Abstract

The question of whether communicable or non-communicable diseases have higher economic effects on households is rarely explored from the global to local level despite of their significant contribution in increasing household catastrophic spending and impoverishment. To shed light into this, therefore, this paper comparatively examines the economic effects of communicable and non-communicable diseases in Tanzania by the use of Tanzania Panel Survey data of 2019/2020 which has been used to analyze different parameters to provide needful information. The empirical analysis employed probit, two-stage residual inclusion (2SRI), and control function approachf (CFA) helpful in controlling endogeneity issues. Findings showed that, comparatively, non-communicable diseases have higher economic effects in endangering households into catastrophic spending and impoverishment comparing to communicable diseases. Conclusively, neglecting developing countries to fights against multiplicative effects of these diseases alone will result in killing their economies since most of these countries depend on donors and household as a means of healthcare financing. However, this paper recommends for global initiatives in reducing the burden of disease by funding on palliative care costs and enhancing the availability of affordable health insurance schemes to reduce household economic burden.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Several research studies have been conducted on communicable and non-communicable diseases (NCDs) to examine the burden of these diseases on household income at the national and global level, but few scholarly works look at both at the same time and compare their consequences on catastrophic expenditure and deprivation (Kazibwe et al., 2021; Bhuyan, 2019; Wamai et al., 2018).

Moreover, communicable diseases have been the leading causative of death globally, but suddenly due to the major medical improvement, innovations, and changes in the way of life, NCDs have overtaken communicable diseases in terms of morbidity and mortality. The complexity of NCDs has been higher than communicable diseases because most NCDs are directly linked with daily human lifestyles, unlike most communicable diseases (Andrew, 2019; Young, 2015). However, NCDs being dangerous killer diseases worldwide today do not mean that malaria, HIV/AIDS, diarrhea, and other recent pandemic diseases like COVID-19 are not severely affecting the universe population but are just well managed due to the improved medical innovations.

Statistically, in 2019, the major top ten causes of death accounted for 55% of entire 55.4 million deaths worldwide with the leading causative on the total number of lives lost being cardiovascular, respiratory infections, neonatal conditions, and other birth complications, while tuberculosis has been one of the world’s worst infectious illnesses, inflicting around 1.2 million fatalities per year. Other deadliest infectious diseases are cholera, malaria, HIV/AIDS, measles, and hepatitis C (Andrew, 2019; WHO, 2020).

Additionally, 71% of the 56.9 million death cases reported globally in 2016 were due to communicable diseases mainly from cancer, heart disease, and diabetes as well as chronic respiratory diseases. These statistics justify that NCDs have surpassed even the most killer diseases like HIV and Malaria. Astonishingly, about 66% of the reported deaths due to NCDs were from middle- and lower-income countries (Andrew, 2019; Mariara et al., 2018; Wamai et al., 2018).

Africa has the highest prevalence of communicable diseases in the world. In 2015, more than three times as many people died from AIDS in sub-Saharan Africa, and more than ten times as many people died from malaria as in the rest of the world combined. However, a World Bank report claims that by 2030, non-communicable diseases are expected to cause more deaths in Africa than communicable diseases of which for every 100 deaths, 70 will be due to NCDs (WHO, 2020; Narayan & Donnenfeld, 2016).

Moreover, between 50 and 88% of deaths in seven African countries, mostly small island nations, are due to non-communicable diseases (WHO, 2022). In addition to that, in seven other countries—majority of them being Africa’s most populous—the diseases claimed between 100,000 and 450,000 lives annually. The WHO reports 2022 indicates that the growing burden of non-communicable diseases has posed a grave threat to the health and lives of millions of people in Africa as more than a third of deaths in the region are due to these illnesses.

Despite of the rising burden of the NCDs, yet communicable diseases have significant share of burden among African countries. As indicated in Fig. 1, major communicable diseases like HIV/AIDS, tuberculosis, and diarrheal in total contribute large number of share of deaths among African countries in 2022. Nowhere is this contrast more striking than in sub-Saharan Africa, where communicable, maternal, nutritional, and newborn diseases continue to dominate. The dramatic progress has been made in reducing the loss of life from many types of communicable diseases and conditions of early childhood, especially diarrheal diseases and lower respiratory infections.

Leading causative of deaths in Africa

In 2016, more than one billion people in sub-Saharan countries, including Tanzania, were affected by CVDs. The disease is accounting for 38.3% of all NCDs deaths, 11.3% of deaths from all causes in the region, and 5.5% of the global CVD-related deaths. Cardiovascular-related diseases are expected to double in sub-Saharan Africa (SSA) by 2020 if there will be no implementation of preventive measures (Andrew, 2019).

On the other hand, Tanzania as one of the African countries in the sub-Saharan regions is not exempted from the burden that has been caused by these diseases. According to recent estimates, approximately 33% of all Tanzanian population is affected by NCDs, mainly being due to cardiovascular diseases, cancer, diabetes, and chronic respiratory diseases4as it has been presented at Table 1.

