 when the proportion of boardroom women is greater than the median, otherwise, SEX = 0, where the proportion of boardroom women is [0, 66.67]. Column 7) and 8) represent dummy variables for the boardroom mean age. Mage = 1 if the mean age is greater than the median, otherwise, Mage = 0.

TABLE 3. Regression results.

The impact of digital transformation on corporate sustainability is consistent whether individual effects are controlled or not. Taking the results in column 2) as an example, the coefficient of digital transformation is 0.006 on corporate sustainability at the 1% significant level. This complements the findings of Sheina et al. (2019) who found that smart city building can significantly improve urban sustainability. We have extended the study to the firm level to enrich the theoretical foundation.

The results in column 3) show that the coefficient of the cross-term between digital transformation and KFB is 0.006 at the 1% significant level, which means that one standard error (1.379) increase in DT improves CS of firms with high patent citations by 0.827% (

The results in column 4) show that the coefficient of the cross-term between digital transformation and TM is 0.002 at the 10% significant level, which means that one standard error increase in DT improves CS of firms with talent inflow by 0.276% than that of firms with talent outflow. In other words, digital transformation may create a talent flow barrier, and the higher the digital transformation of a company, the more it attracts talent inflows. One possible explanation is that technical talent needs a better working environment (Perry, 2001), and the changes brought about by digital transformation meet this requirement (Okrepilov et al., 2019). This is contrary to the findings of Ballestar et al. (2021), who found that digital transformation had a significant negative impact on employment. In contrast, this paper finds that digital transformation can attract an influx of skilled talent, bridging the gap in existing research.

The results in column 5) show that the coefficient of the cross-term between digital transformation and HHI is 0.002 at the 10% significant level, namely, one standard error increase in DT improves CS of firms with high HHI by 0.276% than that of firms with low HHI. This means that firms with high HHI I have a unique market advantage, and that digital transformation further strengthens this monopoly. This is consistent with the findings of Guo et al. (2022), who found that digital transformation exacerbates the monopoly position of firms.

The results in column 6) show that the coefficient of the cross-term between digital transformation and SEX is 0.006 at the 1% significant level, namely, one standard error increase in DT improves CS of firms with more boardroom female by 0.827% than that of firms with low boardroom female. This implies that firms with high digital transformation can attract more professional women to their boards. On the one hand, digital transformation requires flexible thinking (Verhoef et al., 2021) and female directors can moderate communication within, between organizations and between organizations and individuals (Pucheta-Martínez et al., 2019). On the other hand, digital transformation can make promotion and performance appraisal mechanisms more transparent and standardized, potentially reducing women’s disadvantages (Chen et al., 2021). This may send positive signals to society, encouraging more women to join (Terjesen et al., 2016) and thus improve the corporate image (Reguera-Alvarado et al., 2017). This is in line with the findings of Chen and Hao (2022), who found that digital transformation can significantly boost women’s career development. This refutes role congruity theory of prejudice toward female leaders (Eagly and Karau, 2002), where women are less likely to be leaders and less likely to succeed in leadership positions. Instead, this paper argues that digital transformation can mitigate workplace gender discrimination and that an increase in boardroom women will promote corporate sustainability.

The results in columns 7) and 8) show that the coefficient of the digital transformation is 0.010 for firms with high boardroom age and 0.005 for firms with high boardroom age at the 1% and 5% significant level, namely, the digital transformation can accommodate more older board members. This refutes the management signaling hypothesis (Arioglu, 2021), where younger directors, driven by reputational concerns, want to demonstrate their value to the market and are thus more active and adventurous. One possible explanation is that older directors use their connections to have easier access to key resources (e.g., IT or raw materials) that help firms to digitize quickly (Miller and Triana, 2009). Or it could be that younger directors increase board risk (Berger et al., 2014), while older directors are more mature and stable (Ali et al., 2014), which could hedge some of the risks that may be involved in the digital transformation of a firm. This finding is very significant in that the changing boardroom age under digital transformation may send a positive signal to society to attract more skilled older employees to join and thus alleviate the employment difficulties associated with ageing.

