Summary

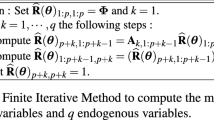

It is well known how, for an ARMA process of order (p 0,q 0), max (p 0,q 0) may be recursively estimatedHannan/Rissanen. Assuming max (p 0,q 0) to be known and, in addition,p 0≥q 0, a simple procedure for the recursive estimation of (p 0,q 0) is presented.

Similar content being viewed by others

References

Durbin, J.: The Fitting of Time Series Models. Revue de l'Institut International de Statistique28, 1960, 233–244.

Findley, D.F.: Geometrical and Lattice Versions of Levinson's General Algorithm, in D.F. Findley (ed.), Applied Time Series Analysis II, Academic Press, 1981.

Hannan, E.J., andJ. Rissanen: Recursive Estimation of Mixed Autoregressive-Moving Average Order. Biometrika67, 1982, 81–94.

Levinson, N.: The Wiener RMS (Root-Mean-Square) Error Criterion in Filter Design and Prediction. Journal of Mathematical Physics25, 1947, 261–278.

Whittle, P.: On Fitting of Multivariate Autoregressions, and the Approximate Canonical Factorisation of a Spectral Density Matrix. Biometrika50, 1963, 129–134.

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Reschenhofer, E. A remark on the recursive estimation of ARMA order. Metrika 32, 93–96 (1985). https://doi.org/10.1007/BF01897804

Received:

Issue Date:

DOI: https://doi.org/10.1007/BF01897804