Additionally, the rate of mortality due to these diseases is highly unacceptable despite having an unequal share in causing the number of deaths and increasing the burden on household income (Chen et al., 2018). Although the major burden due to these diseases at the household level has been the loss of the family members and debts incurred by households to treat the sick family members, at the national level, however, burdens are experienced through increased country’s health economic costs. Nonetheless, the burden at the household level is always coupled when such households are hit with other nutritious deficiencies and maternal problems which are dominant across low- and middle-income nations (Ritchie & Roser, 2018).

Burdens are severe at the household level when households are spending more of its disposable income on treating sick household member to the extent of threating household ability to save and do other socioeconomic activities. At this point, a household is therefore said to fall under catastrophic spending due to healthcare services. However, in this study, health spending is regarded as catastrophic when it exceeded 10% or 25% of household consumption (Wagstaff et al., 2018).

Overview of Tanzania Health System

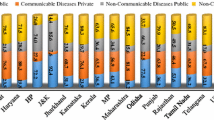

Tanzania is a resource-strained country with a weak healthcare system which is challenged by high maternal mortality, child mortality, HIV/AIDS, pneumonia, and malaria. Tanzania’s population also has some of the lowest rates of access to health personnel in the world. Over 60% of Tanzania healthcare facilities are run by the government with the rest being either faith-based or private. As the country Tanzania is progressing towards universal healthcare, in 2020/2021, the government allocated $387.9 million for the health sector of which $155.5 million were spent on development projects (ITA, 2021). Additionally, high proportions of Tanzania’s health financing (Fig. 2) are financed by foreign donors, despite of the decline in the household contribution, yet for a decade now, households have been highly financing health sector in the country through out-of-pocket (OOP) payments more than the government share of expenditure on it.

Share of healthcare financing in Tanzania, by source

Administratively, Tanzania has a hierarchical health system which is in tandem with the political-administrative hierarchy (Andrew, 2019). At the bottom, there are the dispensaries found in every village where the village leaders have a direct influence on its running. The health centers are found at ward level and the health center in charge is answerable to the ward leaders. At the district, there is a district hospital and at the regional level a regional referral hospital. The tertiary level is usually the zone hospitals, and at a national level, there is the national hospital. There are also some specialized hospitals that do not fit directly into this hierarchy and therefore are directly linked to the ministry of health.

Despite bigger burden enthroned on the shoulders of household on healthcare financing in Tanzania, yet a modest proportion of the population are enrolled in social, community, or private health insurance. Health insurance coverage is still low with only 32% of Tanzanians as of 2019 covered by health insurance. Of that number, only 1% are members of private health insurance.

Diseases and Economy

Communicable and non-communicable diseases have a substantial influence on family income and productivity, which is mostly caused by a loss in the labor force owing to death, absenteeism, and even an increase in the number of workers retiring early (Xu et al., 2003). On the other hand, households are forced to spend a lot of money and cut household income due to high treatment costs coupled with the inability to smooth consumption. Another important effect is on the depletion of lifetime expectations and increased social rate of time preferences.

Ultimately, these increase household dependency ratio, diminishing productivity of labor, lowering household financial resilient, and increasing total household spending as well lowering household capability for the investments in physical capital. Despite these burdens that cut across all households globally, yet severe burdens are experienced in developing countries where health financing systems are not well established and hence deepening poverty (Andrew, 2019; Young, 2015).

Moreover, spending on health is growing faster than the rest of the global economy, accounting for 10% of global gross domestic product (GDP). The WHO reveals that there is a swift upward trajectory of global health spending, which is particularly noticeable in low- and middle-income countries where health spending is growing on average 6% annually compared with 4% in high-income countries. On the other hand, governments provide an average of 51% of a country’s health spending, while more than 35% of health spending per country comes from out-of-pocket expenses. One consequence of this is 100 million people pushed into extreme poverty each year (Andrew, 2019; WHO, 2019).

In cementing these intuitions, literatures report that an average of 2 to 10% of households globally is facing catastrophic healthcare spending with the projections that the situation is worser in developing countries especially in African countries where majority of the world poor population lives (Marshall et al., 2022; Narayan & Donnenfeld, 2016).

This burden threats economic growth in the continent through diversion of resources to healthcare and this cut across all levels from the household to national level. Diseases erode a household’s income and diminish the future productivity of the patients. Moreover, through lowering households’ incomes, and spending power and production capacity, diseases therefore slow down economic growth.

For example, a health life lost estimate by the WHO shows that more than 630 million years have been lost in the Africa region alone with more than 2.4 trillion US dollars being wasted for controlling diseases in 2017 (Andrew, 2019; Wamai et al., 2018). Diseases drain productivity and increase inefficiencies (WHO, 2020), and in sub-Saharan Africa alone, more than 21 million productive years have been lost due to diseases (Kagaruki et al., 2015; Gaziano, 2005).