4.3 Analysis of mechanisms

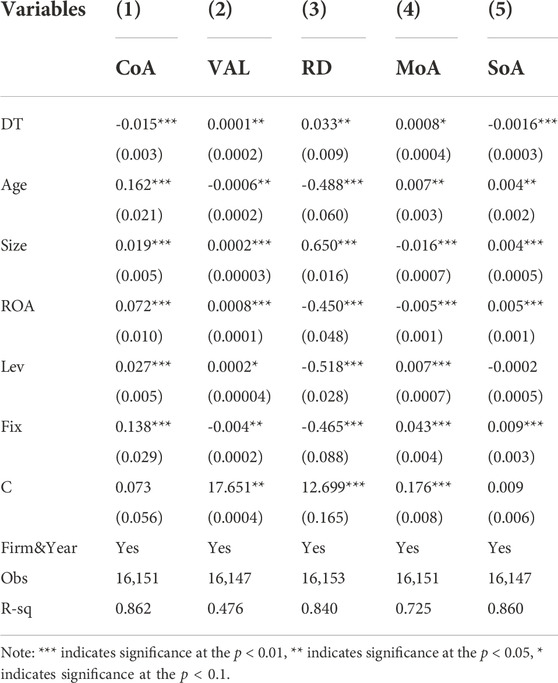

Digital technologies have a transformative or disruptive impact on companies (Boulton, 2020). Integrating different processes and resources to improve quality and efficiency through IoT, cloud services, big data and analytics (Frank et al., 2019). Based on the characteristics of digital transformation, we explain the mechanisms of its effects through the perspectives of cost (Zeng and Lei, 2021), labor productivity (Ballestar et al., 2021), and R&D investment (Guo et al., 2022). Namely, lower costs, higher labor productivity, and more innovative outputs can contribute to corporate sustainable growth. Matt et al. (2015) and Kraus et al. (2021) mention that digital transformation may affect firms’ sales patterns and management expense, however, the existing literature has not verified this, so we test these two paths of action. We use the ratio of management expense to total assets (MoA) measures the change in a firm’s management expense (Setyawati, 2017), such as technology transfer fees, software, hardware, and training cost. The ratio of selling expenses in total assets (SoA) measures the change in a firm’s selling expenses (Jiraporn and Chintrakarn, 2013) in Table 4.

TABLE 4. Analysis of mechanisms.

The regression results in columns 1), 2) and 3) find that digital transformation can reduce production costs and increase labor productivity and innovation output. This is consistent with the findings of Zeng and Lei (2021), Wen et al. (2022). Digital transformation can reduce unnecessary costs in corporate management and optimize internal resource mobilization. Secondly, digital transformation implies that firms use more and more intelligent technologies to improve work efficiency. Finally, digital transformation can help companies to access external R&D information more easily and attract technical talent.

The regression results in columns 4) and 5) find that digital transformation can increase overheads and reduce selling expenses. This validates Setyawati (2017) conjecture that high management costs may hinder the digital transformation of firms and Mattila et al. (2021) opinion that digital transformation would change the sales model to reduce the costs under the traditional sales model. Firstly, digital transformation is seen as the process of transforming a firm from its previous industrial phase to a connected and intelligent industry 4.0 firm, which can be affected by high software costs, hardware costs, and maintenance costs. Secondly, digital transformation involves the creation of special channels among companies, suppliers, and consumers, such as the Internet of Things and blockchain, which can significantly reduce the selling cost, all of which can contribute to corporate sustainability (Wen et al., 2022).

4.4 Selection bias and endogeneity issues

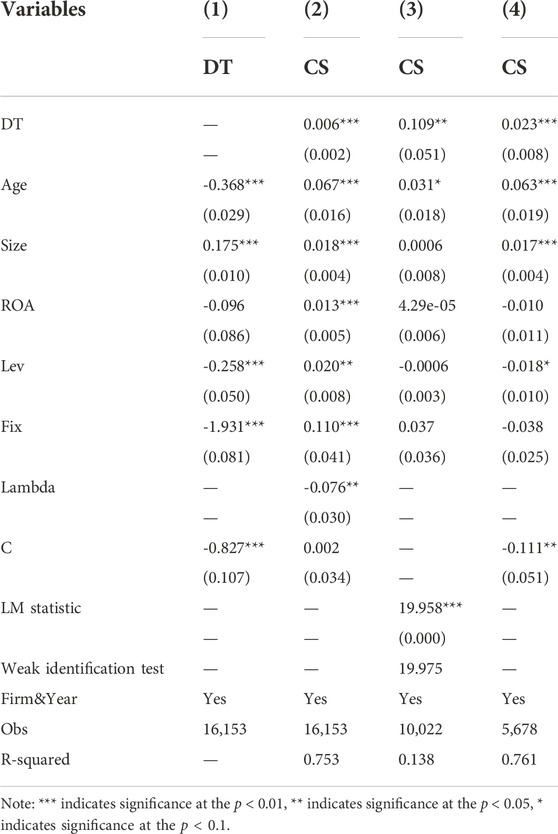

In general, a firm’s choice of geographical location is not random and many factors can influence the choice of firm location, which leads to the problem of selection bias (Cader and Leatherman, 2011). In this paper, we choose the Heckman two-stage model (Heckman and Vytlacil, 1998) to address the endogeneity issues. Second, there is little literature exploring the endogeneity of digital transformation and to mitigate potential endogeneity, we use an instrumental variables approach. We use the number of Internet users in each province to indicate the technological environment in which a firm exists. This data from the statistical yearbooks of each province. Finally, considering the possibility of reverse causality, we used the benchmark natural experiment quasi natural experiment of Broadband China, Broadband China was promulgated in 2014 to promote the digitalization of enterprises and cities through Internet infrastructure development. The Broadband China strategy was promulgated for pilot cities in 2014, 2015 and 2016 respectively, and we use this strategy as a natural experimental group (Zhao et al., 2022) in Table 5.

TABLE 5. Selection bias and endogeneity issues.

