Abstract

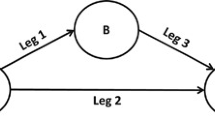

We consider the problem of optimally allocating the seats on a single flight leg to the demands from multiple fare classes that arrive sequentially. It is well-known that the optimal policy for this problem is characterized by a set of protection levels. In this paper, we develop a new stochastic approximation method to compute the optimal protection levels under the assumption that the demand distributions are not known and we only have access to the samples from the demand distributions. The novel aspect of our method is that it works with the nonsmooth version of the problem where the capacity can only be allocated in integer quantities. We show that the sequence of protection levels generated by our method converges to a set of optimal protection levels with probability one. We discuss applications to the case where the demand information is censored by the seat availability. Computational experiments indicate that our method is especially advantageous when the total expected demand exceeds the capacity by a significant margin and we do not have good a priori estimates of the optimal protection levels.

Similar content being viewed by others

References

Bashyam S, Fu MC (1998) Optimizaton of (s,S) inventory systems with random lead times and a service level constraint. Manage Sci 44(12): 243–256

Bertsekas DP, Tsitsiklis JN (1996) Neuro-dynamic programming. Athena Scientific, Belmont

Bertsimas D, de Boer S (2005) Simulation-based booking limits for airline revenue management. Oper Res 53(1): 90–106

Brumelle SL, McGill JI (1993) Airline seat allocation with multiple nested fare classes. Oper Res 41: 127–137

Curry RE (1990) Optimal airline seat allocation with fare classes nested by origins and destinations. Transp Sci 24: 193–204

Ermoliev Y (1988) Stochastic quasigradient methods. In: Ermoliev Y, Wets R(eds) Numerical techniques for stochastic optimization.. Springer, Berlin

Fu M (1994) Sample path derivatives for (s,S) inventory systems. Oper Res 42(2): 351–363

Glasserman P, Tayur S (1995) Sensitivity analysis for base-stock levels in multiechelon production-inventory systems. Manage Sci 41(2): 263–281

Huh WT, Rusmevichientong P (2006) Adaptive capacity allocation with censored demand data: application of concave umbrella functions, Technical report, Cornell University, School of Operations Research and Information Engineering

Huh WT, Levi R, Rusmevichientong P, Orlin JB (2008) Adaptive data-driven inventory control policies based on Kaplan–Meier estimator, Technical report, School of Operations Research and Information Engineering, Cornell University

Karaesmen I, van Ryzin G (2004) Overbooking with substitutable inventory classes. Oper Res 52(1): 83–104

Kunnumkal S, Topaloglu H (2008) Using stochastic approximation algorithms to compute optimal base-stock levels in inventory control problems. Oper Res 56(3): 646–664

Kushner HJ, Clark DS (1978) Stochastic approximation methods for constrained and unconstrained systems. Springer, Berlin

Lautenbacher CJ, Stidham S (1999) The underlying markov decision process in the single-leg airline yield management problem. Transp Sci 33: 136–146

L’Ecuyer P, Glynn P (1994) Stochastic optimization by simulation: Convergence proofs for the GI/G/1 queue in steady state. Manage Sci 40: 1245–1261

Lee T, Hersh M (1993) A model for dynamic airline seat inventory control with multiple seat bookings. Transp Sci 27: 252–265

Littlewood K (1972) Forecasting and control of passengers. In: Proceedings of the 12th AGIFORS, New York, pp 95–117

Mahajan S, van Ryzin G (2001) Stocking retail assortments under dynamic customer substitution. Oper Res 49(3): 334–351

Robinson L (1995) Optimal and approximate control policies for airline booking with sequential nonmonotonic fare classes. Oper Res 43: 252–263

Talluri KT, van Ryzin GJ (2004) The theory and practice of revenue management. Kluwer, Dordrecht

Topaloglu H (2008) A stochastic approximation method to compute bid prices in network revenue management problems. INFORMS J Comput 20(4): 596–610

van Ryzin G, McGill J (2000) Revenue management without forecasting or optimization: An adaptive algorithm for determining airline seat protection levels. Manage Sci 46(6): 760–775

van Ryzin G, Vulcano G (2008a) Computing virtual nesting controls for network revenue management under customer choice behavior. Manuf Serv Oper Manage 10(3): 448–467

van Ryzin G, Vulcano G (2008b) Simulation-based optimization of virtual nesting controls for network revenue management. Oper Res 56(4): 865–880

Wollmer RD (1992) An airline seat management model for a single leg route when lower fare classes book first. Oper Res 40: 26–37

Zinkevich M (2003) Online convex programming and generalized infinitesimal gradient ascent. In: Proceedings of the Twentieth International Conference on Machine Learning (ICML-2003). Washington, DC

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Kunnumkal, S., Topaloglu, H. A stochastic approximation method for the single-leg revenue management problem with discrete demand distributions. Math Meth Oper Res 70, 477–504 (2009). https://doi.org/10.1007/s00186-008-0278-x

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00186-008-0278-x