On the other hand, due to effects of these diseases, health systems in Africa have been challenged by insufficient number of human resources for health, medications, and other medical equipment, of which the final bearer of the burden has always been households. For instance, the cost for treating severe NCDs in Tanzania reached US$ 100 million in 2005 and are projected to reach US$ 500 million in 2025 of which this is expected to deplete more than US$ 2.5 billion in 2025 billion, whereas the burden is always experienced heavily at the household level (Andrew, 2019; Mwai & Muriithi, 2015).

Researches show that households have been selling off their belongings especially the most valuable family or personal assets to acquire money to meet requirements for medical treatment and other healthcare costs and this creates loopholes for the consumption of the accumulated capital. In a long run, capital consumption increases households’ implications on the ability for these households to pay for healthcare as well as the other consumable goods for health which later cracks the household’s level of productivity and incomes (Andrew, 2019; Kyobutungi et al., 2008; Mwai & Muriithi, 2015), hence weakening households’ ability to accumulate wealth by wiping out savings and other durable resources, and thus households become prone to poverty through catastrophic spending and excessive out-of-pocket spending on healthcare service.

Catastrophic health expenditure is a real challenge among household in most developing countries including Tanzania that needs to be well addressed as it has been highly used as a means of healthcare financing despite its effects in increasing inequity in healthcare provision. Tanzania recorded a low share of healthcare expenditure of 7.2% of the country’s GDP (Andrew, 2019) characterized by lower public spending on health at 39% (Andrew, 2019; WHO, 2020). According to Tanzania’s Ministry of Health, catastrophic health expenditure accounts for 52% of entire health spending, with the remainder split between private and public payment systems (Andrew, 2019).

Although catastrophic healthcare payments occur in both rich and poor countries, but more than 90% of the people affected resides in low-income countries. Catastrophic health expenditure can occur regardless of the amount of money paid to healthcare services. Rich households might pay large medical bills without experiencing negative implications, while low levels of spending among poor households can have severe financial implications for livelihoods (Chuma & Maina, 2012).

Various studies have assessed impacts of catastrophic spending on household poverty. These studies, largely conducted in Asia and Latin America, show that healthcare costs are major causes of impoverishment. In their study on health expenditures in 11 Asian countries, they reported that poverty estimates were 14% higher when OOP payments are accounted for and that about 78 million people are pushed into poverty due to healthcare costs (van Doorslaer et al., 2006). Elsewhere, a survey of 89 countries found that catastrophic expenditure was reported by 3%, 1.8%, and 0.6% of households in low-, middle-, and high-income countries respectively (Xu et al., 2007). Few studies have documented the levels of catastrophic health expenditures in Africa. In Burkina Faso, about 15% of households reporting illness incurred costs greater than 40% of their non-food consumption expenditure (Su et al., 2006), while in Uganda, 2.9% of households incurred catastrophic expenditure in 2003 (Xu et al., 2006). In Nigeria, 40.2% of households incurred costs greater than 10% of their consumption expenditure; this proportion reduced to 14.8% when the threshold was set at 40% (Onoka et al., 2011). The poorest households were more likely to incur catastrophic expenditures compared to households.

The major limitation of the few studies conducted in Africa is that they do not assess the implications of healthcare costs on catastrophic spending and impoverishment (Chuma & Maina, 2012; Mwai & Muriithi, 2015; Bhuyan, 2019). Assessing the role of healthcare payments on poverty is important for informing policy on the need to incorporate health financing designs in poverty reduction programs and for highlighting the urgent need to ensure that health financing systems offer financial risk protection. This paper contributes to the literature by comparatively assessing the extent of catastrophic health spending and impoverishment in Tanzania due to communicable and non-communicable diseases.

Specifically, this study provides a wake-up call findings for African countries towards the realization of the Sustainable Development Goals (SDGs) 2030 and African Agenda 2063 in reducing disease burden among households and achieving general target of ensuring health lives and promote well-being for all at all ages.

Theoretical Modeling

According to the unitary household model of a consumer behavior, a household is considered to behave as if it maximizes a single price–independent social utility function subject to a family budget constraint (Becker, 1962; Mwai & Muriithi, 2015). Therefore, household members whose characteristics are given by \(h\) are assumed to derive utility from the consumption of goods \(c\). Total household income \(Y\) is therefore the sum of incomes earned by each household members (labor income \({l}_{i}{w}_{i}\) and non-labor income \({y}_{j}\)), as well as the income received by household members jointly, \({y}_{j}\) (Mwai & Muriithi, 2015).