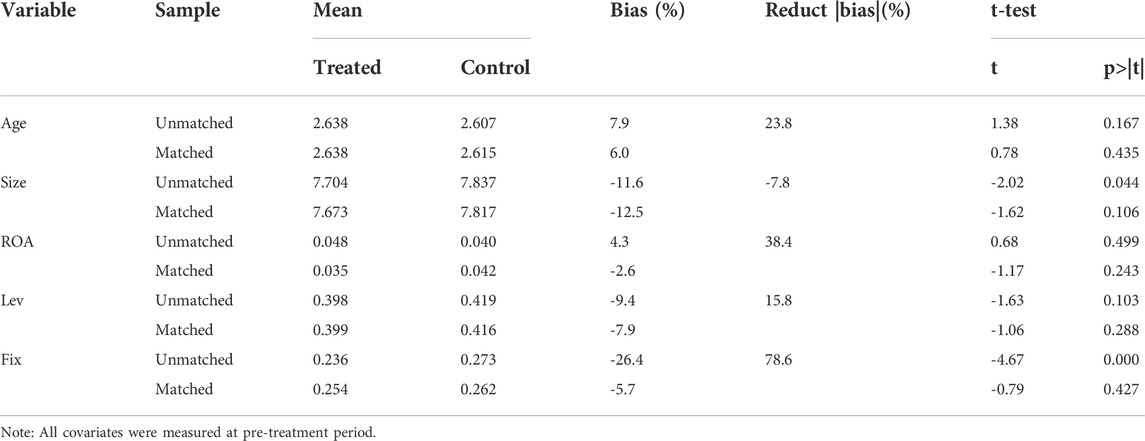

Zhang et al. (2020) mentioned that PSM(Propensity Score Matching) and DID (Differences-in-Differences) methods handle the reverse causal relationship. Zhang et al. (2020) showed that the PSM approach (propensity score matching) can match treatment and control groups by pre-policy city characteristics, handling the reverse causal relationship. We matched two sub-groups using nearest neighbor matching using pre-policy corporate characteristics. This was eventually reduced from 16,159 firm-year observations in the original sample to 5,678 firm-year observations. Appendix Table A2 shows a significant reduction in the standard deviation between the treatment and control groups after matching. This implies that selection bias was eliminated through the PSM. According to Appendix Figure A1, after matching, the PSM probability densities of the experimental and control groups were close, and the matching effect in this paper was good.

Columns 1) and 2) are the regression results of the Heckman two-stage model. The Lambda coefficient in column 2) is statistically significant, which indicates the presence of selection bias. The regression results for DT in column 2) are consistent with the previous regression results. The LM statistics used to test whether the selected IV and endogenous variables are correlated in the lower stratum of column 3) are all significant at the 1% level, indicating that the under-identification hypothesis is rejected. In addition, the weak identification test indicates that the weak instrumentality problem can be eliminated. The above statistics indicate that our choice of instrumental variables is valid. The regression results show that digital transformation can contribute to corporate sustainability. This means that the above regression results remain valid after the endogeneity problem has been overcome. In addition, in the Appendix Table A1, A2, we provide the results of the PSM approach test. addressing reverse causality, we found that broadband China can contribute to corporate sustainable development using the PSM-DID approach in column (4). This is consistent with our results.