Therefore, the household with members \(i\in \left[\mathrm{1,2}\dots \dots ..n\right]\) is facing utility maximization problem that:

However, the utility-maximizing Eq. (1) is thereafter subjected to the household income Eq. (2) which states that:

Additionally, the income generated by labor \({l}_{i}{w}_{i}\) comprises of the salaries and wages, while the non-labor income denoted by \({y}_{j}\) consists of dividends, interest, remittances, and other household’s financial returns. Assuming income is a pooled and individual members in a household have identical preferences, the generic response to the expressed utility maximization problem will result in the household consumption function in terms of prices, \(p\), total household income \(Y\), and household characteristics, \(h\), as presented in Eq. (3):

Therefore, due to the limitations of the unitary model (Chiappori, 1992; Apps & Rees, 1997), the collective household models have been developed with the assumption that the individual member of the household has a utility of \({U}^{\sim i}={\widetilde{u}}^{i} ({c}^{1}, {c}^{2}\dots \dots {c}^{n}, h)\), whereas \({c}^{s} (s=1, 2\dots .n)\) and \(h\) symbolize the consumption function of an individual and the characteristics of the household simultaneously. Therefore, the utility-maximizing function for the household Pareto efficiency is expressed as:

Equation (4) can also be presented as:

where \(W[\cdot ]\) is a price-dependent household aggregate utility function and the maximization is subject to the household budget constraints which is an increasing function of the utility of each household member \({\widetilde{u}}^{1}\) to \({\widetilde{u}}^{n}\). Moreover, the solution on the maximization problem is a Marshallian demand function for each household member, while the covariates of the demand function are household sociodemographic characteristics, individual and joint household income, and the prices.

Household Catastrophic Spending and Impoverishment Models

This research study applied the methodology used by Mahal et al. (2010) and Andrew (2019) in estimating the contribution of non-communicable diseases to catastrophic expenditure. Catastrophic spending normally occurs when expenditure on health surpasses a household’s ability to pay. In this study, the ability to pay is classified when a household consumption spending less combined survival income for all household members.

Therefore, the catastrophic expenditure is expressed as:

where \({M}_{j}\) is the ratio of household healthcare expenditures to its total consumption minus all household members’ combined survival income. The \({M}_{j}\) greater than 30% signifies catastrophic spending. The numerator \({th}_{j}\) reflects household expenditure \(j\), while the denominator \({T}_{cj}\) indicates total household consumption, \(n\) is the size of the household, and \(p\) is the poverty threshold.

Additionally, this paper also examined the probability at which CDs and NCDs influence households to fall under catastrophic expenditure which has been obtained by estimating Eq. (7). A household insurance acquisition has been estimated in the model to assess whether the insured household has an impact or any significant change in lowering the probability for the occurrence of catastrophic spending in the presence of diseases (CDs or NCDs). The model for household catastrophic spending due to NCDs is conveyed as:

whereby a dummy variable \({C}_{sj}\) assumes the value of 1 for households that incurred the catastrophic spending, while another dummy variable \({ncd}_{j}\) shows the presence of an NCD; on the other hand, the dummy \({ins}_{j}\) is a categorical variable showing whether a household has purchased or obtained health insurance, \({h}_{j}\) represents a vector of household characteristics, and \(\alpha\), \(\beta\), and \(\lambda\) are the parameters to be estimated, while \({v}_{j}\) is the stochastic parameter. Additionally, the possible endogeneity may arise during estimating Eq. (7) because the presence of NCDs is also caused by other exogenous factors of which without suppressing, it will lead to estimation bias (“Endogeneity and Heterogeneity” section).

Moreover, this study examines the fact whether household spending on non-communicable diseases impoverishes households in Tanzania of which the relationship of the aforementioned fact can be established through the following set of equations.

From the above equations, \({T}_{sj}^{pc}\), \({T}_{sj}\), and \({T}_{sj}^{npc}\) represent the per capita household spending, gross household spending, and net per capita spending of the household simultaneously, and also \({h}_{j}\) and \({n}_{j}\) are the health spending and household size respectively. The household health expenditure will be considered to be an impoverishing factor if the gross per capita spending of the household exceeds the poverty line for that particular household, while the net per capita spending of the household is also less than the household poverty level of the given expenditure.

To estimate the household impoverishment as the result of NCDs, Eq. (8) is estimated of which the health insurance variables are also included as an important institution parameter that can reduce the household possibility for impoverishment. Additionally estimating Eq. (8) without controlling endogeneity can also make results inconsistent and bias; hence, controlling it is necessary (“Endogeneity and Heterogeneity” section);

From the above equation, \({I}_{sj}\) is a dummy variable that explains whether a household is experiencing an impoverishment; \({ncd}_{\mathrm{ij}}\) is also a dummy variable that shows catastrophic spending (as used herein in the report that is above the cutting point of 30%) as a result of NCDs in a household, while the dummy for insurance is \({ins}_{j}\) and \({h}_{j}\) represents the household characteristics. \({\alpha }_{0}\), \(\gamma\), and \({\beta }_{1}\) are the obtained parameters that have to be estimated, while \({\mu }_{j}\) is a stochastic term.

Methods and Data

Source and Description of Data

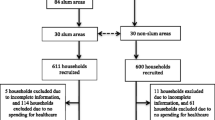

This study has utilized the 2019/2020 National Panel Survey exaggerated data of the World Bank collected by the Tanzania Bureau of Statistics which adopted a two-stage cluster sampling design. Moreover, the survey was completed by 9465 households out of a total of 9552 homes, obtaining a response rate of 99% in the entire country as the survey mapped 27 regions into 419 clusters 248.

Endogeneity and Heterogeneity

In this study, the problem of endogeneity occurred during estimating Eqs. (5) and (8). Normally, endogeneity occurs when there is a correlation between variables of interest and the error term (Table 2). In estimation for the catastrophic and impoverishment models, the likelihood of health inputs being correlated with the stochastic term is high. Therefore, failure to adjust and control this problem of endogeneity will make the parameter estimates to be biased and inconsistent.

However, in relaxing these challenges, instrumental variable (IV) and the two-stage residual inclusion (2SRI) have been applied. 2SRI is the best technique for controlling endogeneity in both linear and non-linear models (Andrew, 2019). 2SRI involves two procedures of which at first, it involves the calculation of residuals to a reduced form from the estimated functions and inserting those residuals as added explanatory variables in the second-stage regression. Generally, the control function approach is an extension of the two-stage residuals with null hypothesis tests of the exogeneity and more often is known as the new stage reduced equation which helps to control both endogeneity and heterogeneity (Andrew, 2019; Mariara et al., 2018).

The instrument used in suppressing this endogeneity arose during estimating Eqs. (5) and (8) is the distance to healthcare facility of which Eqs. (5) and (8) were found to be exactly identified. On the other hand, since CDs, NCDs, impoverishment, and catastrophic spending are binary outcome variables, the probit model has been used in hypothesizing the underlying latent variable. The main advantage with this method is its linearity effect of regressors with latent variables ranging from minus infinity to plus infinity (\(-\mathbf{\infty }\ {\boldsymbol{t}}{\boldsymbol{o}}+\mathbf{\infty })\) while the observed values being 0 or 1 (Andrew, 2019).

Testing Validity of Instruments

Establishing an appropriate instrument in explaining the structural equation is one of the key challenges for controlling endogeneity when using the IV technique. Therefore, the best instruments are noticed by assessing the validity of that instrument and its strength. The decision for checking for validity helps to understand whether instruments possess three characteristics of a good instrument as identified by scholars (Andrew, 2019; Mwai & Muriithi, 2015; Mariara et al., 2018; O'Donnell et al., 2005) that good instruments are those with a high degree of correlation to the endogenous variable while having no causal direct effects on outcome measures, and exogenous in the model specification; when all these characteristics are observed, the instrument is therefore strong and valid whose justification is based on the first-stage regression F statistic and eigenvalue statistic tests as shown in Tables 3 and 4.

The decision criteria on the first-stage F statistic result on Table 3 are based on the ability of the partial R-squared to explain the variations of explanatory variable on the explained variable. Therefore, the partial R-squared is greater and significant and then the instrument is considered not weak. Moreover, Table 4 explains that, since none of the critical values are larger than the minimum eigenvalue statistic, then the null hypothesis that instrument used is weak is rejected and concluding that instrument is strong and satisfies the three conditions of good instrument.

Presentation of Findings

Catastrophic Spending and Communicable Diseases

Table 5 shows the determinant factors for catastrophic health expenditure in households with communicable diseases being the variable of interest. The analysis of the probit model shows that coefficients are insignificant despite being positive before endogeneity and heterogeneity being controlled, and after controlling them, the coefficient becomes both significant and positive as it has been illustrated in column 4 of the output in Table 5.

Control function approach results presented in the last column of Table 5 show that likelihood of occurrence for catastrophic spending is 34.81% higher when a household is experiencing members suffering from communicable diseases. Additionally, the chances for urban residents falling into catastrophic expenditure are 12.804% lower than that of rural residents, which is comfortably proven by the presence of significant income reported from urban households. These findings are contrary to those made in Bangladesh (Bhuyan, 2019) and Kenya (Mwai & Muriithi, 2015).

On the other hand, findings reveal that an increase in household size lowers the likelihood of developing catastrophic spending by 2.77%. However, these findings are inconsistent with the study conducted in Asia which argued that households with large household sizes have higher chances of having large sick members and hence facing catastrophic spending (O'Donnell et al., 2005). The effects are more severe to households that have no health insurance or any other form of waivers as this study has found that having health insurance reduces chances for the households falling into catastrophic spending by 53.926% compared to those households that have no health insurance. Therefore, health insurance is one of the most significant initiatives towards the lowering effects of the catastrophic spending among households in developing countries like Tanzania and hence weakening the power of impoverishment.