4.5 Robustness checks

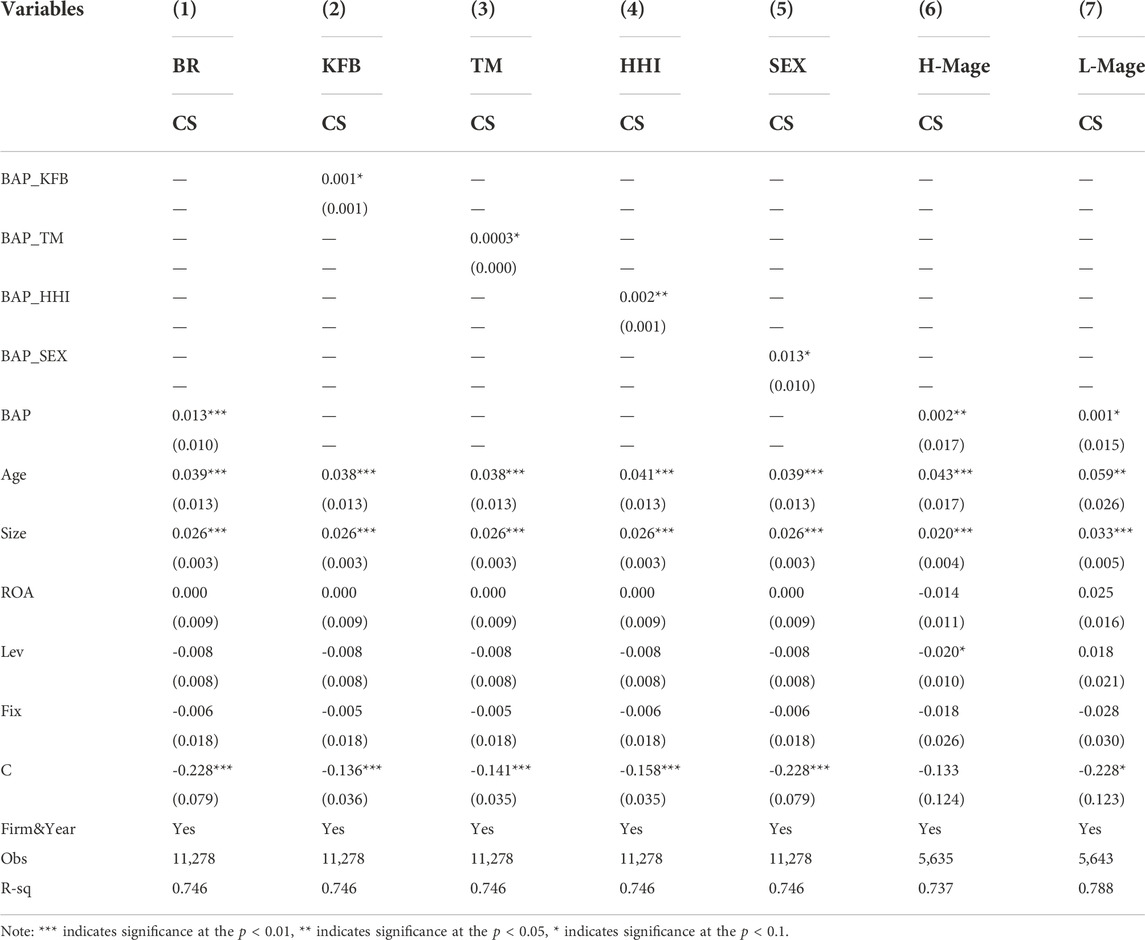

To test the robustness of the results, we used the logarithm of the internet broadband access port (BAP) as a proxy variable for digital transformation (Lee et al., 2022). The results in Table 6 show consistency with the previous results. Therefore, it can be confirmed that our test results are robust.

TABLE 6. Robustness checks.

5 Conclusion and policy implications

This paper explores the relationship between digital transformation and corporate sustainability based on listed Chinese manufacturing companies in 2010–2019. The corporate sustainability were measured from the perspectives of environmental management, environmental control, human resources disclosure, product and consumer disclosure, and community involvement. Moreover, the firm digital transformation was measured by using textual analysis. Firstly, it was found that digital transformation contributes to corporate sustainability. Secondly, based on the fact that digital transformation is disrupting traditional organizational structures and business models, it was found that digital transformation can mitigate the disadvantages of knowledge flow barriers, technician staff exodus, industry monopolies, female board disadvantages and advanced board directors’ aging issues, providing new impetus for corporate sustainability. Finally, the mechanisms of digital transformation were explored in terms of production cost, labor productivity, innovation, and cost of management and sales. It was found that low production costs, high labor productivity, high innovation and low cost of sales are important channels between digital transformation and corporate sustainability.

This paper provides an empirical basis and unique theoretical insights to promote Industry 4.0 construction and corporate sustainable development in emerging developing countries. Based on the findings, the following recommendations are proposed. For governments policy makers: Governments shall increase the construction of digital technology infrastructure such as the Internet, blockchain and big data to accelerate the Industry 4.0 process. Secondly, the government shall recognize that different types of companies have different attitudes towards digital transformation strategies, and take an institutional perspective to break down regional market barriers, as well as the barriers of mobility of knowledge and technology talents, achieving the sustainable development. A healthy knowledge protection system should be established to ensure a smooth flow of knowledge. Encourage corporate R&D collaboration to counteract the negative effects of talent shortages and provide some policy support for companies that are disadvantaged in the market to follow the principle of equality in a market economy. For business managers: Firstly, business managers should recognize the benefits of digital transformation for sustainable development and actively adopt a digital transformation strategy, for example, set up a digital office to effectively guide the digital transformation of the company. Secondly, they should understand that digital transformation is disrupting traditional views, blurring traditional business boundaries and facilitating the flow of knowledge, skilled people, female employees, senior staff and other elements. Finally, despite the increased costs of software, equipment, etc., digital transformation has a positive impact on production costs, sales costs and innovation. Business managers should establish a sound system of resource utilization, production chains and supply chains to realize the maximum effect of digital transformation.

There are also a few limitations to this paper. Firstly, due to the limitations of the study data, we were unable to capture the dynamics and long-term effects of digital transformation. Secondly, we have only explored the changes to traditional business models as a result of digital transformation, but ignored firm and regional heterogeneity, for example, small, medium and large enterprises, state-owned and non-state-owned enterprises, polluting and non-polluting enterprises, coastal and non-coastal enterprises, etc. Thirdly, corporate management characteristics are also important factors influencing digital transformation strategies. For example, overseas background of the board, educational background of the board, and foreign directors on the board. Therefore, we will keep exploring the relationship between digital transformation and corporate sustainability in depth in our future research.

Data availability statement

The data analyzed in this study is subject to the following licenses/restrictions: The datasets generated during and/or analysed during the current study are available in the CSMAR (China Stock Market and Accounting Research Database). Requests to access these datasets should be directed to https://www.gtarsc.com/.