Catastrophic Expenditure and Non-Communicable Diseases

This part entails arguments on features of catastrophic healthcare spending due to non-communicable diseases (NCDs) of which all of the standardized coefficients in Table 6 explain the likelihood of a household falling into catastrophic spending. Column 2 indicates that NCD is both a positive and significant coefficient; however, the magnitude of the coefficient improves after controlling heterogeneity and endogeneity. The confirmatory test for the presence of endogeneity is the significance of the residuals, whereas the control function approach with the interaction effects between NCDs and its residual helped to resolve the problem.

Additionally, the control of endogeneity helped the coefficients to increase since there is no heterogeneity in this estimation. Surprisingly, the coefficient of interaction between non-communicable diseases and residuals (NCD*residual) in column 4 is insignificant, while the coefficient of residual for NCD is significant. This makes the estimation output for 2SRI to be unbiased, consistent, reliable, and harmonious.

The odds for households experiencing catastrophic health spending are 52.684% when there is an NCD victim in a household compared to households that have not been reported suffering from CDs. These findings emphasize that having affected by non-communicable diseases increases the chances for household impoverishment and paralyzes household income due to the increased healthcare spending recalling that an average household’s treatment costs for major NCDs like cardiovascular, cancer, and diabetes in developing countries are $6055.99, $3303.81, and $1017.05 simultaneously which are higher than the GNI of Tanzania which stands at $1080 (Kazibwe et al., 2021).

Communicable Diseases Versus Non-Communicable Diseases on Impoverishment

To understand the extent of the household impoverishment caused by these two groups of diseases, this study has analyzed effects of both diseases on household impoverishment by estimating Eq. (8) for both diseases, and the decision has therefore made based on the extent of influence of caused by the diseases as presented in Tables 7 and 8.

In order to control the problem of endogeneity in the impoverishment models, the 2SRI has been used, making results improved and become more harmonious at column 3. The interaction term insignificance justifies that the heterogeneity is not a problem in this model as it has been suppressed. The coefficient of multiplicative interaction effects of residual and CDs is insignificant, while residuals itself have been seen to be significant at column 3 of 2SRI and insignificant at column 4 of CFA. Therefore, the estimation herein will be done by the use of 2SRI. Therefore, results on column 3 of Table 7 show that odds of household impoverishment due to the prevalence of communicable diseases in a household are 31.576%. The most harmonious technique in estimating NCD effects on household impoverishment is CFA as shown in column 4 of Table 8. According to the findings, households affected by NCDs are likely to be impoverished by 59.746% being 27.17%Footnote 1 higher than households that have been affected by CDs.

The gap between these two groups of diseases is also higher in influencing housing catastrophic spending as results in Table 5 show that CDs have an impact of 34.810%, while NCDs on Table 6 show that the impacts are 52.684% making NCDs being the most leading causative of the catastrophic spending by 17.876%Footnote 2 higher than CDs. Although NCDs have been found to have a greater burden than CDs, yet both have a significant impact on the increase of catastrophic spending and impoverishment.

Discussion

This study has proven that these two groups of diseases deprive individuals’ health and their production capabilities, thus having a greater burden with intense effects on the household savings and income and slowing down the investment activities. Additionally, they lower life span and badly affect productivity, therefore depleting the quantity and quality of countries’ labor force which ends in lowering national output in national income (GNI and GDP) while making households vulnerable to poverty.

In cementing these arguments, from 2000 to 2019, the global health expenditure has risen to reach US$ 8.3 trillion which is nearly 10% of the global GDP (WHO, 2020). Additionally, most burdens are experienced in developing countries where OOP expenditure has remained high close to 42% of the total health spending in 2018 (Andrew, 2019). These justify the increased burden of diseases in the economy where developing countries are highly hit.

Results herein advise that health ministries and other local and international stakeholders are obliged to establish formal apparatus or machinery that will be responsible for enhancing the adoption of precautionary care for most diseases. Normally, preventive health programs are cost-effective compared to costs for curative programs; therefore, prevention strategies aiming at addressing diseases in most of the developing countries are the best approach in reducing effects associated with these diseases as most of these diseases are costly which are lately discovered and become chronic to treatments. Increasing public awareness and encouraging frequently medical checkups as well as provision of the most affordable health insurance can be one of the best strategies in reducing the effects of these diseases at the household and national level.

Finally, the aim of fighting diseases should not be limited to lowering the rate of transmission or prevalence of diseases rather on the increasing productivity and welfare from households to the national level of which this will be achieved by increasing investment (share of GDP expenditure) on the health sector and meet required international standards.

Policy Recommendation

The findings of this study have clearly shown that the burden of diseases is high in Tanzania causing the growth of catastrophic spending and some households falling into impoverishment due to the costs of treating sick members of households. Moreover, since non-communicable diseases have been found to have higher impacts in the prevalence of both catastrophic spending and impoverishment among households in Tanzania, therefore, this study suggests that strong government and political willingness are required to enhance the availability of cheap health insurance schemes that will able afforded by large number of people.

Health insurances in this study have been found to reduce pressures of both catastrophic spending and impoverishment, meaning that through effective government interventions in making health insurance an important right for all citizens in a country, it will help to reduce these pressures to a large extent as results have indicated that the existence of out of pocket increases both catastrophic spending and impoverishment. Thus, Tanzania’s and the entire developing countries’ governments should urgently consider alternative health financing mechanisms that offer financial risk protection to the population that the out-of-pocket payments which have proven in this study to increase both catastrophic spending and impoverishments.

Therefore, developing countries should encourage utilizing risk pooling and income cross-subsidization system that offers financial risk protection among residents instead of just making new polies everyday that are hardly implemented within the limited budget. However, donor-funded projects in health sector should aim at ensuring at lessening the health-caused poverty by investing in the health infrastructures and the availability of community-based health insurances. Thus, the results presented in this paper show the urgent need for developing countries to move beyond endless political discussions and delays and implement reforms that will protect the population from healthcare-related impoverishment.

Availability of Data and Materials

Data set and all other materials will be available upon reasonable request.

References

Andrew, F. (2019). Non communicable diseases in Tanzania: Economic effects and risks factors. Mzumbe University, Morogoro-Tanzania. http://scholar.mzumbe.ac.tz/handle/11192/277/browse?value=Andrew%2C+Felician&type=author. Accessed 01 Jan 2022.

Apps, F., & Rees, R. (1997). Collective labor supply and household production. The Journal of Political Economy, 105(1), 178–190. https://doi.org/10.1086/262070

Becker, G. S. (1962). Investment in human capital: A theoretical analysis. Journal of Political Economy, 70(5), 9–49. Retrieved February 12, 2022, from http://www.jstor.org/stable/1829103

Bhuyan, K. C. (2019). Economic consequences of non-communicable diseases at household level: A case study among adults of some households in Bangladesh. American Journal of Data Mining and Knowledge Discovery, 4(2), 63–69. https://doi.org/10.11648/j.ajdmkd.20190402.12

Chen, S., Kuhn, M., Prettner, K., & Bloom, D. E. (2018). The macroeconomic burden of non communicable diseases in the United States: Estimates and projections. PLoS ONE, 13(11), e0206702. https://doi.org/10.1371/journal.pone.0206702

Chiappori, P. A. (1992). Collective labor supply and welfare. Journal of Political Economy, 105, 191–209. https://doi.org/10.1086/261825

Chuma, J., & Maina, T. (2012). Catastrophic health care spending and impoverishment in Kenya. BMC Health Services Research, 12, 413. https://doi.org/10.1186/1472-6963-12-413

Gaziano, A. T. (2005). Cardiovascular disease in the developing world and its cost-effective management. Journal of Circulation, 112(23), 3547–3553. https://doi.org/10.1161/CIRCULATIONAHA.105.591792

ITA. (2021). Country Commercial Guide: Tanzania – Healthcare. Retrieved August 3, 2022, from International Trade Administration https://www.trade.gov/country-commercial-guides/tanzania-healthcare

Kagaruki, G. B., Mayige, M. T., et al. (2015). Prevalence and risk factors of metabolic syndrome among individuals living with HIV and receiving antiretroviral treatment in Tanzania. British Journal of Medicine & Medical Research, 5(10), 1317–1327. https://doi.org/10.9734/BJMMR/2015/14455

Kazibwe, J., Tran, P. B., & Annerstedt, K. S. (2021). The household financial burden of non-communicable diseases in low- and middle-income countries: A systematic review. Health Research Policy and Systems, 19(1), 96. https://doi.org/10.1186/s12961-021-00732-y. PMID: 34154609; PMCID: PMC8215836.

Kyobutungi, C., Ziraba, A. K., Ezeh, A., et al. (2008). The burden of disease profile of residents of Nairobi’s slums: Results from a Demographic Surveillance System. Population Health Metrics, 6, 1. https://doi.org/10.1186/1478-7954-6-1

Mahal, A., Karan, A., & Engelgau, M. (2010). The economic implications of non-communicable disease for India. Health, Nutrition and Population (HNP) discussion paper. World Bank, Washington, World Bank. https://openknowledge.worldbank.org/handle/10986/13649

Mariara, J., Mwabu, D., & Ndeng’e, G. (2018). The consequences of fertility for child health in Kenya; endogeneity, heterogeneity and the control function approach. AERC. Retrieved January 31, 2022, from https://aercafrica.org/wp-content/uploads/2018/07/RH_06_Kenya_Mariara.pdf

Marshall, D. C., Al Omari, O., Goodall, R., et al. (2022). Trends in prevalence, mortality, and disability-adjusted life-years relating to chronic obstructive pulmonary disease in Europe: An observational study of the global burden of disease database, 2001–2019. BMC Pulmonary Medicine, 22, 289 (2022). https://doi.org/10.1186/s12890-022-02074-z