Author contributions

PC, YH, and CZ wrote, edited and revised the text, created and edited figures and tables. PC and CZ contributed analysis and figures and edited. YH revised the manuscript. All authors contributed to the tables, wrote portions of the text, and edited the manuscript.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Abdalla, S., and Nakagawa, K. (2021). The interplay of digital transformation and collaborative innovation on supply chain ambidexterity. TIM. Rev. 11 (3), 45–56. doi:10.22215/timreview/1428

Ali, M., Ng, Y. L., and Kulik, C. T. (2014). Board age and gender diversity: A test of competing linear and curvilinear predictions. J. Bus. Ethics 125 (3), 497–512. doi:10.1007/s10551-013-1930-9

Andriushchenko, K., Buriachenko, A., Rozhko, O., Lavruk, O., Skok, P., Hlushchenko, Y., et al. (2020). Peculiarities of sustainable development of enterprises in the context of digital transformation. J. Entrepreneursh. Sustain. Issues 16 (3), 2255–2270. doi:10.9770/jesi.2020.7.3(53)

Antonio, A., and Tuffley, D. (2014). The gender digital divide in developing countries. Future Internet 6 (4), 673–687. doi:10.3390/fi6040673

Appio, F. P., Frattini, F., Petruzzelli, A. M., and Neirotti, P. (2021). Digital transformation and innovation management: A synthesis of existing research and an agenda for future studies. J. Prod. Innov. Manage. 38 (1), 4–20. doi:10.1111/jpim.12562

Arioglu, E. (2021). Board age and value diversity: Evidence from a collectivistic and paternalistic culture. Borsa Istanb. Rev. 21 (3), 209–226. doi:10.1016/j.bir.2020.10.004

Ballestar, M. T., Camina, E., Díaz-Chao, Á., and Torrent-Sellens, J. (2021). Productivity and employment effects of digital complementarities. J. Innovation Knowl. 6 (3), 177–190. doi:10.1016/j.jik.2020.10.006

Barrett, M., Davidson, E., Prabhu, J., and Vargo, S. L. (2015). Service innovation in the digital age: Key contributions and future directions. MIS Q. 39 (1), 135–154. doi:10.25300/misq/2015/39:1.03

Berger, A. N., Kick, T., and Schaeck, K. (2014). Executive board composition and bank risk taking. J. Corp. finance 28, 48–65. doi:10.1016/j.jcorpfin.2013.11.006

Bieser, J., and Hilty, L. (2018). Indirect effects of the digital transformation on environmental sustainability: Methodological challenges in assessing the greenhouse gas abatement potential of ICT. EPiC Ser. Comput. 52, 68–81.

Boulton, C. (2020). What is digital transformation? A necessary disruption. Available at https://www. cio. com/article/3211428/what-is-digital-transformation-a-necessary-disruption. html.

Branco, M. C., and Rodrigues, L. L. (2008). Social responsibility disclosure: A study of proxies for the public visibility of Portuguese banks. Br. Account. Rev. 40 (2), 161–181. doi:10.1016/j.bar.2008.02.004

Cader, H. A., and Leatherman, J. C. (2011). Small business survival and sample selection bias. Small Bus. Econ. 37 (2), 155–165. doi:10.1007/s11187-009-9240-4

Castagna, F., Centobelli, P., Cerchione, R., Esposito, E., Oropallo, E., and Passaro, R. (2020). Customer knowledge management in SMEs facing digital transformation. Sustainability 12 (9), 3899. doi:10.3390/su12093899

Certo, S. T. (2003). Influencing initial public offering investors with prestige: Signaling with board structures. Acad. Manag. Rev. 28 (3), 432–446. doi:10.2307/30040731

Chen, H. L. (2011). Does board independence influence the top management team? Evidence from strategic decisions toward internationalization. Corp. Gov. Int. Rev. 19 (4), 334–350. doi:10.1111/j.1467-8683.2011.00850.x

Chen, P., and Hao, Y. (2022). Digital transformation and corporate environmental performance: The moderating role of board characteristics. Corp. Soc. Responsib. Environ. Manag. 29 (5), 1757–1767. doi:10.1002/csr.2324

Chen, P. (2022). The impact of smart city pilots on corporate total factor productivity. Environ. Sci. Pollut. Res. Int., 1–14. doi:10.1007/s11356-022-21681-1

Chin, T., Wang, W., Yang, M., Duan, Y., and Chen, Y. (2021). The moderating effect of managerial discretion on blockchain technology and the firms’ innovation quality: Evidence from Chinese manufacturing firms. Int. J. Prod. Econ. 240, 108219. doi:10.1016/j.ijpe.2021.108219

Dalenogare, L. S., Benitez, G. B., Ayala, N. F., and Frank, A. G. (2018). The expected contribution of Industry 4.0 technologies for industrial performance. Int. J. Prod. Econ. 204, 383–394. doi:10.1016/j.ijpe.2018.08.019

Dragiewicz, M., Burgess, J., Matamoros-Fernández, A., Salter, M., Suzor, N. P., Woodlock, D., et al. (2018). Technology facilitated coercive control: Domestic violence and the competing roles of digital media platforms. Fem. Media Stud. 18 (4), 609–625. doi:10.1080/14680777.2018.1447341

Dregger, J., Niehaus, J., Ittermann, P., Hirsch-Kreinsen, H., and ten Hompel, M. (2016). “The digitization of manufacturing and its societal challenges: A framework for the future of industrial labor,” in 2016 IEEE international symposium on ethics in engineering, science and technology (ETHICS), Vancouver, BC, Canada, 08 September 2016, 1–3.