Mwai, D., & Muriithi, M. (2015). Non-communicable diseases risk factors and their contribution to NCD incidences in Kenya. European Scientific Journal, ESJ, 11(30). Retrieved April 1, 2022, from https://eujournal.org/index.php/esj/article/view/6367

Narayan, K. M., & Donnenfeld, Z. (2016). Envisioning a healthy future. Africas Shifting Burden of Disease. https://doi.org/10.2139/ssrn.2860539

O’Donnell, O, E. van Doorslaer, et al, (2005). Explaining the incidence of catastrophic expenditures on health care: Comparative evidence from Asia. Health Economics, 16, 1159–1184 (2007). https://doi.org/10.1002/hec.1209

Onoka, C. A., Onwujekwe, O. E., Hanson, K., & Uzochukwu, B. S. (2011). Examining catastrophic health expenditures at variable thresholds using household consumption expenditure diaries. Tropical Medicine & International Health, 2011(14), 1334–1341.

Ritchie, H., & Roser, M. (2018). Causes of Death. Published online at OurWorldInData.org. Retrieved from https://ourworldindata.org/causes-of-death. Accessed 19 Jan 2022.

Su, T. T., Kouyate, B., & Flessa, S. (2006). Catastrophic household expenditure for health care in a low-income society: A study from Nouna District. Burkina Faso Bull World Health Organ., 2006(84), 21–27.

van Doorslaer, E., O’Donnell, O., Rannan-Eliya, R. P., Somanathan, A., Adhikari, S. R., Garg, C. C., Harbianto, D., Herrin, A. N., Huq, M. N., Ibragimova, S., et al. (2006). Effect of payments for health care on poverty estimates in 11 countries in Asia: An analysis of household survey data. Lancet, 2006(368), 1357–1364. https://doi.org/10.1016/S0140-6736(06)69560-3

Wagstaff, A., Flores, G., Hsu, J., Smitz, M. F., Chepynoga, K., Buisman, L. R., van Wilgenburg, K., & Eozenou, P. (2018). Progress on catastrophic health spending in 133 countries: A retrospective observational study. The Lancet. Global Health, 6(2), e169–e179. https://doi.org/10.1016/S2214-109X(17)30429-1

Wamai, R. G., Kengne, A. P., & Levitt, N. (2018). Non-communicable diseases surveillance: Overview of magnitude and determinants in Kenya from STEPwise approach survey of 2015. BMC Public Health, 18, 1224. https://doi.org/10.1186/s12889-018-6051-z

WHO. (2019). Countries are spending more on health; but people are still paying too much out of their own pockets. Retrieved August 2, 2022, from https://www.who.int/news/item/20-02-2019-countries-are-spending-more-on-health-but-people-are-still-paying-too-much-out-of-their-own-pockets

WHO. (2020). Global spending on health: Weathering the storm. https://www.who.int/publications/i/item/9789240017788. Accessed 22 Jan 2022.

WHO. (2022). Deaths from noncommunicable diseases on the rise in Africa. Retrieved August 2, 2022, from https://www.afro.who.int/news/deaths-noncommunicable-diseases-rise-africa

Xu, D., Evans, K., & Murray, C. (2003). Household catastrophic health expenditure: A multi-country analysis. The Lancet, 362(July 12), 111–117. https://doi.org/10.1016/S0140-6736(03)13861-5

Xu, K., Evans, D. B., Carrin, G., Aguilar-Rivera, A. M., Musgrove, P., & Evans, T. (2007). Protecting households from catastrophic health spending. Health Aff (millwood), 2007(26), 972–983. https://doi.org/10.1377/hlthaff.26.4.972

Xu, K., Evans, D. B., Kadama, P., Nabyonga, J., Ogwal, P. O., Nabukhonzo, P., & Aguilar, A. M. (2006). Understanding the impact of eliminating user fees: Utilization and catastrophic health expenditures in Uganda. Social Science and Medicine, 2006(62), 866–876. https://doi.org/10.1016/j.socscimed.2005.07.004

Young, D. (2015). Alcohol consumption, beverage prices and measurement error. Journal of Studies on Alcohol, 64(2), 235–238. https://doi.org/10.15288/jsa.2003.64.235

Acknowledgements

The authors would like to thank Hon. Hussein Mohammed Bashe (MP), a minister of Agriculture in the United Republic of Tanzania, for his greater support during the persuasion of this study. His love and passion for scholarly works is highly appreciated.

Author information

Authors and Affiliations

Contributions

All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics Approval and Consent to Participate

Not applicable.

Consent for Publication

Not applicable.

Conflict of Interests

The authors declare no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Kitole, F.A., Lihawa, R.M. & Mkuna, E. Comparative Analysis on Communicable and Non-Communicable Diseases on Catastrophic Spending and Impoverishment in Tanzania. Glob Soc Welf 11, 123–134 (2024). https://doi.org/10.1007/s40609-022-00241-y

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40609-022-00241-y