Drempetic, S., Klein, C., and Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. J. Bus. Ethics 167 (2), 333–360. doi:10.1007/s10551-019-04164-1

Eagly, A. H., and Karau, S. J. (2002). Role congruity theory of prejudice toward female leaders. Psychol. Rev. 109 (3), 573–598. doi:10.1037/0033-295x.109.3.573

Fan, S., Peng, S., and Liu, X. (2021). Can smart city policy facilitate the low-carbon economy in China? A quasi-natural experiment based on pilot city. Complexity 2021, 1–15. doi:10.1155/2021/9963404

Feroz, A. K., Zo, H., and Chiravuri, A. (2021). Digital transformation and environmental sustainability: A review and research agenda. Sustainability 13 (3), 1530. doi:10.3390/su13031530

Frank, A. G., Dalenogare, L. S., and Ayala, N. F. (2019). Industry 4.0 technologies: Implementation patterns in manufacturing companies. Int. J. Prod. Econ. 210, 15–26. doi:10.1016/j.ijpe.2019.01.004

Gfrerer, A. E., Rademacher, L., and Dobler, S. (2021). “Digital needs diversity: Innovation and digital leadership from a female managers’ perspective,” in Digitalization (Cham: Springer), 335–349.

Gomber, P., Kauffman, R. J., Parker, C., and Weber, B. W. (2018). On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. J. Manag. Inf. Syst. 35 (1), 220–265. doi:10.1080/07421222.2018.1440766

Gray, R., Kouhy, R., and Lavers, S. (1995). Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Account. Auditing Account. J. 8, 47–77. doi:10.1108/09513579510146996

Grober, U. (2007). A conceptual history of sustainable development Nachhaltigkeit. Wissenschaftszentrum Berlin für Sozialforschung.

Guo, L., and Xu, L. (2021). The effects of digital transformation on firm performance: Evidence from China’s manufacturing sector. Sustainability 13 (22), 12844. doi:10.3390/su132212844

Guo, X., Song, X., Dou, B., Wang, A., and Hu, H. (2022). Can digital transformation of the enterprise break the monopoly? Pers. Ubiquitous Comput., 1–14. doi:10.1007/s00779-022-01666-0

Hao, W., and Zhang, J. (2021). The reality, risk and governance of regional innovation ecosystems under digital transformation background. IOP Conf. Ser. Earth Environ. Sci. 769 (2), 022052. doi:10.1088/1755-1315/769/2/022052

Heckman, J., and Vytlacil, E. (1998). Instrumental variables methods for the correlated random coefficient model: Estimating the average rate of return to schooling when the return is correlated with schooling. J. Hum. Resour. 33, 974–987. doi:10.2307/146405

Hobbs, J. E. (2020). Food supply chains during the COVID-19 pandemic. Can. J. Agric. Economics/Revue Can. d'agroeconomie. 68 (2), 171–176. doi:10.1111/cjag.12237

Hrustek, L. (2020). Sustainability driven by agriculture through digital transformation. Sustainability 12 (20), 8596. doi:10.3390/su12208596

Hsu, C. S., Lai, W. H., and Yen, S. H. (2019). Boardroom diversity and operating performance: The moderating effect of strategic change. Emerg. Mark. Finance Trade 55 (11), 2448–2472. doi:10.1080/1540496x.2018.1519414

Hu, H. (2022). Can digital transformation of the enterprise break the monopoly? Personal Ubiquitous Comput., 1–14.

Iansiti, M., and Lakhani, K. R. (2020). Competing in the age of AI: Strategy and leadership when algorithms and networks run the world. Boston: Harvard Business Press.

Jafari-Sadeghi, V., Garcia-Perez, A., Candelo, E., and Couturier, J. (2021). Exploring the impact of digital transformation on technology entrepreneurship and technological market expansion: The role of technology readiness, exploration and exploitation. J. Bus. Res. 124, 100–111. doi:10.1016/j.jbusres.2020.11.020

James, P. (2014). Urban sustainability in theory and practice: Circles of sustainability. London: Routledge.

Jia, J., and Li, Z. (2020). Does external uncertainty matter in corporate sustainability performance? J. Corp. Finance 65, 101743. doi:10.1016/j.jcorpfin.2020.101743

Jiao, S., and Sun, Q. (2021). Digital economic development and its impact on econimic growth in China: Research based on the prespective of sustainability. Sustainability 13 (18), 10245. doi:10.3390/su131810245

Jiraporn, P., and Chintrakarn, P. (2013). How do powerful CEOs view corporate social responsibility (CSR)? An empirical note. Econ. Lett. 119 (3), 344–347. doi:10.1016/j.econlet.2013.03.026

Kamble, S. S., Gunasekaran, A., and Gawankar, S. A. (2018). Sustainable industry 4.0 framework: A systematic literature review identifying the current trends and future perspectives. Process Saf. Environ. Prot. 117, 408–425. doi:10.1016/j.psep.2018.05.009

Katmon, N., Mohamad, Z. Z., Norwani, N. M., and Farooque, O. A. (2019). Comprehensive board diversity and quality of corporate social responsibility disclosure: Evidence from an emerging market. J. Bus. Ethics 157 (2), 447–481. doi:10.1007/s10551-017-3672-6

Khalifaturofi'ah, S. O. (2018). Cost efficiency, total assets, and profitability: Evidence from islamic bank. J. Keuang. Dan. Perbank. 22 (4), 769–778.

Kohlrausch, B., and Weber, L. (2021). Gender relations at the digitalised workplace: The interrelation between digitalisation, gender, and work. Gend. a výzkum/Gender Res. 21 (2), 13–31. doi:10.13060/gav.2020.010

Kraus, S., Schiavone, F., Pluzhnikova, A., and Invernizzi, A. C. (2021). Digital transformation in healthcare: Analyzing the current state-of-research. J. Bus. Res. 123, 557–567. doi:10.1016/j.jbusres.2020.10.030

Lam, J. S. L., and Yap, W. Y. (2019). A stakeholder perspective of port city sustainable development. Sustainability 11 (2), 447. doi:10.3390/su11020447

Lee, C. C., Yuan, Y., and Wen, H. (2022). “Can digital economy alleviate CO2 emissions in the transport sector? Evidence from provincial panel data in China,” in Natural resources forum (Oxford, UK: Blackwell Publishing Ltd), 46, 289–310.

Liu, H., Xing, F., Li, B., and Yakshtas, K. (2020). Does the high-tech enterprise certification policy promote innovation in China? Sci. Public Policy 47 (5), 678–688. doi:10.1093/scipol/scaa050

Madaleno, M., and Vieira, E. (2020). Corporate performance and sustainability: Evidence from listed firms in Portugal and Spain. Energy Rep. 6, 141–147. doi:10.1016/j.egyr.2020.11.092

Mallin, C. A., and Michelon, G. (2011). Board reputation attributes and corporate social performance: An empirical investigation of the US best corporate citizens. Account. Bus. Res. 41 (2), 119–144. doi:10.1080/00014788.2011.550740

Matt, C., Hess, T., and Benlian, A. (2015). Digital transformation strategies. Bus. Inf. Syst. Eng. 57 (5), 339–343. doi:10.1007/s12599-015-0401-5

Mattila, M., Yrjölä, M., and Hautamäki, P. (2021). Digital transformation of business-to-business sales: What needs to be unlearned? J. Personal Sell. sales Manag. 41 (2), 113–129. doi:10.1080/08853134.2021.1916396

Miller, T., and Triana, M. D. C. (2009). Demographic diversity in the boardroom: Mediators of the board diversity–firm performance relationship. J. Manag. Stud. 46, 755–786. doi:10.1111/j.1467-6486.2009.00839.x

Moi, L., and Cabiddu, F. (2021). Leading digital transformation through an agile marketing capability: The case of spotahome. J. Manag. Gov. 25 (4), 1145–1177. doi:10.1007/s10997-020-09534-w

Nadkarni, S., and Prügl, R. (2021). Digital transformation: A review, synthesis and opportunities for future research. Manag. Rev. Q. 71 (2), 233–341. doi:10.1007/s11301-020-00185-7

Noor, M. M., Kamardin, H., and Ahmi, A. (2016). The relationship between board diversity of information and communication technology expertise and information and communication technology investment: A review of literature. Int. J. Econ. Financial Issues 6 (7S), 202–214.

Okrepilov, V., Kuzmina, S., and Kuznetsov, S. (2019). Tools of quality economics: Sustainable development of a ‘smart city’under conditions of digital transformation of the economy. IOP Conf. Ser. Mater. Sci. Eng. 497, 012134.

Perry, P. M. (2001). Holding your top talent. Research-Technology Manag. 44 (3), 26–30. doi:10.1080/08956308.2001.11671426

Philip, J., and Gavrilova Aguilar, M. (2022). Student perceptions of leadership skills necessary for digital transformation. J. Educ. Bus. 97 (2), 86–98. doi:10.1080/08832323.2021.1890540

Porter, M. E., and Heppelmann, J. E. (2014). How smart, connected products are transforming competition. Harv. Bus. Rev. 92 (11), 64–88.

Pucheta-Martínez, M. C., Bel-Oms, I., and Olcina-Sempere, G. (2019). Commitment of independent and institutional women directors to corporate social responsibility reporting. Bus. Ethics A Eur. Rev. 28 (3), 290–304. doi:10.1111/beer.12218

Rasiwala, F. S., and Kohli, B. (2021). Artificial intelligence in fintech: Understanding stakeholders perception on innovation, disruption, and transformation in finance. Int. J. Bus. Intell. Res. (IJBIR) 12 (1), 48–65. doi:10.4018/ijbir.20210101.oa3

Reguera-Alvarado, N., de Fuentes, P., and Laffarga, J. (2017). Does board gender diversity influence financial performance? Evidence from Spain. J. Bus. Ethics 141 (2), 337–350. doi:10.1007/s10551-015-2735-9

Santacreu, A. M., and Zhu, H. (2018). What does China’ S rise in patents mean? A look at quality vs. Quantity. A Look. A. T. Qual. vs. Quant., 1–2.

Setyawati, I. (2017). “Did the bank with bigger of total assets had ensured its financial soundness,” in 1st International Conference on Islamic Ecnomics, Business and Philanthropy, 169–175.

Sheina, S. G., Girya, L. V., Seraya, E. S., and Matveyko, R. B. (2019). Intelligent municipal system and sustainable development of the urban environment: Conversion prospects. IOP Conf. Ser. Mat. Sci. Eng. 698 (5), 055015. doi:10.1088/1757-899x/698/5/055015

Sidhu, J. S., Feng, Y., Volberda, H. W., and Van Den Bosch, F. A. (2021). In the Shadow of Social Stereotypes: Gender diversity on corporate boards, board chair’s gender and strategic change. Organ. Stud. 42 (11), 1677–1698. doi:10.1177/0170840620944560

Soto Setzke, D., Riasanow, T., Böhm, M., and Krcmar, H. (2021). Pathways to digital service innovation: The role of digital transformation strategies in established organizations. Inf. Syst. Front., 1–21. doi:10.1007/s10796-021-10112-0

Tang, M. C. (2017). Total factor productivity or labor productivity? Firm heterogeneity and location choice of multinationals. Int. Rev. Econ. Finance 49, 499–514. doi:10.1016/j.iref.2017.03.016

Terjesen, S., Couto, E. B., and Francisco, P. M. (2016). Does the presence of independent and female directors impact firm performance? A multi-country study of board diversity. J. Manag. Gov. 20 (3), 447–483. doi:10.1007/s10997-014-9307-8

Thompson, P. (2006). Patent citations and the geography of knowledge spillovers: Evidence from inventor-and examiner-added citations. Rev. Econ. Stat. 88 (2), 383–388. doi:10.1162/rest.88.2.383

Trenerry, B., Chng, S., Wang, Y., Suhaila, Z. S., Lim, S. S., Lu, H. Y., et al. (2021). Preparing workplaces for digital transformation: An integrative review and framework of multi-level factors. Front. Psychol. 12, 620766. doi:10.3389/fpsyg.2021.620766

Ustundag, A., and Cevikcan, E. (2017). Industry 4.0: Managing the digital transformation. Berlin: Springer.

Vachon, S., and Mao, Z. (2008). Linking supply chain strength to sustainable development: A country-level analysis. J. Clean. Prod. 16 (15), 1552–1560. doi:10.1016/j.jclepro.2008.04.012

Vaska, S., Massaro, M., Bagarotto, E. M., and Dal Mas, F. (2021). The digital transformation of business model innovation: A structured literature review. Front. Psychol. 11, 539363. doi:10.3389/fpsyg.2020.539363

Verhoef, P. C., Broekhuizen, T., Bart, Y., Bhattacharya, A., Dong, J. Q., Fabian, N., et al. (2021). Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 122, 889–901. doi:10.1016/j.jbusres.2019.09.022

Wen, H., Zhong, Q., and Lee, C. C. (2022). Digitalization, competition strategy and corporate innovation: Evidence from Chinese manufacturing listed companies. Int. Rev. Financial Analysis 82, 102166. doi:10.1016/j.irfa.2022.102166

Wicklin, R. (2011). Log transformations: How to handle negative data values. Statistical programming in SAS with an emphasis on SAS/IML programs. Available at http://blogs. sas. com/content/iml/2011/04/27/log-transformations-how-to-handle-negative-datavalues. html.

Wolfe, J. C. (2020). Disruption in the boardroom: Leading corporate governance and oversight into an evolving digital future. New york: Apress.

Yang, J., and Ding, H. (2018). A quantitative assessment of sustainable development based on relative resource carrying capacity in Jiangsu Province of China. Int. J. Environ. Res. Public Health 15 (12), 2786. doi:10.3390/ijerph15122786

Zaid, M. A., Wang, M., Adib, M., Sahyouni, A., and Abuhijleh, S. T. (2020). Boardroom nationality and gender diversity: Implications for corporate sustainability performance. J. Clean. Prod. 251, 119652. doi:10.1016/j.jclepro.2019.119652

Zeng, G., and Lei, L. (2021). Digital transformation and corporate total factor productivity: Empirical evidence based on listed enterprises. Discrete Dyn. Nat. Soc. 2021, 1–6. doi:10.1155/2021/9155861

Zhai, H., Yang, M., and Chan, K. C. (2022). Does digital transformation enhance a firm's performance? Evidence from China. Technol. Soc. 68, 101841. doi:10.1016/j.techsoc.2021.101841

Zhang, Y. J., Shi, W., and Jiang, L. (2020). Does China's carbon emissions trading policy improve the technology innovation of relevant enterprises? Bus. Strategy Environ. 29 (3), 872–885. doi:10.1002/bse.2404

Zhao, S., Peng, D., Wen, H., and Wu, Y. (2022). Nonlinear and spatial spillover effects of the digital economy on green total factor energy efficiency: Evidence from 281 cities in China. Environ. Sci. Pollut. Res. Int., 1–21. doi:10.1007/s11356-022-22694-6

Appendix A:

TABLE A1. Corporate sustainability disclosure items.

TABLE A2. Balancing test.

FIGURE A1. Propensity score of the treated, matched and unmatched controls.

Keywords: digital transformation, textual analysis, knowledge flow barriers, talent barriers, boardroom women, older members

Citation: Zhang C, Chen P and Hao Y (2022) The impact of digital transformation on corporate sustainability- new evidence from Chinese listed companies. Front. Environ. Sci. 10:1047418. doi: 10.3389/fenvs.2022.1047418

Received: 18 September 2022; Accepted: 03 November 2022;

Published: 17 November 2022.

Edited by:

Kifayat Ullah, Riphah International University, PakistanReviewed by:

Huwei Wen, Nanchang University, ChinaMuhammad Azeem, Putra Malaysia University, Malaysia

Copyright © 2022 Zhang, Chen and Hao. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Pengyu Chen, cpy702018@163.com; Yuanyuan Hao, 529513408@qq.com